|

市場調查報告書

商品編碼

1684199

消毒機器人市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Disinfection Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

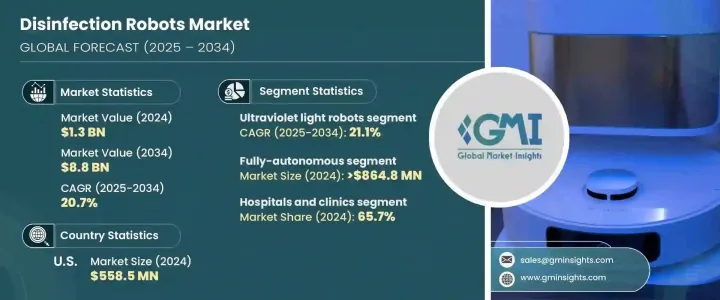

2024 年全球消毒機器人市場規模達到 13 億美元,預計 2025 年至 2034 年期間複合年成長率將達到驚人的 20.7%。 這種快速成長反映了人們對感染控制意識的不斷提高、持續的勞動力短缺、成本效率以及對永續、無化學消毒方法的高度關注。 COVID-19 疫情凸顯了維持嚴格衛生標準的重要性,從而推動醫療保健、旅館業和公共場所採用先進的消毒解決方案。

在機器人和人工智慧技術進步的推動下,自動化轉型進一步增強了對創新消毒機器人的需求,這些機器人可以在減少人為干預的同時提供卓越的清潔效果。隨著各組織努力滿足嚴格的消毒標準並確保人員和客戶的安全,預計未來幾年市場將見證強勁的投資和創新。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 88億美元 |

| 複合年成長率 | 20.7% |

根據產品類型,市場分為紫外線機器人、過氧化氫蒸氣(HPV)機器人和其他機器人。預計紫外線機器人將佔據市場主導地位,以驚人的 21.1% 的複合年成長率成長,到 2034 年將達到 56 億美元。這項尖端技術提供了一種快速、高效且環保的解決方案,可在幾分鐘內實現高達 99.99% 的消毒效果。紫外線機器人因其能夠持續可靠地消除病原體而受到各行各業的青睞,是傳統清潔方法的更好替代方案。

在技術方面,全自動和半自動機器人推動了市場的創新。全自動消毒機器人在 2024 年創造了 8.648 億美元的市場價值,它能夠最大限度地減少對人工的依賴,從而徹底改變感染控制方式。這些機器人連續運行,停機時間極短,確保在不同環境中持續有效率地進行清潔。配備先進的人工智慧 (AI) 導航系統和 LiDAR 測繪技術,全自動機器人可以識別目標區域、繞過障礙物,甚至對最複雜和難以進入的空間進行消毒。這種能力使得它們在醫院、機場和公共交通樞紐等高風險環境中特別有價值。

美國消毒機器人市場在 2024 年創造了 5.585 億美元的產值,預計到 2034 年將以 19.1% 的強勁複合年成長率成長。這些感染會導致住院時間更長且醫療費用更高,促使醫療機構採用利用 UV-C 光和 HPV 技術的消毒機器人。具有最先進導航、人工智慧功能和即時報告功能的全自動機器人越來越受到青睞,以解決勞動力短缺問題並維持整個醫療保健行業嚴格的清潔標準。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 醫院內感染發生率高

- 產品技術進步

- 疫情過後,醫療機構衛生與個人衛生相關支出增加

- 產業陷阱與挑戰

- 產品成本高

- 成長動力

- 成長潛力分析

- 監管格局

- 報銷場景

- 定價分析

- 技術格局

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 紫外線機器人

- 過氧化氫蒸氣(HPV)機器人

- 其他產品類型

第6章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 完全自主

- 半自主

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院和診所

- 門診手術中心 (ASC)

- 製藥和生物技術設施

- 其他最終用戶

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ADIBOT

- akara

- ATEAGO

- bioquell

- BLUE OCEAN ROBOTICS

- BRIDGEPORT MAGNETICS

- Finsen TECH

- Jetbrain

- Mediland Enterprise

- mILAGROW

- OTSAW

- skytron

- TMirob

- Tru-D

- XENEX

The Global Disinfection Robots Market reached USD 1.3 billion in 2024 and is projected to expand at an impressive CAGR of 20.7% between 2025 and 2034. This rapid growth reflects increasing awareness around infection control, ongoing labor shortages, cost efficiency, and a heightened focus on sustainable, chemical-free disinfection methods. The COVID-19 pandemic has underscored the critical importance of maintaining stringent hygiene standards, thus pushing healthcare, hospitality, and public spaces to adopt advanced disinfection solutions.

The shift towards automation, driven by technological advancements in robotics and artificial intelligence, has further bolstered the demand for innovative disinfection robots that provide superior cleaning outcomes while reducing human intervention. As organizations strive to meet rigorous disinfection standards and ensure the safety of personnel and customers, the market is expected to witness robust investment and innovation in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 20.7% |

By product type, the market is segmented into ultraviolet light robots, hydrogen peroxide vapor (HPV) robots, and others. Ultraviolet light robots are anticipated to dominate the market, growing at a remarkable CAGR of 21.1% and reaching USD 5.6 billion by 2034. These robots leverage UV-C technology, which effectively inactivates a broad spectrum of microorganisms by damaging their genetic material, preventing replication. This cutting-edge technology offers a fast, efficient, and environmentally friendly solution, achieving up to 99.99% disinfection within minutes. Ultraviolet light robots are increasingly preferred across industries for their ability to deliver consistent and reliable pathogen elimination, presenting a superior alternative to traditional cleaning methods.

In terms of technology, fully autonomous and semi-autonomous robots drive innovation in the market. Fully autonomous disinfection robots, which generated USD 864.8 million in 2024, are revolutionizing infection control with their ability to minimize reliance on manual labor. These robots operate continuously with minimal downtime, ensuring consistent and efficient cleaning in diverse settings. Equipped with advanced artificial intelligence (AI) navigation systems and LiDAR mapping technologies, fully autonomous robots can identify target areas, navigate obstacles, and disinfect even the most complex and hard-to-access spaces. This capability makes them particularly valuable in high-risk environments such as hospitals, airports, and public transportation hubs.

The U.S. disinfection robots market generated USD 558.5 million in 2024 and is expected to grow at a robust CAGR of 19.1% through 2034. The high prevalence of healthcare-associated infections (HAIs) in the country has accelerated the adoption of advanced disinfection solutions. These infections lead to longer hospital stays and higher medical costs, prompting healthcare facilities to embrace disinfection robots that utilize UV-C light and HPV technologies. Fully autonomous robots with state-of-the-art navigation, AI capabilities, and real-time reporting are increasingly favored to address labor shortages and maintain stringent cleaning standards across the healthcare sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High incidence of hospital-acquired infections

- 3.2.1.2 Technological advancements in products

- 3.2.1.3 Rise in sanitation and hygiene related spending in healthcare settings post-pandemic

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High product cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Pricing analysis

- 3.7 Technology landscape

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 — 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Ultraviolet light robots

- 5.3 Hydrogen peroxide vapor (HPV) robots

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 — 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fully-autonomous

- 6.3 Semi-autonomous

Chapter 7 Market Estimates and Forecast, By End Use, 2021 — 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Pharmaceutical and biotechnology facilities

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 — 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ADIBOT

- 9.2 akara

- 9.3 ATEAGO

- 9.4 bioquell

- 9.5 BLUE OCEAN ROBOTICS

- 9.6 BRIDGEPORT MAGNETICS

- 9.7 Finsen TECH

- 9.8 Jetbrain

- 9.9 Mediland Enterprise

- 9.10 mILAGROW

- 9.11 OTSAW

- 9.12 skytron

- 9.13 TMirob

- 9.14 Tru-D

- 9.15 XENEX

消毒機器人市場報告,按產品類型(紫外線消毒機器人、過氧化氫汽化機器人等)、技術、最終用戶和地區分類,2025 年至 2033 年

消毒機器人市場報告,按產品類型(紫外線消毒機器人、過氧化氫汽化機器人等)、技術、最終用戶和地區分類,2025 年至 2033 年 消毒機器人市場:依產品類型、依最終用戶、依地區

消毒機器人市場:依產品類型、依最終用戶、依地區 消毒機器人市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、最終用途、地區和競爭細分,2020-2030F

消毒機器人市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、最終用途、地區和競爭細分,2020-2030F 消毒機器人:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)消毒機器人市場規模、佔有率、成長分析,按類型、技術、最終用途、地區 - 產業預測,2025-2032全球環境消毒機器人市場:依產品類型、最終用戶、技術、應用、銷售管道、維修服務類型 - 2025-2030 年預測

消毒機器人:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)消毒機器人市場規模、佔有率、成長分析,按類型、技術、最終用途、地區 - 產業預測,2025-2032全球環境消毒機器人市場:依產品類型、最終用戶、技術、應用、銷售管道、維修服務類型 - 2025-2030 年預測 全球消毒機器人市場

全球消毒機器人市場 消毒機器人市場:全球產業分析,規模,佔有率,成長,趨勢,2024-2033年預測2024年消毒機器人全球市場報告消毒機器人市場規模、佔有率和趨勢分析報告:按類型、按技術、按最終用途、按地區、細分市場預測,2024-2030年

消毒機器人市場:全球產業分析,規模,佔有率,成長,趨勢,2024-2033年預測2024年消毒機器人全球市場報告消毒機器人市場規模、佔有率和趨勢分析報告:按類型、按技術、按最終用途、按地區、細分市場預測,2024-2030年