|

市場調查報告書

商品編碼

1685143

第三方物流 (3PL) 市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Third-Party Logistics (3PL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

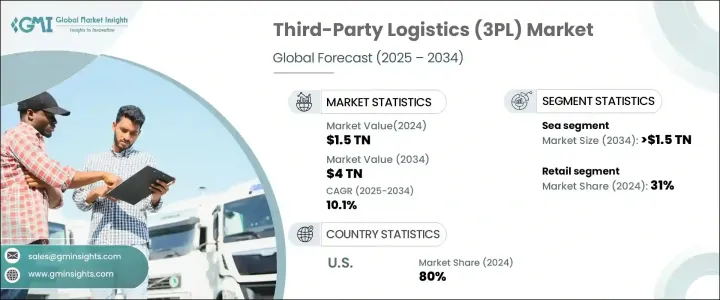

2024 年全球第三方物流市場價值為 1.5 兆美元,預計 2025 年至 2034 年期間的複合年成長率為 10.1%。隨著全球企業面臨不斷成長的訂單量和對更快、更可靠的物流解決方案的需求,這種快速成長是由零售和電子商務領域不斷成長的需求所推動的。網上購物的激增加劇了競爭,迫使企業在管理複雜的供應鏈的同時提高效率。因此,越來越多的企業開始向第三方物流供應商尋求可擴展的物流解決方案,以適應不斷變化的消費者需求和不斷發展的零售趨勢。

除了蓬勃發展的電子商務領域之外,全球供應鏈和跨境貿易的擴張也進一步推動了對複雜物流管理的需求。企業面臨著簡化分銷網路和提高營運效率的持續壓力,因此外包成為一種策略性措施。隨著對最後一哩交付、倉儲和履行中心的日益重視,第三方物流提供者成為確保無縫物流營運的重要合作夥伴。利用第三方專業知識的能力有助於企業降低管理費用、縮短交貨時間並最佳化庫存管理。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.5兆美元 |

| 預測值 | 4兆美元 |

| 複合年成長率 | 10.1% |

技術進步在第三方物流市場擴張中也扮演關鍵角色。資料分析的整合使物流供應商能夠更準確地預測需求波動、最佳化路線並提高營運透明度。即時追蹤系統、自動化和人工智慧驅動的解決方案正在改變供應鏈管理,使物流營運更加靈敏和適應性更強。隨著企業努力提高客戶滿意度,這些尖端技術的採用使得 3PL 服務更具吸引力,並且對於現代供應鏈策略而言變得不可或缺。

市場依運輸方式細分,包括空運、海運、鐵路和公路。海運業在 2024 年佔據了 35% 的市場佔有率,預計到 2034 年將創造 1.5 兆美元的市場價值。隨著全球貿易的不斷擴大,海運因其成本效益和處理大量貨物的能力仍然是長途運輸的首選方式。航運是國際貿易的重要組成部分,特別是對於原料和製成品的大宗運輸而言。隨著全球化的不斷發展以及對高效供應鏈營運的需求不斷成長,企業嚴重依賴海上物流來實現無縫且具成本效益的貿易。

第三方物流市場也按應用進行細分,零售業將在 2024 年佔據 31% 的市場佔有率。隨著供應鏈變得越來越複雜,零售商正在利用 3PL 服務來最佳化國內和國際分銷。消費者對更快、更可靠的配送的期望不斷上升,促使企業與提供端到端物流解決方案(從倉儲到最後一英里配送)的第三方物流供應商合作。透過外包物流業務,零售商可以專注於核心業務活動,同時確保無縫供應鏈執行。

2024 年,美國第三方物流市場佔了 80% 的市佔率。對降低成本和供應鏈最佳化日益重視,推動企業將其物流職能的外包。各行各業的公司都在與第三方物流供應商合作,以簡化營運、提高效率並利用物流專業知識。隨著電子商務的不斷擴張、物流解決方案的先進以及數位轉型的強力推動,美國對第三方物流服務的需求預計將保持強勁,從而鞏固市場的上升軌跡。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 第三方物流供應商

- 托運人

- 承運商

- 倉庫和配送中心

- 技術提供者

- 最終客戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞及舉措

- 監管格局

- 親子市場分析

- 衝擊力

- 成長動力

- 零售和電子商務行業的快速擴張

- 自動化、人工智慧和資料分析的進步

- 貿易和跨境運輸的全球化

- 政府措施促進市場成長

- 產業陷阱與挑戰

- 缺乏物流控制

- 跨境運輸相關風險

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按解決方案,2021 - 2034 年

- 主要趨勢

- 專用合約運輸(DCC)

- 專用運輸管理 (DTM)

- 國際運輸管理(ITM)

- 倉儲和配送

- 物流軟體

第6章:市場估計與預測:按模式,2021 - 2034 年

- 主要趨勢

- 空氣

- 海

- 鐵路和公路

第 7 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 食品和飲料

- 衛生保健

- 零售

- 汽車

- 製造業

- 其他

第 8 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 俄羅斯

- 西班牙

- 荷蘭

- 瑞士

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 印尼

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

- 土耳其

第9章:公司簡介

- AmeriCold Logistics

- BDP International

- Burris Logistics

- CH Robinson

- DB Schenker

- DHL

- DSV

- Echo

- Expeditors

- FedEx

- GEODIS

- JB Hunt

- Kintetsu

- Kuehne + Nagel

- Nippon

- Penske Logistics

- SinoTrans

- Total Quality Logistics

- UPS

- XPO

The Global Third-Party Logistics Market was valued at USD 1.5 trillion in 2024 and is projected to expand at a CAGR of 10.1% between 2025 and 2034. This rapid growth is driven by the increasing demand in retail and e-commerce sectors, as businesses worldwide face rising order volumes and the need for faster, more reliable logistics solutions. The surge in online shopping has intensified competition, pushing companies to enhance efficiency while managing complex supply chains. As a result, more businesses are turning to 3PL providers for scalable logistics solutions that can adapt to fluctuating consumer demands and evolving retail trends.

Beyond the booming e-commerce landscape, the expansion of global supply chains and cross-border trade is further fueling the need for sophisticated logistics management. Companies are under constant pressure to streamline their distribution networks and improve operational efficiency, making outsourcing a strategic move. With a growing emphasis on last-mile delivery, warehousing, and fulfillment centers, 3PL providers are essential partners in ensuring seamless logistics operations. The ability to leverage third-party expertise helps businesses reduce overhead costs, improve delivery timelines, and optimize inventory management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Trillion |

| Forecast Value | $4 Trillion |

| CAGR | 10.1% |

Technological advancements are also playing a pivotal role in the expansion of the 3PL market. The integration of data analytics enables logistics providers to predict demand fluctuations more accurately, optimize routes, and enhance operational transparency. Real-time tracking systems, automation, and artificial intelligence-driven solutions are transforming supply chain management, making logistics operations more responsive and adaptable. As businesses strive to enhance customer satisfaction, the adoption of these cutting-edge technologies is making 3PL services more attractive and indispensable for modern supply chain strategies.

The market is segmented by mode of transport, including air, sea, and rail & road. The sea transportation segment accounted for 35% of the market share in 2024 and is expected to generate USD 1.5 trillion by 2034. As global trade continues to expand, sea freight remains the preferred method for long-distance transportation due to its cost-effectiveness and ability to handle large cargo volumes. Shipping is a crucial component of international trade, particularly for bulk shipments of raw materials and manufactured goods. With increasing globalization and the growing need for efficient supply chain operations, businesses are heavily relying on maritime logistics for seamless and cost-efficient trade.

The third-party logistics market is also segmented by application, with the retail sector holding 31% of the market share in 2024. As supply chains grow in complexity, retailers are leveraging 3PL services to optimize both domestic and international distribution. The rising consumer expectations for faster and more reliable deliveries are prompting businesses to partner with 3PL providers that offer end-to-end logistics solutions, from warehousing to last-mile delivery. By outsourcing logistics operations, retailers can focus on core business activities while ensuring seamless supply chain execution.

The U.S. third-party logistics market captured 80% of the market share in 2024. The increasing emphasis on cost reduction and supply chain optimization is driving businesses to outsource their logistics functions. Companies across industries are partnering with 3PL providers to streamline operations, enhance efficiency, and leverage logistics expertise. With the continuous expansion of e-commerce, advanced logistics solutions, and a strong push toward digital transformation, the demand for third-party logistics services in the U.S. is expected to remain strong, reinforcing the market's upward trajectory.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 3PL providers

- 3.1.2 Shippers

- 3.1.3 Carriers

- 3.1.4 Warehouses and distribution centers

- 3.1.5 Technology providers

- 3.1.6 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Parent and child market analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 The rapid expansion of retail and e-commerce industry

- 3.9.1.2 Advancements in automation, AI, and data analytics

- 3.9.1.3 The globalization of trade and cross-border shipments

- 3.9.1.4 Government initiatives encouraging market growth

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Lack of logistics control

- 3.9.2.2 Risks associated with cross-border transportation

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Dedicated Contract Carriage (DCC)

- 5.3 Dedicated Transportation Management (DTM)

- 5.4 International Transportation Management (ITM)

- 5.5 Warehousing & distribution

- 5.6 Logistics software

Chapter 6 Market Estimates & Forecast, By Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Air

- 6.3 Sea

- 6.4 Rail & Road

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Healthcare

- 7.4 Retail

- 7.5 Automotive

- 7.6 Manufacturing

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Russia

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Switzerland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.5 South America

- 8.5.1 Brazil

- 8.5.2 Argentina

- 8.5.3 Colombia

- 8.5.4 Chile

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

- 8.6.4 Turkey

Chapter 9 Company Profiles

- 9.1 AmeriCold Logistics

- 9.2 BDP International

- 9.3 Burris Logistics

- 9.4 C.H. Robinson

- 9.5 DB Schenker

- 9.6 DHL

- 9.7 DSV

- 9.8 Echo

- 9.9 Expeditors

- 9.10 FedEx

- 9.11 GEODIS

- 9.12 J. B. Hunt

- 9.13 Kintetsu

- 9.14 Kuehne + Nagel

- 9.15 Nippon

- 9.16 Penske Logistics

- 9.17 SinoTrans

- 9.18 Total Quality Logistics

- 9.19 UPS

- 9.20 XPO

4P物流市場分析與2034年預測:類型、產品、服務、技術、應用、組件、部署、最終用戶、功能、解決方案5P物流市場分析及2034年預測:類型、產品、服務、技術、組件、應用、流程、部署、最終用戶、解決方案

4P物流市場分析與2034年預測:類型、產品、服務、技術、應用、組件、部署、最終用戶、功能、解決方案5P物流市場分析及2034年預測:類型、產品、服務、技術、組件、應用、流程、部署、最終用戶、解決方案 2025年第三方物流(3PL)全球市場報告

2025年第三方物流(3PL)全球市場報告 2025 年至 2033 年第三方化學品分銷市場按類型(大宗化學品、特種化學品)、應用(紡織、汽車和運輸、農業、製藥、工業製造等)和地區分類

2025 年至 2033 年第三方化學品分銷市場按類型(大宗化學品、特種化學品)、應用(紡織、汽車和運輸、農業、製藥、工業製造等)和地區分類 2025 年至 2029 年全球第三方化學品分銷

2025 年至 2029 年全球第三方化學品分銷 中國第三方物流(3PL) -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)英國第三方物流(3PL) -市場佔有率分析、產業趨勢與成長預測(2025-2030 年)全球港口服務市場:依類型、服務和地區預測至2032年

中國第三方物流(3PL) -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)英國第三方物流(3PL) -市場佔有率分析、產業趨勢與成長預測(2025-2030 年)全球港口服務市場:依類型、服務和地區預測至2032年 第三方物流市場規模、佔有率、按服務類型、運輸方式和地區的成長分析 - 按行業預測,2024-2031 年2025-2033 年日本 3PL 市場報告(按運輸、服務類型、最終用途和地區)

第三方物流市場規模、佔有率、按服務類型、運輸方式和地區的成長分析 - 按行業預測,2024-2031 年2025-2033 年日本 3PL 市場報告(按運輸、服務類型、最終用途和地區)