|

市場調查報告書

商品編碼

1522857

光電:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Optoelectronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

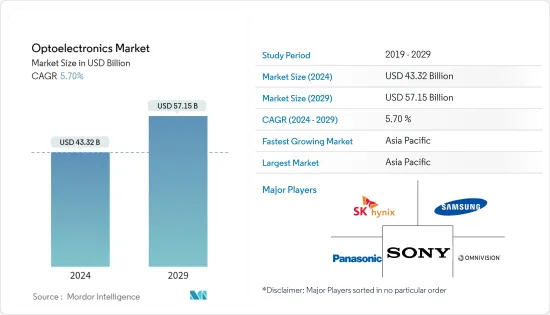

預計2024年光電市場規模為433.2億美元,預計2029年將達571.5億美元,在預測期內(2024-2029年)複合年成長率為5.70%。

主要亮點

- 一些市場推動因素正在增加對研究市場的需求。目前光電子學的市場趨勢集中在各種裝置的小型化、系統的最高整合度,例如發光二極體陣列、雷射陣列以及在同一晶片上與其他電子元件的整合系統。

- 光纖通訊、光儲存、光學成像領域的整合也正在推動光電子市場的發展。此外,對智慧消費電子產品和下一代技術不斷成長的需求預計將推動光電子產品的採用。

- 由於消費者對更好性能和更高解析度的需求不斷成長,對 LED 的高需求使其成為電子設備顯示技術的行業標準。 LED 用於手錶、電腦零件、醫療設備、光纖通訊、開關、消費性電子產品和 7 段顯示器等領域。

- 此外,光電裝置也用於各種消費性電子產品,從音訊技術到生物醫學設備。該技術的工業應用的增加和 Li-Fi 市場的擴大也促進了市場的成長。 Li-Fi 是一種利用紅外線和可見頻譜進行高速資料通訊的無線通訊技術。 Li-Fi技術傳輸資料的速度非常快,每秒鐘可以傳輸224GB的資料。

光電市場趨勢

消費性電子產品大幅成長

- 光電子產品用於消費性電子市場的各種應用。 LED 徹底改變了照明系統,並用於電腦組件、手錶、開關、消費性電子產品等。智慧型手錶使用光電二極體等光電感測器來監測使用者的心率。 CMOS 影像感測器通常用於智慧型手機、平板電腦和數位單眼反光 (DSLR) 相機。 5G 網路的擴展以及具有先進技術和功能的新產品的推出正在推動智慧型手機、平板電腦和數位單眼相機的採用。混合實境耳機市場的擴張也在推動市場研究。

- 隨著5G智慧型手機的普及,許多公司都推出了針對5G智慧型手機的影像感測器,這對市場做出了積極的貢獻。例如,2022年,Google在印度推出了支援5G網路的Pixel 6a、Pixel 7和Pixel 7 Pro。 GooglePixel 6a支援19個5G頻段,而Pixel 7和7 Pro則支援22個5G頻段。

- 據GSMA稱,拉丁美洲已進入5G時代,預計到2022年將有1500萬個連接。到 2025 年,5G 預計將佔該地區總連接數的 12%,其中一些國家,特別是巴西,這一比例將達到 20%,高於地區平均水平。

- 此外,根據愛立信的數據,到2028年,西歐的智慧型手機用戶數將達到4.59億。截至 2022 年,西歐智慧型手機用戶數約為 4.4 億。

- 混合實境耳機市場的擴張也在推動市場研究。例如,2023 年 6 月,蘋果發布了 Vision Pro,這是一款配備 3D 相機的混合實境耳機,可協助用戶拍攝 3D 太空照片和影片。

- 目前,大多數 AR 耳機都依賴一個或多個專用影像感測器,例如將調變紅外線光源與電荷耦合元件 (CCD) 影像感測器結合的飛行時間 (ToF) 相機。因此,對這些耳機的需求不斷成長正在顯著推動研究市場的需求。

亞太地區佔主要佔有率

- 由於其經濟成長和在全球電子市場的巨大佔有率,預計中國將出現強勁的成長率。該國的製造業正在快速成長,各種技術正在被引入製造和通訊領域。

- 日本政府採取了強硬措施來振興消費性電子和汽車等產業。政府也希望減少生產設施的集中度,以減少因地域限制而對生產的依賴。世界不同地區對半導體和電子供應鏈的日益關注預計將為所研究市場的成長提供有利的機會。

- 印度的購買力不斷增強,社群媒體影響力的不斷增強預計將推動電子產品市場的發展。在印度,網路使用者數量近年來大幅增加。網路需求的成長增加了對更快、更有效率的資料傳輸的需求,從而增加了對光電子產品的需求。

- 韓國汽車工業是世界乘用車銷售和生產的主要市場之一。目前,它佔韓國製造業總產值的10%以上,並且由於大量投資而不斷成長。該產業由現代汽車集團等主要汽車製造商主導,該集團旗下擁有現代、起亞和捷恩斯。因此,韓國在推動汽車產業自動化技術方面具有很大的影響力。

- 據KAMA稱,2022年,韓國出口乘用車和商用車約230萬輛,比上年的204萬輛增加15%。此外,2022年,韓國生產了約376萬輛汽車。起亞汽車生產的汽車最多,佔韓國汽車銷售的39.4%。亞太地區汽車需求和產量的不斷成長將提供重大的市場開拓機會。

光電產業概況

光電市場處於半固體狀態,預計將繼續以創新主導,策略聯盟和頻繁收購將成為參與者建立自己地位的關鍵策略。同時,SK 海力士公司、松下公司、三星電子、豪威科技公司和索尼公司專注於進一步付加價值和最佳化產品組合,以實現利潤最大化。

- 2024 年 1 月 - Osram Licht AG 推出 ALIYOS 技術,該技術突破了多段區域照明的界限,並實現了發光模式的個人化。透明度、薄度和高設計自由度等特點使客戶的照明解決方案與眾不同。基於 ALYYOS 的照明裝置由分段式迷你 LED 組成,可顯示符號、字母、圖像和抽象圖案,用於裝飾、資訊、警告和其他目的。透明的特殊功能允許將多個 LED 箔片放置在彼此後面。3D排列和每段的完全亮度控制,加上模組的透明度,可實現全新的照明和動畫效果。

- 2023 年 12 月 - 三星電子和 SK 海力士同意將影像感測器的「感測器上 AI」技術商業化。兩家公司的目標是改進以AI為中心的影像感測器技術,挑戰日本市場領導SONY,並征服下一代市場。該公司目前正在進行一項概念驗證研究,重點關注使用 CIM(記憶體計算)加速器的臉部辨識和物體辨識功能,這是一種下一代技術,可以執行計算 AI 模型所需的乘法和加法運算。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 和其他宏觀經濟因素對市場的影響

第5章市場動態

- 市場促進因素

- 對智慧消費性電子產品和下一代技術的需求不斷成長

- 增加技術的工業應用

- Li-Fi市場的擴大

- 市場限制因素

- 製造加工成本高

- 光電裝置中的能量損失和加熱挑戰

第6章 市場細分

- 依設備類型

- LED

- 雷射二極體

- 影像感測器

- 光耦合器

- 光伏電池

- 其他

- 按最終用戶產業

- 車

- 航太/國防

- 消費性電子產品

- IT

- 衛生保健

- 住宅/商業

- 產業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 法國

- 德國

- 西班牙

- 亞洲

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 北美洲

第7章 競爭格局

- 供應商市場佔有率分析

- 公司簡介

- SK Hynix Inc.

- Panasonic Corporation

- Samsung Electronics

- Omnivision Technologies Inc.

- Sony Corporation

- Ams Osram AG

- Signify Holding

- Vishay Intertechnology Inc.

- Texas Instruments Inc.

- LITE-ON Technology Corporation

- Rohm Company Limited

- Mitsubishi Electric Corporation

- Broadcom Inc.

- Sharp Corporation

第8章投資分析

第9章 市場機會及未來趨勢

The Optoelectronics Market size is estimated at USD 43.32 billion in 2024, and is expected to reach USD 57.15 billion by 2029, growing at a CAGR of 5.70% during the forecast period (2024-2029).

Key Highlights

- Several market drivers augment the demand for the studied market. The current market trends in optoelectronics are focused on scaling down the sizes of different devices and achieve top levels of integration in systems, such as arrays of light-emitting diodes, laser arrays, and integrated systems with other electronic elements on the same chip.

- The convergence of optical communication, optical storage, and optical imaging sectors is also driving the advancements in the optoelectronics market. Moreover, the growing demand for smart consumer electronics and next-generation technologies is anticipated to boost the adoption of optoelectronics.

- High demands for LEDs have become an industry standard for display technology in electronic devices due to an increase in demand demand for better performance and higher resolution among consumers. LEDs are used in areas like watches, computer components, medical devices, fiber optic communication, switches, household appliances, and 7-segment displays.

- Further, optoelectronic devices are used in various consumer electronic products, ranging from audiovisual technology to biomedical equipment. The increasing industrial applications of the technology and the expansion of the Li-Fi market are also contributing to the market growth. Li-Fi is a wireless communication technology that makes use of infrared and visible light spectrum for high-speed data communication. Li-Fi technology transmits data very quickly and can deliver 224 GB of data per second.

Optoelectronics Market Trends

Consumer Electronics to Witness Significant Growth

- Optoelectronics has various applications in the consumer electronics market. LEDs have revolutionized lighting systems and are used in computer components, watches, switches, household appliances, etc. Smartwatches use optoelectronic sensors, such as photodiodes, to monitor the user's heart rate. CMOS image sensors are often used in smartphones, tablets, and digital single-lens reflex (DSLR) cameras. The growing 5G network and introduction of new products with advanced technologies and features fuels the adoption of smartphones, tablets, and DSLR cameras. Also, the expanding market for mixed reality headsets is aiding the market studied.

- With the rising proliferation of 5G smartphones, many players are introducing image sensors targeted for 5G smartphones, which is contributing positively to the market. For instance, in 2022, Google launched the Pixel 6a, Pixel 7, and Pixel 7 Pro to support the 5G network in India. The Google Pixel 6a supports 19 5G bands, whereas Pixel 7 and 7 Pro support 22 5G bands.

- According to GSMA, Latin America enters the 5G era with 15 million connections expected by 2022. By 2025, 5G is predicted to account for 12% of the region's total connections, with some countries, most notably Brazil, at 20%, exceeding the regional average.

- Furthermore, according to Ericsson, the number of smartphone subscriptions in Western Europe will reach 459 million by 2028. There were approximately 440 million smartphone subscriptions in Western Europe as of 2022.

- Also, the expanding market for mixed reality headsets is aiding the market studied. For instance, in June 2023, Apple introduced Vision Pro, a mixed-reality headset with a 3D camera to help users capture spatial photos and videos in 3D.

- Currently, most AR headsets depend on one or more special imaging sensors, including time of flight (ToF) cameras, which combine a modulated IR light source with a charged coupled device (CCD) image sensor. Thus, the growing demand for these headsets significantly fuels the demand of the studied market.

Asia-Pacific to Hold Major Share

- China is expected to experience a significant growth rate owing to its growing economy and significant share in the global electronics market. The manufacturing industry is rapidly growing in the country and is witnessing the deployment of various technologies in the manufacturing and telecommunications sectors, which is expected to aid the market's growth.

- The Japanese government is taking stringent measures to revive its industries, such as consumer electronics and automotive. Also, the government wishes to reduce the clustering of production facilities in one place to reduce production dependency on geographical constraints. The enhanced focus on the semiconductor and electronics supply chain by various global regions is expected to provide profitable opportunities for the growth of the studied market.

- India has a growing purchasing power, and the growing influence of social media is expected to drive the market for electronic goods. The increase in the number of internet users in India has witnessed a significant increase in recent years. This growth in the internet demand increased demand for faster and more efficient data transmission, driving the need for optoelectronics.

- The South Korean automotive industry is one of the major global markets for vehicle sales and production of passenger cars. It currently contributes more than 10% of all manufacturing output in the country and is experiencing growth owing to significant investments. The industry is dominated by major automakers such as the Hyundai Motor Group, which owns Hyundai, Kia, and Genesis. As a result, South Korea wields significant influence in driving automation technologies in its Automotive industry.

- According to KAMA, in 2022, South Korea exported approximately 2.3 million vehicles, comprising passenger cars and commercial vehicles, representing a 15% increase from the previous year's 2.04 million units. In addition, in 2022, around 3.76 million vehicles were manufactured in South Korea. Kia Motors produced the highest number of vehicles, accounting for 39.4% of automobile sales in South Korea. The increasing automotive demand and production in the Asia Pacific region would offer significant opportunities for developing the market studied.

Optoelectronics Industry Overview

The optoelectronics market is semi-consolidated and is expected to remain innovation-led, with strategic alliances and frequent acquisitions adopted as the key strategies by the players to establish their presence. Meanwhile, companies SK Hynix Inc., Panasonic Corporation, Samsung Electronics, Omnivision Technologies Inc., and Sony Corporation are focusing on further developing value-added capabilities and optimizing product mix to maximize margins.

- January 2024 - Osram Licht AG introduced the ALIYOS technology, which pushes the boundaries of multi-segmented area lighting and allows individualization of light emission patterns. Characteristics like transparency, thinness, and a high freedom of design differentiate customer's lighting solutions. An ALIYOS-based lighting unit can configure the segmented mini-LEDs to display symbols, words, images, or abstract patterns for the purposes of decoration, information, or warning. Due to the special feature of transparency, several LED foils can be placed behind each other. A three-dimensional arrangement and the full brightness control of each segment, in combination with the transparency of the modules, enable completely new lighting and animation effects.

- December 2023 - Samsung Electronics and SK Hynix joined to commercialize "On-sensor AI" technology for image sensors. They aim to elevate their image sensor technologies centered around AI and challenge the market leader, Japan's Sony, to dominate the next-generation market. The company is currently conducting proof-of-concept research focused on facial and object recognition features, using a Computing In Memory (CIM) accelerator, a next-generation technology capable of performing multiplication and addition operations required for AI model computations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing demand for Smart Consumer Electronics and Next Generation Technologies

- 5.1.2 Increasing Industrial Applications of the Technology

- 5.1.3 Expansion of the Li-Fi Market

- 5.2 Market Restraints

- 5.2.1 High Manufacturing and Fabricating Costs

- 5.2.2 Challenges With Energy Loss and Heating of Optoelectronic Devices

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 LED

- 6.1.2 Laser Diode

- 6.1.3 Image Sensors

- 6.1.4 Optocouplers

- 6.1.5 Photovoltaic cells

- 6.1.6 Others

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Aerospace and Defense

- 6.2.3 Consumer Electronics

- 6.2.4 Information Technology

- 6.2.5 Healthcare

- 6.2.6 Residential and Commercial

- 6.2.7 Industrial

- 6.2.8 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Germany

- 6.3.2.4 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Market Share Analysis

- 7.2 Company Profiles*

- 7.2.1 SK Hynix Inc.

- 7.2.2 Panasonic Corporation

- 7.2.3 Samsung Electronics

- 7.2.4 Omnivision Technologies Inc.

- 7.2.5 Sony Corporation

- 7.2.6 Ams Osram AG

- 7.2.7 Signify Holding

- 7.2.8 Vishay Intertechnology Inc.

- 7.2.9 Texas Instruments Inc.

- 7.2.10 LITE-ON Technology Corporation

- 7.2.11 Rohm Company Limited

- 7.2.12 Mitsubishi Electric Corporation

- 7.2.13 Broadcom Inc.

- 7.2.14 Sharp Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年光電全球市場報告

2025 年光電全球市場報告 全球汽車光電市場

全球汽車光電市場 歐洲光電:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲光電:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 紅外線光電:全球市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

紅外線光電:全球市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 光電市場:電動車,按車輛類型、設備、分佈、應用分類 - 全球預測 2025-2030

光電市場:電動車,按車輛類型、設備、分佈、應用分類 - 全球預測 2025-2030 汽車光電市場:按通路、產品、車輛、應用程式分類 - 全球預測 2025-2030

汽車光電市場:按通路、產品、車輛、應用程式分類 - 全球預測 2025-2030 光電元件市場報告:2030 年趨勢、預測與競爭分析

光電元件市場報告:2030 年趨勢、預測與競爭分析 光電市場:不同設備類型,各終端用戶產業,各地區,2024年~2031年

光電市場:不同設備類型,各終端用戶產業,各地區,2024年~2031年 光電子市場 - 按類型(光伏 (PV) 電池、光耦合器、圖像感測器、發光二極體 (LED))、按最終用途(住宅和商業、工業)、按行業和預測,2024 年 - 2032 年

光電子市場 - 按類型(光伏 (PV) 電池、光耦合器、圖像感測器、發光二極體 (LED))、按最終用途(住宅和商業、工業)、按行業和預測,2024 年 - 2032 年 2030 年光電元件市場預測:按元件、材料、應用、最終用戶和地區分類的全球分析

2030 年光電元件市場預測:按元件、材料、應用、最終用戶和地區分類的全球分析