|

市場調查報告書

商品編碼

1637740

超級資料中心:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Mega Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

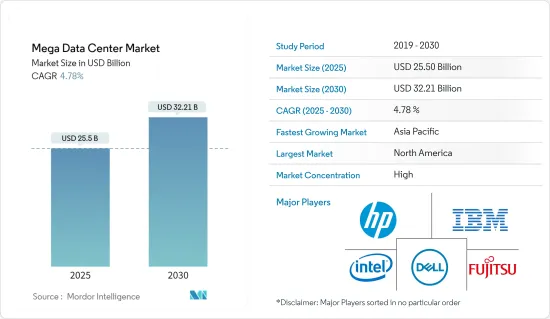

超級資料中心市場在 2025 年的價值預估將達到 255 億美元,預計到 2030 年將達到 322.1 億美元,預測期內(2025-2030 年)的複合年成長率為 4.78%。

主要亮點

- 多年來,資料中心產業一直受到虛擬的推動。公司一直在嘗試透過將 IT 操作集中在數量更少、利用率更高的機器上來減少基礎設施。這個過程拓寬了我們對資料中心的整體視野。經營多個資料中心的公司可能會選擇將其設施集中為更少、更大的實施,以降低複雜性和成本。

- 根據位置不同,擁有較少的超級資料中心可以讓公司利用某些當地優勢,例如稅收優惠、低能源價格、氣候或替代能源的可用性。因此,超級資料中心的出現是為了盡量降低成本並實現利潤最大化。

- 選擇軟體主導、行業相關、設置良好的大型資料中心的好處是,與今天相比,IT 管理成本資料,速度和頻寬與本地資料中心相當。這種能力可能會刺激全球的 IT 支出。早期採用者將有更多機會投資新IT技術,以降低整體業務成本並增加收益。

- 雲端和主機託管服務的成長以及相關的成本效益和規模經濟的提高正在推動超級資料中心市場的發展。微軟、Google、亞馬遜網路服務 (AWS) 和 Facebook 的資料中心都自成一派。他們正在建立一個全自動、自我修復、聯網的巨量資料超級資料中心正常運作。

- 然而,高昂的初始投資和低資源可用性對這個市場構成了挑戰。儘管面臨這些挑戰,但許多組織已經部署或正在部署超級資料中心。

超級資料中心市場趨勢

銀行和金融部門對資料中心的需求不斷增加

- 銀行和金融業是最大的資料產生器之一,而資料中心控制營運成本的需求是主要促進因素。金融和銀行機構使用資料中心來儲存客戶記錄、員工管理、交易、遠端銀行、電話銀行、自助查詢和其他電子銀行服務,而這些服務的運作都需要資料。

- 資料中心作為基礎設施被視為金融的未來。許多金融機構正在建立私有雲端系統來容納龐大的網路、儲存和伺服器容量,以支援其零售金融中心、ATM 和活躍的線上帳戶。

- 雖然許多銀行都維護自己的資料中心,但隨著銀行收益的波動,我們看到這種趨勢正在改變。此外,維護資料中心需要適當的冷卻、安全和電力設備,從而增加 IT、房地產和營運成本。這可能會在預測期內對 BFSI 產業構成挑戰。

亞太地區不斷成長的需求推動市場

- 中國各地對高密度、冗餘設施的需求不斷成長,推動該國資料中心設計和開發的變革。中國每 100 人擁有 50 名網路用戶,顯示還有很大的發展空間,其連接生態系統由 73 個主機託管資料中心、52 個雲端服務供應商和 0 個網路結構組成。

- 但它凸顯了在中國維護資料中心的困難,電力、空間和 IP 傳輸的成本都非常高。同樣,在印度,數位經濟佔其GDP的9.5%。數位經濟中,固定電話用戶規模255.18億美元,行動電話規模10,110.54億美元,資料中心發展空間龐大。

- 此外,由於監管和安全原因,印度的許多組織,尤其是 BFSI 領域的組織,被禁止在國外的資料中心託管資料。因此,資料中心供應商擴大在印度建立資料中心,標誌著該國超級資料中心設施的增加。

超級資料中心產業概況

超級資料中心市場由於前期投入高、資源供給少等原因,市場集中度較高,為該市場帶來挑戰。市場的主要企業包括Cisco、戴爾軟體、富士通和惠普企業。市場的最新趨勢包括:

2022 年 9 月,微軟在卡達開設了一個新的資料中心區域,成為第一家在該國提供企業級服務的超大規模雲端供應商。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查假設和定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 市場促進因素與限制因素簡介

- 市場促進因素

- 資料中心整合需求不斷成長

- 銀行和金融部門對資料中心的需求不斷增加

- 市場限制

- 投資和安裝成本高

- 技術簡介

第5章 市場區隔

- 按解決方案

- 貯存

- 網路

- 伺服器

- 安全功能

- 其他解決方案

- 按最終用戶

- BFSI

- 通訊和 IT

- 政府

- 媒體與娛樂

- 其他最終用戶

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第6章 競爭格局

- 公司簡介

- Cisco Systems Inc.

- Dell Software Inc.

- Fujitsu Ltd

- Hewlett-Packard Enterprise

- IBM Corporation

- Intel Corporation

- Juniper Networks Inc.

- Verizon Wireless

第7章投資分析

第8章 市場機會與未來趨勢

The Mega Data Center Market size is estimated at USD 25.50 billion in 2025, and is expected to reach USD 32.21 billion by 2030, at a CAGR of 4.78% during the forecast period (2025-2030).

Key Highlights

- Virtualization has driven the data center industry over the years. Companies have sought to reduce infrastructure by focusing IT operations on fewer, more highly utilized machines. This process has led to a wider view of data centers in general. Companies operating multiple data centers can choose to focus their facilities on fewer and larger implementations to decrease complexity and costs.

- Implementing fewer mega data centers, depending on their locations, can allow a company to enjoy advantages of certain local benefits, such as tax incentives, low energy prices, climate, or availability of alternative energy sources. Thus, mega data centers result from attempts to minimize cost and maximize profit.

- The merits of choosing a software-led, industry-relevant, and adequately set-up mega data center are lower costs of IT management compared to the present, as well as the ability to access a vast amount of internet and industrial Internet data at local data center speed and bandwidth. This capability is likely to spur IT spending worldwide, as early adopters will have substantial opportunities to invest in new IT techniques to reduce overall business costs and increase revenues.

- Factors including increasing cloud and colocation services, associated cost benefits, and improved economies of scale drive the market for mega data centers. Microsoft, Google, Amazon Web Services (AWS), and Facebook data centers are in a class by themselves. They have to function fully automatic, self-healing, networked mega data centers that operate at fiber optic speeds to make a fabric that can access any node in any particular data center, as there are multiple pathways to every node.

- However, higher initial investments and low resource availability are some factors presenting challenges to this market. Despite such challenges, various organizations have already adopted or are initiating the adoption of mega data centers.

Mega Data Centers Market Trends

Rising Demand of Data Centers in Banking and Finance Sectors

- The banking and finance sector is one of the largest generators of data, and the need for a data center to regulate the cost of operations is a primary driver. Finance and banking structures use data centers to store customer records, employee management, transactions, and electronic banking services, such as remote banking, telebanking, and self-inquiry, which need data centers to function.

- Data centers, as infrastructure, are believed to be the future of finance. Many institutions have created private cloud systems to accommodate massive network, storage, and server capacities to support their retail financial centers, ATMs, and active online accounts.

- Many banks maintain their own data centers, but it has been observed that the trend is changing due to fluctuations in the banks' profits. Also, maintaining a data center is cumbersome, owing to the cost drain on IT, real estate, and operations, as it requires proper cooling, security, and power facilities. This can act as a challenge for the BFSI industry during the forecast period.

Growing Demand from Asia-Pacific to Drive the Market

- The growing demand for high-density, redundant facilities throughout China is precipitating a shift in the design and development of the country's data centers. China has 50 internet users per 100 population, indicating scope for a lot of development, and the connectivity ecosystem comprises 73 colocation data centers, 52 cloud service providers, and 0 network fabrics.

- However, power, space, and IP transit all cost more in China, emphasizing the difficulties in maintaining a data center. Similarly, in India, the digital economy contributes 9.5% of the GDP. The digital economy includes USD 25,518 million fixed-line telephone subscriptions and 1,011.054 million mobile telephone subscriptions, indicating a lot of scope for the development of data centers.

- Moreover, owing to regulatory and security reasons, a number of organizations in India, especially from the BFSI sector, are not allowed to host their data in a data center that is out of the country. As a result, the data center providers are setting up local data centers in India, indicating the growing mega data center facilities in India.

Mega Data Centers Industry Overview

The mega data center market is highly concentrated due to higher initial investments and low availability of resources, which present challenges to this market. Some of the key players in the market are Cisco Systems Inc., Dell Software Inc., Fujitsu Ltd, and Hewlett-Packard Enterprise. Some recent developments in the market include:

In September 2022, Microsoft launched its new data center region in Qatar, becoming the first hyper-scale cloud provider to offer enterprise-grade services in the nation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Introduction to Market Drivers and Restraints

- 4.4 Market Drivers

- 4.4.1 Increasing Demand for Data Center Consolidation

- 4.4.2 Rising Demand of Data Centers in Banking and Finance Sectors

- 4.5 Market Restraints

- 4.5.1 High Investment and Installation Costs

- 4.6 Technology Snapshot

5 MARKET SEGMENTATION

- 5.1 By Solution

- 5.1.1 Storage

- 5.1.2 Networking

- 5.1.3 Server

- 5.1.4 Security

- 5.1.5 Other Solutions

- 5.2 By End-user

- 5.2.1 BFSI

- 5.2.2 Telecom and IT

- 5.2.3 Government

- 5.2.4 Media and Entertainment

- 5.2.5 Other End-users

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Dell Software Inc.

- 6.1.3 Fujitsu Ltd

- 6.1.4 Hewlett-Packard Enterprise

- 6.1.5 IBM Corporation

- 6.1.6 Intel Corporation

- 6.1.7 Juniper Networks Inc.

- 6.1.8 Verizon Wireless

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球超大規模資料中心市場(至 2030 年):按電力容量(10-50MW、50-100MW、101MW 以上)、 IT基礎設施(伺服器、儲存、網路)、電氣基礎設施(PDU、UPS 系統)和機械基礎設施(冷卻系統、機架)分類

全球超大規模資料中心市場(至 2030 年):按電力容量(10-50MW、50-100MW、101MW 以上)、 IT基礎設施(伺服器、儲存、網路)、電氣基礎設施(PDU、UPS 系統)和機械基礎設施(冷卻系統、機架)分類 全球超大規模資料中心市場:市場規模、市場佔有率、趨勢、產業分析(依組件、部署類型、電力容量、最終用戶和地區)、未來預測(2025-2034年)

全球超大規模資料中心市場:市場規模、市場佔有率、趨勢、產業分析(依組件、部署類型、電力容量、最終用戶和地區)、未來預測(2025-2034年) 2025-2033 年按組件、最終用戶、垂直產業(銀行、金融服務和保險、電信和 IT、媒體和娛樂、政府和公眾等)和地區分類的大型資料中心市場

2025-2033 年按組件、最終用戶、垂直產業(銀行、金融服務和保險、電信和 IT、媒體和娛樂、政府和公眾等)和地區分類的大型資料中心市場 2025 年至 2029 年全球超大規模資料中心市場超大規模資料中心:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)超大規模資料中心市場:按組件、設施規模、最終用戶和行業分類 - 2025-2030 年全球預測超級資料中心市場:按組件、最終用戶、行業分類 - 2025-2030 年全球預測

2025 年至 2029 年全球超大規模資料中心市場超大規模資料中心:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)超大規模資料中心市場:按組件、設施規模、最終用戶和行業分類 - 2025-2030 年全球預測超級資料中心市場:按組件、最終用戶、行業分類 - 2025-2030 年全球預測 超大規模資料中心市場 - 按組件、用戶類型、最終用戶、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測,2019-2029F2024 年超級資料中心世界市場報告

超大規模資料中心市場 - 按組件、用戶類型、最終用戶、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測,2019-2029F2024 年超級資料中心世界市場報告 超大規模資料中心市場 - 全球展望與預測(2023-2028)

超大規模資料中心市場 - 全球展望與預測(2023-2028)