|

市場調查報告書

商品編碼

1537602

二甲醚:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Dimethyl Ether - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

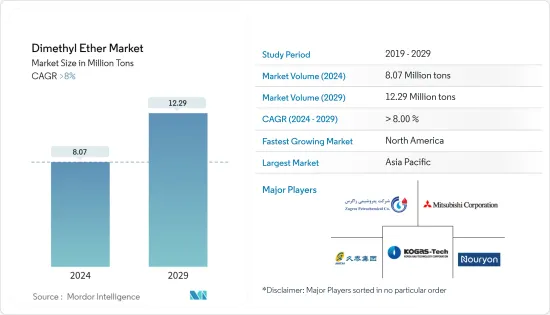

預計2024年全球二甲醚市場規模將達到807萬噸,2029年將達到1,229萬噸,2024-2029年預測期間複合年成長率超過8%。

COVID-19 對市場產生了負面影響,考慮到大流行的情況,隨著人們出行頻率的減少,汽車行業對基於 DME 的液化石油氣燃料的需求減少。然而,在封鎖放鬆後,該行業出現反彈,全球燃料需求不斷增加。

主要亮點

- 短期內,對液化石油氣混合用途應用的需求不斷成長以及對非電動和電動車日益成長的興趣正在推動市場成長。

- 改造現有基礎設施以使用 DME 的高昂成本以及電動車使用量的增加可能會成為市場的限制因素。

- 未來幾年可能是市場的機遇,因為越來越多的研究使用二甲醚作為替代燃料,但市場尚未建立。

- 由於對燃料、液化石油氣等的強勁需求,亞太地區可能在預測期內主導調查市場。

二甲醚市場趨勢

液化石油氣混合領域佔市場主導地位

- 液化石油氣 (LPG) 是二甲醚 (DME) 的重要應用之一,在許多應用中,二甲醚可以預先指定的比例與常規 LPG 混合。

- 二甲醚作為替代燃料添加劑混入液化石油氣中,可增強燃燒、減少有害排放,並減少對液化石油氣的依賴。目前,DME-LPG 混合物中使用的 DME 大約為 15-25%,但更高的混合物正在研究中,因為更好的混合物可能需要改變所使用的設備。

- DME 用於車輛用丙烷汽車燃氣的液化石油氣混合物中。據丙烷教育和研究委員會稱,美國道路上有近 26 萬輛液化石油氣車輛配備經過認證的燃料系統。許多用於車隊應用,例如校車、接駁車和警車。

- 同樣,根據歐洲替代燃料觀測站(EAFO)的數據,2022年匈牙利液化石油氣(LPG)汽車的數量將為23,194輛。不過,與 2021 年的 24,141 套相比,這是最低的。

- 中國、印度、印尼等國正積極推廣使用二甲醚作為替代燃料。

- 根據中國國家統計局的數據,2023年12月中國液化石油氣(LPG)產量為443萬噸,較2023年11月的415萬噸增加。

- 因此,預計上述因素將在未來幾年對市場產生重大影響。

亞太地區主導市場

- 二甲醚 (DME) 來自各種最終用途,例如液化石油氣混合、推進劑和燃料,其中亞太地區消耗量最大。在亞太地區,中國佔了最大的需求佔有率,其次是日本、韓國和印度。

- 中國是第一個開始商業規模使用二甲醚混合液化石油氣的國家。中國的二甲醚需求大部分用於家庭使用(液化石油氣混合烹飪燃氣供應)。在中國,20%的二甲醚混合液化石油氣產品用於此目的。

- 根據石油規劃和分析小組的數據,截至 2023 年 10 月,PSU OMC(IOCL、BPCL、HPCL)的國內液化石油氣客戶群總計達 31.54 億,有 25,425 家液化石油氣經銷商為其提供服務。

- 據經濟產業省預計,2022年日本液化石油氣(LPG)產量將為307萬噸。

- 印尼是另一個積極推廣二甲醚混合液化石油氣以滿足其能源需求的亞洲國家。 Air Products and Chemicals 和 PT Bukit Asam 等公司正在進行以煤炭生產二甲醚用於液化石油氣混合的計劃。

- 因此,由於上述因素,預計該地區的 DME 需求在預測期內將會增加。

二甲醚行業概況

二甲醚市場部分整合,前五家公司佔據主要佔有率。市場主要企業包括(排名不分先後)韓國天然氣公司、ZPCIR、九台能源集團、三菱商事株式會社和諾力昂。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章 研究方法

第3章執行摘要

第4章市場動態

- 促進因素

- 液化石油氣混合用途需求增加

- 人們對非電動和電動車的興趣日益濃厚

- 其他

- 抑制因素

- 修改現有基礎設施以使用 DME 的成本很高

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商議價能力

- 消費者議價能力

- 新進入的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔(市場規模:基於數量)

- 目的

- 推進劑

- 液化石油氣混合物

- 燃料

- 其他用途

- 起源

- 天然氣

- 煤炭

- 生物基產品

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 合併、收購、合資、合作夥伴關係和協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- DME-AEROSOL

- Grillo-Werke AG

- Jiutai Energy Group

- KOREA GAS CORPORATION

- Mitsubishi Corporation

- Nouryon

- Oberon Fuels, Inc.

- PCC Group

- Shell plc

- The Chemours Company

- ZPCIR

第7章 市場機會及未來趨勢

- 加強二甲醚作為替代燃料的研究

- 未成熟市場為 DME 成長提供巨大潛力

The Dimethyl Ether Market size is estimated at 8.07 Million tons in 2024, and is expected to reach 12.29 Million tons by 2029, growing at a CAGR of greater than 8% during the forecast period (2024-2029).

COVID-19 negatively impacted the market, and considering the pandemic scenario, the demand for DME-based LPG fuel from the automotive segment decreased as people were not traveling frequently. However, after the easing of lockdowns, the industry picked up, and the fuel demand has increased worldwide.

Key Highlights

- Over the short term, the growing demand for LPG blending applications and increasing interest in non-electric and electric vehicles are driving the market growth.

- High costs for altering current infrastructure to use DME and increasing EV use can act as a restraint for the market.

- Growing research for using DME as an alternative fuel and an under-established market will likely create opportunities for the market in the coming years.

- Asia-Pacific is likely to dominate the market studied during the forecast period with robust demand for fuel, LPG, and others.

Dimethyl Ether Market Trends

LPG Blending Segment to Dominate the Market

- Liquefied petroleum gas (LPG) is one of the significant applications of dimethyl ether (DME), which can be blended with traditional LPG at a pre-specified ratio for many applications.

- DME is blended with LPG as an alternative fuel additive for enhancing combustion, reducing hazardous emissions, and reducing dependency on LPG. Currently, around 15-25% of DME is utilized in DME-LPG blends, with higher ratio blends being researched, as a better blend may require equipment changes for usage.

- DME is used for LPG blending that is in Propane autogas in vehicles. According to the Propane Education and Research Council, there are nearly 260,000 on-road LPG vehicles with certified fuel systems in the United States. Many are used in fleet applications, such as school buses, shuttles, and police vehicles.

- Similarly, according to the European Alternative Fuels Observatory (EAFO), the number of liquefied petroleum gas (LPG) vehicles in Hungary will be 23,194 in 2022. However, the number is lowest when compared to 24,141 in 2021.

- Countries like China, India, and Indonesia are aggressively pushing for the use of DME as an alternate fuel, as these countries are highly dependent on imports to meet their local LPG demand.

- According to the National Bureau of Statistics of China, the liquefied petroleum gas (LPG) production output in China was 4.43 million metric tons in December 2023 and registered growth when compared to 4.15 million metric tons in November 2023.

- Therefore, the factors above are expected to impact the market significantly in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific holds the largest consumption share of dimethyl ether (DME) from various end-use applications such as LPG blending, propellants, fuels, and others. In Asia-Pacific, China has a significant share of demand, followed by Japan, South Korea, and India, among others.

- China is the first country to start using DME-blended LPG on a commercial scale. The majority of China's DME demand is from households (for LPG blended cooking gas supply). In China, 20% of DME blended LPG products are used for this purpose.

- According to the Petroleum Planning and Analysis Cell, as of October 2023, PSU OMCs (IOCL, BPCL, and HPCL) together have 31.54 crore active LPG customers in the domestic category whom 25,425 LPG distributors are serving.

- According to the METI (Japan), the production volume of liquified petroleum gas (LPG) in Japan accounted for 3.07 million metric tons in 2022.

- Indonesia is another Asian country aggressively pushing for DME blended LPG for its energy needs. Companies, such as Air Products and Chemicals and PT Bukit Asam, are moving forward with significant projects in the country to produce DME from coal for LPG blending applications.

- Thus, the demand for DME in the region is expected to increase during the forecast period due to the factors mentioned above.

Dimethyl Ether Industry Overview

The dimethyl ether market is partially consolidated, with the top five players accounting for a significant share. Some of the key players in the market include (not in any particular order) KOREA GAS CORPORATION, ZPCIR, Jiutai Energy Group, Mitsubishi Corporation, and Nouryon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from LPG Blending Applications

- 4.1.2 Increasing Interest in Non-Electric and Electric Vehicles

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 High Costs for the Alteration of Current Infrastructure to Use DME

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Propellants

- 5.1.2 LPG Blending

- 5.1.3 Fuel

- 5.1.4 Other Applications

- 5.2 Source

- 5.2.1 Natural Gas

- 5.2.2 Coal

- 5.2.3 Bio-based Products

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle-East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 DME-AEROSOL

- 6.4.2 Grillo-Werke AG

- 6.4.3 Jiutai Energy Group

- 6.4.4 KOREA GAS CORPORATION

- 6.4.5 Mitsubishi Corporation

- 6.4.6 Nouryon

- 6.4.7 Oberon Fuels, Inc.

- 6.4.8 PCC Group

- 6.4.9 Shell plc

- 6.4.10 The Chemours Company

- 6.4.11 ZPCIR

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Research for Use of DME as an Alternative Fuel

- 7.2 Under Established Market Offers Huge Potential for DME Growth

碳酸二乙酯市場-全球產業規模、佔有率、趨勢、機會和預測(按銷售管道、最終用途、地區和競爭細分,2020-2030 年)

碳酸二乙酯市場-全球產業規模、佔有率、趨勢、機會和預測(按銷售管道、最終用途、地區和競爭細分,2020-2030 年) 生物二甲醚全球市場報告:趨勢、預測和競爭分析(至 2031 年)2025年二甲醚全球市場報告

生物二甲醚全球市場報告:趨勢、預測和競爭分析(至 2031 年)2025年二甲醚全球市場報告 全球丙二醇甲醚醋酸酯市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)全球二甲醚市場(2018-2034)

全球丙二醇甲醚醋酸酯市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)全球二甲醚市場(2018-2034) 二乙醚:市場佔有率分析、產業趨勢、成長預測(2025-2030)

二乙醚:市場佔有率分析、產業趨勢、成長預測(2025-2030) 二甲醚市場規模、佔有率、成長分析、材料、應用和地區 - 產業預測,2024-2031 年

二甲醚市場規模、佔有率、成長分析、材料、應用和地區 - 產業預測,2024-2031 年 二乙醚市場:未來預測(2025-2030)

二乙醚市場:未來預測(2025-2030) 二甲醚市場:按原料、形式和應用分類 - 2025-2030 年全球預測到 2030 年二甲醚市場預測:按原料、應用和地區分類的全球分析

二甲醚市場:按原料、形式和應用分類 - 2025-2030 年全球預測到 2030 年二甲醚市場預測:按原料、應用和地區分類的全球分析