|

市場調查報告書

商品編碼

1698338

氫燃料電池汽車市場機會、成長動力、產業趨勢分析及2025-2034年預測Hydrogen Fuel Cell Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

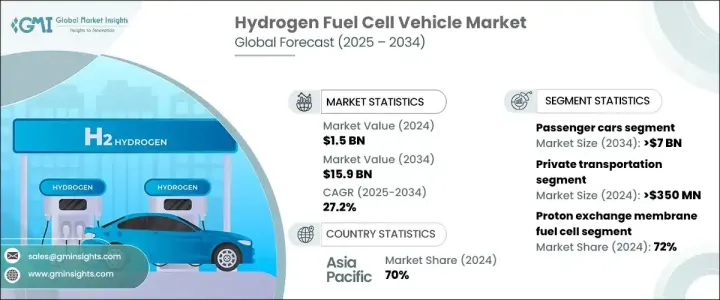

2024 年全球氫燃料電池汽車市場規模達到 15 億美元,預計 2025 年至 2034 年間將以 27.2% 的強勁複合年成長率成長。清潔能源解決方案的需求激增,加上對氫燃料補給基礎設施的投資不斷增加,正在推動市場擴張。世界各國政府正投入大量資金建立廣泛的加氫網路,確保其可及性並鼓勵廣泛採用氫動力汽車。在各國努力實現嚴格的排放目標並向永續的交通解決方案轉型之際,這些努力至關重要。

隨著全球汽車製造商將重點轉向零排放汽車,氫燃料電池技術作為傳統內燃機和電池電動車的可行替代品越來越受到關注。氫動力汽車結合了長續航力和快速加油時間,具有獨特的優勢,解決了電動車的關鍵問題,例如充電時間長。這項優勢加上政府支持清潔能源計畫的政策,正在激發消費者的興趣並加快採用率。領先的汽車公司正在增加產量以滿足不斷成長的需求,一些製造商推出了新的氫燃料電池車型以滿足市場需求。此外,燃料電池技術的不斷進步使得氫動力交通更加經濟高效,進一步鞏固了其在未來交通運輸中的地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15億美元 |

| 預測值 | 159億美元 |

| 複合年成長率 | 27.2% |

氫燃料電池汽車市場按車輛類型細分,包括乘用車、商用車和專用車。 2024 年,乘用車市場佔據主導地位,達到 50%,預計到 2034 年將創造 70 億美元的市場價值。對零排放運輸的日益追求迫使汽車製造商開發氫動力乘用車,將燃料電池技術與電池系統結合,以提高行駛里程和效率。消費者對氫動力汽車的偏好日益成長,因為它們能夠長途行駛,而無需像電動車那樣長時間充電。消費者情緒的轉變正在推動汽車製造商投資氫技術,進一步促進市場成長。

就技術而言,市場分為質子交換膜 (PEM) 燃料電池、固體氧化物燃料電池、鹼性燃料電池、磷酸燃料電池和其他類型。 2024年,PEM燃料電池憑藉其卓越的效率、輕量化的結構和快速的啟動能力佔據市場主導地位,佔有72%的佔有率。這些特性使得PEM燃料電池成為氫動力汽車的首選。薄膜材料和燃料電池堆設計的不斷進步正在推動性能的提高,同時降低生產成本,使該技術更容易被大規模採用。

亞太地區成為氫燃料電池汽車市場的領先地區,到 2024 年將佔據 70% 的市場。這一成長得益於政府對氫燃料補給基礎設施和大規模氫氣生產計劃的大量投資。該地區各國正積極將氫能納入其長期能源戰略,並提供大量財政激勵措施以加速汽車普及。隨著汽車製造商擴大生產以滿足日益成長的需求,氫動力汽車的發展勢頭強勁,鞏固了該地區在全球市場的主導地位。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 原物料供應商

- 零件供應商

- 製造商

- 技術提供者

- 最終用途

- 供應商格局

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 監管格局

- 價格趨勢

- 成本細分分析

- 衝擊力

- 成長動力

- 政府加強對氫燃料電池汽車的誘因與補貼力度

- 擴大加氫基礎設施

- 增加綠色氫氣生產的投資

- 零排放商業運輸需求不斷成長

- 產業陷阱與挑戰

- 生產和加油成本高

- 加氫基礎設施有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 掀背車

- SUV

- 商用車

- 輕型商用車(LCV)

- 重型商用車(HCV)

- 專用車輛

- 工業車輛

- 軍用車輛

第6章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 質子交換膜燃料電池(PEMFC)

- 固態氧化物燃料電池(SOFC)

- 鹼性燃料電池

- 磷酸燃料電池

- 其他

第7章:市場估計與預測:依範圍,2021 - 2034 年

- 主要趨勢

- 短距離(0-250英里)

- 中距離(251-500英里)

- 長距離(500 英里以上)

第8章:市場估計與預測:依功率範圍,2021 年至 2034 年

- 主要趨勢

- 小於150kW

- 150-250千瓦

- 250kW以上

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 私人交通

- 大眾運輸

- 工業的

- 軍事與國防

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- BMW

- FAW Group

- Ford

- General Motors

- Great Wall Motor

- Honda

- Hyundai

- Hyzon Motors

- Iveco Group

- MAN Energy Solutions

- Mercedes-Benz

- Nikola Corporation

- Porsche

- Renault

- Riversimple

- SAIC

- Stellantis

- Toyota

- Volkswagen

- Volvo

The Global Hydrogen Fuel Cell Vehicle Market reached USD 1.5 billion in 2024 and is projected to expand at a robust CAGR of 27.2% between 2025 and 2034. The surging demand for clean energy solutions, in line with increasing investments in hydrogen refueling infrastructure, is propelling market expansion. Governments worldwide are making substantial financial commitments to build an extensive hydrogen refueling network, ensuring accessibility and encouraging widespread adoption of hydrogen-powered vehicles. These efforts are crucial as nations strive to meet stringent emissions targets and transition toward sustainable transportation solutions.

As global automotive manufacturers shift focus toward zero-emission vehicles, hydrogen fuel cell technology is gaining traction as a viable alternative to conventional internal combustion engines and battery electric vehicles. Hydrogen-powered vehicles offer a unique advantage by combining long-range capabilities with rapid refueling times, addressing key concerns associated with battery electric vehicles, such as lengthy charging durations. This advantage, along with government policies supporting clean energy initiatives, is fueling consumer interest and accelerating adoption rates. Leading automotive companies are ramping up production to cater to the rising demand, with several manufacturers unveiling new hydrogen fuel cell models in response to market needs. Additionally, ongoing advancements in fuel cell technology are making hydrogen-powered mobility more cost-effective and efficient, further solidifying its position in the future of transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $15.9 Billion |

| CAGR | 27.2% |

The hydrogen fuel cell vehicle market is segmented by vehicle type, including passenger cars, commercial vehicles, and specialized vehicles. In 2024, the passenger car segment held a dominant 50% market share and is expected to generate USD 7 billion by 2034. The increasing push for zero-emission transportation is compelling automakers to develop hydrogen-powered passenger cars that integrate fuel cell technology with battery systems to enhance driving range and efficiency. Consumers are showing a growing preference for hydrogen vehicles due to their ability to travel long distances without the extended charging times associated with battery electric vehicles. This shift in consumer sentiment is driving automakers to invest in hydrogen technology, further boosting market growth.

In terms of technology, the market is categorized into proton exchange membrane (PEM) fuel cells, solid oxide fuel cells, alkaline fuel cells, phosphoric acid fuel cells, and other variants. In 2024, PEM fuel cells dominated the market, holding a 72% share due to their superior efficiency, lightweight structure, and rapid start-up capability. These characteristics make PEM fuel cells the preferred choice for hydrogen-powered vehicles. Continuous advancements in membrane materials and fuel cell stack design are driving performance improvements while reducing production costs, making the technology more accessible for mass adoption.

Asia Pacific emerged as the leading region in the hydrogen fuel cell vehicle market, capturing a significant 70% share in 2024. This growth is driven by extensive government investments in hydrogen refueling infrastructure and large-scale hydrogen production initiatives. Countries across the region are actively incorporating hydrogen into their long-term energy strategies, providing substantial financial incentives to accelerate vehicle adoption. As automakers scale up production to meet growing demand, hydrogen-powered mobility is gaining momentum, reinforcing the region's position as a dominant player in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End Use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trends

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising government incentives and subsidies for adoption of hydrogen fuel cell vehicles

- 3.10.1.2 Expanding hydrogen refueling infrastructure

- 3.10.1.3 Increasing investments in green hydrogen production

- 3.10.1.4 Growing demand for zero-emission commercial transport

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High production and refueling costs

- 3.10.2.2 Limited hydrogen refueling infrastructure

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Heavy Commercial Vehicles (HCV)

- 5.4 Specialized Vehicles

- 5.4.1 Industrial vehicles

- 5.4.2 Military vehicles

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Proton Exchange Membrane Fuel Cells (PEMFCs)

- 6.3 Solid Oxide Fuel Cells (SOFCs)

- 6.4 Alkaline fuel cell

- 6.5 Phosphoric acid fuel cell

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Range, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short range (0-250 Miles)

- 7.3 Medium range (251-500 Miles)

- 7.4 Long range (Above 500 Miles)

Chapter 8 Market Estimates & Forecast, By Power Range, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Less than 150kW

- 8.3 150-250kW

- 8.4 Above 250kW

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Private transportation

- 9.3 Public transportation

- 9.4 Industrial

- 9.5 Military & defense

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 BMW

- 11.2 FAW Group

- 11.3 Ford

- 11.4 General Motors

- 11.5 Great Wall Motor

- 11.6 Honda

- 11.7 Hyundai

- 11.8 Hyzon Motors

- 11.9 Iveco Group

- 11.10 MAN Energy Solutions

- 11.11 Mercedes-Benz

- 11.12 Nikola Corporation

- 11.13 Porsche

- 11.14 Renault

- 11.15 Riversimple

- 11.16 SAIC

- 11.17 Stellantis

- 11.18 Toyota

- 11.19 Volkswagen

- 11.20 Volvo

2025 年至 2033 年氫燃料電池汽車市場報告(按技術(質子交換膜燃料電池、磷酸燃料電池等)、車輛類型(乘用車、商用車)和地區分類)

2025 年至 2033 年氫燃料電池汽車市場報告(按技術(質子交換膜燃料電池、磷酸燃料電池等)、車輛類型(乘用車、商用車)和地區分類) 汽車燃料電池系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

汽車燃料電池系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 氫內燃機市場按條件、功率、燃料類型、應用和最終用途行業分類 - 2025-2030 年全球預測

氫內燃機市場按條件、功率、燃料類型、應用和最終用途行業分類 - 2025-2030 年全球預測 2025年全球氫燃料電池汽車市場報告

2025年全球氫燃料電池汽車市場報告 2025 年燃料電池電動汽車全球市場報告

2025 年燃料電池電動汽車全球市場報告 2025 年燃料電池汽車全球市場報告

2025 年燃料電池汽車全球市場報告 H2-ICE 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

H2-ICE 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球氫動力卡車市場規模、佔有率及趨勢分析報告:按車輛、燃料電池技術、行駛里程、馬達功率、應用、地區和細分市場進行預測(2025-2030 年)

全球氫動力卡車市場規模、佔有率及趨勢分析報告:按車輛、燃料電池技術、行駛里程、馬達功率、應用、地區和細分市場進行預測(2025-2030 年) 汽車燃料電池市場機會、成長動力、產業趨勢分析及 2024 - 2032 年預測

汽車燃料電池市場機會、成長動力、產業趨勢分析及 2024 - 2032 年預測 燃料電池電動車市場規模、佔有率、成長分析,按車輛、類型、範圍、產量、地區 - 產業預測,2025-2032 年

燃料電池電動車市場規模、佔有率、成長分析,按車輛、類型、範圍、產量、地區 - 產業預測,2025-2032 年