|

市場調查報告書

商品編碼

1631592

東協 UPVC 門窗:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)ASEAN UPVC Doors And Windows - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

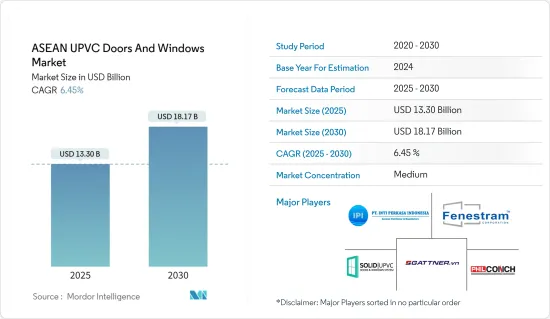

預計2025年東協UPVC門窗市場規模為133億美元,預計2030年將達181.7億美元,複合年成長率為6.45%。

近年來,東南亞國協的建築業取得了顯著的成長。對門窗(包括 UPVC 產品)的需求增加直接歸因於此成長。 UPVC門窗因其耐用性、能源效率、低維護要求和成本效益而在東南亞國協廣受歡迎。它廣泛用於商業、工業和住宅用途。

東南亞國協收入階層不斷壯大,可支配收入不斷增加,導致住宅和建築計劃支出增加,進一步拉動了對UPVC門窗的需求。多個東南亞國協正在投資機場、公路、鐵路和智慧城市等基礎設施發展計劃。這些計劃需要高品質的門窗,包括 UPVC 產品。東協各國政府正在實施能源效率法規並推廣永續建築方法。 UPVC 門窗以其優異的隔熱性能而聞名,使其成為節能建築的有吸引力的選擇。

東協UPVC門窗市場趨勢

越南高成長帶動東協市場

在整個研究期間,越南由於快速的工業化和都市化已成為東南亞國協中成長最快的市場。人們對 UPVC 優點的認知不斷增強,加上該國住宅和商業建設活動的蓬勃發展,可能會推動 UPVC 在門窗中的使用增加。在目前處於市場前沿的亞太地區,UPVC門窗的需求正在快速成長,這主要得益於產品創新和技術進步。該地區不斷擴大的電氣和電子工業、汽車工業的快速成長以及整體工業化進一步推動了這一成長。

商業領域的快速成長推動市場

印尼、泰國、越南和馬來西亞等東南亞國協的工業和建築業正在快速成長。這種快速成長增加了對 UPVC 門窗的需求。這些國家的快速都市化和正在進行的基礎設施計劃進一步推動了這項需求。隨著城市的擴張和新計劃的出現,UPVC 門窗的能源效率和美觀變得至關重要。東南亞國協的消費者越來越意識到UPVC門窗的好處,包括增強安全性、降噪和耐候性。因此,木材和鋁等傳統材料明顯轉向 UPVC。

東協UPVC門窗產業概況

東協UPVC門窗市場較為分散。本報告重點介紹了東協 UPVC 門窗市場的主要國際參與者。目前,INTI PERKASA INDONESIA、SOLID UPVC Doors & Windows System、PHILCONCH、Gartner.vn 和 Fenestram Corp. 等少數菁英公司在市場上佔據主導地位。然而,技術進步和產品創新使中小企業能夠增加市場佔有率、贏得新契約並開拓未開發的市場。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察與動態

- 市場概況

- 市場促進因素

- UPVC 產品的耐用性和低維護性推動了市場

- 市場限制因素

- UPVC門窗的安裝流程

- 市場機會

- 住宅重建和改建趨勢的上升創造了機會

- 價值鏈/供應鏈分析

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- 洞察市場創新

- COVID-19 對市場的影響

第5章市場區隔

- 依產品類型

- UPVC門

- UPVC窗

- 按最終用戶類型

- 住宅

- 商業的

- 按分銷管道

- 實體門市

- 網路商店

- 按地區

- 印尼

- 馬來西亞

- 菲律賓

- 新加坡

- 泰國

- 越南

- 其他東南亞國協

第6章 競爭狀況

- 公司簡介

- Deceuninck

- INTI PERKASA INDONESIA

- LG Hausys

- VINCA

- ARC Component Manufacturing Rayong Co. Ltd

- SOLID|UPVC Doors & Windows System

- Aluplast

- Fenestram Corp.

- PHILCONCH

- VEKA

- Gattner*

第7章 市場趨勢

第8章 免責聲明

The ASEAN UPVC Doors And Windows Market size is estimated at USD 13.30 billion in 2025, and is expected to reach USD 18.17 billion by 2030, at a CAGR of 6.45% during the forecast period (2025-2030).

ASEAN countries have witnessed significant growth in the construction industry in recent years. The rising demand for doors and windows, including UPVC products, can be directly attributed to this growth. UPVC doors and windows are popular in ASEAN countries due to their durability, energy efficiency, low maintenance requirements, and cost-effectiveness. They are extensively utilized in commercial, industrial, and residential structures.

The rising middle-income group population in ASEAN countries has increased disposable incomes, which has resulted in higher spending on housing and construction projects, further driving the demand for UPVC doors and windows. Several ASEAN countries are investing in infrastructure development projects, such as airports, roads, railways, and smart cities. These projects require high-quality doors and windows, including UPVC products. Governments across ASEAN countries have been implementing energy efficiency regulations and promoting sustainable construction practices. UPVC doors and windows are known for their excellent thermal insulation properties, making them an attractive choice for energy-efficient buildings.

ASEAN UPVC Doors & Windows Market Trends

Vietnam's High Growth Rate Driving the ASEAN Market

Throughout the study period, Vietnam's swift industrialization and urbanization have positioned it as the fastest-growing market across ASEAN countries. Growing awareness of the benefits of UPVC, coupled with the country's booming residential and commercial construction activities, is set to drive the increased use of UPVC in doors and windows. The Asia-Pacific, currently at the forefront of the market, is witnessing a surge in demand for UPVC doors and windows, primarily driven by product innovations and technological advancements. This growth is further bolstered by the region's expanding electric and electronic industries, a burgeoning automotive industry, and overall industrialization.

Rapid Growth in the Commercial Segment Fueling the Market

ASEAN countries, including Indonesia, Thailand, Vietnam, and Malaysia, have seen robust growth in their industrial and construction sectors. This surge has spurred a heightened demand for UPVC doors and windows, driven by the rising need for commercial and industrial buildings. Rapid urbanization and ongoing infrastructure projects across these nations further bolster this demand. As cities expand and new projects emerge, the energy efficiency and aesthetic appeal of UPVC doors and windows become paramount. Consumers in ASEAN nations are increasingly recognizing the benefits of UPVC doors and windows, including enhanced security, noise reduction, and weather resistance. Consequently, there has been a marked shift toward UPVC, shifting focus from conventional materials such as wood and aluminum.

ASEAN UPVC Doors & Windows Industry Overview

The ASEAN UPVC doors and windows market exhibits fragmentation. This report highlights key international players in the ASEAN UPVC doors and windows market. Currently, a select few, including INTI PERKASA INDONESIA, SOLID UPVC Doors & Windows System, PHILCONCH, Gartner.vn, and Fenestram Corp., dominate the market in terms of share. However, driven by technological advancements and product innovations, mid-sized and smaller firms are bolstering their market presence, clinching new contracts, and exploring untapped markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Durability and Low Maintenance of UPVC Products Driving the Market

- 4.3 Market Restraints

- 4.3.1 Installation Process for UPVC Doors and Windows

- 4.4 Market Opportunities

- 4.4.1 Rising Trends of Home Renovations and Remodeling Creating Opportunities

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Innovations in the Market

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 UPVC Doors

- 5.1.2 UPVC Windows

- 5.2 End-user Type

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 Distribution Channel

- 5.3.1 Offline Stores

- 5.3.2 Online Stores

- 5.4 Geography

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Philippines

- 5.4.4 Singapore

- 5.4.5 Thailand

- 5.4.6 Vietnam

- 5.4.7 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Deceuninck

- 6.1.2 INTI PERKASA INDONESIA

- 6.1.3 LG Hausys

- 6.1.4 VINCA

- 6.1.5 ARC Component Manufacturing Rayong Co. Ltd

- 6.1.6 SOLID | UPVC Doors & Windows System

- 6.1.7 Aluplast

- 6.1.8 Fenestram Corp.

- 6.1.9 PHILCONCH

- 6.1.10 VEKA

- 6.1.11 Gattner*

7 MARKET FUTURE TRENDS

8 DISCLAIMER

UPVC 門窗:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

UPVC 門窗:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 中國 UPVC 門窗:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國 UPVC 門窗:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)![PVC 窗戶市場:趨勢、機會與競爭分析 [2024-2030]](/sample/img/cover/42/1448492.png) PVC 窗戶市場:趨勢、機會與競爭分析 [2024-2030]

PVC 窗戶市場:趨勢、機會與競爭分析 [2024-2030] 住宅 UPVC 門窗市場 - 按產品類型(UPVC 門和 UPVC 窗)、配銷通路(實體門市和線上商店)按地區、競爭分類的全球行業規模、佔有率、趨勢、機會和預測,2018-2028 年

住宅 UPVC 門窗市場 - 按產品類型(UPVC 門和 UPVC 窗)、配銷通路(實體門市和線上商店)按地區、競爭分類的全球行業規模、佔有率、趨勢、機會和預測,2018-2028 年 商用 UPVC 門窗市場 - 按產品類型(UPVC 門和 UPVC 窗)、配銷通路(實體門市和線上商店)按地區、競爭細分的全球行業規模、佔有率、趨勢、機會和預測 2018-2028

商用 UPVC 門窗市場 - 按產品類型(UPVC 門和 UPVC 窗)、配銷通路(實體門市和線上商店)按地區、競爭細分的全球行業規模、佔有率、趨勢、機會和預測 2018-2028 PVC簡介窗市場:各產品類型,各終端用戶,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測

PVC簡介窗市場:各產品類型,各終端用戶,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測![uPVC門窗市場:趨勢、機遇、競爭分析 [2023-2028]](/sample/img/cover/42/1289750.png) uPVC門窗市場:趨勢、機遇、競爭分析 [2023-2028]

uPVC門窗市場:趨勢、機遇、競爭分析 [2023-2028]