|

市場調查報告書

商品編碼

1277028

智能商業建築中的物聯網:市場規模和競爭格局(2023-2028)The Internet of Things in Smart Commercial Buildings 2023 to 2028: Market Sizing & Competitive Landscape |

||||||

本報告總結並提供了全球商業建築物聯網市場規模(至 2028 年)和競爭格局的最新分析結果。

本報告重點關注商業房地產市場,全面評估了物聯網市場的市場規模、應用和機會,以及主要促進因素和障礙。

主要問題

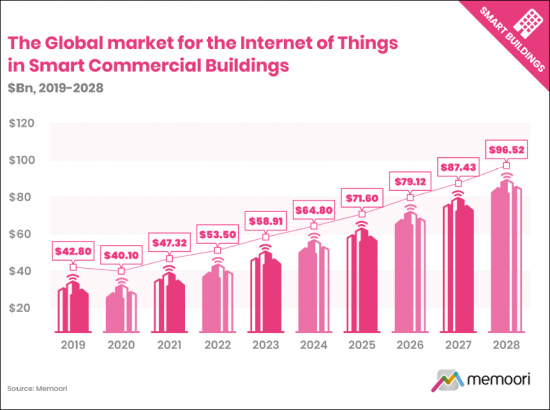

- 用於智能商業建築 (BIoT) 的 IoT(物聯網)市場規模有多大? : 根據最新分析,到 2022 年,BIoT 市場將增長至 535 億美元,較 2021 年增長 13%。 包括整體經濟復甦慢於預期、芯片組短缺和供應鏈中斷在內的幾個因素低於我們 13.8% 的預測。 BIoT 的市場規模預計將在 2022 年至 2028 年間以 10.33% 的複合年增長率增長,達到 965 億美元。

- BIoT 市場採用的促進因素是什麼? :房地產企業的投資不僅是為了讓他們的資產更具可持續性,也是為了提高他們的業績並推動更高的租金和收益率。 隨著能源成本預計將繼續上升,對節能技術和可持續解決方案的關注仍將是許多公司的首要任務。

- BIoT 市場面臨哪些挑戰和障礙? :網絡安全是越來越多越來越容易受到網絡攻擊的智能建築的重要考慮因素。 智能建築系統和設備通常缺乏動態修補功能,設施管理團隊可能缺乏必要的 IT 技能來管理網絡安全。

建築行業正朝著可持續發展和降低能源消耗的方向發展。 根據 EIA 的 2018 年 CBECS 消費和支出調查,與 2012 年相比,2018 年商業建築每平方英尺建築面積的能源消耗下降了 12%。 然而,由於建築和建築施工佔全球能源消耗的三分之一和二氧化碳排放量的近 40%,建築行業尚未達到未來可持續發展所需的目標。

要到 2050 年實現淨零排放,建築業主和運營商需要加大新建和翻新力度。 國際能源署呼籲到 2030 年將改造率從目前的不到 1% 每年提高 2.5%。

本報告中提及的物聯網公司:(節選)

|

|

內容

前言

執行摘要

第 1 章簡介

- 智能商業建築物聯網市場概覽

- BIOT供應鏈

第 2 章市場規模和區域分析

- 全球 BIoT 市場預測

- 市場收入:按硬件、按軟件、按服務

- 市場收入:按行業分類

- 市場收入:按應用分類

- BIoT 市場分析:按地區

- 按地區比較

- 北美

- 拉丁美洲

- 亞太地區

- 歐洲

- 中東和非洲

第 3 章BIoT市場應用

- 安全和訪問控制

- 影像監控

- 影像管理系統 (VMS)

- VSaaS(視頻監控即服務)

- 訪問控制

- 用於安全和訪問控制的 AI 應用程序

- 能源管理和環境控制

- 物聯網和人工智能在能源管理中的作用

- 實時能源跟蹤和分析

- 暖通空調優化

- 平衡優先級並集成多個系統

- 能源管理和環境控制的未來

- 網格互動建築

- 需求響應和負載管理

- 需求側管理策略

- 減載和調峰

- 可再生能源與 PEV 的整合

- 網格交互構建領域的領先公司

- 智能運維

- 空間、佔用率、人員流動

- 空氣質量

- 衛生/健康/保健

- 智能照明

- 租戶和工作經驗

- 消防與安全

- 廢物和水管理

- 水資源管理

- 廢物管理

- 數位孿生

- 數位孿生定義

- 數位孿生、BIM(建築資訊模型)和物聯網之間的關係

- 數位孿生的 3D 建模

- 挑戰和批評

- 成功的數位孿生的先決條件

- 市場認可度和採用率

- 數位孿生供應商

第 4 章智能建築物聯網平台

- 物聯網平台

- BIoT平台生態系統

- BIoT平台產品

第 5 章市場展望和用例:按市場部門分類

- 商業辦公室

- 零售

- 零售業務業績

- 零售業的未來

- 零售業的物聯網機遇

- 酒店業

- 酒店

- 餐廳/餐飲服務

- 數據中心

- 其他行業

- 交通

- 公共集會/場所

- 倉庫

- 小建築

第 6 章 BIoT 市場 - 採用的促進因素

- 經濟和商業促進因素

- 降低運營成本並提高效率

- 租戶優先級和資產價值

- 工作場所的要求和期望

- 技術促進因素

- 技術成本

- 數據量和可訪問性

- 新技術

- 能源效率和可持續性的促進因素

- 商業建築領域的可持續發展記錄

- 翻新的重要性

- 企業立場、投資和舉措

- 與能源成本相關的因素

- ESG報告

- 應對物聯網的不利影響

- 促進健康和福祉的因素

- 政府政策和法規

- 環境和可持續發展法規

- 政府獎勵和補貼

- 物聯網、數據、網絡安全法規

- 其他投資和政策促進因素

- 標準和認證

- 建築標準和認證的變化

- 智能數位連接

- 可持續性、能源和 ESG 績效

- 健康與幸福

- 網絡安全標準和要求

第 7 章 BIoT 市場:挑戰與障礙

- 技術問題

- 網路安全

- 網路保險

- 數據隱私

- 系統複雜性和互操作性

- 數據相關問題

- 抵制行業的變化和發展

- 抵制 CRE 行業的變革

- 行業發展和轉型的促進因素

- 領導、調試、採購

- 物聯網項目負責人和決策者

- 構建生命週期

- 利益相關方的調試、採購和協調

- 調試和採購挑戰

- 利益相關者在整個建築生命週期中的優先事項

- 利益相關者之間實現協調

- 物聯網技術與建築設計的有效融合

- IT/OT 利益相關者

- 每位房東/房客的獎勵

- 成本趨勢和業務案例

- 物聯網項目成本

- 商業案例中的趨勢

第 8 章競爭格局

This Report is a new 2023 Study which Makes an Objective Assessment of the Commercial Building IoT Market Size & Competitive Landscape to 2028

Our new report focuses on market sizing, applications and opportunities in the Internet of Things market, as well as a comprehensive evaluation of the drivers and barriers to adoption that are specific to the Commercial Real Estate sector.

New for 2023, it INCLUDES at no extra cost, a spreadsheet containing the data from the report AND high-resolution presentation charts showing the key findings. It is the second instalment of a two-part series, with the first report (published last month) covering IoT Device Projections, Adoption & Meta-Trends Analysis. These reports are included in our 2023 Premium Subscription Service.

KEY QUESTIONS ADDRESSED:

- What is the Size of the Internet of Things Market in Smart Commercial Buildings (BIoT)? Our latest analysis indicates that the BIoT market grew to $53.5 billion in 2022, representing a 13% rise from 2021. Performance was slightly down from our forecast of 13.8% for the year due to several factors, including a slower-than-anticipated overall economic recovery, a lack of chipsets, and disrupted supply chains. Memoori forecasts that the BIoT market size will grow at a CAGR of 10.33% to $96.5 billion between 2022 and 2028.

- What is Driving BIoT Market Adoption? Real estate stakeholders are investing not only to improve the sustainability credentials of their assets but also to enhance their performance, resulting in better rent and yields. As rising energy costs are expected to continue increasing, the focus on energy-efficient technologies and sustainable solutions is likely to remain a significant priority for many companies.

- What Challenges & Barriers Does the BIoT Market Face? Cybersecurity is a crucial consideration for the growing number of smart buildings, which are increasingly susceptible to cyber attacks. Smart building systems and devices often lack dynamic patching capabilities, and facilities management teams may lack the IT skills required to manage cybersecurity.

The building sector is making progress towards sustainable development and reducing energy consumption. The EIA's 2018 CBECS consumption and expenditures survey found that commercial buildings consumed 12% less energy per square foot of floorspace in 2018 than in 2012. However, the building sector still falls short of the targets required for sustainable future development, as buildings and building construction contribute to one-third of global energy consumption and almost 40% of CO2 emissions.

To achieve net zero by 2050, building owners and operators must redouble their efforts in new construction and retrofits. The IEA is now calling for an increase in retrofit rates of 2.5% annually by 2030, up from less than 1% today.

WITHIN ITS 236 PAGES AND 26 CHARTS AND TABLES, THE REPORT FILTERS OUT ALL THE KEY FACTS AND DRAWS CONCLUSIONS, SO YOU CAN UNDERSTAND EXACTLY WHAT IS SHAPING THE FUTURE OF THIS GLOBAL IOT MARKET

- The Building Internet of Things market is complex and multifaceted, involving a wide range of players from traditional building automation companies to specialized manufacturers, ICT vendors, property firms, and software vendors offering middleware, platforms, and cloud-based data analytics services. While some companies offer end-to-end BIoT solutions, others specialize in specific areas such as data intelligence, automation, or energy optimization and analytics.

- The smart building startup landscape is also expanding rapidly, with a 20% increase in the number of new entrants founded since 2021. Consolidation is expected in the wider platforms space, but there remain considerable market opportunities for cloud-based software offerings for specialist applications or vertical markets.

- While the level of fragmentation in the BIoT market can act as a source of confusion and frustration for buyers, leading platform solution providers are beginning to emerge, and the user base seems likely to coalesce around a more limited number of platform providers.

This report provides valuable information to companies so they can improve their strategic planning exercises AND look at the potential for developing their business through mergers, acquisitions and alliances.

WHO SHOULD BUY THIS REPORT?

The information contained in this report will be of value to all those engaged in managing, operating and investing in commercial smart buildings (and their advisers) around the world. In particular, those wishing to understand exactly how the Internet of Things is impacting commercial real estate will find it most useful.

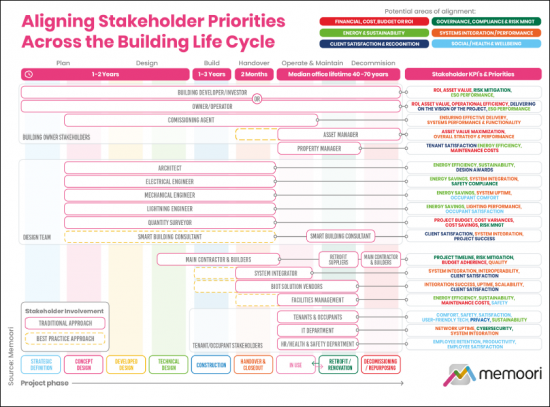

ALIGNING STAKEHOLDER PRIORITIES

The infographic below illustrates key stakeholders in a smart building project, their priorities and KPIs, and the project phases they might be involved in under traditional and best practice approaches. Encouraging collaboration, communication, and standardized practices among stakeholders can help bridge the gap and foster innovation.

The integration of Internet of Things technology into building design is a complex process that requires coordination and alignment among all parties involved. A comprehensive and cohesive design approach involving key stakeholders from the earliest stages leads to improved decision-making and better outcomes .

Internet of Things Companies Mentioned INCLUDE: (but NOT limited to)

|

|

Table of Contents

Preface

The Executive Summary

1. Introduction

- 1.1. Overview of the IoT Market in Smart Commercial Buildings

- 1.2. The BIOT Supply Chain

2. Market Sizing and Regional Analysis

- 2.1. BIoT Global Market Forecasts

- 2.1.1. Market Revenue by Hardware, Software & Services

- 2.1.2. Market Revenue by Vertical

- 2.1.3. Market Revenue by Application

- 2.2. BIoT Market Analysis by Region

- 2.2.1. Regional Comparisons

- 2.2.2. North America

- 2.2.3. Latin America

- 2.2.4. Asia Pacific

- 2.2.5. Europe

- 2.2.6. Middle East & Africa

3. BIoT Market Applications

- 3.1. Security & Access Control

- 3.1.1. Video Surveillance

- 3.1.2. Video Management Systems (VMS)

- 3.1.3. Video Surveillance as a Service (VSaaS)

- 3.1.4. Access Control

- 3.1.5. AI Applications for Security & Access Control

- 3.2. Energy Management & Environmental Control

- 3.2.1. The Role of IoT and AI in Energy Management

- 3.2.2. Real-Time Energy Tracking and Analysis

- 3.2.3. HVAC Optimization

- 3.2.4. Balancing Priorities and Integrating Multiple Systems

- 3.2.5. The Future of Energy Management and Environmental Control

- 3.3. Grid Interactive Buildings

- 3.3.1. Demand Response and Load Management

- 3.3.2. Demand-Side Management Strategies

- 3.3.3. Load Shedding and Peak Shaving

- 3.3.4. Integrating Renewables and PEV's

- 3.3.5. Leading Players in Grid Interactive Buildings

- 3.4. Smart Operations & Maintenance

- 3.5. Space, Occupancy & People Movement

- 3.6. Air Quality

- 3.7. Hygiene, Health & Wellness

- 3.8. Smart Lighting

- 3.9. Tenant & Workplace Experience

- 3.10. Fire & Safety

- 3.11. Waste & Water Management

- 3.11.1. Water Management

- 3.11.2. Waste Management

- 3.12. Digital Twin

- 3.12.1. Defining Digital Twins

- 3.12.2. The Relationship Between Digital Twins, BIM & IoT

- 3.12.3. 3D Modelling for Digital Twins

- 3.12.4. Challenges & Criticisms

- 3.12.5. Prerequisites for Successful Digital Twins

- 3.12.6. Market Perceptions & Adoption Rates

- 3.12.7. Digital Twin Vendors

4. Smart Building IoT Platforms

- 4.1. IoT Platforms

- 4.2. The BIoT Platform Eco-System

- 4.3. BIoT Platform Offerings

5. Prospects & Use Cases by Market Vertical

- 5.1. Commercial Offices

- 5.2. Retail

- 5.2.1. Retail Sector Performance

- 5.2.2. The Future of Retail

- 5.2.3. Retail Sector IoT Opportunities

- 5.3. Hospitality

- 5.3.1. Hotels

- 5.3.2. Restaurants & Food Services

- 5.4. Data Centers

- 5.5. Other Verticals

- 5.5.1. Transport

- 5.5.2. Public Assembly/Venues

- 5.5.3. Warehouses

- 5.6. Smaller Buildings

6. BIoT Market - Adoption Drivers

- 6.1. Economic & Business Drivers

- 6.1.1. Operational Cost Savings and Efficiency Gains

- 6.1.2. Tenant Priorities & Property Value

- 6.1.3. Workplace Demands & Expectations

- 6.2. Technology Drivers

- 6.2.1. Technology Costs

- 6.2.2. Data Volume & Accessibility

- 6.2.3. Emerging Technologies

- 6.3. Energy Efficiency & Sustainability Drivers

- 6.3.1. Sustainability Performance in the Commercial Building Sector

- 6.3.2. The Critical Importance of Retrofits

- 6.3.3. Corporate Attitudes, Investments, and Initiatives

- 6.3.4. Energy Cost-related Drivers

- 6.3.5. ESG Reporting

- 6.3.6. Countering the Adverse Impacts of the IoT

- 6.4. Health & Wellbeing Drivers

- 6.5. Government Policies & Regulations

- 6.5.1. Environmental and Sustainability Regulations

- 6.5.2. Government Incentives and Subsidies

- 6.5.3. IoT, Data & Cybersecurity Regulations

- 6.5.4. Other Investment or Policy Drivers

- 6.6. Standards & Certification

- 6.6.1. The Evolving Landscape of Building Standards & Certifications

- 6.6.2. Smart & Digital connectivity

- 6.6.3. Sustainability, Energy & ESG performance

- 6.6.4. Health & Wellbeing

- 6.6.5. Cybersecurity Standards and Requirements

7. BIoT Market - Challenges & Barriers

- 7.1. Technology Challenges

- 7.1.1. Cybersecurity

- 7.1.2. Cyber Insurance

- 7.1.3. Data Privacy

- 7.1.4. Systems Complexity & Interoperability

- 7.1.5. Data Related Challenges

- 7.2. Resistance to Change and Industry Evolution

- 7.2.1. Resistance to Change in the CRE Industry

- 7.2.2. Industry evolution and transition drivers

- 7.3. Leadership, Commissioning & Procurement

- 7.3.1. IoT Project Leadership & Decision Makers

- 7.4. Building Life Cycles

- 7.5. Commissioning, Procurement & Stakeholder Alignment

- 7.5.1. Commissioning & Procurement Challenges

- 7.5.2. Stakeholder Priorities Across the Building Life Cycle

- 7.5.3. Achieving Stakeholder Alignment

- 7.5.4. Effective Integration of IoT Technology into Building Design

- 7.5.5. IT vs OT Stakeholders

- 7.5.6. Landlord/Tenant split incentives

- 7.6. Costs & Business Case Development

- 7.6.1. IoT Project Costs

- 7.6.2. Business Case Development

8. The Competitive Landscape

List of Charts and Figures

- Fig 1.1 - The Internet of Things in Smart Commercial Buildings 2023 v5.1

- Fig 1.2 - The BIoT Supply Chain

- Fig 2.1 - The Global Market for the Internet of Things in Smart Commercial Buildings, $Bn 2019-2028

- Fig 2.2 - The Global Market for the Internet of Things in Smart Commercial Buildings, Breakdown by Hardware, Software, & Services, $Bn 2022-2028

- Fig 2.3 - Market Breakdown by Hardware, Software & Services, Market Size $Bn, % of Total Market

- Fig 2.4 - The Market for the Internet of Things in Smart Commercial Buildings Market by Vertical, $Bn 2022 & 2028

- Fig 2.5 - The Market for the Internet of Things in Smart Commercial Buildings Market by Application, $Bn 2022 & 2028

- Fig 2.6 - Regional Growth Indicators

- Fig 2.7 - The Market for the Internet of Things in Smart Commercial Buildings Market by Region 2022 to 2028, % of Global Market

- Fig 2.8 - BIoT Related Patent Applications by Country, May 2023

- Fig 2.9 - Percentage Share of Academic Publications, Selected Technologies

- Fig 2.10 - Frontier Technology Readiness by Region

- Fig 2.11 - The Market for the Internet of Things in Smart Commercial Buildings North America, $Bn 2022 - 2028

- Fig 2.12 - The Market for the Internet of Things in Smart Commercial Buildings Latin America, $Bn 2022 - 2028

- Fig 2.13 - The Market for the Internet of Things in Smart Commercial Buildings Asia Pacific, $Bn 2022 - 2028

- Fig 2.14 - The Market for the Internet of Things in Smart Commercial Buildings Europe, $Bn 2022 - 2028

- Fig 2.15 - The Market for the Internet of Things in Smart Commercial Buildings Middle East & Africa, $Bn 2022 - 2028

- Fig 4.1 - Typical IoT Platform Functionality

- Fig 6.1 - Price Inflation for Information Technology, Hardware & Services since 1988

- Fig 6.2 - Non-Residential Building Sector CO2 Emissions 2010 - 2030

- Fig 6.3 - Buildings Share of Global Final Energy & CO2 Emissions 2021

- Fig 6.4 - Average Electricity & Gas Prices for Non-Household Consumers

- Fig 7.1 - Building Component Life Cycles

- Fig 7.2 - Aligning Stakeholder Priorities Across the Building Life Cycle

日本物聯網市場預測:2024-2032

日本物聯網市場預測:2024-2032 Geo IoT的技術·解決方案·用途·服務:2025~2030年

Geo IoT的技術·解決方案·用途·服務:2025~2030年 物聯網市場預測:連結數、收入和技術趨勢(2024-2032)

物聯網市場預測:連結數、收入和技術趨勢(2024-2032) 國際romingukorido市場:2020-2029年

國際romingukorido市場:2020-2029年 物聯網 (IoT) 市場規模、佔有率及成長分析(按組件、部署、組織規模、平台、技術、垂直產業和地區)-2025 年至 2032 年產業預測

物聯網 (IoT) 市場規模、佔有率及成長分析(按組件、部署、組織規模、平台、技術、垂直產業和地區)-2025 年至 2032 年產業預測 物聯網現況:2025年春季

物聯網現況:2025年春季 2025 年全球物聯網解決方案與服務市場報告

2025 年全球物聯網解決方案與服務市場報告 不斷發展的物聯網格局:穩定性、轉變和多樣化路徑

不斷發展的物聯網格局:穩定性、轉變和多樣化路徑 SPS Fair 2024:工業自動化最新趨勢

SPS Fair 2024:工業自動化最新趨勢 物聯網市場:2033 年市場分析與預測 - 按類型、產品、服務、技術、組件、應用、最終用戶、設備、部署、解決方案

物聯網市場:2033 年市場分析與預測 - 按類型、產品、服務、技術、組件、應用、最終用戶、設備、部署、解決方案