|

市場調查報告書

商品編碼

1632096

美國智慧電錶:市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)United States Smart Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

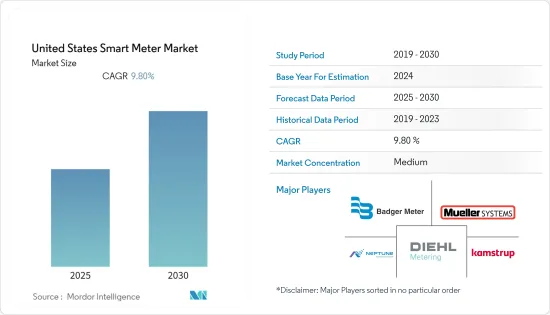

美國智慧電錶市場預計在預測期內複合年成長率為 9.8%。

主要亮點

- 隨著公用事業公司尋求更有效率、可靠和安全的方式來管理能源發電、傳輸和分配,智慧電網是一種將能源供應與特定市場的需求相匹配的有效方法,同時消除了浪費。智慧電錶是智慧電網中最重要的設備之一,具有公用事業公司和客戶之間的雙向通訊功能。近年來,美國對智慧電網計劃的投資增加,各種政府政策,特別是強制要求和財政獎勵,是智慧電錶市場採用的主要推動力。

- 例如,2021 年 9 月,美國農業部宣布投入 4.64 億美元,用於建造或改善可再生能源基礎設施,幫助48 個州的農村社區、農業生產者和企業降低能源成本,波多黎各也宣布將進行投資。農業部透過電力貸款計畫提供了 3.35 億美元融資,其中 1.02 億美元用於智慧電網技術投資。

- 此外,消費者對智慧和環保服務的需求不斷增加,消費者現在正在尋找個人化服務,以最佳化其使用並減少帳單。透過智慧電錶資料,公用事業公司可以幫助客戶降低能源成本,這也是推動市場成長的因素。

- 在 COVID-19 爆發之初,許多智慧電錶製造商面臨的主要影響是生產中斷導致的供應問題。此外,由於封鎖措施,住宅、商業和工業對智慧電錶的需求也有所下降。然而,隨著疫情封鎖的放鬆,智慧電錶的製造和供應正在恢復到正常水平,許多製造商的銷售開始復甦。

- 然而,安裝智慧電錶基礎設施的初始投資通常遠高於傳統電錶,並且需要更長的時間才能獲得高投資回報。龐大的資本需求對能源消費者和電力公司來說都是一個重大挑戰,也是一種市場限制。

美國智慧電錶市場趨勢

智慧燃氣表領域顯著成長

- 智慧型瓦斯表使用超音波或電磁技術來測量瓦斯流量,並使用無線通訊連接到區域網路或廣域網路。

- 它還配備了洩漏和衝擊檢測系統,可以檢測緊急情況,並在發生地震活動或燃氣洩漏時立即關閉燃氣流,或啟用遠端控制以確保安全。智慧型瓦斯表依靠低壓電池供電來延長使用壽命並避免火災風險。

- 智慧燃氣表使燃氣公司能夠有效管理能源生產、發行和交付業務,降低成本並最佳化資源分配。遠端監控客戶消費量並打開和關閉燃氣,避免昂貴的現場訪問。

- 2021 年 8 月,美國電力公司路易斯維爾天然氣電力公司(LG&E) 和肯塔基州公用事業公司(KU) 與蘭迪斯齒輪公司簽署了一項為期五年的協議,提供智慧計量和智慧電網基礎設施和技術。該合約包括供應 93 萬個智慧電錶、30 萬個燃氣模組和一個連接的物聯網網路。

- 美國政府對智慧電錶安裝的有利舉措是推動市場成長的主要因素。此外,網路普及率不斷上升,以及高速網路技術和智慧型手機的普及率不斷提高,也推動了市場的發展。透過將智慧型燃氣表與智慧型手機同步,您可以使用智慧型手機應用程式輕鬆遠端監控燃氣表。

住宅領域佔據主要市場佔有率

- 美國對智慧電錶的最大需求是住宅電錶,因為越來越多的消費者使用這些電錶來更準確地監控家庭用電量。大多數的住宅智慧電錶都是由電力公司購買和安裝。

- 在住宅領域,對智慧電錶的需求主要是由於空調、電視、冰箱、照明、吊扇、洗衣機、電腦和暖通空調(暖氣、通風和空調)等家用電器的使用增加而導致的電力消耗增加。 )設備正在被拖走。公用事業公司正在尋找方法來滿足運作這些設備的動態電力需求,因此正在投資智慧電錶以增強電網彈性和營運。

- 智慧電錶還可以幫助將分散式能源(DER)、能源儲存和電動車充電設備整合到住宅領域。

- 此外,政府不斷努力促進家庭採用智慧電錶,以提高抄表的準確性,並為消費者和公用事業公司提供更好的能源消耗透明度,這正在推動市場成長。

- 根據美國能源局統計,全國已安裝超過1億個先進智慧電錶,其中住宅安裝量佔所有安裝量的88%。隨著使用最新技術不斷提高電網效率,預計消費者將有越來越多的機會有效管理電力消耗,並透過安裝智慧電錶實現長期顯著節省。

美國智慧電錶產業概況

美國智慧電錶市場競爭適度,參與者眾多。這些公司利用策略協作行動來增加市場佔有率並提高盈利。

- 2021 年 9 月 - 卡姆魯普宣布推出新型智慧電錶 OMNIA,以加強其在先進計量市場的產品。這款新產品基於蜂巢式物聯網。隨著能源公司和技術供應商尋求開發彈性網路以實現快速、安全的資料遠端檢測,蜂巢式物聯網是通訊標準,在公共產業行業中不斷被廣泛採用。

- 2022 年 5 月 - Neptune Technology Group 選擇美國企業收費和收益解決方案供應商BillingPlatform 來開發Neptune 的智慧水解決方案(例如智慧電錶),推出專為計量工具、網路、軟體和服務設計的基於訂閱的收費。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- 產業價值鏈分析

- COVID-19 爆發對產業的影響

第5章美國智慧電錶市場:產業政策及政策監管

第6章美國智慧電錶與智慧電網計劃

第7章市場動態

- 市場促進因素

- 消費者意識不斷增強,政府法規要求安裝智慧電錶

- 加大智慧電網計劃投資

- 加大智慧城市建設投入

- 市場挑戰

- 與安裝智慧電錶相關的成本增加、安全問題和整合困難

- AMI與客戶資訊系統、配電管理系統、收費系統等整合

第8章市場區隔

- 按類型

- 智慧燃氣表

- 智慧水錶

- 智慧電錶

- 按最終用戶

- 商業的

- 產業

- 住宅

第9章智慧電錶軟體系統研究

第10章競爭格局

- 公司簡介

- Badger Meter Inc.

- Mueller Systems LLC

- Diehl Metering US

- Kamstrup

- Neptune Technology Group Inc.

- General Electric Co.

- Itron Inc.

- Sensus USA Inc.(Xylem Inc.)

- Elster American Meter(Honeywell International Inc.)

第11章供應商市場佔有率分析

第12章投資分析

第13章 市場未來前景

簡介目錄

Product Code: 91304

The United States Smart Meter Market is expected to register a CAGR of 9.8% during the forecast period.

Key Highlights

- As utilities seek more efficient, reliable, and secure ways to manage energy generation, transmission, and distribution, the smart grid has emerged as an effective approach to aligning the supply of energy in a given market with demand while reducing waste. The smart meter is one of the most important devices used in the smart grid and has two-way communication capability between electric utilities and customers. In recent years, increasing investments in smart grid projects along with different government policies, particularly mandates and fiscal incentives, are among the key drivers of market adoption of smart meters in the United States.

- For instance, in September 2021, the U.S. Department of Agriculture announced that it would invest USD 464 million to build or improve renewable energy infrastructure and help rural communities, agricultural producers, and businesses lower energy costs in 48 states and Puerto Rico. The USDA financed USD 335 million of these investments through the Electric Loan Program, including USD 102 million for investments in smart grid technology.

- Further, consumer demand for smart and green services continues to grow and they are now seeking personalized services that enable them to optimize usage and reduce bills. Through smart meter data, utilities are able to help customers reduce energy costs, which is another factor driving the growth of the market.

- At the start of the Covid-19, the primary impact faced by many smart meter manufacturers was supply problems, owing to halted production. Moreover, owing to lockdown measures, demand for residential, commercial, and industrial use of smart meters also decreased. However, with the ease of the pandemic-related lockdowns, manufacturing and supply of smart meters are returning to normal levels, with many manufacturers starting to witness a recovery in sales.

- However, the initial investment involved in setting up smart meter infrastructure is usually much higher as compared to traditional meters, and it also takes a longer time to achieve high returns on investments. The requirement for huge capital poses a significant challenge to both energy consumers and utility providers, which acts as a market restraint.

US Smart Meter Market Trends

Smart Gas Meter Segment to Grow Significantly

- A smart gas meter utilizes ultrasonic or electromagnetic technologies to measure gas flow, while using wireless communication to connect to local or wide area networks, which allows infrastructure maintenance, remote location monitoring, and automatic billing.

- The device also has leakage and shock detection systems that can significantly increase safety by detecting emergency situations and enabling the immediate and remote cutting of the gas flow in case of seismic activity or gas leakage. A smart gas meter relies on low-voltage battery power to extend operational life and avoid ignition hazards.

- Smart gas metering allows gas companies to efficiently manage their operations, including energy production, distribution, and deliveries, while reducing costs and optimizing resource allocation. They can remotely monitor customers' consumption and switch gas on and off to avoid costly onsite visits.

- In August 2021, US utility companies Louisville Gas and Electric Company (LG&E) and Kentucky Utilities Company (KU) signed a five-year contract with Landis+Gyr for the provision of smart meters and smart grid infrastructure and technologies. The agreement includes the supply of 930,000 smart electricity meters, 300,000 gas modules and an IoT network for connectivity.

- Favorable government initiatives towards the installation of smart meters in the US are the primary factors driving the market growth. Further, rising internet penetration along with increased adoption of high-speed network technologies and smartphones are also propelling the market, as the synching of smart gas meters with smartphones can easily be used to perform remote monitoring of the gas meters with smartphone apps.

Residential Sector to Hold a Major Market Share

- The most demand for smart meters in the United States is for residential meters, as more consumers are using these meters to monitor electricity usage at their homes more accurately. The bulk of residential smart meters is procured and installed by utilities.

- In the residential sector, the demand for smart meters is primarily driven by the rising power consumption due to increased use of home appliances like air conditioners, televisions, refrigerators, lighting, ceiling fans, cloth washers, personal computers, and HVAC (Heating, ventilation, and air conditioning) equipment in residential buildings. Utilities are looking for ways to address the dynamic demand for power from the operations of this equipment and are thus investing in smart meters to enhance grid resiliency and operations.

- Smart meters also help in integrating distributed energy resources (DERs), energy storage technologies, and EV charging facilities in the residential sector.

- Further, the increasing government initiatives to boost the adoption of smart meters in households to reinforce accurate meter readings and provide better transparency in energy consumption for both consumers and utility companies are also propelling the market growth.

- As per the United States Department of Energy, over 100 million advanced smart electric meters have already been installed throughout the country, with residential installations representing 88% of the total. With continued efforts to use modern technology to improve the effectiveness of the electric grid, consumers are expected to have more opportunities to manage electricity consumption efficiently and reap significant savings in the long run through the installation of smart meters.

US Smart Meter Industry Overview

The United States smart meter market is moderately competitive and consists of some influential players. These businesses are leveraging strategic collaborative actions to improve their market percentage and enhance their profitability.

- September 2021 - Kamstrup introduced a new smart electricity meter, OMNIA, to enhance its offering within the advanced metering market. The new product is based on cellular IoT, a communications standard that continues to see widespread adoption within the utility industry, as energy companies and technology vendors seek to develop a resilient network for fast and secure data telemetry.

- May 2022 - Neptune Technology Group selected US-based enterprise billing and monetization solution provider, BillingPlatform, for its subscription-based billing capabilities to be used with Neptune's Smart Water solutions, which include measurement tools like smart meters, networks, software, and services designed for the critical work of water.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness-Porter's Five Force Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Outbreak on the Industry

5 UNITED STATES SMART METERS MARKET - INDUSTRY POLICIES AND REGULATIONS

6 UNITED STATES SMART METERS AND SMART GRID INITIATIVES

7 MARKET DYNAMICS

- 7.1 Market Drivers

- 7.1.1 Higher Consumer Awareness and Government Regulations Mandating the Installation of Smart Meters

- 7.1.2 Increased Investments in Smart Grid Projects

- 7.1.3 Investments in Smart City Developments

- 7.2 Market Challenges

- 7.2.1 Higher Costs, Security Concerns and Integration Difficulties with the Installation of Smart Meters

- 7.3 AMI integration with customer information system, distribution management system, billing systems, etc.

8 MARKET SEGMENTATION

- 8.1 By Type

- 8.1.1 Smart Gas Meters

- 8.1.2 Smart Water Meters

- 8.1.3 Smart Electricity Meters

- 8.2 By End-User

- 8.2.1 Commercial

- 8.2.2 Industrial

- 8.2.3 Residential

9 STUDY ON SMART METERS SOFTWARE SYSTEM

10 COMPETITIVE LANDSCAPE

- 10.1 Company Profiles

- 10.1.1 Badger Meter Inc.

- 10.1.2 Mueller Systems LLC

- 10.1.3 Diehl Metering US

- 10.1.4 Kamstrup

- 10.1.5 Neptune Technology Group Inc.

- 10.1.6 General Electric Co.

- 10.1.7 Itron Inc.

- 10.1.8 Sensus USA Inc. (Xylem Inc.)

- 10.1.9 Elster American Meter (Honeywell International Inc.)

11 VENDOR MARKET SHARE ANALYSIS

12 INVESTMENT ANALYSIS

13 FUTURE OUTLOOK OF THE MARKET

02-2729-4219

+886-2-2729-4219

2025 年至 2033 年智慧電錶市場規模、佔有率、趨勢及預測(依產品、技術、最終用途及地區)

2025 年至 2033 年智慧電錶市場規模、佔有率、趨勢及預測(依產品、技術、最終用途及地區) 歐洲智慧電錶市場 - 第19版

歐洲智慧電錶市場 - 第19版 全球智慧電錶市場(至 2030 年)按類型(電力/天然氣/水)、組件(硬體/軟體)、技術(AMI/AMR)、通訊技術(RF/PLC/蜂窩)、最終用戶(住宅/商業/工業)和地區分類

全球智慧電錶市場(至 2030 年)按類型(電力/天然氣/水)、組件(硬體/軟體)、技術(AMI/AMR)、通訊技術(RF/PLC/蜂窩)、最終用戶(住宅/商業/工業)和地區分類 智慧型燃氣計量系統市場規模、佔有率和成長分析(按技術、類型、組件和地區)- 2025-2032 年產業預測

智慧型燃氣計量系統市場規模、佔有率和成長分析(按技術、類型、組件和地區)- 2025-2032 年產業預測 中東和非洲智慧計量:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

中東和非洲智慧計量:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 亞太地區智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區智慧電錶:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲智慧電錶 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

歐洲智慧電錶 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 2025-2033 年日本智慧電錶市場報告(按產品、技術、最終用途和地區)

2025-2033 年日本智慧電錶市場報告(按產品、技術、最終用途和地區) 全球智慧電錶市場:按產品、組件、技術、通訊技術、應用分類 - 預測 2025-2030 年

全球智慧電錶市場:按產品、組件、技術、通訊技術、應用分類 - 預測 2025-2030 年 全球智慧電錶市場機會與策略(至2033年)

全球智慧電錶市場機會與策略(至2033年)

▼