|

市場調查報告書

商品編碼

1685207

防火材料市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Fire Stopping Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

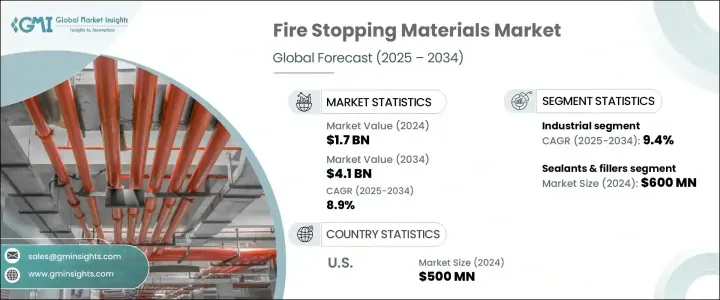

2024 年全球防火材料市場規模達到 17 億美元,預計將經歷強勁成長,2025 年至 2034 年的複合年成長率為 8.9%。推動這一市場擴張的幾個關鍵因素包括加強消防安全法規、建築活動激增以及全球城市化和工業化速度的加速。此外,防火技術的進步和消防安全意識的提高進一步推動了各行業對防火材料的需求。石油和天然氣、航太、海洋和資料中心等行業對這些材料的需求尤其突出,因為這些行業的營運風險較高,因此都有嚴格的消防安全要求。

儘管成長軌跡看好,但市場仍面臨重大挑戰。主要障礙之一是先進防火解決方案的成本高昂,這可能會阻礙其採用,尤其是對於中小型企業而言。不同地區之間監管框架不一致的問題也使製造商和最終用戶的合規工作變得複雜。供應鏈中斷和替代材料的競爭(可提供更低的初始成本)進一步增加了市場的複雜性。建築業放緩和技術勞動力持續短缺等經濟不確定性也對實現市場持續成長構成挑戰。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 17億美元 |

| 預測值 | 41億美元 |

| 複合年成長率 | 8.9% |

防火材料領域,特別是密封劑和填料類別,在 2024 年的市場規模為 6 億美元,預計到 2034 年的複合年成長率將達到 9.4%。密封劑和填料的創新是這一成長的關鍵,製造商不斷開發性能更強、更易於使用、更耐用的產品。膨脹型密封劑越來越受歡迎,因為它們在高溫下膨脹,能夠有效密封縫隙,防止火勢蔓延。防火砂漿也發揮著至關重要的作用,特別是在密封防火牆和地板上的電纜、管道和管子周圍的大開口時,從而滿足商業和工業環境中日益成長的防火需求。

工業部門在 2024 年佔據了防火材料市場的 49%,預計在 2025 年至 2034 年期間的複合年成長率為 9.4%。這一成長是由石油和天然氣設施、化工廠和製造基地等高風險環境中嚴格的消防安全法規所推動的。由於存在易燃化學品、氣體和重型機械,在這些操作中防止火勢蔓延至關重要。隨著這些行業的不斷擴大,對防火材料的需求只會增加。

在美國,防火材料市場在 2024 年創收 5 億美元,預計到 2034 年將以 9.2% 的複合年成長率成長。該國的成長歸因於更嚴格的消防安全標準、蓬勃發展的建築業以及被動防火技術的不斷進步。對改造、翻新和保護關鍵基礎設施的關注進一步支持了該地區市場的強勁上升趨勢。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算。

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 更嚴格的消防安全規定

- 建設、都市化和工業化進程加快

- 產業陷阱與挑戰

- 防火材料成本高

- 熟練勞動力不足

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 塗料

- 密封劑和填料

- 矽酮密封膠

- 丙烯酸密封劑

- 膨脹密封劑

- 其他(水泥填料等)

- 板材

- 礦棉板

- 膨脹板材

- 複合板

- 其他(石膏板等)

- 膩子和泡沫

- 膨脹膩子

- 防火泡沫

- 膨脹泡沫

- 其他(膩子墊等)

- 其他(項圈、火塊等)

第 6 章:市場估計與預測:按產品類型,2021-2034 年

- 主要趨勢

- 被動防火

- 主動防火

第 7 章:市場估計與預測:按防火等級,2021 年至 2034 年

- 主要趨勢

- 1小時額定

- 2 小時額定

- 3 小時額定

- 4 小時額定

- 額定時間超過 4 小時

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 電力

- 機械的

- 管道

- 其他

第 9 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 住宅

- 商業的

- 工業的

- 石油和天然氣

- 汽車

- 製造業

- 資料中心

- 其他(汽車、船等)

第 10 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直接銷售

- 間接銷售

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 12 章:公司簡介

- 3M

- Bostik

- Emseal Joint Systems

- Everkem

- Flame Stop

- Fosroc

- HB Fuller Company

- Hilti

- Promat

- RectorSeal

- Rockwool

- Sika

- Specified Technologies

- Tremco

- Unique Fire Stop Products

The Global Fire Stopping Materials Market reached USD 1.7 billion in 2024 and is projected to experience robust growth, with a CAGR of 8.9% from 2025 to 2034. Several key factors are driving this market expansion, including tightening fire safety regulations, a surge in construction activities, and the increasing rate of urbanization and industrialization worldwide. Additionally, advancements in fire stopping technologies and heightened awareness surrounding fire safety further fuel the demand for fire stopping materials across various sectors. The need for these materials is especially prominent in industries such as oil and gas, aerospace, marine, and data centers, all of which have strict fire safety requirements due to the high-risk nature of their operations.

Despite the promising growth trajectory, the market faces significant challenges. One of the primary hurdles is the high cost associated with advanced fire stopping solutions, which can inhibit adoption, particularly for small and medium-sized enterprises. There is also the issue of inconsistent regulatory frameworks across different regions, which complicates compliance for manufacturers and end-users alike. Supply chain disruptions and competition from alternative materials, which can offer lower initial costs, further add to the market's complexities. Economic uncertainties, such as slowdowns in the construction industry and the ongoing shortage of skilled labor, also pose challenges to achieving consistent growth in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 8.9% |

The fire stopping materials segment, specifically the sealants and fillers category, accounted for USD 600 million in 2024 and is expected to grow at a CAGR of 9.4% through 2034. Innovation in sealants and fillers has been key to this growth, with manufacturers continuously developing products that offer enhanced performance, easier application, and greater durability. Intumescent sealants, in particular, are gaining popularity as they expand under high temperatures to effectively seal gaps and prevent the spread of fire. Firestopping mortars also play a crucial role, particularly in sealing large openings around cables, ducts, and pipes in fire-rated walls and floors, thereby addressing the growing demand for fire protection in commercial and industrial settings.

The industrial sector, which accounted for 49% of the fire stopping materials market in 2024, is projected to grow at a CAGR of 9.4% between 2025 and 2034. This growth is driven by stringent fire safety regulations in high-risk environments such as oil and gas facilities, chemical plants, and manufacturing sites. The need to prevent fire spread in these operations is critical due to the presence of flammable chemicals, gases, and heavy machinery. As these industries continue to expand, the demand for fire stopping materials will only increase.

In the U.S., the fire stopping materials market generated USD 500 million in 2024 and is expected to grow at a CAGR of 9.2% through 2034. The country's growth is attributed to stricter fire safety standards, a booming construction industry, and ongoing advancements in passive fire protection technologies. The focus on retrofitting, renovations, and protecting critical infrastructure further supports the strong upward trend of the market in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Stricter fire safety regulations

- 3.6.1.2 Increased construction, urbanization, and industrialization

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of fire stopping materials

- 3.6.2.2 Inadequate skilled labor

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Coatings

- 5.3 Sealants & fillers

- 5.3.1 Silicone-based sealants

- 5.3.2 Acrylic sealants

- 5.3.3 Intumescent sealants

- 5.3.4 Others (cementitious fillers etc.)

- 5.4 Sheets & boards

- 5.4.1 Mineral wool boards

- 5.4.2 Intumescent sheets

- 5.4.3 Composite boards

- 5.4.4 Others (gypsum-based boards etc.)

- 5.5 Putty & foam

- 5.5.1 Intumescent putty

- 5.5.2 Fire-rated foam

- 5.5.3 Expanding foam

- 5.5.4 Others (putty pads etc.)

- 5.6 Others (collars, fire blocks etc.)

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Passive fire protection

- 6.3 Active fire protection

Chapter 7 Market Estimates & Forecast, By Fire Rating, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 1-hour rated

- 7.3 2-hour rated

- 7.4 3-hour rated

- 7.5 4-hour rated

- 7.6 More than 4-hour rated

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Electrical

- 8.3 Mechanical

- 8.4 Plumbing

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

- 9.4.1 Oil & gas

- 9.4.2 Automotive

- 9.4.3 Manufacturing

- 9.4.4 Data centers

- 9.4.5 Others (automotive, marine etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 Bostik

- 12.3 Emseal Joint Systems

- 12.4 Everkem

- 12.5 Flame Stop

- 12.6 Fosroc

- 12.7 H. B. Fuller Company

- 12.8 Hilti

- 12.9 Promat

- 12.10 RectorSeal

- 12.11 Rockwool

- 12.12 Sika

- 12.13 Specified Technologies

- 12.14 Tremco

- 12.15 Unique Fire Stop Products

不燃覆材全球市場報告:趨勢、預測和競爭分析(至 2031 年)

不燃覆材全球市場報告:趨勢、預測和競爭分析(至 2031 年) 全球防火材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球防火材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 全球消防市場:2025 年

全球消防市場:2025 年 防火材料市場規模、佔有率和成長分析(按產品、火災類型、分銷管道、應用、最終用戶和地區)- 2025-2032 年行業預測2030 年防火材料市場預測:按類型、應用、最終用戶和地區進行的全球分析2025年全球建築防火材料市場報告

防火材料市場規模、佔有率和成長分析(按產品、火災類型、分銷管道、應用、最終用戶和地區)- 2025-2032 年行業預測2030 年防火材料市場預測:按類型、應用、最終用戶和地區進行的全球分析2025年全球建築防火材料市場報告 全球防火材料市場:市場規模、佔有率、趨勢分析(按材料、應用、最終用途和地區)、細分市場預測(2025-2030 年)

全球防火材料市場:市場規模、佔有率、趨勢分析(按材料、應用、最終用途和地區)、細分市場預測(2025-2030 年) 全球防火材料市場:按類型、應用、最終用戶、地區、機會、預測,2018-2032 年防火材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)2030 年消防材料市場預測:按材料類型、應用、最終用戶和地區分類的全球分析

全球防火材料市場:按類型、應用、最終用戶、地區、機會、預測,2018-2032 年防火材料:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)2030 年消防材料市場預測:按材料類型、應用、最終用戶和地區分類的全球分析