|

市場調查報告書

商品編碼

1684793

高速資料轉換器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測High-speed Data Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

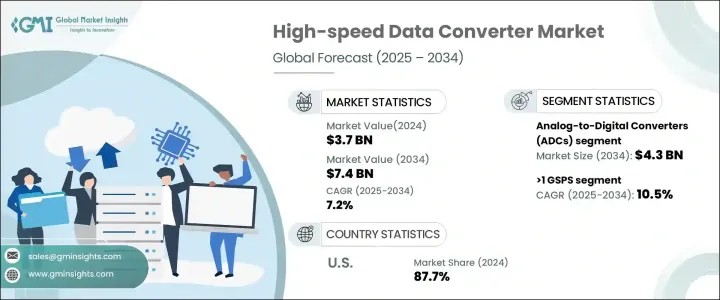

2024 年全球高速數據轉換器市場價值為 37 億美元,預計 2025 年至 2034 年的複合年成長率為 7.2%。這一成長是由 5G 技術和下一代通訊網路的快速發展所推動的,這推動了對高速資料轉換器的需求。這些設備對於高效的訊號傳輸和處理至關重要,使其成為現代電信基礎設施中不可或缺的一部分。隨著各行各業努力滿足對更高資料速率和更低延遲日益成長的需求,高速資料轉換器在確保無縫連接和最佳效能方面發揮關鍵作用。

市場也受益於這些轉換器在電信、工業自動化和汽車等領域的日益普及,因為即時資料處理和系統效率至關重要。此外,向節能和高解析度組件的轉變正在加速先進資料轉換器的發展,以滿足高科技應用對速度和準確性日益成長的需求。物聯網設備整合度不斷提高,再加上人工智慧和機器學習的進步,進一步增加了對高速資料轉換器的需求,因為這些技術嚴重依賴精確、高效的資料處理。半導體技術的不斷創新也支持了市場的成長軌跡,這使得生產更緊湊、更節能、更高性能的轉換器成為可能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 37億美元 |

| 預測值 | 74億美元 |

| 複合年成長率 | 7.2% |

市場按類型細分,主要類別為類比數位轉換器 (ADC) 和數位類比轉換器 (DAC)。隨著對類比訊號精確數位化的需求不斷成長,ADC 的市場規模預計到 2034 年將達到 43 億美元。需要即時資料轉換的行業正在推動具有更低功耗和更高解析度的高效能 ADC 的發展。這些轉換器對於需要高速資料處理的應用至關重要,使其成為不斷發展的數位生態系統的基石。隨著各行各業尋求提高各種應用中訊號轉換的品質和效率,對 DAC 的需求也不斷增加。

根據頻段,市場分為 125 MSPS、125 MSPS 至 1 GSPS 和 >1 GSPS。預計 >1 GSPS 部分將以最快的速度成長,預測期內預計複合年成長率為 10.5%。這種成長歸因於高階應用中對高速資料處理的需求不斷增加。同時,125 MSPS 至 1 GSPS 段由於其性能和功率效率的平衡仍然是一個受歡迎的選擇。汽車、衛星通訊和中端電信等行業正在推動這些轉換器的採用,因為它們增強了網路功能並支援中等位元率。

受5G基礎設施的快速擴張、半導體領域的強勁需求以及物聯網服務的廣泛採用的推動,美國在2024年佔據了高速資料轉換器市場的87.7%。對國防和航太應用的日益關注也促進了對高性能資料轉換器的需求不斷成長。行業領導企業之間的策略合作正在促進創新和研究,進一步推動市場的成長。隨著技術進步和基礎設施發展為高速資料轉換器創造新的機遇,美國市場的主導地位預計將繼續保持。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 高速通訊網路的需求不斷增加

- 以數據為中心的應用程式的成長

- 不斷擴大的消費性電子產品市場

- 汽車電子的進步

- 軟體定義無線電 (SDR) 的採用日益增多

- 產業陷阱與挑戰

- 設計複雜度高,製造成本高

- 科技快速發展,產品生命週期短

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 類比數位轉換器 (ADC)

- 數位類比轉換器 (DAC)

第6章:市場估計與預測:依決議,2021 年至 2034 年

- 主要趨勢

- 8 位元

- 10 位元

- 12 位元

- 16 位元

- 24 位元及以上

第 7 章:市場估計與預測:按頻段,2021-2034 年

- 主要趨勢

- <125 MSPS

- 125 MSPS 至 1 GSPS

- >1 GSPS

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 汽車

- 電信

- 工業的

- 測試與管理

- 衛生保健

- 消費性電子產品

- 其他

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- IQ-ANALOG

- Advanced Micro Devices, Inc.

- Analog Devices, Inc.

- Asahi Kasei Microdevices Corporation

- Avia Semiconductor Ltd.

- Broadcom Inc.

- Datel, Inc.

- Faraday Technology Corporation

- GlobalSpec

- Infineon Technologies AG

- Microchip Technology Inc.

- Monolithic Power Systems, Inc.

- Mouser Electronics, Inc.

- NXP Semiconductors

- ON Semiconductor

- Qualcomm Technologies, Inc.

- Renesas Electronics Corporation

- ROHM Semiconductor

- STMicroelectronics

- Texas Instruments

The Global High-Speed Data Converter Market, valued at USD 3.7 billion in 2024, is expected to grow at a CAGR of 7.2% from 2025 to 2034. This growth is driven by the rapid evolution of 5G technology and next-generation communication networks, which are fueling the demand for high-speed data converters. These devices are critical for efficient signal transmission and processing, making them indispensable in modern telecommunications infrastructure. As industries strive to meet the increasing need for higher data rates and lower latency, high-speed data converters are playing a pivotal role in ensuring seamless connectivity and optimal performance.

The market is also benefiting from the growing adoption of these converters in sectors such as telecommunications, industrial automation, and automotive, where real-time data processing and system efficiency are paramount. Additionally, the shift toward energy-efficient and high-resolution components is accelerating the development of advanced data converters, which cater to the rising demand for speed and accuracy in high-tech applications. The increasing integration of IoT devices, coupled with advancements in artificial intelligence and machine learning, is further amplifying the need for high-speed data converters, as these technologies rely heavily on precise and efficient data processing. The market's growth trajectory is also supported by ongoing innovations in semiconductor technology, which are enabling the production of more compact, energy-efficient, and high-performance converters.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 7.2% |

The market is segmented by type, with Analog-to-Digital Converters (ADCs) and Digital-to-Analog Converters (DACs) being the primary categories. ADCs are projected to reach USD 4.3 billion by 2034, driven by the increasing demand for accurate digitalization of analog signals. Industries requiring real-time data conversion are pushing the development of high-performance ADCs that offer lower power consumption and enhanced resolution. These converters are essential for applications that demand high-speed data processing, making them a cornerstone of the evolving digital ecosystem. The demand for DACs is also rising as industries seek to improve the quality and efficiency of signal conversion in various applications.

Based on frequency bands, the market is divided into 125 MSPS, 125 MSPS to 1 GSPS, and >1 GSPS. The >1 GSPS segment is expected to grow at the fastest rate, with a projected CAGR of 10.5% during the forecast period. This growth is attributed to the increasing need for high-speed data processing in advanced applications. Meanwhile, the 125 MSPS to 1 GSPS segment remains a popular choice due to its balance of performance and power efficiency. Industries such as automotive, satellite communications, and mid-range telecommunications are driving the adoption of these converters as they enhance network capabilities and support moderate bit rates.

The United States held an 87.7% share of the high-speed data converter market in 2024, driven by the rapid expansion of 5G infrastructure, strong demand in the semiconductor sector, and the widespread adoption of IoT services. The growing focus on defense and aerospace applications is also contributing to the rising demand for high-performance data converters. Strategic collaborations among leading industry players are fostering innovation and research, further propelling the market's growth. The US market's dominance is expected to continue as advancements in technology and infrastructure development create new opportunities for high-speed data converters.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for high-speed communication networks

- 3.6.1.2 Growth in data-centric applications

- 3.6.1.3 Expanding consumer electronics market

- 3.6.1.4 Advancements in automotive electronics

- 3.6.1.5 Rising adoption of Software-Defined Radios (SDRs)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High design complexity and manufacturing costs

- 3.6.2.2 Rapid technological evolution and short product lifecycles

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Analog-to-Digital Converters (ADCs)

- 5.3 Digital-to-Analog Converters (DACs)

Chapter 6 Market Estimates & Forecast, By Resolution, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 8-bit

- 6.3 10-bit

- 6.4 12-bit

- 6.5 16-bit

- 6.6 24-bit and above

Chapter 7 Market Estimates & Forecast, By Frequency Band, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 <125 MSPS

- 7.3 125 MSPS TO 1 GSPS

- 7.4 >1 GSPS

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Telecommunications

- 8.4 Industrial

- 8.5 Test & management

- 8.6 Healthcare

- 8.7 Consumer Electronics

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 IQ-ANALOG

- 10.2 Advanced Micro Devices, Inc.

- 10.3 Analog Devices, Inc.

- 10.4 Asahi Kasei Microdevices Corporation

- 10.5 Avia Semiconductor Ltd.

- 10.6 Broadcom Inc.

- 10.7 Datel, Inc.

- 10.8 Faraday Technology Corporation

- 10.9 GlobalSpec

- 10.10 Infineon Technologies AG

- 10.11 Microchip Technology Inc.

- 10.12 Monolithic Power Systems, Inc.

- 10.13 Mouser Electronics, Inc.

- 10.14 NXP Semiconductors

- 10.15 ON Semiconductor

- 10.16 Qualcomm Technologies, Inc.

- 10.17 Renesas Electronics Corporation

- 10.18 ROHM Semiconductor

- 10.19 STMicroelectronics

- 10.20 Texas Instruments

電阻器數位轉換器市場按產品類型、解析度、設備類型和應用分類 - 2025-2030 年全球預測

電阻器數位轉換器市場按產品類型、解析度、設備類型和應用分類 - 2025-2030 年全球預測 2025年高速資料轉換器全球市場報告

2025年高速資料轉換器全球市場報告 2025年資料據轉換器全球市場報告

2025年資料據轉換器全球市場報告 全球資料轉換器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球資料轉換器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 資料轉換器市場規模、佔有率、成長分析(按類型、按採樣率、按應用、按地區)- 產業預測,2025 年至 2032 年

資料轉換器市場規模、佔有率、成長分析(按類型、按採樣率、按應用、按地區)- 產業預測,2025 年至 2032 年 高速資料轉換器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、技術、資料速率、最終用戶產業、地區和競爭細分,2020-2030 年

高速資料轉換器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品類型、技術、資料速率、最終用戶產業、地區和競爭細分,2020-2030 年 資料轉換器 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

資料轉換器 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球資料轉換器市場:按類型、取樣率、解析度、產業 - 預測 2025-2030

全球資料轉換器市場:按類型、取樣率、解析度、產業 - 預測 2025-2030 全球類比數位轉換器市場:按產品、解析度、應用和最終用途產業 - 預測 2025-2030 年

全球類比數位轉換器市場:按產品、解析度、應用和最終用途產業 - 預測 2025-2030 年 高速資料轉換器的全球市場:按類型、頻寬和應用分類 - 2025-2030 年預測

高速資料轉換器的全球市場:按類型、頻寬和應用分類 - 2025-2030 年預測