|

市場調查報告書

商品編碼

1435201

屋頂太陽能發電裝置:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Rooftop Solar Photovoltaic Installation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

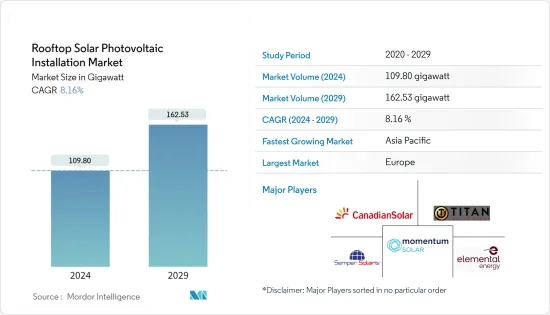

屋頂太陽能發電裝置市場規模預計到2024年為109.80吉瓦,預計到2029年將達到162.53吉瓦,在預測期內(2024-2029年)複合年成長率為8.16%。

2020 年,市場受到 COVID-19 的負面影響。目前市場處於大流行前的水平。

主要亮點

- 從長遠來看,政府的支持性政策(例如太陽能板安裝的激勵和稅收優惠、太陽能光伏安裝成本的降低以及電池板效率的提高)預計將在預測期內推動市場發展。

- 另一方面,中國和西方之間的地緣政治緊張局勢使得太陽能供應鏈極易受到破壞。由於幾個主要西方國家過度依賴中國的太陽能發電面板,導致進口禁令和關稅增加的地緣政治事件預計將限制市場。

- 儘管如此,新的技術進步和鈣鈦礦太陽能電池的發展預計將為未來屋頂太陽能發電安裝市場創造多個機會。

- 亞太地區是 2021 年屋頂太陽能裝置的最大市場。此外,由於中國和印度等多個新興經濟體的存在,該地區可能是預測期內成長最快的市場。

屋頂太陽能發電(PV)安裝市場趨勢

住宅屋頂安裝預計將主導市場

- 住宅部分包括個人住宅和多用戶住宅。與商業和工業屋頂系統相比,住宅屋頂系統較小。住宅屋頂太陽能發電系統的容量範圍通常高達 50 kW。

- 近年來,由於成本下降和政府支持政策,全球住宅屋頂太陽能發電系統的安裝量大幅增加。住宅屋頂太陽能裝置可以佈置為較小的配置,以供迷你電網或個人使用。在各國,居住者需要方便、負擔得起且可靠的電力選擇,對住宅屋頂系統的需求不斷增加。在許多國家,太陽能發電比從電網購買電力更具經濟吸引力。

- 例如,近年來,美國住宅屋頂太陽能光電裝置容量快速成長,住宅屋頂部分新增1,156兆瓦,特別是在2021年第四季。此外,根據太陽能產業協會的數據,屋頂太陽能安裝商在 2021 年完成了超過 50 萬個住宅計劃。 2021年住宅太陽能裝置量與前一年同期比較增30%,創下2015年以來的最高年度成長率。這種不斷成長的需求導致了住宅太陽能需求的增加。太陽能發電工程可歸因於較低的能源產出成本、極端天氣事件、太陽能儲存容量的增加以及全國家用電動車充電站數量的增加。 2017年,美國住宅太陽能裝置總量約2.2吉瓦,2021年將增加至4.2吉瓦。

- 2022年5月,歐盟委員會主席烏蘇拉·馮德萊恩宣布,到2029年,居民應在新住宅的屋頂安裝太陽能。俄羅斯和烏克蘭之間的衝突導致歐盟修改了其可再生能源目標,這可能是由於減少對石化燃料的依賴。此外,歐盟委員會將 2030 年可再生能源目標從 40% 提高到 45%。為了實現這一雄心勃勃的目標,政府計劃為主要可再生地區提供更快的許可流程。目前,許可過程需要六到九年的時間,但預計將縮短至一年。

- 歐盟也在推動太陽能板的本地生產。例如,Enel Green Power 與歐盟簽署了一項協議,擴建其在義大利的太陽能板超級工廠。在歐盟的資助下,Enel Green Power 的目標是將其發電量從目前的 200 兆瓦增加 15 倍,達到 3 吉瓦。該生產設施預計將於 2024 年 7 月運作。總投資約6億歐元,其中歐盟的資金預計約為1.18億歐元。這也將有助於在不久的將來降低屋頂太陽能板的成本,預計這將增加歐洲對住宅屋頂太陽能系統的需求。

- 近年來,中國、印度和澳洲等國政府大力推廣住宅領域太陽能計劃並降低安裝成本,增加了對住宅屋頂的需求。

- 例如,印度政府啟動了新能源和可再生能源部(MNRE)第二階段併網屋頂太陽能發電計畫。根據該計劃,2022年4月,泰米爾南都能源發展局發布競標,在泰米爾南都安裝12兆瓦併網住宅屋頂太陽能光電系統。同樣,特倫甘納邦可再生能源委員會公司已競標指定供應商興建50兆瓦併網住宅屋頂太陽能發電工程。

- 因此,由於上述幾點,預計住宅屋頂太陽能安裝市場將在預測期內佔據主導地位。

預計亞太地區將主導市場

- 近年來,亞太地區已成為太陽能裝置的主要市場。過去 10 年來,太陽能發電的平準化能源成本 (LCOE) 降低了 88% 以上。因此,印尼、馬來西亞和越南等該地區的新興國家增加了太陽能發電能力。總能源結構。

- 中國幾乎擁有全球所有最大的光伏(PV)製造公司和設施,全球近70%的光伏(PV)製造能力集中在中國。這些公司也控制多晶矽、矽錠和晶圓製造等其他業務,這些業務構成了太陽能板供應鏈不可或缺的一部分。與其他國家的太陽能設備製造商相比,全球太陽能供應鏈的卓越管理使中國製造商具有顯著優勢。

- 漢能迅速擴大了分散式屋頂太陽能發電能力,特別是在需求旺盛的東部沿海地區。然而,在78吉瓦的分散式太陽能發電容量中,只有20吉瓦來自住宅,約58吉瓦來自辦公大樓和工業建築。就工商業建築而言,投資者通常會租用屋頂,以折扣價向建築物業主供電,然後將其餘部分出售給電網。

- 2021年6月,國家能源局發布關於進行分散式太陽能發電地市級試點的通知,旨在增加屋頂太陽能發電量。 75個地級政府將選擇企業安裝分散式太陽能發電並開始測試。根據國家能源局的說法,所有擁有足夠屋頂、良好電網以及部署該計劃的技術和財政能力的縣都將有資格參加該計劃,該計劃將以連通性和網路升級的形式提供支持。表示將得到電網公司的支持。出口能源。此外,全縣黨建築屋頂比例不低於50%,醫院、學校等其他公共建築屋頂比例不低於0%,適合安裝屋頂太陽能。

- 據印度新能源和可再生能源部稱,截至2020年3月,總合36.69吉瓦的太陽能發電工程正在進行中,已發出意向書(LoI)但尚未委託,約18.47吉瓦的競標已發出但尚未投產。意向書尚未發出。 2020-21年,印度進口了價值25億美元的太陽能矽晶圓、電池、模組和逆變器。

- 屋頂太陽能在該國的普及不斷提高,可歸因於工商業消費者的高零售電價、有利的淨計量政策、企業社會責任計劃以及消費者意識的增強。

- 因此,由於上述幾點,亞太地區預計將在預測期內主導屋頂太陽能發電安裝市場。

屋頂光電安裝產業概況

屋頂太陽能發電市場本質上是整合的。市場主要企業包括(排名不分先後)Titan Solar Power NV Inc.、Momentum Solar、Canadian Solar Inc.、Elemental Energy Inc.和Semper Solaris Construction Inc.。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2027年之前的市場規模與需求預測(金額)

- 2027 年屋頂光伏 (PV) 市場(數量)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 安裝位置

- 住宅

- 商業/工業

- 地區

- 北美洲

- 亞太地區

- 歐洲

- 南美洲

- 中東/非洲

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Titan Solar Power NV Inc.

- Momentum Solar

- Canadian Solar Inc.

- Elemental Energy Inc.

- Semper Solaris Construction Inc.

- Pink Energy

- ReVision Energy LLC

- ADT Solar

- Baker Electric Home Energy

- Infinity Energy Inc.

第7章 市場機會及未來趨勢

The Rooftop Solar Photovoltaic Installation Market size is estimated at 109.80 gigawatt in 2024, and is expected to reach 162.53 gigawatt by 2029, growing at a CAGR of 8.16% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

- Over the long term, supportive government policies in the form of incentives and tax benefits for solar panel installation, declining PV installation costs, and rising panel efficiencies are expected to drive the market during the forecast period

- On the other hand, owing to the geopolitical tensions between China and western countries, the solar PV supply chain is highly vulnerable to disruptions. Geopolitical events leading to import bans and higher tariffs are expected to restrain the market, as several major western countries are overdependent on China for solar PV panels.

- Nevertheless, New technological advancements and development of perovskite solar cells are expected to create several opportunities for rooftop solar PV installation market in the future.

- Asia-Pacific was the largest market for rooftop solar PV installation in 2021. The region is also likely to be the fastest-growing market during the forecast period due to the presence of several developing economies, such as China and India.

Rooftop Solar Photovoltaic (PV) Installation Market Trends

Residential Rooftop Installation Expected to Dominate the Market

- The residential segment includes individual houses and residential building complexes. Residential rooftop mounted systems are small compared to commercial and industrial rooftop systems. The residential rooftop solar PV system typically has a capacity range of up to 50 kW.

- The deployment of residential rooftop solar PV systems has increased significantly in recent years across the world, owing to the declining costs and the government's supportive policies. Residential rooftop solar PV installations can be arranged in smaller configurations for mini-grids or personal use. There is a rise in demand for residential rooftop systems from various countries where residents need accessible, affordable, and reliable electricity options. In many countries, the electricity generated from solar PV electricity is more economically attractive than buying electricity from the grid.

- For instance, in the past couple of years, the United States experienced rapid growth in residential rooftop solar installed capacity, particularly in the fourth quarter of 2021, the residential rooftop segment added 1,156 MW. Furthermore, as per the solar energy industries association, rooftop solar installers completed more than 500,000 residential projects in 2021. Residential solar installations grew 30% year-over-year in 2021, the highest annual growth rate since 2015. This rise in demand for residential solar projects can be attributed to the reducing cost of energy generation cost, extreme weather events, improved solar storage capacity, and an increased number of home EV charging stations across the country. In 2017, the total residential solar PV installation in the United States was around 2.2 GW, which increased to 4.2 GW in 2021.

- In May 2022, the President of the European Commission, Ursula von der Leyen, announced residents to install the rooftop solar for new residential buildings by 2029. Due to the Russia-Ukraine conflict, the European Union has revised its renewable energy targets, which can be ascribed to the lowering the dependency on fossil fuels. Furthermore, the European Commission increased its renewable energy target for 2030 from 40% to 45%. To achieve this ambitious target, the government is planning to provide renewable go-to-areas where governments can give a quicker permitting process. Currently, the permitting process takes six to nine years, which is expected to bring down to one year.

- The European Union is also promoting the local manufacturing of solar panels. For instance, Enel Green Power signed a deal with the European Union to scale up a solar panel Gigafactory in Italy. Enel Green Power, with funding from European Union, aims to raise its production by fifteen-fold to 3 GW from the current 200 MW. The production facility is expected to be commissioned by July 2024. The total investment is around EUR 600 million, and European Union funding will likely be around EUR 118 million. This will also help to reduce the rooftop solar panel cost in the near future, which is expected to boost the demand for residential rooftop solar systems in Europe.

- The demand for residential rooftops has increased in countries, such as China, India, and Australia, in the past couple of years due to government initiatives to promote solar energy projects in the residential sector and reduced installation costs.

- For instance, the Government of India initiated phase II of the Ministry of New and Renewable Energy's (MNRE) grid-connected rooftop solar program. Under this program, in April 2022, the Tamil Nandu energy development agency issued a tender to install 12 MW of grid-connected residential rooftop solar systems in Tamil Nandu. Similarly, Telangana state's Renewable Energy Department Corporation invited bids to appoint suppliers to build 50 MW of grid-connected residential rooftop solar projects.

- Therefore, owing to the above points, residential rooftop solar PV installation market is expected to dominate the market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific, in recent years, has been the primary market for solar energy installations. The Levelized Cost of Energy (LCOE) for solar PV in the last decade reduced by more than 88%, because of which developing countries in the region, such as Indonesia, Malaysia, and Vietnam, saw an increase in solar energy installation capacity in their total energy mix.

- China is home to nearly all the largest solar photovoltaic (PV) manufacturing companies and facilities globally, with nearly 70% of the global solar PV manufacturing capacity situated in China. These companies also dominate other businesses such as polysilicon, ingot, and wafer-making, which form an integral part of the solar panel supply chain. This extraordinary control of the global solar PV supply chain puts Chinese manufacturers at a greater advantage when compared to solar equipment manufacturers from other countries.

- hina has been rapidly expanding distributed rooftop solar PV capacity, especially in the eastern coastal regions, where the demand is higher. However, only 20 GW of the 78 GW of distributed solar capacity is residential, and around 58 GW is generated on offices and industrial buildings. For C&I buildings, investors will usually lease a rooftop, provide power to the building owner at a discount, and sell the remainder to the grid.

- In June 2021, China's National Energy Administration (NEA) published a notice on county-level trials of distributed solar power generation, designed to boost rooftop solar. 75 county-level governments have picked firms to install distributed solar and are set to start trials. According to the NEA, any county equipped with appropriate rooftops, good grid access and the technical and financial capacity to roll out the programme will be eligible for the program and will be helped by electricity grid companies in the form of provision of connections and network upgradations to export energy. Additionally, at least 50% of the rooftops of a county's Party and government buildings and 0% of other public buildings such as hospitals and schools should be suitable for the installation of rooftop solar PV.

- According to the Indian Ministry of New and Renewable Energy, as of March 2020, 36.69 GW of total solar projects are in the pipeline for which Letter of Intent (LoI) has been issued but not commissioned and for around 18.47 GW tenders have been issued but LoI are yet to be issued.. In 2020-21, India imported solar wafers, cells, modules and inverters worth USD 2.5 billion.

- The increased adoption of rooftop solar in the country can be attributed to high retail tariffs for C&I consumers, favorable net metering policies, corporate social responsibility programs and increased consumer awareness.

- Therefore, owing to the above points, Asia-Pacific is expeceted to dominate the rooftop solar PV installation market during the forecast period.

Rooftop Solar Photovoltaic (PV) Installation Industry Overview

The rooftop solar installations market is consolidated in nature. Some of the key players in the market (in no particular order) include Titan Solar Power NV Inc, Momentum Solar, Canadian Solar Inc., Elemental Energy Inc., and Semper Solaris Construction Inc among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Rooftop Solar Photovoltaic (PV) Installed Market in GW, till 2027

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.2 Restraints

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Residential

- 5.1.2 Commercial and Industrial

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Asia-Pacific

- 5.2.3 Europe

- 5.2.4 South America

- 5.2.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Titan Solar Power NV Inc.

- 6.3.2 Momentum Solar

- 6.3.3 Canadian Solar Inc.

- 6.3.4 Elemental Energy Inc.

- 6.3.5 Semper Solaris Construction Inc.

- 6.3.6 Pink Energy

- 6.3.7 ReVision Energy LLC

- 6.3.8 ADT Solar

- 6.3.9 Baker Electric Home Energy

- 6.3.10 Infinity Energy Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

DG 屋頂太陽能光電市場 - 全球產業規模、佔有率、趨勢、機會和預測,按容量(10 kW 以下、11 kW - 100 kW、100 kW 以上)、最終用戶(住宅、商業、工業)細分,按地區,按比賽,2020-2030F

DG 屋頂太陽能光電市場 - 全球產業規模、佔有率、趨勢、機會和預測,按容量(10 kW 以下、11 kW - 100 kW、100 kW 以上)、最終用戶(住宅、商業、工業)細分,按地區,按比賽,2020-2030F 亞太地區屋頂太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

亞太地區屋頂太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 屋頂太陽能光電市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署、按技術、按電網類型、按最終用戶、按地區和競爭細分,2019-2029F

屋頂太陽能光電市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署、按技術、按電網類型、按最終用戶、按地區和競爭細分,2019-2029F 屋頂太陽能發電市場:按電網類型、技術和最終用戶分類 - 2025-2030 年全球預測

屋頂太陽能發電市場:按電網類型、技術和最終用戶分類 - 2025-2030 年全球預測 太陽能屋頂系統市場:按類型、按系統類型、按屋頂類型、按技術、按組件、按最終用戶、按電網連接、按安裝 - 2025-2030 年全球預測

太陽能屋頂系統市場:按類型、按系統類型、按屋頂類型、按技術、按組件、按最終用戶、按電網連接、按安裝 - 2025-2030 年全球預測 屋頂太陽能光伏發電安裝市場評估:技術類型 (單結晶·多結晶·薄膜)·電網類型 (並聯型·離網)·展開 (住宅·商業·產業)·各地區的機會及預測 (2017-2031年)

屋頂太陽能光伏發電安裝市場評估:技術類型 (單結晶·多結晶·薄膜)·電網類型 (並聯型·離網)·展開 (住宅·商業·產業)·各地區的機會及預測 (2017-2031年) 屋頂太陽能EPC市場、機會、成長動力、產業趨勢分析與預測,2024-2032

屋頂太陽能EPC市場、機會、成長動力、產業趨勢分析與預測,2024-2032 全球屋頂太陽能光電市場規模研究(按部署、按技術、按電網類型、按最終用途和 2022-2032 年區域預測)

全球屋頂太陽能光電市場規模研究(按部署、按技術、按電網類型、按最終用途和 2022-2032 年區域預測) 全球屋頂太陽能市場

全球屋頂太陽能市場 屋頂太陽能市場:按部署、按技術、按電網類型、按最終用途:2023-2032 年全球機會分析和產業預測

屋頂太陽能市場:按部署、按技術、按電網類型、按最終用途:2023-2032 年全球機會分析和產業預測