|

市場調查報告書

商品編碼

1699245

汽車雷達市場機會、成長動力、產業趨勢分析及2025-2034年預測Automotive Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

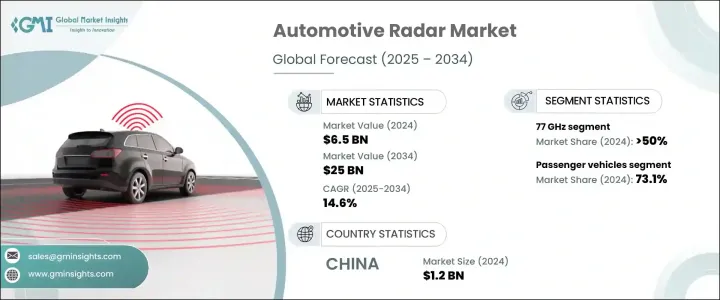

2024 年全球汽車雷達市場估值達 65 億美元,預計 2025 年至 2034 年期間的複合年成長率為 14.6%。這一成長得益於雷達技術的不斷進步,包括 4D 成像雷達、數位波束成形和人工智慧雷達處理等創新。這些增強功能正在提高範圍、解析度和干擾抑制,使雷達系統對於先進駕駛輔助系統(ADAS) 和自動駕駛更加有效。

無線 (OTA) 軟體更新可讓車輛接收雷達能力升級,進一步加速採用。電動和連網汽車的興起也推動了需求,因為雷達技術在盲點監控、自適應巡航控制和自動停車等安全功能中發揮著至關重要的作用。隨著連網汽車數量的不斷增加,汽車產業正在從獨立的雷達感測器轉向整合車輛網路轉變,以促進與其他汽車、基礎設施和基於雲端的系統的即時通訊。重點地區的嚴格安全法規進一步促使汽車製造商將基於雷達的解決方案作為其車型的標準功能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 65億美元 |

| 預測值 | 250億美元 |

| 複合年成長率 | 14.6% |

根據頻率,市場分為 24 GHz、77 GHz 和 79 GHz 雷達。 77 GHz 細分市場在 2024 年佔據了最大的市場佔有率,超過 50%。其廣泛採用是由於其卓越的解析度和更長的偵測範圍,這對於車道維持輔助和自動緊急煞車等關鍵安全功能至關重要。歐洲和北美的法規已將 77 GHz 雷達確立為新的行業標準,而中國最近的政策變化要求所有新車都配備高頻雷達系統,這正在加速亞太地區的採用。

市場分為乘用車和商用車,其中乘用車在 2024 年佔 73.1% 的佔有率。消費者對增強安全功能的偏好日益成長,導致基於雷達的駕駛輔助系統廣泛整合。在監管框架和更新的安全評級系統的推動下,盲點偵測和自適應巡航控制等技術正在成為私人車輛的標準。世界各國政府正在執行更嚴格的指導方針,使高頻雷達成為符合防撞和乘員保護標準的必需品。汽車製造商正在利用雷達技術來增強自動駕駛能力,特別是在 2 級和 3 級自動駕駛汽車中,高速公路駕駛和自動變換車道等功能依賴高精度雷達感測器。

就範圍而言,市場分為中程雷達 (MRR)、短程雷達 (SRR) 和遠程雷達 (LRR),其中 MRR 將在 2024 年佔據主導地位。其在城市交通中的重要性日益增加,其中自動停車和防撞需要 360 度態勢感知。隨著城市擴展智慧交通系統,叫車車隊、電動車和最後一哩外送服務擴大整合 MRR,以便在高流量環境中實現安全導航。智慧交通系統 (ITS) 的興起進一步推動了其應用,因為雷達感測器在即時交通監控、預測分析和事故預防中發揮關鍵作用。

根據銷售管道,市場也分為 OEM 和售後市場。 2024 年,隨著汽車製造商繼續將雷達系統直接整合到新車型中, OEM領域將佔據主導地位。領先的製造商正在與雷達技術提供者合作,以便在豪華車和中檔車中大規模部署 ADAS 功能。隨著消費者對汽車安全的意識不斷增強,汽車製造商擴大將基於雷達的解決方案作為標準而非可選功能。

亞太地區引領全球汽車雷達市場,光是中國一項,到 2024 年市場規模就將達 12 億美元。在政府推動智慧交通和智慧高速公路系統措施的大力支持下,對自動駕駛、人工智慧感測器和汽車電氣化的投資正在推動成長。鼓勵新能源汽車(NEV)採用雷達的優惠政策使該地區處於汽車雷達技術創新的前沿。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 晶片組提供者

- 雷達感測器生產商

- 一級汽車供應商

- 人工智慧和軟體供應商

- 利潤率分析

- 技術與創新格局

- 專利分析

- 用例

- 價格趨勢

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 對 ADAS 和自動駕駛汽車的需求不斷成長

- 雷達系統的技術進步

- 提高車輛電氣化和連接性

- 消費者道路安全意識不斷增強

- 產業陷阱與挑戰

- 成本高且整合複雜

- 干擾和標準化問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按頻率,2021 - 2034 年

- 主要趨勢

- 24 GHz雷達

- 77 GHz雷達

- 79 GHz雷達

第6章:市場估計與預測:依範圍,2021 - 2034 年

- 主要趨勢

- 短程雷達(SRR)

- 中程雷達(MRR)

- 遠程雷達(LRR)

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車(LCV)

- 重型商用車(HCV)

第8章:市場估計與預測:按銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第9章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 自適應巡航控制 (ACC)

- 盲點偵測(BSD)

- 前方碰撞警示 (FCW)

- 車道偏離預警系統 (LDWS)

- 自動緊急煞車(AEB)

- 停車輔助系統 (PA)

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- Analog Devices

- Aptiv

- Arbe Robotics

- Bosch

- Continental

- Denso

- Echodyne

- Fujitsu Ten

- Hella

- Hitachi Astemo

- Infineon Technologies

- Mitsubishi Electric

- NXP Semiconductors

- Oculii

- Smart Radar System

- Texas Instruments

- Uhnder

- Valeo

- Veoneer

- ZF Friedrichshafen

The Global Automotive Radar Market reached a valuation of USD 6.5 billion in 2024 and is projected to expand at a CAGR of 14.6% from 2025 to 2034. This growth is driven by the continuous advancement of radar technology, including innovations such as 4D imaging radar, digital beamforming, and AI-powered radar processing. These enhancements are improving range, resolution, and interference suppression, making radar systems more effective for advanced driver assistance systems (ADAS) and autonomous driving.

Over-the-air (OTA) software updates are allowing vehicles to receive radar capability upgrades, further accelerating adoption. The rise of electric and connected vehicles is also fueling demand, as radar technology plays a crucial role in safety features like blind spot monitoring, adaptive cruise control, and automated parking. With the increasing number of connected vehicles, the industry is transitioning from standalone radar sensors to integrated vehicle networks that facilitate real-time communication with other cars, infrastructure, and cloud-based systems. Strict safety regulations across key regions are further pushing automakers to implement radar-based solutions as standard features in their models.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $25 Billion |

| CAGR | 14.6% |

By frequency, the market is categorized into 24 GHz, 77 GHz, and 79 GHz radar. The 77 GHz segment held the largest market share of over 50% in 2024. Its widespread adoption is driven by its superior resolution and longer detection range, which are essential for critical safety features like lane-keeping assistance and automated emergency braking. Regulations in Europe and North America have established 77 GHz radar as the new industry standard, and recent policy changes in China mandating high-frequency radar systems in all new cars are accelerating adoption in the Asia Pacific region.

The market is segmented into passenger and commercial vehicles, with passenger cars holding a 73.1% share in 2024. Growing consumer preference for enhanced safety features has led to the widespread integration of radar-based driver assistance systems. Technologies such as blind spot detection and adaptive cruise control are becoming standard in personal vehicles, driven by regulatory frameworks and updated safety rating systems. Governments worldwide are enforcing stricter guidelines, making high-frequency radar a necessity for compliance with crash avoidance and occupant protection standards. Automakers are leveraging radar technology to enhance self-driving capabilities, particularly in Level 2 and Level 3 autonomous vehicles, where features like highway pilot and automated lane changes rely on high-precision radar sensors.

In terms of range, the market is divided into medium-range radar (MRR), short-range radar (SRR), and long-range radar (LRR), with MRR dominating in 2024. Its importance is growing in urban mobility, where self-parking and collision avoidance require 360-degree situational awareness. As cities expand smart transportation systems, ride-hailing fleets, electric vehicles, and last-mile delivery services are increasingly integrating MRR for safe navigation in high-traffic environments. The rise of intelligent transportation systems (ITS) is further driving adoption, as radar sensors play a key role in real-time traffic monitoring, predictive analytics, and accident prevention.

The market is also classified by sales channel into OEMs and aftermarket. In 2024, the OEM segment held the dominant share as automakers continued integrating radar systems directly into new vehicle models. Leading manufacturers are collaborating with radar technology providers to enable large-scale deployment of ADAS features in both luxury and mid-range vehicles. As consumer awareness of vehicle safety grows, automakers are increasingly including radar-based solutions as standard rather than optional features.

The Asia Pacific region leads the global automotive radar market, with China alone accounting for USD 1.2 billion in 2024. Investments in autonomous driving, AI-powered sensors, and vehicle electrification are driving growth, with strong support from government initiatives promoting smart transportation and intelligent highway systems. Favorable policies encouraging radar adoption in new energy vehicles (NEVs) are positioning the region at the forefront of innovation in automotive radar technology.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Chipset providers

- 3.2.2 Radar sensor producers

- 3.2.3 Tier-1 auto suppliers

- 3.2.4 AI & software providers

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Price trend

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for ADAS and autonomous vehicles

- 3.10.1.2 Technological advancements in radar systems

- 3.10.1.3 Increasing vehicle electrification and connectivity

- 3.10.1.4 Growing consumer awareness of road safety

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High costs and complex integration

- 3.10.2.2 Interference and standardization issues

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Frequency, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 24 GHz radar

- 5.3 77 GHz radar

- 5.4 79 GHz radar

Chapter 6 Market Estimates & Forecast, By Range, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short-Range radar(SRR)

- 6.3 Medium-Range radar(MRR)

- 6.4 Long-Range radar(LRR)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Adaptive Cruise Control (ACC)

- 9.3 Blind Spot Detection (BSD)

- 9.4 Forward Collision Warning (FCW)

- 9.5 Lane Departure Warning System (LDWS)

- 9.6 Automatic Emergency Braking (AEB)

- 9.7 Parking Assistance (PA)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Analog Devices

- 11.2 Aptiv

- 11.3 Arbe Robotics

- 11.4 Bosch

- 11.5 Continental

- 11.6 Denso

- 11.7 Echodyne

- 11.8 Fujitsu Ten

- 11.9 Hella

- 11.10 Hitachi Astemo

- 11.11 Infineon Technologies

- 11.12 Mitsubishi Electric

- 11.13 NXP Semiconductors

- 11.14 Oculii

- 11.15 Smart Radar System

- 11.16 Texas Instruments

- 11.17 Uhnder

- 11.18 Valeo

- 11.19 Veoneer

- 11.20 ZF Friedrichshafen

汽車雷達市場規模、佔有率及成長分析(按範圍、頻寬、應用和地區)- 2025-2032 年產業預測

汽車雷達市場規模、佔有率及成長分析(按範圍、頻寬、應用和地區)- 2025-2032 年產業預測 2025 年全球汽車雷達市場報告

2025 年全球汽車雷達市場報告 2030 年汽車雷達市場預測:按距離、車輛、頻率、技術、應用、最終用戶和地區進行的全球分析

2030 年汽車雷達市場預測:按距離、車輛、頻率、技術、應用、最終用戶和地區進行的全球分析 敵對車輛緩解裝置的全球市場:2024 年

敵對車輛緩解裝置的全球市場:2024 年 中國的汽車用毫米波(MMW)雷達產業(2024年)

中國的汽車用毫米波(MMW)雷達產業(2024年) 全球汽車雷達市場:按範圍、頻率、應用和車型 - 2025-2030 年預測

全球汽車雷達市場:按範圍、頻率、應用和車型 - 2025-2030 年預測 汽車技術雷達:汽車產業的技術雷達

汽車技術雷達:汽車產業的技術雷達 汽車雷達市場規模、佔有率、趨勢分析報告:2024-2030 年按距離、頻率、引擎、車輛、應用、地區和細分市場預測

汽車雷達市場規模、佔有率、趨勢分析報告:2024-2030 年按距離、頻率、引擎、車輛、應用、地區和細分市場預測 汽車雷達市場 - 全球和區域分析:按應用、按車輛類型、按推進力、按距離、按頻率、按地區 - 分析和預測 (2024-2034)

汽車雷達市場 - 全球和區域分析:按應用、按車輛類型、按推進力、按距離、按頻率、按地區 - 分析和預測 (2024-2034) 2024-2032 年按範圍、車輛類型、應用(自適應巡航控制、自動緊急煞車、盲點偵測、前方碰撞警告、智慧停車輔助等)和地區分類的汽車雷達市場報告

2024-2032 年按範圍、車輛類型、應用(自適應巡航控制、自動緊急煞車、盲點偵測、前方碰撞警告、智慧停車輔助等)和地區分類的汽車雷達市場報告