|

市場調查報告書

商品編碼

1685690

汽車燃料電池系統:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Automotive Fuel Cell System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

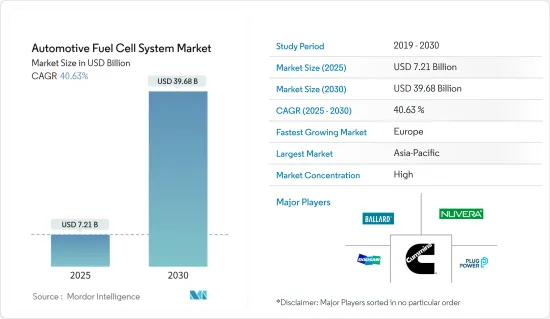

預計 2025 年汽車燃料電池系統市場規模為 72.1 億美元,到 2030 年將達到 396.8 億美元,預測期內(2025-2030 年)的複合年成長率為 40.63%。

主要亮點

- 新冠疫情對市場的影響不如對其他汽車領域嚴重。儘管封鎖期間需求有所下降,但預計市場將在 2021 年獲得成長動力,並在整個預測期內保持高成長。

- 隨著環保意識的增強,各國政府和環保機構制定了更嚴格的排放氣體法規和立法,預計未來幾年節能柴油引擎的製造成本將會增加。因此,預計短期內新型商用車柴油引擎領域將出現成長乏力的局面。

- 此外,傳統的石化燃料動力來源的商用車輛,尤其是卡車和公共汽車,也增加了運輸排放氣體。燃料電池商用車被認為是低排放或零排放氣體汽車,其出現有望減少重型商用車的排放氣體。

- 此外,全球各國政府機構選擇綠色能源出行來抑制交通污染的舉措是預計在不久的將來推動燃料電池系統市場發展的關鍵因素。

汽車燃料電池系統市場趨勢

政府清潔能源措施推動氫燃料需求

- 預計在不久的將來推動燃料電池商用車市場發展的關鍵因素是世界各國政府主動選擇綠色能源出行來限制和減少交通污染。全球多個政府已推出計劃,鼓勵燃料電池電動車(FCEV)在道路上行駛,這也將有助於汽車燃料電池產業的發展。

- 2022年2月,日本環境省宣布將支持地方政府和企業建立氫能商業聯盟。該部正在與一些公司和地方政府合作,實施一個氫氣供應鏈平台,生產低碳氫化合物並在當地利用。目標是到2030年左右在日本全國開展示範實驗,並實現氫氣供應鏈平台。

- 2022年2月,印度新和可再生能源部宣布了一項「可再生能源研究與開發」計劃,以支持可再生能源各個方面的研究,包括基於氫能的運輸和燃料電池開發。該部列出了一些關鍵進展。印度科學研究所(IISc)建立了一座透過生質能氣化生產高純度氫氣的工廠。國際粉末冶金和新材料高級研究中心(ARCI)燃料電池技術中心將安裝一條綜合自動化生產線,用於製造20kW PEM燃料電池堆。

- 2022年1月,德國政府宣布支持氫動力卡車CryoTRUCK計劃。測試專家 IABG 和慕尼黑工業大學將共同開發用於遠距氫氣卡車的帶有加油系統的 CRYOGAS 氫氣罐。 CryoTRUCK計劃為期三年半,總預算超過 2500 萬歐元,將開發和檢驗用於重型燃料電池卡車的低溫壓縮氫氣 (CRYOGAS) 儲存和加油系統的第一代技術。

- 這些舉措正在加速燃料電池運輸的採用並推動市場向前發展。然而,燃料電池車在全球市場廣泛應用的一個主要障礙是缺乏氫能基礎設施。全球加氫站數量少的原因是投資高,氫氣生產採用傳統方法,導致排放量高,難以遵守嚴格的能源政策法規。

- 建立新的加氫基礎設施成本非常高(但比建立甲醇或乙醇基礎設施便宜)。由天然氣生產的氫氣可能比汽油便宜。氫氣是透過水和電的水解產生的,除非使用低成本的非高峰電力或太陽能電池板,否則使用傳統方法生產的氫氣比汽油更昂貴。

歐洲:預計高成長

- 歐盟計畫大幅減少運輸部門的溫室氣體排放。因此,一些歐洲國家已將部署燃料電池(主要是 PEMFC)等創新技術作為實現這些目標的手段。預計這將為不久的將來參與該市場的燃料電池製造商創造巨大的機會。

- 歐洲佔全球整體氫能投資提案的 30% 以上(約 760 億美元),總合提案近 314 個計劃,其中 268 個項目計劃到 2030 年全面或部分試運行使用。

- 歐盟正在提案世界上最嚴格的排放標準,以減少傳統燃料汽車的使用,並鼓勵該地區使用替代燃料汽車。這些排放法規預計將推動市場和汽車製造商向零排放汽車邁進。

- 已經啟動了多個計劃來探索和開發解決車輛排放氣體問題的解決方案。例如,正在進行的歐盟支持計劃,如將部署 1,000 輛氫動力公車和基礎設施的 H2BusEurope 項目,以及將在 22 個歐洲城市投入營運約 300 輛燃料電池電動巴士 (FCEB) 的 JIVE 和 JIVE 2計劃,將獲得歐盟 (EU) 地平線電動公車 (FCEB) 的 JIVE 和 JIVE 2項目,將獲得歐盟 (EU) 地平電動公車 (FCEB) 的 JIVE 和 JIVE 2項目,將獲得歐盟 (EU) 地平電動公車 2020 燃料和電池架構計畫下的萬歐元的津貼。計劃聯盟由來自七個國家的22個成員組成。

- 此外,在市場上營運的公司正在採用新產品開發、聯合開發、合約、協議等策略來保持其市場地位。例如

- 2022 年 9 月,現代汽車公司和依維柯集團在漢諾威 IAA 交通運輸展上推出了首款 IVECO eDAILYFuel 電池電動車。兩家公司於 7 月初推出了配備現代燃料電池系統的氫動力 IVECO BUS 車輛。 eDAILY 燃料電池電動車 (FCEV) 代表著依維柯最暢銷、運行時間最長的大型貨車的光明未來。

- 此外,該地區氫技術的發展可能有助於擴大市場。

- 例如,2022年3月,康明斯宣布位於德國黑爾滕的全新氫燃料電池系統生產中心已成功運作。這一重要發展加強了該公司擴展替代能源解決方案的努力,並有望促進整個歐洲採用氫技術。該工廠的初始生產能力為每年 10 兆瓦,用於燃料電池系統的工程和組裝。

- 在該地區營運的公司正在不斷開發新材料和新燃料電池技術。我們也正在努力擴大我們的設施。隨著一些公司宣布即將進行的投資,表明他們對燃料電池技術的承諾,預計這一趨勢將持續下去。

汽車燃料電池系統產業概況

- 汽車燃料電池系統市場主要由 Ballard Power Systems Inc.、Doosan Fuel Cell、Hydrogenics 和 Nedstack Fuel Cell Technology BV 等公司主導。這些公司正在利用新技術和創新技術擴展業務,以獲得競爭優勢。

- 2023年2月,斗山燃料電池公司與南澳政府及斗山物產旗下子公司HyAxiom簽署了合作聲明。根據協議,南澳大利亞州和斗山燃料電池公司承諾「交換生產綠色氫氣及其衍生物的設備和經驗」、「制定策略和合作夥伴關係,以實現氫氣出口的全球競爭力」以及「共用氫氣生產的最佳實踐」。

- 2022 年 7 月,依維柯集團透過其品牌 IVECO BUS 宣布與 HTWO 合作,為未來歐洲製造的氫動力公車配備世界上最先進的燃料電池系統。 HTWO 於 2020 年 12 月首次發布,是現代汽車集團基於燃料電池系統的氫能業務品牌,同時也體現了現代汽車對氫能經濟的堅定承諾。 HTWO 憑藉其在現代 FCEV 中採用的成熟燃料電池技術,正在將其燃料電池技術產品擴展到其他汽車OEM和非汽車領域,從而實現氫氣在所有領域的使用。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 政府措施支持市場成長

- 市場限制

- 缺乏基礎設施對市場成長構成挑戰

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 電解質類型

- 聚合物電子膜燃料電池

- 直接甲醇燃料電池

- 鹼性燃料電池

- 磷酸燃料電池

- 車輛類型

- 搭乘用車

- 商用車

- 燃料類型

- 氫

- 甲醇

- 輸出

- 小於100KW

- 100~200KW

- 200KW以上

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 北美洲

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- BorgWarner Inc.

- Nuvera Fuel Cells LLC

- Ballard Power Systems Inc.

- Hydrogenics(Cummins Inc.)

- Nedstack Fuel Cell Technology BV

- Oorja Corporation

- Plug Power Inc.

- SFC Energy AG

- Watt Fuel Cell Corporation

- Doosan Fuel Cell Co. Ltd

第7章 市場機會與未來趨勢

- 提高可再生能源整合度

簡介目錄

Product Code: 46343

The Automotive Fuel Cell System Market size is estimated at USD 7.21 billion in 2025, and is expected to reach USD 39.68 billion by 2030, at a CAGR of 40.63% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic did not impact the market as severely as it had affected other automotive segments. While the demand experienced a decline during the lockdown, it was expected that the market would gain momentum in 2021, with high growth continuing throughout the forecast period.

- With the growing environmental concerns, governments and environmental agencies are enacting stringent emission norms and laws, which are expected to increase the manufacturing cost of fuel-efficient diesel engines in the coming years. As a result, the new commercial vehicle diesel engines segment is expected to register a sluggish growth rate during the short term.

- Additionally, conventional fossil fuel-powered commercial vehicles, especially trucks, and buses, are responsible for increasing transportation emissions. The advent of fuel-cell commercial vehicles, which are considered low or zero-emission vehicles, is anticipated to reduce vehicular emissions emitted by heavy commercial vehicles.

- Moreover, initiatives by government bodies around the world to opt for green energy mobility in order to curtail and curb transportation pollution is a key factor that is projected to drive the fuel cell system market in the near future.

Automotive Fuel Cell System Market Trends

Government Initiatives for Clean Energy is Driving the Hydrogen Fuel Demand

- Government initiatives throughout the world to choose green energy mobility in order to restrict and reduce transportation pollution is a crucial driver that is expected to boost the fuel cell commercial vehicle market in the near future. Several governments are already laying out plans throughout the world to encourage fuel-cell electric vehicles (FCEVs) on the road will also help the automotive fuel-cell industry grow.

- In February 2022, Japan's Ministry of the Environment announced that it would support local governments and companies in the establishment of a hydrogen business consortium. The ministry has been jointly implementing a hydrogen supply chain platform that generates low-carbon hydrogen and utilizes it in the region with certain companies and local governments. It aims to realize the hydrogen supply chain platform after conducting demonstrations across Japan by around 2030.

- In February 2022, the Indian Ministry of New and Renewable Energy announced that it implemented the 'Renewable Energy Research and Technology Development' program to support research in various aspects of renewable energy, including inter-alia hydrogen-based transportation and fuel cell development. The ministry listed some of its major development. The Indian Institute of Science (IISc) established a production plant for high-purity hydrogen generation through biomass gasification. International Advanced Research Centre for Powder Metallurgy and New Materials (ARCI) Center for Fuel Cell Technologies is setting up an integrated automated manufacturing line for producing 20 kW PEM fuel cell stacks.

- In January 2022, the German government announced support for the CryoTRUCK project for hydrogen trucks. The testing specialist IABG and the Technical University of Munich are jointly developing a CRYOGAS hydrogen gas tank with a refueling system for hydrogen trucks in long-distance transport. The three-and-a-half-year CryoTRUCK project, with a total budget of more than EUR 25 million, will develop and validate a first-generation technology for cryogenic compressed hydrogen gas (CRYOGAS) storage and refueling systems in heavy-duty fuel cell trucks.

- Such initiatives are driving the market forward by increasing the adoption of fuel-cell transportation. However, the major obstacle to the introduction of a wide range of fuel cell vehicles in the global market is the lack of hydrogen infrastructure. Factors for fewer hydrogen refueling stations around the world are the involvement of high investment and conventional production methods of hydrogen, which is leading to high emission levels and making it difficult to be in line with the stringent Energy Policy Act.

- Establishing a new hydrogen refueling infrastructure is extremely costly (but not any costlier than establishing a methanol or ethanol infrastructure). Hydrogen that is produced from natural gas can be cheaper than gasoline. Hydrogen produced from water and electricity via hydrolysis is more expensive than gasoline using conventional methods unless low-cost off-peak electricity is used or solar panels are employed.

Europe Expected to Witness High Growth Rate

- The European Union plans to reduce greenhouse gas (GHG) emissions from the transportation sector significantly. As a result, several countries in Europe have identified the implementation of innovative technologies, such as fuel cells (primarily PEMFC), as a way to meet these objectives. This, in turn, is expected to provide a significant opportunity for the fuel cell manufacturers involved in the market in the near future.

- Europe is home to over 30% of proposed hydrogen investments globally (about USD 76 billion), with nearly 314 project proposals in total and 268 aiming for full or partial commissioning through 2030.

- The European Union (EU) has proposed some of the most stringent emission standards in the world in order to reduce the usage of conventional fuel vehicles and encourage the use of alternative fuel vehicles in the region. These emission standards are projected to push the market and vehicle manufacturers toward zero-emission vehicles.

- Several projects have been initiated to explore and develop acceptable solutions to the problem of automobile emissions. For instance, ongoing EC-supported initiatives include the H2BusEurope scheme that involves the deployment of 1,000 hydrogen buses and infrastructure and the JIVE and JIVE 2 projects that involve putting into operation nearly 300 fuel cell electric buses (FCEBs) in 22 cities across Europe and will be supported in part by a 32 million euro grant from the FCH JU (Fuel Cells and Hydrogen Joint Undertaking) within the European Union's Horizon 2020 framework program for research and innovation. The project consortium consists of 22 members from seven different countries.

- Furthermore, companies operating in the market are adopting strategies such as new product developments, collaborations, contracts, and agreements to sustain their market position. For instance,

- In September 2022, Hyundai Motor Company and Iveco Group at IAA Transportation 2022 in Hannover unveiled the first IVECO eDAILYFuel Cell Electric Vehicle. The two companies announced hydrogen-powered IVECO BUS vehicles with Hyundai's fuel cell system earlier in July. The eDAILYFuel Cell Electric Vehicle (FCEV) exemplifies IVECO's best-selling and longest-running large van's future potential.

- In addition, the development of hydrogen technology in the region will help in the expansion of the market.

- For instance, in March 2022, Cummins Inc. announced the successful operation of its new Hydrogen fuel cell systems production center in Herten, Germany. This significant development is expected to bolster the company's efforts in scaling up alternative power solutions and promote the widespread adoption of hydrogen technologies throughout Europe. The facility boasts an initial production capacity of 10MW per year for fuel cell system engineering and assembly.

- The companies active in the region are constantly working on new materials and new fuel cell technologies. They are also spending on the expansion of their facilities. These trends are expected to continue in the coming years, as some companies have indicated their focus on fuel cell technology by announcing their upcoming investments.

Automotive Fuel Cell System Industry Overview

- The automotive fuel cell system market is dominated by players such as Ballard Power Systems Inc., Doosan Fuel Cell Co. Ltd, Hydrogenics, and Nedstack Fuel Cell Technology BV. These companies have been expanding their businesses using new and innovative technologies to have an advantage over their competitors.

- In February 2023, Doosan Fuel Cell signed a statement of cooperation with the South Australian government and HyAxiom, a subsidiary of Doosan Corporation. In accordance with the agreement, South Australia and Doosan Fuel Cell committed to "exchange equipment and experience for the production of eco-friendly hydrogen and derivatives, to "create strategies and alliances to achieve worldwide competitiveness in hydrogen exports," and to "share best practices for hydrogen production.

- In July 2022, Iveco Group, through its brand IVECO BUS, announced that it would partner with HTWO to equip its future European hydrogen-powered buses with world-leading fuel cell systems. HTWO, as a fuel cell system-based hydrogen business brand of Hyundai Motor Group, was first released in December 2020 with Hyundai's strong commitment to a hydrogen economy. With its proven fuel cell technology utilized in Hyundai FCEVs, HTWO is expanding the provision of fuel cell technology to other automobile OEMs and non-automobile sectors to make hydrogen available for everything.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Government Initiatives to Support The Market Growth

- 4.2 Market Restraints

- 4.2.1 Lack of Infrastructure poses a Challenge For The Growth of The Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Electrolyte Type

- 5.1.1 Polymer Electronic Membrane Fuel Cell

- 5.1.2 Direct Methanol Fuel Cell

- 5.1.3 Alkaline Fuel Cell

- 5.1.4 Phosphoric Acid Fuel Cell

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Fuel Type

- 5.3.1 Hydrogen

- 5.3.2 Methanol

- 5.4 Power Output

- 5.4.1 Below 100 KW

- 5.4.2 100-200 KW

- 5.4.3 Above 200 KW

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BorgWarner Inc.

- 6.2.2 Nuvera Fuel Cells LLC

- 6.2.3 Ballard Power Systems Inc.

- 6.2.4 Hydrogenics (Cummins Inc.)

- 6.2.5 Nedstack Fuel Cell Technology BV

- 6.2.6 Oorja Corporation

- 6.2.7 Plug Power Inc.

- 6.2.8 SFC Energy AG

- 6.2.9 Watt Fuel Cell Corporation

- 6.2.10 Doosan Fuel Cell Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Renewable Energy Integration

02-2729-4219

+886-2-2729-4219

2025 年至 2033 年氫燃料電池汽車市場報告(按技術(質子交換膜燃料電池、磷酸燃料電池等)、車輛類型(乘用車、商用車)和地區分類)

2025 年至 2033 年氫燃料電池汽車市場報告(按技術(質子交換膜燃料電池、磷酸燃料電池等)、車輛類型(乘用車、商用車)和地區分類) 氫內燃機市場按條件、功率、燃料類型、應用和最終用途行業分類 - 2025-2030 年全球預測

氫內燃機市場按條件、功率、燃料類型、應用和最終用途行業分類 - 2025-2030 年全球預測 2025年全球氫燃料電池汽車市場報告

2025年全球氫燃料電池汽車市場報告 2025 年燃料電池電動汽車全球市場報告

2025 年燃料電池電動汽車全球市場報告 2025 年燃料電池汽車全球市場報告

2025 年燃料電池汽車全球市場報告 H2-ICE 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

H2-ICE 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 氫燃料電池汽車市場機會、成長動力、產業趨勢分析及2025-2034年預測

氫燃料電池汽車市場機會、成長動力、產業趨勢分析及2025-2034年預測 全球氫動力卡車市場規模、佔有率及趨勢分析報告:按車輛、燃料電池技術、行駛里程、馬達功率、應用、地區和細分市場進行預測(2025-2030 年)

全球氫動力卡車市場規模、佔有率及趨勢分析報告:按車輛、燃料電池技術、行駛里程、馬達功率、應用、地區和細分市場進行預測(2025-2030 年) 汽車燃料電池市場機會、成長動力、產業趨勢分析及 2024 - 2032 年預測

汽車燃料電池市場機會、成長動力、產業趨勢分析及 2024 - 2032 年預測 燃料電池電動車市場規模、佔有率、成長分析,按車輛、類型、範圍、產量、地區 - 產業預測,2025-2032 年

燃料電池電動車市場規模、佔有率、成長分析,按車輛、類型、範圍、產量、地區 - 產業預測,2025-2032 年

▼