|

市場調查報告書

商品編碼

1699358

住宅自動電動馬達啟動器市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Residential Automatic Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

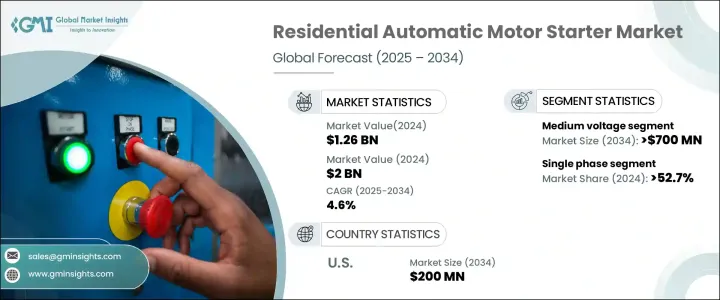

2024 年全球住宅自動電動馬達啟動器市值為 12.6 億美元,預計 2025 年至 2034 年期間的複合年成長率為 4.6%。這種穩步擴張反映了人們對能源效率的日益關注以及對可靠、緊湊和方便用戶使用的電氣解決方案日益成長的需求。隨著越來越多的屋主轉向智慧生活,對與現代住宅設置無縫整合的先進馬達啟動器的需求不斷增加。消費者越來越重視能夠提高便利性、降低能耗並符合永續發展趨勢的設備。

城市化和快速的住宅發展進一步推動了市場的發展,業主和建築商積極尋求高效的電力管理解決方案。家庭自動化系統的採用推動了對能夠最佳化電氣性能同時確保安全的智慧馬達啟動器的需求。此外,支持能源效率的監管政策正在加速這些系統的部署。智慧監控功能和增強的耐用性等技術進步使得這些啟動器在住宅應用中更具吸引力。隨著住宅領域逐漸注重高性能、節省空間和環保的電力基礎設施,全球對自動電動馬達啟動器的需求將持續激增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12.6億美元 |

| 預測值 | 20億美元 |

| 複合年成長率 | 4.6% |

市場根據電壓分為低壓、中壓和高壓部分。其中,中壓市場預計將實現顯著成長,預計到 2034 年將創造 7 億美元的市場價值。這些系統因其效率、緊湊的設計和易於安裝而越來越受到認可,使其成為現代住宅設置的理想選擇。尋求節省空間和簡化電氣解決方案的屋主青睞中壓電動馬達起動器,進一步推動了其在各個地區的應用。

就相位而言,家用自動電動機啟動器市場分為單相和三相系統。 2024 年,單相電動馬達起動器佔據 52.7% 的主導佔有率,預計需求將穩定上升。智慧家庭的日益普及、對永續性的高度重視以及對節能電氣解決方案的需求都是這一趨勢的關鍵因素。由於家庭希望在不影響可靠性的情況下最佳化能源消耗,單相啟動器正在成為現代電氣系統的經濟高效的選擇。

隨著節能智慧解決方案的日益普及,美國住宅自動電動馬達啟動器市場預計到 2034 年將達到 2 億美元。隨著城市化進程的加速、新住宅建設的繁榮以及對高效電源管理的高度重視,對先進馬達起動器的需求正在上升。屋主和建築商都認知到將這些系統整合到現代住宅中的好處,確保最佳電力使用,同時提高安全性和便利性。隨著市場的發展,自動電動機啟動器在塑造永續住宅基礎設施方面的作用將變得更加突出。

目錄

第1章:方法論與範圍

- 市場範圍和定義

- 市場估計和預測參數

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:按電壓,2021 - 2034

- 主要趨勢

- 低的

- 中等的

- 高的

第6章:市場規模及預測:依階段,2021 - 2034

- 主要趨勢

- 單相

- 三相

第7章:市場規模及預測:依地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 俄羅斯

- 英國

- 義大利

- 西班牙

- 荷蘭

- 奧地利

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 紐西蘭

- 馬來西亞

- 印尼

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 奈及利亞

- 科威特

- 阿曼

- 拉丁美洲

- 巴西

- 秘魯

- 阿根廷

第8章:公司簡介

- ABB

- C&S Electric

- CHINT Group

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric

- Havells India

- L&T Electrical and Automation

- Lovato Electric

- Mitsubishi Electric

- Rockwell Automation

- Schneider Electric

- Siemens

- SKN-Bentex Group

- WEG

The Global Residential Automatic Motor Starter Market was valued at USD 1.26 billion in 2024 and is projected to grow at a CAGR of 4.6% between 2025 and 2034. This steady expansion reflects the rising focus on energy efficiency and the increasing demand for reliable, compact, and user-friendly electrical solutions. As more homeowners shift toward smart living, the need for advanced motor starters that seamlessly integrate with modern residential setups continues to rise. Consumers are increasingly prioritizing devices that enhance convenience, reduce energy consumption, and align with sustainability trends.

Urbanization and rapid residential development further fuel the market, with property owners and builders actively seeking efficient power management solutions. The adoption of home automation systems is pushing demand for intelligent motor starters capable of optimizing electrical performance while ensuring safety. Additionally, regulatory policies supporting energy efficiency are accelerating the deployment of these systems. Technological advancements, including smart monitoring features and enhanced durability, are making these starters more attractive for residential applications. As the residential sector evolves with a focus on high-performance, space-saving, and eco-friendly electrical infrastructure, the demand for automatic motor starters will continue to surge worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.26 Billion |

| Forecast Value | $2 Billion |

| CAGR | 4.6% |

The market is categorized based on voltage into low, medium, and high-voltage segments. Among these, the medium-voltage segment is poised for significant growth, projected to generate USD 700 million by 2034. These systems are increasingly recognized for their efficiency, compact design, and easy installation, making them ideal for modern residential setups. Homeowners looking for space-saving and simplified electrical solutions are favoring medium-voltage motor starters, further driving their adoption across various regions.

In terms of phase, the residential automatic motor starter market is divided into single-phase and three-phase systems. Single-phase motor starters held a dominant 52.7% share in 2024, with demand expected to rise steadily. The growing popularity of smart homes, the heightened emphasis on sustainability, and the need for energy-efficient electrical solutions are all key contributors to this trend. As households aim to optimize energy consumption without compromising reliability, single-phase starters are emerging as a cost-effective choice for modern electrical systems.

The United States residential automatic motor starter market is on track to reach USD 200 million by 2034, driven by the increasing adoption of energy-efficient smart solutions. With a surge in urbanization, a boom in new residential construction, and a heightened focus on efficient power management, the demand for advanced motor starters is rising. Homeowners and builders alike are recognizing the benefits of integrating these systems into modern homes, ensuring optimal electricity usage while enhancing safety and convenience. As the market evolves, the role of automatic motor starters in shaping sustainable residential infrastructure will only become more prominent.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Netherlands

- 7.3.8 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.4.6 New Zealand

- 7.4.7 Malaysia

- 7.4.8 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 South Africa

- 7.5.6 Nigeria

- 7.5.7 Kuwait

- 7.5.8 Oman

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 C&S Electric

- 8.3 CHINT Group

- 8.4 Danfoss

- 8.5 Eaton

- 8.6 Emerson Electric

- 8.7 Fuji Electric

- 8.8 Havells India

- 8.9 L&T Electrical and Automation

- 8.10 Lovato Electric

- 8.11 Mitsubishi Electric

- 8.12 Rockwell Automation

- 8.13 Schneider Electric

- 8.14 Siemens

- 8.15 SKN-Bentex Group

- 8.16 WEG

家庭能源管理系統供應商-評估10家家庭能源管理系統供應商的策略與執行:Guidehouse Research排行榜報告

家庭能源管理系統供應商-評估10家家庭能源管理系統供應商的策略與執行:Guidehouse Research排行榜報告 家庭能源管理系統 (HEMS) 市場 - 成長、未來展望、競爭分析,2025 年至 2033 年

家庭能源管理系統 (HEMS) 市場 - 成長、未來展望、競爭分析,2025 年至 2033 年 全球家庭能源管理系統市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球家庭能源管理系統市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年至 2033 年按產品類型、通訊技術、系統類型和地區分類的家庭能源管理系統市場報告

2025 年至 2033 年按產品類型、通訊技術、系統類型和地區分類的家庭能源管理系統市場報告 家庭能源管理系統市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測家庭能源管理系統市場:按組件、技術、模組、部署、結構類型、應用分類 - 2025-2030 年全球預測

家庭能源管理系統市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測家庭能源管理系統市場:按組件、技術、模組、部署、結構類型、應用分類 - 2025-2030 年全球預測 智慧家庭能源管理設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、通訊技術、地區和競爭細分,2019-2029F

智慧家庭能源管理設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、通訊技術、地區和競爭細分,2019-2029F 家庭能源管理系統(HEMS)市場 – 第二版

家庭能源管理系統(HEMS)市場 – 第二版 全球家庭能源管理系統市場,2024-2028

全球家庭能源管理系統市場,2024-2028 家庭能源管理:發電、消耗、需求回應

家庭能源管理:發電、消耗、需求回應