|

市場調查報告書

商品編碼

1537681

邏輯IC:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Logic IC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

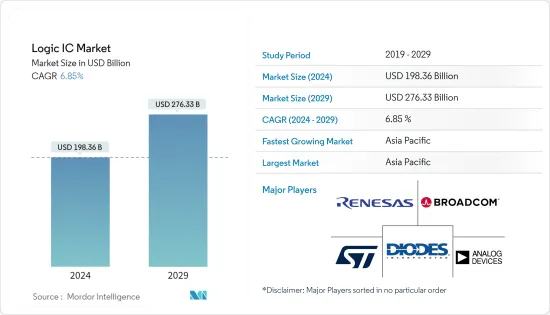

邏輯IC市場規模預計到2024年為1,983.6億美元,預估至2029年將達2,763.3億美元,預測期內(2024-2029年)複合年成長率為6.85%。

出貨量方面,預計將從2024年的652.4億台成長到2029年的801億台,預測期間(2024-2029年)複合年成長率為4.19%。

半導體製造流程的不斷進步正在開發更複雜、更有效率的邏輯 IC。更小的電晶體尺寸、更高的性能和更低的功耗使得開發可用於廣泛應用的高效能邏輯 IC 成為可能。邏輯 IC 非常靈活,可用於多種應用。它可以配置為執行多種邏輯功能,例如 AND、OR、NOT 和 XOR。這種靈活性使得智慧電路的設計和開發能夠滿足各種行業的要求,包括消費性電子、汽車、通訊和工業自動化。

主要亮點

- 邏輯IC對電子設備的小型化和整合化做出了巨大貢獻。由於半導體製造技術的發展,近年來小型且複雜的邏輯電路已被整合到單晶片中。這種整合使電子系統能夠增強其功能,同時減少其物理尺寸和消費量,從而可用於行動裝置、無線技術甚至空間受限的應用。顯示輔助器、通用邏輯和 MOS 觸控螢幕控制器是近年來顯著推動市場發展的一些邏輯組件。

- 此外,最終用戶行業的進步正在增加對小型且堅固的半導體設備的需求。例如,與傳統 PCB基板不同,現代智慧型手機需要更小的 PCB基板。我們也看到物聯網設備的出現,例如具有不規則和不同形狀的穿戴式設備,這只能透過小型化來實現。因此,對小型化IC元件的需求預計將大幅增加。

- 物聯網和工業物聯網的出現對電子設備的設計和尺寸產生了重大影響,包括智慧家庭、辦公室、穿戴式裝置、遠端監控和控制等技術的引入。此外,OEM和設計師在開發穿戴式技術時首先考慮小型化。

- 需要小型化電子元件的另一項進步是攜帶式電子產品,其中需要更小、更薄的半導體系統以節省空間和小型化。對於航太和電動車等高度整合和高速應用,提高電氣性能以盡量減少噪音影響的需求也很明顯。由於設計最終產品時考慮這些因素,邏輯 IC 元件在開發先進電子系統中變得越來越重要。

- 邏輯 IC 預計將執行各種複雜的功能。隨著技術的進步,電子設備需要具有更尖端的功能和性能。設計人員必須結合複雜的邏輯電路和演算法來滿足這些需求。功能的增加導致了更大、更複雜的設計,使得管理和最佳化各個元件之間的複雜互動成為一項挑戰。

- COVID-19 大流行極大地改變了市場,影響了客戶行為、業務收益以及公司營運的許多方面。疫情暴露了供應方面以前未被注意到的風險,可能導致關鍵零件的短缺。因此,半導體公司正在積極重組其供應鏈以增強彈性,而這些調整可能會在疫情後繼續下去。

邏輯IC市場趨勢

快速成長的汽車領域

- 邏輯 IC 對於汽車控制和通訊系統至關重要。它們用於引擎控制單元(ECU)、變速箱控制單元(TCU)、防鎖死煞車系統、資訊娛樂系統、安全氣囊控制模組和系統以及各種其他電控系統。 IC 可以處理和執行用於車輛控制、監控和通訊的高級演算法和邏輯功能。

- 消費者尋求先進的功能、便利性和無縫的使用者體驗,包括舒適性、安全性和便利性,例如ADAS(高級駕駛輔助系統)、智慧照明系統、個人化設定和語音控制等。滿足消費者期望並提供創新功能正在推動汽車產業對邏輯 IC 的需求。

- 各種 ADAS 技術在現代車輛中變得司空見慣,包括自動緊急煞車、車道偏離警告和主動式車距維持定速系統。邏輯 IC 對於處理感測器資料、做出即時決策和控制車輛功能至關重要。未來的趨勢很可能會導致更先進的ADAS功能的發展,需要邏輯IC具有更高的運算能力、更低的延遲和增強的感測器融合能力。

- 安全和功能要求在汽車行業中非常重要。邏輯 IC 可確保 ADAS、自動駕駛、動力傳動系統控制等各種汽車系統的安全可靠運作。對符合 ISO 26262 等嚴格安全標準的高性能、可靠邏輯 IC 的需求正在推動汽車市場的需求。

- 追求自動駕駛汽車是汽車產業的重要趨勢。邏輯 IC 對於自動駕駛所需的複雜處理和決策至關重要。

- 羅蘭貝格預計,2025年4級輕型自動駕駛汽車的滲透率將達到1%,此後市場佔有率將逐步增加。此外,到 2030 年,預計 4 級小型自動駕駛汽車將佔全球市場的 5%。隨著自動駕駛技術的進步,將需要具有更高處理能力、先進感測器整合和強大安全功能的邏輯 IC。

- 此外,環境問題和政府法規正在加速向電動車的轉變。電動車基於先進的電力電子和電池管理,因此需要專門的邏輯 IC 來確保最佳的能源使用、馬達控制和充電基礎設施整合。

- IEA最新報告預計,2022年全球電動車銷量將超過1,000萬輛,2023年銷量預計將成長35%,達到1,400萬輛。 2023年,中國、歐洲、美國等地區電動車銷量將達1,390萬輛。

亞太地區錄得強勁成長

- 亞太地區僅包含對中國和日本的分析。該地區是全球半導體產業充滿活力且快速成長的部分。憑藉新興經濟體、強大的製造能力以及不斷成長的電子產品需求,亞太地區對於推動邏輯 IC 創新、生產和消費至關重要。

- 亞太地區是世界半導體製造中心,中國和日本等國家在半導體製造和組裝方面處於領先地位。主要半導體晶圓代工廠、組裝和測試設施以及電子製造服務的存在使得邏輯 IC 的生產變得高效且具有成本效益。中國擁有龐大且快速擴張的消費性電子和汽車市場,隨著工業化和自動化的開拓,ADAS和電動車市場正在不斷發展。

- 由於國內市場的穩定表現和巨大的潛力,中國被稱為汽車和旅行行業的世界領導者。中國工業和資訊化部預測,到2025年國內汽車產量將達到3,500萬輛,進一步鞏固中國作為世界領先汽車製造商之一的地位。根據中國汽車工業協會統計,2023年8月,中國新能源汽車銷售84.6萬輛,其中搭乘用80.8萬輛,商用車3.9萬輛。純電動車保有量為 55.9 萬輛,插電式油電混合車保有量為 24.8 萬輛。

- 此外,根據中國汽車物流市場預測,到2025年,新能源乘用車類別中的純電動車(BEV)預計將佔據84%的市場佔有率,並且由於ADAS整合度的增加,這一比例預計還會增加。 2024年,中國智慧駕駛系統的採用可能會達到閾值。自動駕駛等級的採用將比預期更快,從而有可能縮短車輛更換週期。供應的增加,可能伴隨著密集的消費者教育和媒體曝光,可能會加速中國消費者向智慧駕駛的轉變。

- 亞太地區電動車市場的快速成長預計將對邏輯積體電路(IC)市場產生重大影響。隨著電動車採用 ADAS 和智慧駕駛系統等更先進的技術,對 IC,尤其是處理和控制系統的 IC 的需求可能會激增。此外,向電動車的轉變需要充電基礎設施的發展,而充電基礎設施高度依賴IC技術。因此,專門從事邏輯 IC 的半導體公司有望從全部區域不斷擴大的電動車市場中受益。

邏輯IC產業概況

由於全球參與者和中小企業的存在,邏輯 IC 市場呈現分散化。該市場的主要企業包括意法半導體、瑞薩電子公司、Analog Devices Inc.、Broadcom Inc.和Diodes Incorporated。市場上的不同參與者正在採取各種策略,例如收購和聯盟,以加強其產品陣容並獲得永續的競爭優勢。

- 2024年4月,Centrica Energy與義法半導體簽署了一份在義大利供應可再生能源的長期協議。這是義大利一座新太陽能發電廠所生產能源的為期 10 年的合約。

- 2024 年 4 月,瑞薩電子甲府工廠開始營運,這是一家專用生產晶圓的工廠。位於山梨縣甲斐市。甲府工廠先前營運瑞薩子公司瑞薩半導體製造有限公司旗下的 150mm 和 200mm 晶圓生產線。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- 市場宏觀走勢分析

- 技術簡介

第5章市場動態

- 市場促進因素

- 日益關注設備整合

- 增加工廠資本投資以提高產能

- 市場限制因素

- 邏輯 IC 設計的複雜度不斷增加

第6章 市場細分

- 按IC類型

- 數位雙極性

- 透過MOS邏輯

- MOS通用

- MOS閘陣列

- MOS驅動器/控制器

- MOS標準單元

- MOS專用

- 按用途

- 家用電子電器

- 車

- 資訊科技和通訊

- 電腦

- 其他

- 按地區

- 美國

- 歐洲

- 亞洲

- 澳洲/紐西蘭

- 中東/非洲

第7章 競爭格局

- 公司簡介

- STMicroelectronics NV

- Renesas Electronics Corp.

- Analog Devices Inc.

- Broadcom Inc.

- Diodes Incorporated

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Texas Instruments Inc.

- Intel Corporation

- Toshiba Corporation

第8章投資分析

第9章 市場的未來

The Logic IC Market size is estimated at USD 198.36 billion in 2024, and is expected to reach USD 276.33 billion by 2029, growing at a CAGR of 6.85% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 65.24 billion units in 2024 to 80.10 billion units by 2029, at a CAGR of 4.19% during the forecast period (2024-2029).

Ongoing advancements in semiconductor manufacturing processes have led to the development of more complex and efficient logic ICs. Smaller transistor sizes, improved performance, and lower power consumption enable the creation of high-performance logic ICs for a wide range of applications. A logic IC is very flexible and can be used in various applications. One can configure them to perform multiple logical functions, such as AND, OR, NOT, and XOR. This flexibility allows for designing and developing intelligent circuits that meet requirements in different industries, such as consumer electronics, automotive, telecommunications, and industry automation.

Key Highlights

- Logic ICs have significantly aided the miniaturization and integration of electronic devices. The development of the technology to manufacture semiconductors has produced small, more complex logic circuits on a single chip in recent years. This integration increases functionality while reducing electronic systems' physical size and energy consumption so that they can be used in portable devices, wireless technology, or space-constrained applications. Display drivers, general purpose logic, and MOS touch screen controllers are some of the logic components that have gained significant market traction in recent years.

- Furthermore, advances in end-user industries have created the need for small and robust semiconductor devices. For instance, nowadays, smartphones require a smaller PCB board, unlike traditional PCB boards. There has also been the advent of IoT devices, such as wearables with irregular and different shapes, which can only be achieved through miniaturization. This is expected to boost the need for miniaturized IC components significantly.

- The advent of the IoT and IIoT has largely impacted the design and size of electronics, with the introduction of technologies like smart homes, offices, wearables, remote monitoring, and control. Moreover, OEMs and designers consider miniaturization a primary focus while creating wearable technologies.

- Another advancement that demands miniaturized electronic components is portable electronic equipment, which requires smaller and thinner semiconductor systems for saving space and miniaturization. Due to highly integrated, high-speed applications like aerospace and electric vehicles, the demand for improved electrical performance to minimize noise effects is also evident. As a result of these considerations when designing end products, logic IC components are becoming increasingly important in developing advanced electronic systems.

- Logic ICs are expected to perform a wide range of complex functions. The demand for more state-of-the-art features and capabilities in electronic devices grows as technology advances. Designers need to incorporate complex logic circuits and algorithms to meet these requirements. This increased functionality leads to larger and more intricate designs, making it challenging to manage and optimize the complex interactions between different components.

- The market has undergone substantial changes due to the COVID-19 pandemic, impacting customer behavior, business revenues, and various aspects of corporate operations. The pandemic revealed previously unnoticed risks on the supply side, potentially resulting in shortages of essential parts and components. Consequently, semiconductor companies are proactively restructuring their supply chains to enhance resilience, and these adjustments may persist in the post-pandemic era.

Logic IC Market Trends

The Automotive Segment to Witness Rapid Growth

- Logic ICs are essential in vehicle control and communications systems. They are used in engine control units (ECUs), transmission control units (TCUs), antilock braking systems infotainment, airbag control modules, systems, and various other electronic control units. ICs can process and execute sophisticated algorithms and logical functions for vehicle control, monitoring, and communication.

- Consumers expect vehicles to offer advanced features, convenience, and a seamless user experience, including comfort, safety, and convenience, such as advanced driver assistance, intelligent lighting systems, personalized settings, and voice control. Meeting consumer expectations and providing innovative features drive the demand for logic ICs in the automotive industry.

- Various ADAS technologies, such as automatic emergency braking, lane departure warning, and adaptive cruise control, are becoming more prevalent in modern vehicles. Logic ICs are critical in processing sensor data, enabling real-time decision-making, and controlling vehicle functions. Future trends may involve the development of more advanced ADAS features, requiring logic ICs with higher computational power, low latency, and enhanced sensor fusion capabilities.

- In the automotive industry, safety and functional requirements are of great importance. Logic ICs ensure various automotive systems' safe and reliable operation, including ADAS, autonomous driving, and powertrain control. The need for high-performance, reliable logic ICs that meet stringent safety standards, such as ISO 26262, drives the demand in the automotive market.

- The pursuit of autonomous vehicles is a significant trend in the automotive industry. Logic ICs are essential for the complex processing and decision-making required for autonomous driving.

- According to Roland Berger, in 2025, the penetration rate of level 4 light autonomous vehicles is expected to be 1%, with a gradually increasing market share in subsequent years. Furthermore, 5% of the global market is anticipated to comprise level 4 light autonomous vehicles by 2030. As self-driving technology advances, logic ICs with increased processing power, advanced sensor integration, and robust safety features are likely to be in demand.

- Moreover, due to environmental concerns and government regulations, the shift toward the use of electric vehicles is gaining momentum. EVs are based on advanced power electronics and battery management, which requires specialized logic ICs to ensure optimum energy use, motor control, or charging infrastructure integration.

- According to the latest report from IEA, over 10 million electric vehicles were bought worldwide in 2022, and sales were estimated to increase by 35% in 2023 to reach 14 million. In 2023, China, Europe, the United States, and other regions sold 13.9 million electric vehicles.

Asia-Pacific to Register Major Growth

- Asia-Pacific consists of the analysis of only China and Japan. The region is a dynamic and rapidly growing segment of the global semiconductor industry. With emerging economies, strong manufacturing capabilities, and growing demand for electronic devices, Asia-Pacific is pivotal in driving innovation, production, and consumption of logic ICs.

- Asia-Pacific is a global manufacturing hub for semiconductor production, with countries such as China and Japan leading in semiconductor manufacturing and assembly. The presence of leading semiconductor foundries, assembly and testing facilities, and electronics manufacturing services enables efficient and cost-effective production of logic ICs. It is home to a vast and rapidly expanding consumer electronics market and automotive market with developments in ADAS and EVs along with increasing industrialization and automation.

- China is known as a global leader in the automotive and mobility industry owing to the consistent performance of the domestic market and its enormous potential. The Chinese Ministry of Industry and Information Technology projects that domestic vehicle production will reach 35 million by 2025, further strengthening its position as the world's leading car manufacturer. According to CAAM, China's new energy vehicle sales amounted to 846,000 units, 808,000 of which were passenger EVs and 39,000 were commercial electric vehicles during August 2023. Sales of BEVs and PHEVs recorded 559,000 and 248,000 vehicles, respectively.

- Furthermore, according to the forecast from China's automotive logistics market, it is expected that the battery electric vehicles (BEV) in the new energy passenger vehicle category will have 84% of the market share by 2025, which leads to major technological advancements in the segment like integration of ADAS in BEVs. In 2024, China is likely to achieve a threshold in adopting intelligent driving systems. The replacement cycle of vehicles could be shortened by more rapid adoption of AD levels than anticipated. An increase in supply may be accompanied by intensive consumer education and media exposure, which will accelerate Chinese consumers' shift toward smart driving.

- The rapid growth of EV markets in Asia-Pacific is expected to impact the logic integrated circuit (IC) market significantly. As EVs incorporate more advanced technologies like ADAS and intelligent driving systems, the demand for ICs, especially those for processing and control systems, will likely surge. Additionally, the shift toward EVs necessitates developing charging infrastructure, which relies heavily on IC technology. As a result, semiconductor companies specializing in logic ICs are poised to benefit from the expanding EV markets across the region.

Logic IC Industry Overview

The logic IC market is fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are STMicroelectronics NV, Renesas Electronics Corp., Analog Devices Inc., Broadcom Inc., and Diodes Incorporated. The various players in the market are adopting different strategies, such as acquisitions and partnerships, to enhance their product offerings and gain a sustainable competitive advantage.

- In April 2024, a long-term agreement was signed between Centrica Energy and STMicroelectronics for the supply of electricity produced from renewable sources in Italy. It is a 10-year contract for energy produced by a new solar farm in Italy.

- In April 2024, Renesas started the operation of Kofu Factory, a dedicated wafer fab. It is located in Kai City, Yamanashi Prefecture, Japan. The Kofu Factory previously operated both 150 mm and 200 mm wafer fabrication lines under Renesas Semiconductor Manufacturing Co., a subsidiary of Renesas.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Analysis of Macroeconomic Trends on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Focus on Device Integration

- 5.1.2 Increasing Capital Expenditure of Fabs to Augment Production Capacity

- 5.2 Market Restraints

- 5.2.1 Complexity Associated with Logic IC Design

6 MARKET SEGMENTATION

- 6.1 By IC Type

- 6.1.1 Digital Bipolar

- 6.1.2 By MOS Logic

- 6.1.2.1 MOS General Purpose

- 6.1.2.2 MOS Gate Arrays

- 6.1.2.3 MOS Drivers/Controllers

- 6.1.2.4 MOS Standard Cells

- 6.1.2.5 MOS Special Purpose

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 IT and Communication

- 6.2.4 Computer

- 6.2.5 Other Applications

- 6.3 By Geography***

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 STMicroelectronics NV

- 7.1.2 Renesas Electronics Corp.

- 7.1.3 Analog Devices Inc.

- 7.1.4 Broadcom Inc.

- 7.1.5 Diodes Incorporated

- 7.1.6 NXP Semiconductors NV

- 7.1.7 ON Semiconductor Corporation

- 7.1.8 Texas Instruments Inc.

- 7.1.9 Intel Corporation

- 7.1.10 Toshiba Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球消費標準邏輯IC-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

全球消費標準邏輯IC-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 消費性專用邏輯IC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

消費性專用邏輯IC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 用於電腦和周邊設備的標準邏輯 IC -市場佔有率分析、行業趨勢和統計、成長預測 (2025-2030)

用於電腦和周邊設備的標準邏輯 IC -市場佔有率分析、行業趨勢和統計、成長預測 (2025-2030) 電腦及周邊設備專用邏輯IC:全球市場佔有率分析、產業趨勢與成長預測(2025-2030)

電腦及周邊設備專用邏輯IC:全球市場佔有率分析、產業趨勢與成長預測(2025-2030) 全球專用邏輯IC市場

全球專用邏輯IC市場 專用邏輯IC的全球市場2024-2028

專用邏輯IC的全球市場2024-2028 標準邏輯IC的全球市場2024-2028

標準邏輯IC的全球市場2024-2028 專用邏輯 IC 市場報告:2030 年趨勢、預測與競爭分析

專用邏輯 IC 市場報告:2030 年趨勢、預測與競爭分析 LogicIC市場:各類型,各用途,各技術,各終端用戶,各產品,各地區-規模,佔有率,展望,機會分析,2023年~2030年

LogicIC市場:各類型,各用途,各技術,各終端用戶,各產品,各地區-規模,佔有率,展望,機會分析,2023年~2030年 全球邏輯 IC 市場規模研究與預測:按類型(TTL、CMOS、混合信號 IC)、產品類型、應用、地區劃分,2022-2029 年

全球邏輯 IC 市場規模研究與預測:按類型(TTL、CMOS、混合信號 IC)、產品類型、應用、地區劃分,2022-2029 年