|

市場調查報告書

商品編碼

1522875

CNG LPG汽車:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)CNG LPG Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

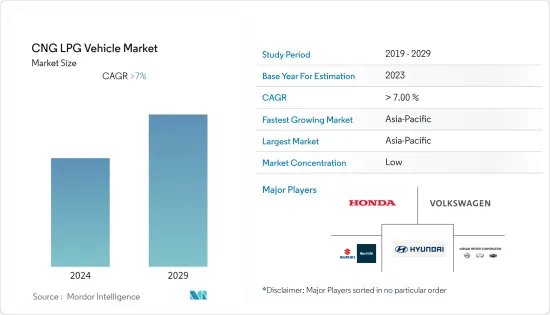

CNG LPG汽車市場規模預計到2024年為67.3億美元,預計到2029年將達到101.3億美元,在預測期內(2024-2029年)複合年成長率為7%,預計將會成長。

由於環境問題日益嚴重、燃料價格上漲以及能源多樣化的增加,CNG 和 LPG 汽車的全球市場正在擴大。近年來,CNG 和 LPG 汽車技術取得了重大改進,包括燃料儲存、引擎效率和安全功能。這些進步使 CNG 和 LPG 汽車在性能和可靠性方面更具競爭力。

由於壓縮天然氣和液化石油氣比汽油和柴油便宜,營運成本降低是主要推動因素。這方面對於商用車和高里程車輛尤其有吸引力。世界各地都在加強廢氣排放法規,並且比傳統燃料排放的污染物更少的壓縮天然氣和液化石油氣汽車的採用正在加速。

隨著世界轉向永續能源,壓縮天然氣和液化石油氣汽車可能會保持其相關性,特別是在電動車基礎設施落後的地區。汽車技術和燃料基礎設施的持續改進也可能增加壓縮天然氣和液化石油氣汽車的市場吸引力。

亞太地區是全球最大的汽車市場。儘管全球最大的汽車市場中國市場成長緩慢,但預計該地區將在預測期內引領壓縮天然氣和液化石油氣汽車市場的成長。

因此,由於上述因素的綜合作用,預計未來幾年市場將顯著成長。

CNG LPG汽車市場趨勢

商用車推動 CNG 和 LPG 汽車需求

CNG 和 LPG 通常比傳統汽油或柴油便宜。對於商用車業者來說,燃料成本佔營運費用的很大一部分。 CNG 和 LPG 的成本較低,可以在車輛的整個使用壽命期間節省大量成本,使這些選擇在經濟上具有吸引力。與波動的石油市場相比,CNG和LPG價格整體穩定。這種穩定性使公司能夠更好地預測和管理營運成本,這對商業營運至關重要。

全球日益嚴格的排放氣體法規也是主要推動力。 CNG 和 LPG 汽車比柴油和汽油汽車排放更少的污染物,如氮氧化物 (NOx)、顆粒物 (PM) 和二氧化碳 (CO2)。 CNG和LPG汽車更符合環境標準,特別是在空氣品質問題嚴重的都市區。

隨著 CNG 和 LPG 加氣站的擴建,這些燃料變得越來越容易取得。此類基礎設施的發展通常是政府措施或私人組織與政府機構之間夥伴關係的結果。現代 CNG 和 LPG 汽車在性能、可靠性和燃油效率方面顯著提高。因此,與傳統燃油動力汽車的競爭日益加劇。

在天然氣和液化石油氣因國內生產而容易取得且價格低廉的地區,自然有利用這些資源的動力。世界上許多城市都設立了低排放氣體區,不符合特定排放標準的車輛將被禁止通行或必須支付費用。 CNG 和 LPG 汽車通常符合這些標準,使其成為在都市區營運的公司的首選。

然而,天然氣汽車提供的成本優勢以及鼓勵採用替代燃料汽車的政府支持政策正在推動全球 CNG/LPG 汽車市場的發展。例如

- 2022 年 11 月,印度新德里每公斤 CNG 的價格為 78.61 印度盧比,而汽油為每公升 96.72 印度盧比(1.16 美元),柴油為每公升 96.67 印度盧比(1.16 美元)(94 美分)。由於壓縮天然氣和汽油/柴油之間的巨大定價差異,以及壓縮天然氣汽車比汽油/柴油汽車更省油,過去幾年印度壓縮天然氣汽車的銷量幾乎加倍。

因此,預計所有上述因素將在未來五年共同推動全球 CNG/LPG 汽車市場的發展。

預計亞太地區將成為預測期內最大的市場

在印度成長的推動下,亞太地區預計將成為全球最大的壓縮天然氣和液化石油氣汽車市場。

亞太地區的城市是全球污染最嚴重的地區之一。 CNG 和 LPG 汽車比柴油和汽油汽車排放的污染物更少,這使其成為改善城市空氣品質的有吸引力的選擇。因此,許多國家都在關注排放法規的全球趨勢。 CNG 和 LPG 汽車被認為是加強這些環境法規的實際步驟。

此外,全部區域的監管政策正在強化這一趨勢。嚴格的排放控制政策,例如印度的巴拉特第六階段排放標準,正在推動清潔燃料汽車(包括壓縮天然氣和液化石油氣)的採用。此外,中國和印度等國家製定了促進替代燃料汽車的具體政策,將壓縮天然氣和液化石油氣汽車納入更廣泛的碳減排策略。

技術進步大大提高了壓縮天然氣和液化石油氣汽車的吸引力。車輛技術的改進不僅提高了性能和可靠性,還提高了效率。這些車輛的續航里程和加油時間得到了顯著改善。補充這些技術進步的是加氣基礎設施的擴展,這對於壓縮天然氣和液化石油氣汽車的生存至關重要。這種擴張,特別是在印度和中國,有助於使這些燃料更容易用於個人和商業用途。亞太地區市場動態的特點是汽車保有量大幅成長,這進一步增加了對壓縮天然氣和液化石油氣汽車的需求。

由於天然氣價格較低和採用更嚴格的排放法規,歐洲和北美預計將成為亞太地區之後的第二大市場。

CNG LPG汽車產業概況

CNG/LPG 汽車市場高度分散,由多個全球和本地參與者主導。主要企業包括現代、鈴木、日產、大眾和工業。大公司正在透過推出新產品和組建合資企業來鞏固其市場地位。例如,

- 2022 年 8 月,大眾集團商用車部門 Traton SE 旗下品牌斯堪尼亞向南非豪登省的 BridCam 經銷商交付了全國第一輛純專用卡車。

- 2022年1月,依維柯客車與象牙海岸共和國SOTRA合作,開始在當地組裝配備CNG引擎的依維柯Daily Minibus。

- 2022年1月,Eicher(VECV)展出了4.9噸和5.9噸卡車的CNG車型。這些是 VECV 提供的最輕負載容量的卡車,但隨著 CNG 站的佔地面積預計在未來幾年會增加,VECV 計劃推出更高負載容量的CNG 卡車。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究成果

- 研究場所

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 對清潔能源的需求不斷成長推動市場

- 市場限制因素

- 不斷上升的安全疑慮正在限制市場

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按燃料類型

- 壓縮天然氣 (CNG)

- 液化石油氣(LPG)

- 按車型分類

- 客車

- 商用車

- 按銷售管道

- OEM

- 改造

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 併購

- 公司簡介

- Hyundai Motor Company

- Suzuki Motor Corporation

- Nissan Motor Co. Ltd

- Volkswagen AG

- Honda Motor Company

- IVECO SpA

- AB VOLVO

- Ford Motor Company

- Tata Motors Limited

- Traton SE

第7章 市場機會及未來趨勢

第8章 客製化

- 市場數量(個)

The CNG LPG Vehicle Market size is estimated at USD 6.73 billion in 2024, and is expected to reach USD 10.13 billion by 2029, growing at a CAGR of 7% during the forecast period (2024-2029).

The global market for CNG and LPG vehicles has been growing, driven by increasing environmental concerns, rising fuel prices, and the push for energy diversification. In recent years, significant improvements have been made in CNG and LPG vehicle technologies, including fuel storage, engine efficiency, and safety features. These advancements have made CNG and LPG vehicles more competitive in terms of performance and reliability.

Lower operational costs due to cheaper CNG and LPG compared to petrol and diesel are significant drivers. This aspect is particularly appealing for commercial and high-mileage vehicles. Stricter emission regulations worldwide are boosting the adoption of CNG and LPG vehicles, as they emit fewer pollutants compared to conventional fuels.

With the global shift toward sustainable energy, CNG and LPG vehicles are likely to maintain their relevance, especially in regions where electric vehicle infrastructure is lagging. Continuous improvements in vehicle technology and fuel infrastructure may also enhance the market appeal of CNG and LPG vehicles.

Asia-Pacific is the largest market for automobiles in the world. The region, despite the sluggish growth in the Chinese market, the largest automobile market in the world, is expected to lead the growth in the CNG and LPG vehicles market during the forecast period.

Thus, the confluence of the aforementioned factors is expected to produce significant growth in the market in the coming years.

CNG LPG Vehicle Market Trends

Commercial Vehicles Fueling the Demand for CNG and LPG Vehicle

CNG and LPG are often cheaper than traditional petrol and diesel fuels. For commercial vehicle operators, fuel cost is a significant portion of operating expenses. The lower cost of CNG and LPG can translate into substantial savings over the lifetime of the vehicle, making these options financially attractive. Compared to the more volatile oil market, CNG and LPG prices are generally more stable. This stability allows businesses to better forecast and manage their operating costs, which is crucial for commercial operations.

Increasingly stringent emission regulations worldwide are a significant driver. CNG and LPG vehicles emit fewer pollutants such as nitrogen oxides (NOx), particulate matter (PM), and carbon dioxide (CO2) compared to diesel and petrol vehicles. In urban areas, especially where air quality is a major concern, CNG and LPG vehicles are more compliant with environmental standards.

The expansion of CNG and LPG fueling stations has made these fuels more accessible. This infrastructure development is often a result of either government initiatives or partnerships between private entities and government bodies. Modern CNG and LPG vehicles have seen significant improvements in terms of performance, reliability, and fuel efficiency. This makes them more competitive with traditional fuel vehicles.

In regions where natural gas or LPG is readily available and less expensive due to domestic production, there is a natural inclination to utilize these resources. Many cities worldwide are introducing low-emission zones where vehicles that do not meet certain emission standards are either banned or subject to a fee. CNG and LPG vehicles often meet these standards, making them a viable option for businesses operating within urban areas.

However, the cost advantage offered by natural gas vehicles and supportive government policies to encourage the adoption of alternative fuel-powered vehicles is driving the global CNG and LPG vehicle market. For instance,

- In November 2022, 1 kg of CNG was priced at INR 78.61 (94 cents) compared to petrol, which cost INR 96.72 (USD 1.16) per liter, and diesel, which was priced at INR 96.67 (USD 1.16) per liter in New Delhi, India. This substantial difference in CNG and petrol/diesel pricing and the higher mileage of CNG vehicles than petrol/diesel vehicles has almost doubled the sales of CNG vehicles in India over the past few years.

Thus, the combination of all the above factors is anticipated to propel the market for CNG and LPG vehicles worldwide over the next five years.

Asia-Pacific Region is Expected to be the Largest Market During the Forecast Period

Asia-Pacific is forecasted to be the largest market for CNG and LPG vehicles in the world, led by the growth in India.

Cities in Asia-Pacific are among the most polluted globally. CNG and LPG vehicles emit fewer pollutants compared to diesel and petrol vehicles, making them attractive options for improving urban air quality. Therefore, many countries are aligned with global trends in emission standards. CNG and LPG vehicles are seen as practical steps toward meeting these stricter environmental regulations.

Moreover, regulatory policies across the region reinforce this trend. Stringent emission control policies, such as India's Bharat Stage VI emission standards, have expedited the adoption of cleaner fuel vehicles, including CNG and LPG. Furthermore, countries like China and India have specific policies promoting alternative fuel vehicles, situating CNG and LPG vehicles within broader carbon reduction strategies.

Technological advancements significantly contribute to the attractiveness of CNG and LPG vehicles. Improvements in vehicle technology have not only enhanced performance and reliability but also increased efficiency. The range and refueling times of these vehicles have seen marked improvements. Complementing these technological strides is the expansion of refueling infrastructure, which is critical for the practicality of CNG and LPG vehicles. This expansion, notably in India and China, has been instrumental in making these fuels more accessible for both personal and commercial use. The market dynamics of the Asia-Pacific region are characterized by a vast and growing vehicle population that further fuels the demand for CNG and LPG vehicles.

Following Asia-Pacific, Europe and North America are predicted to be the next biggest markets due to lower prices of natural gas and the adoption of stringent emission norms.

CNG LPG Vehicle Industry Overview

The CNG and LPG vehicle market is highly fragmented and dominated by several global and local players. Some of the major players are Hyundai Motor Company, Suzuki Motor Corporation, Nissan Motor Co. Ltd, Volkswagen AG, and Honda Motor Company. The major companies are launching new products and forming joint ventures to cement their market position. For instance,

- In August 2022, Scania, a brand of Traton SE, the Volkswagen Group commercial vehicle division, delivered the country's first dedicated natural gas truck to BridCam Distributors in Gauteng, South Africa.

- In January 2022, Iveco Bus partnered with SOTRA in Ivory Coast, Africa, to start the local assembly of CNG-powered Iveco Daily Minibus.

- In January 2022, Eicher (VECV) showcased CNG variants of its 4.9 and 5.9-metric-ton trucks, typically used in last-mile delivery operations by fleet owners. While these are the lightest payload trucks VECV offers, the automaker plans to bring in CNG trucks with higher payloads as the footprint of CNG stations is likely to increase in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand for Clean Energy Driving the Market

- 4.3 Market Restraints

- 4.3.1 Rising Safety Concerns is Antcipated to Restrain the Market

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Fuel Type

- 5.1.1 Compressed Natural Gas (CNG)

- 5.1.2 Liquefied Petroleum Gas (LPG)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 By Sales Channel

- 5.3.1 OEM

- 5.3.2 Retrofitting

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers & Acquisitions

- 6.3 Company Profiles

- 6.3.1 Hyundai Motor Company

- 6.3.2 Suzuki Motor Corporation

- 6.3.3 Nissan Motor Co. Ltd

- 6.3.4 Volkswagen AG

- 6.3.5 Honda Motor Company

- 6.3.6 IVECO SpA

- 6.3.7 AB VOLVO

- 6.3.8 Ford Motor Company

- 6.3.9 Tata Motors Limited

- 6.3.10 Traton SE

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 CUSTOMIZATION

- 8.1 Market Volume In Units

CNG坦克的全球市場(~2035年):汽缸坦克各類型,各汽缸複合材料類型,各汽缸車輛類型,各類型企業,各地區,產業趨勢,預測

CNG坦克的全球市場(~2035年):汽缸坦克各類型,各汽缸複合材料類型,各汽缸車輛類型,各類型企業,各地區,產業趨勢,預測 CNG 和 LPG 汽車市場按燃料類型、引擎系統、汽缸類型、銷售管道和車輛類型分類 - 全球預測 2025-2032 年

CNG 和 LPG 汽車市場按燃料類型、引擎系統、汽缸類型、銷售管道和車輛類型分類 - 全球預測 2025-2032 年 全球 CNG 和 LPG 汽車市場

全球 CNG 和 LPG 汽車市場 全球 CNG 儲槽市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

全球 CNG 儲槽市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測 2025年全球CNG和LPG汽車市場報告CNG 和 LPG 汽車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

2025年全球CNG和LPG汽車市場報告CNG 和 LPG 汽車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 印度 CNG 汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)非洲的 CNG 和 LPG 車輛:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)CNG 摩托車市場按產品類型、引擎類型、控制系統、引擎容量、燃料箱容量和最終用戶分類 - 2025-2030 年全球預測

印度 CNG 汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)非洲的 CNG 和 LPG 車輛:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)CNG 摩托車市場按產品類型、引擎類型、控制系統、引擎容量、燃料箱容量和最終用戶分類 - 2025-2030 年全球預測 全球 CNG 儲罐市場按車輛類型、儲罐類型、材料類型、應用和地區分類 - 預測至 2029 年

全球 CNG 儲罐市場按車輛類型、儲罐類型、材料類型、應用和地區分類 - 預測至 2029 年