|

市場調查報告書

商品編碼

1628706

聲學感測器 -市場佔有率分析、行業趨勢/統計、成長預測 (2025-2030)Acoustic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

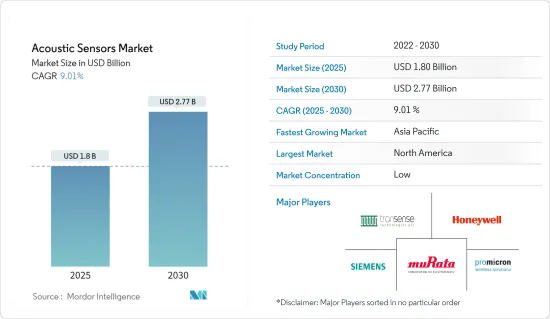

聲學感測器市場規模預計到 2025 年為 18 億美元,預計到 2030 年將達到 27.7 億美元,預測期內(2025-2030 年)複合年成長率為 9.01%。

主要亮點

- 大多數人使用基於攝影機的感測技術。由於基於 RF 的方法簡單且侵入性低,因此研究主要集中在這種方法上。由於RFID不需要電池,因此經常用於供應鏈管理和儲存等企業業務。此外,由於室內 WiFi 基礎設施的廣泛可用性,基於 WiFi 的感測方法已被證明在將感測功能整合到智慧家庭和職場方面非常有效。

- 除了攝影機和基於射頻的解決方案之外,聲學訊號代表了感測的第3D。為了降噪和遠距離拾音,Galaxy Note 3和Amazon Echo內建了多個高性能麥克風。 Galaxy S9 和 Google Home 配備了多個立體聲揚聲器。此外,許多行動裝置現在提供發燒級的高品質錄音(例如 192kHz),大大提高了基於聲學的檢測能力。

- 此外,通訊行業的進步正在推動整個聲學感測器市場的發展。根據GSMA統計,截至2024年1月,已有47通訊業者在獨立(SA)網路上部署了商用5G服務。此外,超過一半的營運商預計將在標準發布一年內實施 5G-Advanced。 2024 年 5G SA 和 5G-Advanced 的推廣可能會引發新一波 5G 投資,特別是在關鍵市場。

- 此外,當今汽車應用對聲學感測器的需求量很大。電動車中使用的馬達完全靜音,可能會對粗心的行人造成危險。因此,現代電動和混合動力汽車必須配備聲音警報系統。因此,對交通管理的日益關注預計將推動市場成長。根據瑞銀預測,到 2030 年,全球自動駕駛汽車感測器半導體市場規模預計將達到 300 億美元。汽車趨勢的變化可能會導致預測期內汽車聲學感測器的潛在成長。

- 各種公司正在投資各種應用的聲學感測器,包括國防應用中有毒有害蒸氣的環境監測、食品分析和控制以及引擎油老化、微生物和癌細胞檢測等醫療應用。智慧型設備。例如,2024年7月,特斯拉宣布有意推出自動駕駛叫車服務,但前提是自動駕駛技術已解決。特斯拉的專利詳細介紹了一種先進的感測器陣列,其中包括影像、聲學、熱學、壓力、電容、射頻和氣體感測器,用於監控車輛內部環境。

- 聲學感測器面臨許多技術挑戰,包括刺耳的聲音洩漏和高功耗,這相對縮短了電池供電設備的電池壽命。

- 此外,持續的政治動盪和挫折預計將對電子產業產生重大影響。這場衝突已經加劇了已經影響該行業的半導體供應鏈問題和晶片短缺問題。這種破壞可能以鎳、鈀、銅、鈦、鋁和鐵礦石等關鍵原料的價格波動的形式出現,導致材料短缺。這被認為會在聲學感測器的生產中引起問題。

聲學感測器市場趨勢

消費性電子產品推動市場成長

- 聲學感測器廣泛應用於家用電子電器,特別是智慧型手機和筆記型電腦。家用電子電器極大地促進了合適的感測器和技術的開發,消費性電子產品是聲學感測器的重要投資者和消費者。愛立信數據顯示,2023年第二季全球5G用戶數激增1.75億,總合接近13億人。中國、印度和美國的智慧型手機行動網路訂閱數量最多。

- 在許多消費和通訊應用中,聲學感測器的使用極大地有助於射頻濾波器的開發。例如,創建一個聲學設備相對容易。由於表面波聲濾波器在智慧型手機領域的廣泛使用,感測器材料的成本在過去三十年中有所下降。

- 大多數電話和類似設備都包括麥克風和揚聲器,它們有利於聲學感測應用,並且實施起來相對便宜。

- 此外,2023 年 11 月,日本科技巨頭 NEC Corporation 開始在亞太地區擴展萬事達卡的生物識別結帳計畫。 NEC 和萬事達卡簽署了一份合作備忘錄,同意將 NEC 的尖端臉部認證和生物識別技術整合到該計劃中。

- 由於 LTE、4G 和 5G 設備(尤其是 5G 智慧型手機)產量的增加,聲學技術公司擁有巨大的業務擴展機會。由於射頻濾波器能夠將無線電訊號與智慧型手機用來發送和接收資料的多個頻段分開,因此射頻濾波器正日益成為這些設備中的標準組件。

- 隨著 5G 技術的出現,新型先進 SAW 濾波器的發展潛力更大,因為它們在低於 2.7GHz 頻率範圍內提供比競爭性 BAW 濾波器更高性能的解決方案。家用電子電器的此類發展可能會進一步推動所研究的市場成長。

亞太地區成長率顯著

- 由於亞太地區在全球半導體製造業中佔據主導地位,預計在預測期內將顯著成長。該地區也是全球領先的家用電子電器、電動車和先進電子設備製造商之一,也是全球聲學感測器的主要消費者之一。 GSMA 報告稱,到 2023 年,該地區將擁有 14.5 億行動網路用戶和近 20 億個 4G 連線。到2024年初,該地區已累積3億個5G連接,用戶滲透率達10%。

- 由於該地區專注於建設基礎設施以實現 5G 技術,因此預計該地區對射頻半導體的需求將會增加。 GSMA預測,2020年至2025年間,亞太地區行動電話電信商將在網路上投資超過4,000億美元,其中3,310億美元將專門用於5G部署。

- 由於美國、中國、韓國、日本和印度等主要和新興國家的智慧型手機、平板電腦和其他電子設備的使用量增加,聲學感測器預計將在預測期內擴大。根據IBEF統計,2024年第一季印度智慧型手機出貨量達3,530萬部,較去年同期成長8%。此外,2023 年報告預測,全球高階智慧型手機市場將在中國、印度、中東和非洲以及拉丁美洲實現創紀錄的銷售量。尤其是印度,將成為全球成長最快的高階市場。

- 大多數知名智慧型手機製造商,包括 LG 和三星,都在其最新的 5G 型號中使用射頻濾波器。 SAW 感測器的開發也使 5G 和 4G 多模行動裝置能夠以比性能指標相當的競爭性商業替代品更低的成本使用更節能的射頻路徑。

- 由於聲學感測器在家用電子電器的廣泛應用,中國目前佔據亞太聲學感測器市場的最高佔有率。聲學感測器在其他重要的最終用戶產業(包括汽車、國防和工業領域)的使用尤其廣泛。根據國際能源總署(IEA)預測,2023年中國新電動車登記數量將快速成長,達810萬輛,與前一年同期比較增加35%。

聲學感測器產業概況

聲學感測器市場適度細分,由多家主要企業組成。從市場佔有率來看,目前幾家主要企業佔據市場主導地位。然而,創新和永續技術使許多公司能夠透過贏得新合約和開拓新市場來擴大其市場佔有率。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- 產業價值鏈分析

- 評估宏觀經濟趨勢對市場的影響

第5章市場動態

- 市場促進因素

- 通訊市場的成長

- 製造成本低

- 市場限制因素

- 與聲學感測器相關的技術問題

第6章 市場細分

- 按類型

- 有線

- 無線的

- 按波浪類型

- 表面波

- 體波

- 按感測參數

- 溫度

- 壓力

- 扭力

- 按用途

- 車

- 航太/國防

- 家用電子電器

- 醫療保健

- 工業的

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- Siemens AG

- Transense Technologies PLC

- Pro-micron GmbH

- Honeywell Sensing and Productivity Solutions

- Murata Manufacturing Co., Ltd.

- Vectron International Inc.(Microchip technology Incorporated)

- IFM Efector Inc.

- Dytran Instruments Inc.

- CTS Corporation

- Campbell Scientific Inc.

- API Technologies Corp.

第8章投資分析

第9章 未來趨勢

簡介目錄

Product Code: 51622

The Acoustic Sensors Market size is estimated at USD 1.80 billion in 2025, and is expected to reach USD 2.77 billion by 2030, at a CAGR of 9.01% during the forecast period (2025-2030).

Key Highlights

- Most people use camera-based sensing. Research has focused on RF-based approaches for their ease and lack of intrusion. Because RFID doesn't require batteries, it is frequently used in corporate operations like supply chain management and storage. Furthermore, WiFi-based sensing approaches have been shown to be quite effective in integrating sensing functions in a smart home or workplace due to the widespread availability of indoor WiFi infrastructures.

- Acoustic signals offer a third dimension for sensing in addition to camera- and RF-based solutions since microphones and speakers are increasingly often found in mobile, wearable, and smart appliance devices. For noise reduction and far-field speech pickup, the Galaxy Note 3 and Amazon Echo include numerous sophisticated microphones built into them. Both the Galaxy S9 and Google Home have multiple stereo speakers. Additionally, many mobile devices now offer high recording quality (such as 192 kHz) aimed at audiophiles, which has significantly improved acoustic-based detection capabilities.

- Furthermore, advancement in the communication industry is boosting the overall acoustic sensor market. According to GSMA, As of January 2024, 47 operators have rolled out commercial 5G services on Standalone (SA) networks. Additionally, over half of these operators anticipate implementing 5G-Advanced within a year of its standard release. The surge in 5G SA and 5G-Advanced initiatives in 2024 is poised to catalyze a fresh wave of 5G investments, particularly in leading markets.

- Moreover, acoustic sensors have recently seen significant demand in automotive applications. The complete silence of the motors used in EVs may pose a hazard to inattentive pedestrians. As a result, the latest electric and hybrid cars will have to be equipped with an acoustic warning system. Therefore, rising concerns regarding traffic management will drive market growth. According to UBS, the global market for sensor semiconductors in autonomous vehicles is anticipated to reach USD 30 billion by 2030. Changes in automotive trends may lead to potential growth for acoustic sensors for automotive applications during the forecast period.

- Various companies are investing in Acoustic sensors due to their deployment in smart devices that can be used in diverse fields like environmental monitoring of toxic and hazardous vapors in defense applications, food analysis and control, engine oil aging, microorganism, and healthcare applications like cancer cell detection. For instance, in In July 2024, Tesla unveiled its intentions to introduce an automated ride-hailing service, contingent on resolving self-driving technology. Tesla's patent details a sophisticated sensor array, encompassing image, acoustic, thermal, pressure, capacitive, radio frequency, and gas sensors, to monitor the vehicle's interior environment. such instances are creating the demand for acoustic sensors from automotive industry.

- There are many technical challenges associated with acoustic sensors, such as annoying audible sound leakage and large power consumption, which can relatively reduce the battery life of battery-powered devices, and the acoustic sensing system can affect the music play and voice calls.

- Furthermore, the ongoing political pus and downs are expected to impact the electronics industry significantly. The conflict has already exacerbated the semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may come in the form of volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, aluminum, and iron ore, resulting in material shortages. This would obstruct the manufacturing of acoustic sensors.

Acoustic Sensors Market Trends

Consumer Electronics to Drive the Market Growth

- Acoustic sensors are widely used in consumer electronics, notably smartphones and laptops. The development of the appropriate sensors and technologies was greatly aided by consumer electronics, one of the significant investors and consumers of acoustic sensors. According to Ericsson, in Q2 of 2023, global 5G subscriptions surged by 175 million, nearing a total of 1.3 billion. China, India, and the United States have the highest smartphone mobile network subscriptions.

- In many consumer and communication applications, using sound sensors greatly aided the development of RF filters. For instance, the creation of acoustic devices is relatively straightforward. The cost of sensor materials has declined over the past three decades due to the widespread use of surface wave acoustic filters in the smartphone sector.

- Most telephones and comparable devices are equipped with microphones and speakers that facilitate acoustic-sensing applications and have a comparatively cheap implementation cost.

- Further, iIn November 2023, NEC Corporation, a leading Japanese technology firm, took the helm in expanding the Mastercard Biometric Checkout Programme across the Asia Pacific (APAC). Signing a Memorandum of Understanding, NEC and Mastercard agreed to integrate NEC's cutting-edge face recognition and liveness verification tech into the initiative, aiming to boost its uptake among APAC merchants.

- Acoustic wave technology companies have a massive opportunity to expand due to the rising production of LTE, 4G, and 5G devices, particularly 5G smartphones. Due to their ability to separate radio signals from the many spectrum bands smartphones utilize to receive and send data, RF filters are increasingly employed as standard parts in these devices.

- With the advent of 5G technology, new advanced SAW filters have more development potential since they provide a higher performance solution than competitive BAW filters in the sub-2.7 GHz frequency region. Such developments in consumer electronics may further propel the studied market growth.

Asia-Pacific to Witness a Significant Growth Rate

- The Asia-Pacific region is anticipated to grow significantly over the forecast period due to its dominance in the global semiconductor manufacturing industry. The region is also one of the global manufacturers of consumer electronics, electric vehicles, and advanced electronic devices, among others, making it one of the significant consumers of acoustic sensors globally. In 2023, the region boasted 1.45 billion mobile internet subscribers and nearly 2 billion 4G connections, as reported by GSMA. By early 2024, the region had already amassed 300 million 5G connections, marking a 10% adoption rate among subscribers.

- The region's demand for RF semiconductors is anticipated to rise due to the growing emphasis on expenditures to build infrastructure to enable 5G technology. The GSMA estimates that between 2020 and 2025, mobile operators in the Asia-Pacific region will invest more than USD 400 billion in their networks, of which USD 331 billion will go toward 5G deployments.

- Acoustic sensors are anticipated to expand throughout the projected period due to the rising use of smartphones, tablets, and other electronic devices in major and emerging countries, including the United States, China, South Korea, Japan, and India. According to IBEF,In the first quarter of 2024, India's smartphone shipments surged by 8% year-on-year, hitting a total of 35.3 million units.. Further, in its 2023 report it was stated on the global premium smartphone market forecasts record-setting sales in China, India, the Middle East, Africa, and Latin America. India, in particular, is set to lead as the world's fastest-growing premium market..

- Most well-known smartphone manufacturers, including LG and Samsung, use RF filters in their most recent 5G models. The development of SAW sensors also makes it possible for 5G and 4G multimode mobile devices to use more power-efficient RF pathways at a lower cost than competing commercial alternatives with comparable performance metrics.

- Due to the widespread usage of acoustic sensors in consumer electronics, China now owns the highest share of the Asia-Pacific acoustic sensor market. The use of acoustic sensors in other significant end-user industries, including the automotive, defense, and industrial sectors, is particularly strong. According to international Energy Agency , In 2023, China saw a surge in new electric car registrations, hitting 8.1 million, marking a 35% rise from the previous year. such instances are playing a huge role in the growth of the studied market.

Acoustic Sensors Industry Overview

The Acoustic Sensors Market is moderately fragmented and consists of several prominent players. In terms of market share, some of the significant players currently dominate the market. However, with innovative and sustainable technologies, many organizations expand their market existence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Telecommunications Market

- 5.1.2 Low Manufacturing Costs

- 5.2 Market Restraints

- 5.2.1 Technical Challenges Associated with Acoustic Sensors

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wired

- 6.1.2 Wireless

- 6.2 By Wave Type

- 6.2.1 Surface Wave

- 6.2.2 Bulk Wave

- 6.3 By Sensing Parameter

- 6.3.1 Temperature

- 6.3.2 Pressure

- 6.3.3 Torque

- 6.4 By Application

- 6.4.1 Automotive

- 6.4.2 Aerospace & Defense

- 6.4.3 Consumer Electronics

- 6.4.4 Healthcare

- 6.4.5 Industrial

- 6.4.6 Other Applications

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Transense Technologies PLC

- 7.1.3 Pro-micron GmbH

- 7.1.4 Honeywell Sensing and Productivity Solutions

- 7.1.5 Murata Manufacturing Co., Ltd.

- 7.1.6 Vectron International Inc. (Microchip technology Incorporated)

- 7.1.7 IFM Efector Inc.

- 7.1.8 Dytran Instruments Inc.

- 7.1.9 CTS Corporation

- 7.1.10 Campbell Scientific Inc.

- 7.1.11 API Technologies Corp.

8 INVESTMENT ANALYSIS

9 FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

亞太地區聲學感測器 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

亞太地區聲學感測器 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 北美聲學感測器:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)

北美聲學感測器:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年) 歐洲聲學感測器:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲聲學感測器:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 美國聲學感測器:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)

美國聲學感測器:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030) 聲學感測器市場:按類型、波形、感測參數、應用分類 - 2025-2030 年全球預測

聲學感測器市場:按類型、波形、感測參數、應用分類 - 2025-2030 年全球預測 聲波感測器市場:按產品類型、設備、感測參數、產業分類 - 2025-2030 年全球預測

聲波感測器市場:按產品類型、設備、感測參數、產業分類 - 2025-2030 年全球預測 聲波感測器的全球市場規模:按技術、按感測參數、按應用、按地區、範圍和預測

聲波感測器的全球市場規模:按技術、按感測參數、按應用、按地區、範圍和預測 聲波感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、設備、垂直領域、地區和競爭細分,2019-2029F

聲波感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、設備、垂直領域、地區和競爭細分,2019-2029F 聲波感測器市場、機會、成長動力、產業趨勢分析與預測,2024-2032

聲波感測器市場、機會、成長動力、產業趨勢分析與預測,2024-2032 聲音感測器(聲音感測器):市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

聲音感測器(聲音感測器):市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

▼