|

市場調查報告書

商品編碼

1911823

RISC-V技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)RISC-V Tech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

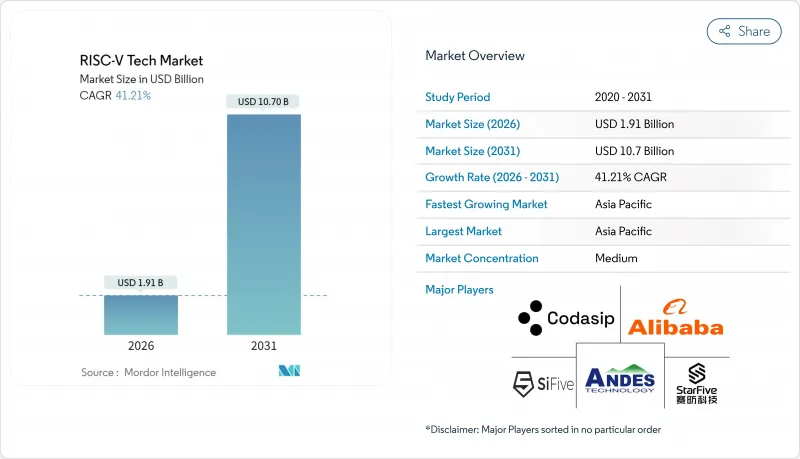

RISC-V 技術市場預計到 2025 年將達到 13.5 億美元,到 2026 年將成長到 19.1 億美元,到 2031 年將成長到 107 億美元,在預測期(2026-2031 年)內複合年成長率為 41.21%。

亞太地區在2024年佔據45.8%的主導地位,預計年複合成長率將達到65.2%,64位元核心在2024年佔據42.4%的主導地位,以及家用電子電器、汽車、物聯網和資料中心等領域的加速應用,是推動RISC-V技術成長的主要動力。可客製化的開放標準IP、美國、歐盟和中國的本土半導體項目,以及不斷擴展的檢驗生態系統,都在推動設計方案的採用,加快產品上市速度,並吸引新企業進入RISC-V技術市場。然而,由於ISA擴展分散導致的軟體複雜性、與ARM相比有限的向下相容性,以及成熟節點高階EDA人才的短缺,仍然是可能減緩RISC-V技術普及速度的重大阻力。

物聯網領域對成本高度敏感的設計要求,加上各國半導體自給自足政策,正在為RISC-V技術市場的垂直整合企業和區域領導者創造策略機會。 128位元核心的早期商業化、ISO 26262和ISO/SAE 21434認證IP的出現,以及透過RVA23規範推進的工具鏈標準化進程,都顯示RISC-V技術在高效能運算、汽車和工業自動化領域具有持續的擴充性。對開源硬體Start-Ups的投資熱情日益高漲,專利共用聯盟的建立,以及IP供應商和EDA供應商之間的合作,進一步降低了准入門檻,並加速了軟硬體一體化技術的整合。

全球 RISC-V 技術市場趨勢與洞察

快速採用以人工智慧/機器學習為中心的邊緣工作負載

邊緣人工智慧的日益普及推動了對具有可調延遲和能耗的模組化處理器的需求,而RISC-V技術市場憑藉其向量擴展能力,能夠加速攝影機、工業感測器和汽車系統中的神經網路推理,從而充分利用這一轉變帶來的機會。中國針對自主研發人工智慧晶片的半導體計畫進一步鞏固了這一優勢,最大限度地降低了其受西方出口管制的影響。這項開放標準的柔軟性催生了一個由IP供應商、工具鏈開發商和認證機構組成的網路,縮短了特定領域計算的設計週期,並為汽車安全和工廠自動化等領域的新型部署模式提供了可能。

軟體工具鏈成熟度吸引一級原始設備製造商

與 GCC、LLVM 和 RVA23 規範的增強相容性提供了統一的工具鏈和強大的 Java/Python 執行時間環境,從而增強了市場對 RISC-V 技術的信心。隨著 Intel、Google 和 NVIDIA 等主要支持者向上游貢獻程式碼,切換成本降低,一級 OEM 廠商現在可以使用單一開發工作流程支援多種效能等級。隨著軟體穩定性的提高,許多開發者和獨立軟體供應商 (ISV) 已開始移植其雲端、邊緣和嵌入式堆疊,進一步提升了 RISC-V 技術在企業和消費領域的市場滲透率。

碎片化的指令集架構擴展增加了軟體的複雜度。

由於 RISC-V 規範允許自訂擴展,數十家廠商紛紛推出各自的調整版本,這使得二進位檔案的可移植性和持續整合流程變得複雜。儘管 RVA23 規格規定了必要的 AI/ML 功能,但仍有許多選用功能,迫使作業系統廠商維護多個核心和工具鏈版本。這導致企業資訊長們必須同時維護基於 ARM 的平行藍圖,延緩了市場向 RISC-V 技術的全面過渡。

細分市場分析

截至2025年,64位設計將佔據RISC-V技術市場41.85%的佔有率,市佔率佔比最高。半導體製造商青睞64位元內核,因為主流Linux發行版、Chromebook韌體和容器化雲端軟體均已支援64位元內核,這使得設計人員無需進行大規模重新設計即可獲得大眾市場收益。未來三年,隨著工具鏈的日益成熟以及諸如SiFive的P870-D(可擴展至256個內核)等更大內核的藍圖,超大規模資料中心超大規模資料中心業者將能夠在百億億次級(PB級)性能水平上測試RISC-V機架。

同時,128 位元架構的複合年成長率高達 58.2%,在 RISC-V 技術市場中位居榜首。這是因為百萬兆級運算和參數超過一兆的 AI 模型需要龐大的位址空間和高精度的向量運算。基因組學和氣候模擬等領域的記憶體密集型工作負載也促使研究機構開發 128 位元 RISC-V叢集原型。廠商們正競相在作業系統、虛擬機器管理程式和編譯器層級添加軟體支持,目前 GCC 和 LLVM 的初始修補程式已經發布。雖然 32 位元核心在對成本敏感的物聯網節點領域仍然佔據主導地位,但隨著更多 MCU 廠商效仿瑞薩電子的做法,將其高階微控制器過渡到 64 位元位址空間,預計 32 位元核心的市場佔有率將逐漸萎縮。

區域分析

亞太地區預計到2025年將維持45.25%的營收佔比,並在2031年之前以62.7%的複合年成長率成長,這主要得益於國家主導的資本推動晶圓廠擴張、智慧財產權池建設和檢驗實驗室發展。中國的專利聯盟降低了訴訟風險,使阿里巴巴、天海德和百度等公司能夠擴大國內資料中心晶片和人工智慧晶片的規模。印度的「印度設計」宣傳活動正在增加新的組裝和測試能力,而Mindgrove計畫在2025年開始量產MCU。

歐洲正透過投資2.4億歐元,在DARE、eProcessor和SiPearl的Rhea等合資企業中建立自主化策略。 Rhea專案由巴塞隆納超級運算中心設計。這些專案利用RISC-V架構來規避地緣政治風險並提升供應鏈韌性,使其成為EuroHPC長期發展藍圖的基石。優先發展領域包括百萬兆級高效能運算、節能型邊緣節點和安全型國防電子設備。

北美依然是創新的搖籃,資金籌措Start-Ups津貼、跨境計劃人工智慧推理加速器和雲端到邊緣編配工具,所有這些都將推動RISC-V技術進入高性能市場。可客製化和降低成本是支撐轉型投入的因素。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速採用以人工智慧/機器學習為中心的邊緣工作負載

- 軟體工具鏈成熟度吸引一級原始設備製造商

- 國家半導體主權計畫(歐盟晶片法案、晶片與科學法案)

- 開放標準 IP 加速晶片上市

- 商業級檢驗生態系統(與 Imperus 和 Synopsys 合作)

- 第三方RISC-V加速器在特定領域運算中的興起

- 市場限制

- 碎片化的指令集架構擴展增加了軟體的複雜度。

- ARM指令集架構(ISA)的向後相容性保證有限

- 智慧財產權賠償和專利訴訟的不確定性

- 成熟節點RISC-V EDA人才短缺

- 產業價值鏈分析

- 監管環境

- 技術展望(晶片組和異質整合)

- 宏觀經濟因素如何影響市場

- 投資分析

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依處理器核心類型

- 32 位元

- 64 位元

- 128 位元

- 透過使用

- 智慧型手機

- 5G設備

- 資料中心

- 個人電腦和遊戲機

- 蜂巢式網路基礎設施

- 物聯網設備

- 其他用途

- 按最終用戶行業分類

- 運算和儲存

- 通訊基礎設施

- 家用電子電器

- 汽車和運輸設備

- 醫療保健

- 航太/軍事

- 產業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Alibaba Group Holding Limited(T-Head Semiconductor)

- Andes Technology Corporation

- Antmicro Sp. z oo

- Apex Semiconductor(Shenzhen)Co., Ltd.

- Bluespec, Inc.

- C-Sky Microsystems Co., Ltd.

- CloudBEAR OU

- EMBEdded Logic Solutions Ltd.

- GreenWaves Technologies SA

- Huawei Technologies Co., Ltd.(HiSilicon)

- Imagination Technologies Limited

- Lattice Semiconductor Corporation

- Microchip Technology Incorporated

- MipSoC Ltd.

- Red Hat, Inc.(SiFive joint IP)

- Rivos Inc.

- SiFive, Inc.

- StarFive Technology Co., Ltd.

- Ventana Micro Systems, Inc.

- Western Digital Corporation

第7章 市場機會與未來展望

The RISC-V Tech market was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.91 billion in 2026 to reach USD 10.7 billion by 2031, at a CAGR of 41.21% during the forecast period (2026-2031).

Growth is powered by Asia-Pacific's 45.8% 2024 leadership and its projected 65.2% CAGR, the 64-bit core's 42.4% 2024 domination, and accelerating adoption in consumer electronics, automotive, IoT, and data-center segments. Customizable open-standard IP, sovereign semiconductor programs in the United States, European Union, and China, and an expanding verification ecosystem are amplifying design wins, shortening time-to-market, and attracting new entrants to the RISC-V Tech market.However, software complexity from fragmented ISA extensions, limited backward compatibility compared with ARM, and a shortage of senior EDA talent in mature nodes remain substantial headwinds that could temper adoption momentum.

Cost-sensitive design requirements in IoT are dovetailing with national chip-sovereignty mandates, creating a strategic opening for vertically integrated players and regional champions across the RISC-V Tech market. Early commercialization of 128-bit cores, the arrival of ISO 26262- and ISO/SAE 21434-certified IP, and growing tool-chain standardization through the RVA23 Profile point to sustained scalability into high-performance computing, automotive, and industrial automation. Investors' willingness to deploy capital into open-hardware startups, as well as alliances that pool patents or link IP vendors with EDA suppliers, are further diluting the barriers to entry and accelerating convergence toward a more cohesive software and hardware stack.

Global RISC-V Tech Market Trends and Insights

Rapid proliferation of AI/ML-centric edge workloads

Edge AI adoption is lifting demand for modular processors able to tune latency and energy consumption, and the RISC-V Tech market is capitalizing on that pivot through vector extensions that accelerate neural-network inference in cameras, industrial sensors, and in-vehicle systems. Chinese semiconductor programs targeting indigenous AI chips have pressed home this advantage, minimizing vulnerability to Western export controls. The same open-standard flexibility is spawning a network of IP vendors, tool-chain developers, and certification bodies, compressing design cycles for domain-specific compute and helping to unlock new deployment models in automotive safety and factory automation.

Software tool-chain maturity attracting Tier-1 OEMs

Growing alignment around GCC, LLVM, and the RVA23 Profile has strengthened confidence in the RISC-V Tech market by offering unified toolchains and robust Java and Python runtimes. Flagship backers such as Intel, Google, and Nvidia are contributing code upstream, lowering switching costs and enabling Tier-1 OEMs to target multiple performance tiers under a single development workflow. As software stability improves, broad-based developers and ISVs have begun porting cloud, edge, and embedded stacks, moving the RISC-V Tech market deeper into enterprise and consumer segments.

Fragmented ISA extensions are increasing software complexity

Because the RISC-V specification permits custom extensions, dozens of vendors have introduced proprietary tweaks that complicate binary portability and continuous-integration pipelines. While the RVA23 Profile sets out mandatory AI/ML features, optional elements remain numerous, forcing OS vendors to maintain multiple kernels and tool-chain variants. Enterprise CIOs cite this as a reason to keep ARM-based roadmaps in parallel, delaying full commitment to the RISC-V Tech market.

Other drivers and restraints analyzed in the detailed report include:

- National chip-sovereignty programs (EU Chips Act, CHIPS and Science Act)

- Open-standard IP accelerating silicon time-to-market

- Limited backward-compatibility guarantees versus ARM ISA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

64-bit designs delivered 41.85% of the RISC-V Tech market share in 2025, translating into the largest slice of the RISC-V Tech market size. Semiconductor houses favor 64-bit cores because mainstream Linux distributions, Chromebook firmware, and containerized cloud software already support them, letting designers capture mass-market revenue without heavy re-engineering. Over the next three years, broader tool-chain maturity and big-core roadmaps such as SiFive's P870-D, which scales to 256 cores, will enable hyperscalers to test RISC-V racks at petascale performance levels.

The 128-bit cohort is registering a 58.2% CAGR, the fastest within the RISC-V Tech market, as exascale computing and AI models larger than 1 trillion parameters demand huge address spaces and high-precision vector math. Memory-intensive workloads in genomics and climate simulation are also nudging research centers to prototype 128-bit RISC-V clusters. Vendors are racing to add software support at the operating-system, hypervisor, and compiler levels, with early patches already appearing in GCC and LLVM. Although 32-bit cores remain the go-to choice for cost-sensitive IoT nodes, their share will compress modestly as more MCU vendors follow Renesas in migrating premium microcontrollers to 64-bit address spaces.

The RISC-V Tech Market Report is Segmented by Processor Core Type (32-Bit, 64-Bit, 128-Bit), Application (Smartphones, 5G Devices, Data Centers, and More), End-User Industry (Computing and Storage, Consumer Electronics, Medical, Industrial, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 45.25% of 2025 revenue and will grow at a 62.7% CAGR through 2031 as state-led capital drives fab expansion, IP pooling, and verification labs. China's patent alliance reduces litigation hazards and empowers firms like Alibaba, T-Head, and Baidu to scale indigenous data-center and AI silicon. India's design-in-India campaigns are adding new assembly and test capacity, with Mindgrove planning volume MCU shipments in 2025.

Europe is carving an autonomy pathway through EUR 240 million in joint ventures such as DARE, eProcessor, and SiPearl's Rhea, engineered at the Barcelona Supercomputing Center. These programs leverage RISC-V to hedge geopolitical risk and promote supply-chain resilience, making the architecture a linchpin of EuroHPC's long-term road map. Focus areas include exascale HPC, energy-efficient edge nodes, and secure defense electronics.

North America remains the innovation crucible: new funding for Rivos, Tenstorrent, and other Silicon Valley startups underscores deep-tech investor confidence. CHIPS Act grants reinforce domestic prototyping capacity, while cross-border projects with Japanese partners accelerate 2 nm process adoption. Regional priorities include chiplets, low-power AI inference accelerators, and cloud-to-edge orchestration tools, all of which extend the reach of the RISC-V Tech market into high-performance segments where customization and license savings justify transition costs.

- Alibaba Group Holding Limited (T-Head Semiconductor)

- Andes Technology Corporation

- Antmicro Sp. z o.o.

- Apex Semiconductor (Shenzhen) Co., Ltd.

- Bluespec, Inc.

- C-Sky Microsystems Co., Ltd.

- CloudBEAR OU

- EMBEdded Logic Solutions Ltd.

- GreenWaves Technologies S.A.

- Huawei Technologies Co., Ltd. (HiSilicon)

- Imagination Technologies Limited

- Lattice Semiconductor Corporation

- Microchip Technology Incorporated

- MipSoC Ltd.

- Red Hat, Inc. (SiFive joint IP)

- Rivos Inc.

- SiFive, Inc.

- StarFive Technology Co., Ltd.

- Ventana Micro Systems, Inc.

- Western Digital Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid proliferation of AI/ML-centric edge workloads

- 4.2.2 Software toolchain maturity attracting Tier-1 OEMs

- 4.2.3 National chip-sovereignty programs (EU Chips Act, CHIPS and Science Act)

- 4.2.4 Open-standard IP accelerating silicon time-to-market

- 4.2.5 Commercial-grade verification ecosystems (imperas, Synopsys partnerships)

- 4.2.6 Emergence of 3rd-party RISC-V accelerators for domain-specific compute

- 4.3 Market Restraints

- 4.3.1 Fragmented ISA extensions increasing software complexity

- 4.3.2 Limited backward-compatibility guarantees vs. ARM ISA

- 4.3.3 IP indemnification and patent-litigation uncertainties

- 4.3.4 Scarcity of RISC-V ready EDA talent in mature nodes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Chiplet and Heterogenous Integration)

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Processor Core Type

- 5.1.1 32-bit

- 5.1.2 64-bit

- 5.1.3 128-bit

- 5.2 By Application

- 5.2.1 Smartphones

- 5.2.2 5G Devices

- 5.2.3 Data Centers

- 5.2.4 Personal Computers and Game Consoles

- 5.2.5 Cellular Network Infrastructure

- 5.2.6 IoT Devices

- 5.2.7 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Computing and Storage

- 5.3.2 Communication Infrastructure

- 5.3.3 Consumer Electronics

- 5.3.4 Automotive and Transportation

- 5.3.5 Medical

- 5.3.6 Aerospace and Military

- 5.3.7 Industrial

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South-East Asia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Alibaba Group Holding Limited (T-Head Semiconductor)

- 6.4.2 Andes Technology Corporation

- 6.4.3 Antmicro Sp. z o.o.

- 6.4.4 Apex Semiconductor (Shenzhen) Co., Ltd.

- 6.4.5 Bluespec, Inc.

- 6.4.6 C-Sky Microsystems Co., Ltd.

- 6.4.7 CloudBEAR OU

- 6.4.8 EMBEdded Logic Solutions Ltd.

- 6.4.9 GreenWaves Technologies S.A.

- 6.4.10 Huawei Technologies Co., Ltd. (HiSilicon)

- 6.4.11 Imagination Technologies Limited

- 6.4.12 Lattice Semiconductor Corporation

- 6.4.13 Microchip Technology Incorporated

- 6.4.14 MipSoC Ltd.

- 6.4.15 Red Hat, Inc. (SiFive joint IP)

- 6.4.16 Rivos Inc.

- 6.4.17 SiFive, Inc.

- 6.4.18 StarFive Technology Co., Ltd.

- 6.4.19 Ventana Micro Systems, Inc.

- 6.4.20 Western Digital Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

RISC-V 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

RISC-V 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 RISC-V技術市場,規模,佔有率,趨勢,產業分析報告:各產品類型,各用途,各終端用戶,各地區-2025年~2034年市場預測

RISC-V技術市場,規模,佔有率,趨勢,產業分析報告:各產品類型,各用途,各終端用戶,各地區-2025年~2034年市場預測 RISC-V技術的全球市場

RISC-V技術的全球市場