|

市場調查報告書

商品編碼

1627143

北美智慧工廠:市場佔有率分析、產業趨勢與成長預測(2025-2030)North America Smart Factory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

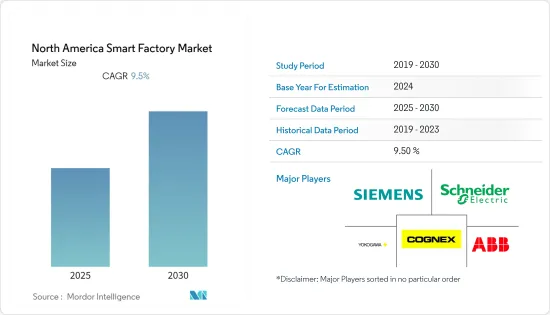

北美智慧工廠市場預計在預測期內複合年成長率為 9.5%

主要亮點

- 瑪麗維爾大學預測,到 2025 年,全球每年將產生超過 180 兆千兆位元組的資料。其中大部分將由工業物聯網支援的產業產生。根據工業IoT(IIoT) 巨頭微軟的一項研究,85% 的公司至少擁有一個 IIoT使用案例計劃。這一數字可能還會增加,94% 的受訪者表示他們將在 2021 年之前實施 IIoT 策略。

- 物聯網技術正在克服製造業的勞動力短缺問題,尤其是在美國等已開發國家。為此,在美國,聯邦政府和私人企業正在投資工業4.0物聯網技術,以擴大美國已經輸給中國和其他人事費用較低國家的工業基礎。因此,物聯網技術可能主要推動智慧工廠解決方案在全球的採用。

- 此外,最近的關稅上漲可能會迫使美國製造商以更低的成本生產商品,這可以透過自動化來實現。在關稅上調之前投資自動化的汽車公司處於領先地位,並已成為其他公司削減成本的藍圖。生產工業機器人和自動化產品的公司將受益,因為它們是自動化所需機器人和設備的最大生產商。

- 協作機器人等自動化技術需要人工干預和互動。此外,工業控制系統(ICS)存在潛在的安全風險。因此,需要實施ICS安全解決方案來防止系統受到安全威脅,增加了ICS的維修成本。網路安全解決方案的進步正在減少人們對 ICS 相關安全問題的擔憂。

北美智慧工廠市場趨勢

半導體產業顯著成長

- 該地區的電子行業正在穩步成長,並在設計和無晶圓廠領域營運的許多公司中佔有很大佔有率。根據美國人口普查局的數據,到2023年,半導體和其他電子元件產業的收益預計將達到1,051.6億美元。

- 此外,該地區對智慧型手機和消費性電子產品的需求強勁,這推動了研究市場的需求。愛立信表示,在 5G 需求的推動下,到 2025 年,智慧型手機用戶預計將達到 3.6 億。

- 此外,該地區對智慧型穿戴裝置不斷成長的需求正在引領半導體需求。據思科系統公司稱,到2022年,北美連網穿戴裝置數量將達到4.39億美元。這些發展正在增加該地區的市場需求。

- 根據半導體產業協會(SIA)統計,半導體產業在美國直接僱用了近25萬名工人。美國也是一些世界領先的汽車製造商的所在地,這些製造商正在投資電動車以及需要高性能積體電路的自動駕駛汽車的潛力。這是推動半導體矽晶圓市場需求的主要因素之一。例如,2020年12月,全球鋰離子應用矽碳複合材料供應商Group14 Technologies獲得由SK Materials主導的1,700萬美元B輪資金籌措。

- 儘管新冠疫情對美國許多人和許多行業造成了嚴重影響,但半導體產業卻是一大局部。這導致對各種晶片的需求增加,給已經全速運轉的供應鏈帶來了更大的壓力。這導致市場相關人員投資於產品開發。

通訊是市場領先的細分市場之一

- 有線通訊在將訊息從特定來源傳送到目的地時往往具有相對較小的失真。例如,當從有線類比數位轉換器接收數位編碼資料並以 8kbit/s 的固定速率傳送到單一數位控制器時,幾乎沒有資料遺失或失真。此外,還有有線網路通訊協定,例如 PROFIBUS-DP 和 ControlNet,旨在透過使用令牌控制對網路的存取來實現相對恆定的延遲設定檔。

- 例如,FieldComm Group、PI(Profibus & Profinet International)和ODAVA正在共同努力推動工業乙太網路的發展。它旨在利用 IEEE 802.3.cg 目前正在進行的工作,將 EtherNet/IP、HART-IP 和 PROFINET 的使用擴展到製程工業中的危險場所。

- 無線網路的發展為工業自動化提供了多種可能性。無線工業自動化的想法長期以來一直是許多組織無法實現的目標,但 5G 正在開始使這一目標成為現實。私人公司已經開始在其工廠內部署 5G 網路,並看到效能、延遲更低、確定性和可靠性方面的改進。

- 例如,康寧和Verizon已在康寧位於美國希科里的光纜製造工廠部署了5G超寬頻服務。康寧將使用 Verizon 的 5G 技術,在全球最大的光纖電纜製造工廠之一測試 5G 在工廠自動化、品質保證和其他增強方面的應用。

- 包含無線通訊的單一設備的成本通常比有線網路更高。然而,增加的初始成本可以透過多種方式抵消。從長遠來看,無線設備通常是最具成本效益的選擇,可以節省您生產區域內的佈線成本。

北美智慧廠產業概況

北美智慧工廠市場適度整合,有多家大型企業。公司不斷投資於策略聯盟和產品開發,以增加市場佔有率。我們將介紹一些最近的市場發展趨勢。

- 2021年4月-三菱電機公司開發了7款新的X系列產品,包括2款HVIGBT和5款HVDIODE,使X系列功率半導體模組總合達到24種。這些模組是為高電壓馬達、直流輸電設備、大容量工業設備等大容量、小容量高壓大電流設備的逆變器而開發的。將於7月起依序發售。

- 2020 年 9 月 - 西門子和格蘭富簽署數位策略合作夥伴關係關係,重點關注兩家公司在三個主要領域提供的互補產品和解決方案:用水和污水應用、工業自動化和建築技術。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 在整個價值鏈中擴大物聯網 (IoT) 技術的採用

- 對能源效率的需求不斷成長

- 市場限制因素

- 龐大資金投入轉型

- 容易受到網路攻擊

第6章 市場細分

- 依產品

- 機器視覺系統

- 相機

- 處理器

- 軟體

- 外殼

- 影像擷取卡

- 整合服務

- 照明

- 工業機器人

- 關節式機器人

- 笛卡兒機器人

- 圓柱形機器人

- SCARA機器人

- 並聯機器人

- 協作工作機器人

- 控制設備

- 繼電器和開關

- 伺服馬達及驅動器

- 感應器

- 通訊技術

- 有線

- 無線的

- 其他

- 機器視覺系統

- 依技術

- 產品生命週期管理 (PLM)

- 人機介面 (HMI)

- 企業資源規劃(ERP)

- 製造執行系統(MES)

- 集散控制系統(DCS)

- 監控控制和資料採集(SCADA)

- 可程式邏輯控制器(PLC)

- 其他

- 按最終用戶產業

- 車

- 半導體

- 石油和天然氣

- 化學/石化

- 製藥

- 航太/國防

- 飲食

- 礦業

- 其他

- 按國家/地區

- 美國

- 加拿大

第7章 競爭格局

- 公司簡介

- ABB Ltd.

- Cognex Corporation

- Siemens AG

- Schneider Electric SE

- Yokogawa Electric Corporation

- Kuka AG

- Rockwell Automation Inc.

- Honeywell International Inc.

- Robert Bosch GmbH

- Mitsubishi Electric Corporation

- Fanuc Corporation

- Emerson Electric Company

- FLIR Systems Inc.

第8章投資分析

第9章 市場未來展望

簡介目錄

Product Code: 50131

The North America Smart Factory Market is expected to register a CAGR of 9.5% during the forecast period.

Key Highlights

- The Maryville University estimates that by 2025, over 180 trillion gigabytes of data will be created worldwide every year. A large portion of this will be generated by IIoT-enabled industries. A survey by the Industrial IoT (IIoT) giant, Microsoft, found that 85% of companies have at least one IIoT use case project. This number will increase, as 94% of the respondents said they will implement IIoT strategies by 2021.

- IoT technologies are overcoming the labor shortage in the manufacturing sector, especially in the developed countries, like the United States. Due to this, the Federal Government and the private sector in the United States are investing in Industry 4.0 IoT technologies, to increase the American industrial base, which was taken over by China and other low labor cost countries. Therefore, IoT technologies may mainly drive the adoption of smart factory solutions, across the world.

- Also, the recent increase in tariffs is likely to force manufacturers of the United States to produce goods at a lower cost, which is to be achieved through automation. Auto companies that invested in automation pre-tariffs are ahead of the game, and they are the cost-saving blueprint for other companies. Companies that produce industrial robots and automation products are set to benefit, as they are the largest producers of the robots and equipment needed for automation.

- Automation technologies, such as collaborative robots, require human intervention/ interaction. Furthermore, industrial control systems (ICS) are laced with security risks. Hence, ICS security solutions must be installed to prevent security threats to the systems, which increases the cost of maintaining ICS. Nevertheless, advancements in cybersecurity solutions are reducing the fear of security issues associated with ICS.

North America Smart Factory Market Trends

Semiconductor Industry is Observing a Significant Growth

- The electronics industry in the region is growing at a steady pace and holds a prominent share in a number of enterprises operating in the design and fabless space. According to the US Census Bureau, the revenue of the semiconductors and other electronic components sector is expected to reach USD 105.16 billion by 2023.

- Moreover, the region commands significant demand for smartphones and consumer electronics, which is driving demand for the studied market. According to Ericsson, smartphone subscription is expected to reach 360 million by 2025, augmented by the demand from 5G.

- Additionally, the increasing demand for smart wearables in the region is spearheading the demand for semiconductors in the region. By 2022, the number of connected wearable devices in North America is expected to reach USD 439 million, according to Cisco Systems. Such developments are augmenting demand for the market in the region.

- According to the Semiconductor Industry Association (SIA), the semiconductor industry directly employs nearly a quarter of a million workers in the United States. The United States is also home to some of the world's major automotive players, who are investing in electric vehicles and in the self-driving potential of cars, which demand high-performance ICs. This is one of the major factors to drive demand for the semiconductors silicon wafers market. For instance, in December 2020, Group14 Technologies, a global provider of silicon-carbon composite materials for lithium-ion applications, secured USD 17 million in Series B funding led by SK Materials.

- The pandemic has been brutally bad for many people and industries in the United States, but the semiconductor industry has been one of the only bright spots. That translates to additional demand for chips of all sorts, which increased the pressure on a supply chain that was already running as fast as it could. Thus, driving market players to invest in product development.

Communication is One of the Segment Driving the Market

- Wired communication tends to have a relatively low degree of distortion when delivering information from a particular source to a destination. For instance, receiving digitally encoded data from a wired analog to digital converter, sent to a single digital controller at a fixed rate of 8 kbit/second, occurs with little data loss and distortion, i.e., only the least significant bits tend to have errors. In addition, there are wired networking protocols that aim to achieve a relatively constant delay profile by using a token to control access to the network, such as PROFIBUS-DP and ControlNet.

- For instance, FieldComm Group, PI (Profibus & Profinet International), and ODAVA are working together to promote developments for Industrial Ethernet. It is aimed to expand the use of EtherNet/IP, HART-IP, and PROFINET into hazardous locations in the process industry, leveraging the work currently underway in the IEEE 802.3.cg.

- Wireless networks are advancing in ways that are driving many possibilities for industrial automation. The idea of wireless industrial automation has long been an unachievable goal for many organizations, but 5G is starting to make this goal a reality. Companies are already beginning to deploy private 5G networks within plants and are seeing an increase in performance, low latency, determinism, and reliability.

- For instance, Corning and Verizon have installed a 5G Ultra-Wideband service in Corning's fiber optic cable manufacturing facility in Hickory, United States. Corning will use Verizon's 5G technology to test the application of 5G to enhance functions, such as factory automation and quality assurance, in one of the most extensive fiber optic cable manufacturing facilities in the world.

- Individual devices incorporating wireless communication are generally costlier than wired networks. However, this increased upfront cost offset in multiple ways. Wireless devices often prove to be the most cost-effective option over the long run, owing to factors such as saving the cost of running cabling through a production area.

North America Smart Factory Industry Overview

The North American Smart Factory Market is moderately consolidated, with the presence of a few major companies. The companies are continuously investing in making strategic partnerships and product developments to gain more market share. Some of the recent developments in the market are:

- April 2021- Mitsubishi Electric Corporation developed seven new X-Series products, including two HVIGBTs and five HVDIODEs, bringing the total number of X-Series power semiconductor modules to 24. These modules are designed for increasingly big-capacity, small-sized inverters used in traction motors, DC-power transmitters, substantial industrial machines, and other high-voltage, large-current equipment. Beginning in July, the models will be released in order.

- September 2020 - Siemens and Grundfos signed a digital partnership framework for strategic cooperation between the two companies to focus on complementary products and solutions provided by both parties in three main areas: water and wastewater applications, industrial automation and building technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Covid-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Internet of Things (IoT) Technologies Across the Value Chain

- 5.1.2 Rising Demand for Energy Efficiency

- 5.2 Market Restraints

- 5.2.1 Huge Capital Investments for Transformations

- 5.2.2 Vulnerable to Cyber Attacks

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Machine Vision Systems

- 6.1.1.1 Cameras

- 6.1.1.2 Processors

- 6.1.1.3 Software

- 6.1.1.4 Enclosures

- 6.1.1.5 Frame Grabbers

- 6.1.1.6 Integration Services

- 6.1.1.7 Lighting

- 6.1.2 Industrial Robotics

- 6.1.2.1 Articulated Robots

- 6.1.2.2 Cartesian Robots

- 6.1.2.3 Cylindrical Robots

- 6.1.2.4 SCARA Robots

- 6.1.2.5 Parallel Robots

- 6.1.2.6 Collaborative Industry Robots

- 6.1.3 Control Devices

- 6.1.3.1 Relays and Switches

- 6.1.3.2 Servo Motors and Drives

- 6.1.4 Sensors

- 6.1.5 Communication Technologies

- 6.1.5.1 Wired

- 6.1.5.2 Wireless

- 6.1.6 Other Products

- 6.1.1 Machine Vision Systems

- 6.2 By Technology

- 6.2.1 Product Lifecycle Management (PLM)

- 6.2.2 Human Machine Interface (HMI)

- 6.2.3 Enterprise Resource and Planning (ERP)

- 6.2.4 Manufacturing Execution System (MES)

- 6.2.5 Distributed Control System (DCS)

- 6.2.6 Supervisory Controller and Data Acquisition (SCADA

- 6.2.7 Programmable Logic Controller (PLC)

- 6.2.8 Other Technologies

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Semiconductors

- 6.3.3 Oil and Gas

- 6.3.4 Chemical and Petrochemical

- 6.3.5 Pharmaceutical

- 6.3.6 Aerospace and Defense

- 6.3.7 Food and Beverage

- 6.3.8 Mining

- 6.3.9 Other End-user Industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Cognex Corporation

- 7.1.3 Siemens AG

- 7.1.4 Schneider Electric SE

- 7.1.5 Yokogawa Electric Corporation

- 7.1.6 Kuka AG

- 7.1.7 Rockwell Automation Inc.

- 7.1.8 Honeywell International Inc.

- 7.1.9 Robert Bosch GmbH

- 7.1.10 Mitsubishi Electric Corporation

- 7.1.11 Fanuc Corporation

- 7.1.12 Emerson Electric Company

- 7.1.13 FLIR Systems Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

02-2729-4219

+886-2-2729-4219

2025 年智慧工廠全球市場報告

2025 年智慧工廠全球市場報告 數位工廠數據

數位工廠數據 2025-2033 年日本智慧工廠市場報告(按現場設備、技術、最終用途產業和地區)

2025-2033 年日本智慧工廠市場報告(按現場設備、技術、最終用途產業和地區) 智慧工廠市場規模、佔有率、趨勢分析報告:按現場設備、按技術、按應用、按地區、細分市場預測,2025-2030 年

智慧工廠市場規模、佔有率、趨勢分析報告:按現場設備、按技術、按應用、按地區、細分市場預測,2025-2030 年 智慧工廠介紹:2024智慧工廠市場:按技術、組件和行業分類 - 2025-2030 年全球預測智慧工廠市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、技術、最終用戶產業、地區和競爭細分,2019-2029F2024-2032 年按現場設備、技術、最終用途產業和地區分類的智慧工廠市場報告智慧工廠市場報告:2030 年趨勢、預測與競爭分析

智慧工廠介紹:2024智慧工廠市場:按技術、組件和行業分類 - 2025-2030 年全球預測智慧工廠市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、技術、最終用戶產業、地區和競爭細分,2019-2029F2024-2032 年按現場設備、技術、最終用途產業和地區分類的智慧工廠市場報告智慧工廠市場報告:2030 年趨勢、預測與競爭分析 智慧工廠全球市場2024-2028

智慧工廠全球市場2024-2028

▼