|

市場調查報告書

商品編碼

1642148

超大規模資料中心:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Hyperscale Datacenter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

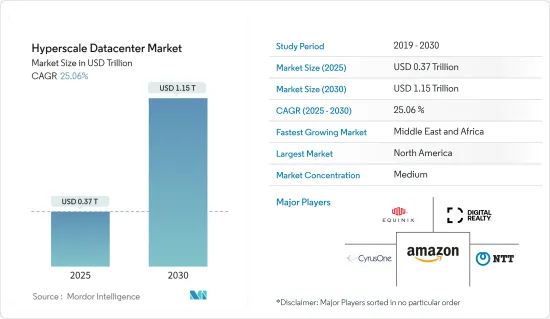

超大規模資料中心市場在 2025 年的價值預估將達到 3,700 億美元,預計到 2030 年將達到 1.15 兆美元,在預測期內(2025-2030 年)的複合年成長率為 25.06%。

近年來,由於滿足高階應用的運算和儲存需求不斷成長,超大規模資料中心變得極其強大。業務關鍵型應用程式的激增增加了資料中心的複雜性。隨著網路、電子商務、社交媒體、巨量資料、運算、線上遊戲託管和 Hadoop 的普及,對提高應用程式速度、能源效率和伺服器密度的基礎設施的需求也日益成長。

主要亮點

- 近年來,資料被認為是新興經濟體的基礎。幾乎每個企業現在使用的資料都比以前多,而且未來可能會消耗資料。這種指數級成長的資料生成需要儲存在某個地方並從某個地方存取。據Cisco稱,全球 IP資料流量從 2016 年的每月 96,054 Petabyte成長到 2018 年的每月 150,910 Petabyte,去年達到每月 278,108 Petabyte。

- 此外,透過網路提供的應用程式和服務對Over-The-Top(OTT) 應用的需求日益成長,正在繞過傳統的分銷方式。 Over-The-Top服務與媒體和通訊領域高度相關,且成本低廉,促進了資料的大規模成長,從而推動了市場發展。

- 此外,作為數位轉型策略的一部分,許多企業迅速採用物聯網、雲端運算、巨量資料和分析技術,也為資料中心帶來了越來越大的壓力,從而促進了全球超大規模資料中心的成長。

- 提供大規模雲端服務、電子商務、先進藥物研究、石油和天然氣、航太、股票交易所等的公司正在投資必要的網路基礎設施。然而,現有的新一代防火牆 (NGFW) 必須滿足超大規模架構的大規模和效能需求,因此尋找能夠滿足這些需求的安全解決方案成為一項挑戰。

- 隨著最近的 COVID-19 疫情,資料中心的需求在超大規模公司和雲端平台之間分化。相較之下,許多商業用戶的支出卻放緩了。疫情導致租賃需求集中在關鍵的雲端市場。疫情過後,隨著數位化應用的增加以及企業轉向混合和遠端工作模式,市場實現了蓬勃發展。

超大規模資料中心市場趨勢

對雲端運算和其他高效能技術的需求不斷成長,推動著市場

- 由於科技的應用和消費者對雲端的偏好日益成長,對雲端基礎的解決方案的需求正在激增。這項技術允許用戶從遠端位置存取資料。企業越來越意識到將資料遷移到雲端而不是建置和維護內部基礎設施對於節省成本和資源的重要性,這推動了對雲端基礎的解決方案的需求。

- 這些優勢使得大大小小的企業擴大採用雲端基礎的解決方案。未來幾年,雲端運算和虛擬可能會透過分解軟體來降低設定成本,最終減少硬體使用。

- 世界各地的企業和政府機構正在將其測試環境和更多業務關鍵型工作負載和運算實例遷移到雲端。同樣,對於消費者而言,雲端服務可以透過多種裝置隨時隨地輕鬆存取內容和服務。

- 預計整個印尼對資料儲存和託管服務的需求將大幅增加。雅加達的兩個資料中心將滿足客戶的需求,特別是雲端服務供應商和金融業,他們需要靈活的設施設計來幫助他們實現業務目標。領先的IT基礎設施和服務公司之一 NTT Corporation 今年 4 月擴大了其超大規模資料中心的足跡,在印尼推出了其最大的資料中心(雅加達 3資料中心),以支援東南亞日益成長的數位經濟。

- 企業使用雲端運算最常見的方式之一是透過許多全球領先的科技公司提供的許多「即服務」替代方案。這些服務使企業無需內部基礎設施即可獲得運算能力、軟體和其他與雲端相關的業務。據 Flexera Software 稱,截至今年 3 月,46% 的受訪者已經在 Amazon Web Services 上運行大量工作負載。

預計德國將佔據較大市場佔有率

- 全球疫情導致電子交易、系統和數位資訊激增,導致歐洲數位流量大幅增加。新興企業的迅速崛起和人口的成長正在推動對超大規模資料中心的需求。

- 過去幾年,受超大規模資料中心發展和GDPR實施的推動,德國資料中心市場取得了顯著成長,刺激了德國的投資和區域雲端網路的發展。

- 雲端運算的使用和投資不斷增加,正在鼓勵德國許多參與者改善其雲端基礎設施,從而推動市場成長。例如,2021年8月,Google宣布將在2030年前投資10億歐元,用於增加可再生能源的使用並在德國發展雲端運算基礎設施。

- 今年 6 月,Vantage資料中心宣佈在柏林和華沙啟動兩個待開發區園區。新地點是 Vantage 斥資 20 億美元在歐洲擴張計劃的一部分,旨在為兩個熱門市場的超大規模資料中心業者和雲端供應商提供資料中心園區。

- 今年 2 月,美國和歐洲超大規模資料中心開發商和營運商 Cloud HQ 宣布將在德國法蘭克福東南部的奧芬巴赫建造一個 112 兆瓦、120 萬平方英尺(108,000平方公尺)的超大規模資料中心園區。 CloudHQ 法蘭克福資料中心園區總投資 11 億歐元(11.5 億美元),建成後將成為德國最大的超大規模資料中心之一。

超大規模資料中心產業概覽

超大規模資料中心市場相當分散,既有全球參與者,也有規模較小的參與者。此外,超大規模資料中心正在被各行各業所應用,為供應商提供了成長機會。市場參與者正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

- 研究框架

- 二次調查

- 初步調查

- 資料三角測量與洞察生成

第3章執行摘要

第4章 市場洞察

- 市場概況

- 市場動態

- 市場促進因素

- 對雲端運算和其他高效能技術的需求不斷增加

- 生成式人工智慧能力的崛起推動對超大規模設施的需求

- 市場限制

- 資料中心安全問題

- 能源消耗過多和容量規劃不高效

- 市場促進因素

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場區隔

- 依資料中心類型

- 企業/超大規模自建

- 超大規模主機託管

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 德國

- 荷蘭

- 法國

- 愛爾蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 新加坡

- 日本

- 澳洲

- 印尼

- 其他亞太地區

- 中東和非洲

- 南美洲

- 北美洲

第6章 競爭格局

- 公司簡介

- Digital Realty Trust, Inc.

- Equinix, Inc.

- CyrusOne, Inc.

- NTT Ltd

- Quality Technology Services

- Vantage Data Centers, LLC

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alphabet Inc.

- Meta Platforms Inc.

第7章投資分析

第8章 市場機會與未來趨勢

第 9 章:關於發布者

The Hyperscale Datacenter Market size is estimated at USD 0.37 trillion in 2025, and is expected to reach USD 1.15 trillion by 2030, at a CAGR of 25.06% during the forecast period (2025-2030).

Hyperscale data centers have become highly powerful in recent years due to the increased computing and storage requirements to serve high-end applications. Business-critical apps are increasing, resulting in greater data center complexity. With the rising popularity of the web, e-commerce, social media, big data, computing, online gaming hosting, and Hadoop, the infrastructure needs to improve application speed, energy efficiency, and server density are increasing.

Key Highlights

- In the recent past, data was considered the foundation of an emerging economy. Almost all enterprises use more data than before and will probably consume even more data in the future. This rapidly increasing data generation must be stored and accessed from somewhere. According to Cisco Systems, the global IP data traffic increased from 96,054 petabytes per month in 2016 to 150,910 petabytes per month in 2018, and it reached 278,108 petabytes per month last year.

- Moreover, the rising demand for over-the-top (OTT) applications through an app or service that can be availed over the internet bypass traditional distribution practices. Services available for over-the-top services are significantly related to the media and communication sector, which can be accessed at a lower cost and contributes to massive data growth, thereby driving the market.

- Furthermore, owing to the rapidly increasing adoption of IoT, cloud, and Big Data, analytics across multiple enterprises as a part of their digital transformation strategy, the burden on the data centers is also increasing, leading to growth in the hyperscale data centers globally.

- Enterprises that offer large cloud services, e-commerce, advanced research of pharmaceuticals, oil and gas, aerospace, stock exchange, and others have invested in the network infrastructure they require. However, sourcing security solutions to meet these needs presents a challenge since existing next-generation firewalls (NGFWs) still need to meet the massive scale and performance needs of hyperscale architectures.

- With the recent outbreak of COVID-19 worldwide, the demand for the data center is bifurcated with strong buying by hyperscale companies and cloud platforms. In contrast, there was a slowdown in spending by many enterprise users. Pandemic-driven leasing activity was concentrated in significant cloud markets. After the pandemic, the market is growing rapidly with the increased adoption of digitization and enterprises moving toward hybrid and remote working models.

Hyperscale Data Center Market Trends

Growing Demand for Cloud Computing and Other Hight Performance Technologies Driving the Market

- The demand for cloud-based solutions is surging, owing to the growing application of technology and consumer propensity towards the cloud. This technology allows the user to access the data from remote locations. The increasing realization among companies about the importance of saving money and resources by moving their data to the cloud rather than building and maintaining on-premise infrastructure is driving the demand for cloud-based solutions.

- Owing to these benefits, large enterprises and SMEs are increasingly adopting cloud-based solutions. Over the next few years, cloud computing and virtualization will be able to save the setup cost of software by dividing it, ultimately leading to decreasing the use of hardware.

- Enterprises and government organizations worldwide are moving from test environments to placing more work-critical workloads and compute instances into the cloud. Similarly, for consumers, cloud services offer anywhere and easy access to content and services on multiple devices.

- The demand for data storage and managed hosting services is expected to increase dramatically across Indonesia. Jakarta's two Data Centers will accommodate clients' needs, particularly cloud service providers and the financial industry, which require flexible facility designs to help them achieve their business objectives. In April this year, NTT Ltd, one of the leading IT infrastructure and services companies, expanded its hyperscale data center footprint by launching the largest data center in Indonesia (Jakarta's third data center) to support the growing digital economy in Southeast Asia.

- One of the most common methods for businesses to use cloud computing is to use the numerous "as-a-service" alternatives provided by many major global technology corporations. These services give businesses access to computing power, software, and other cloud-related operations without the need for on-premises infrastructure. According to Flexera Software, as of March this year, 46% of respondents are already running significant workloads on Amazon Web Services.

Germany is Expected to Hold Major Market Share

- European digital traffic increased tremendously due to the surge in electronic transactions, systems, and digital information during the global pandemic. When paired with the rapid rise of new firms and the ever-increasing population, this boosts demand for hyperscale data centers.

- Over the past few years, the German data center market has grown notably with the rise in the development of hyperscale data centers, and owing to the implementation of GDPR, which has been driving investments and the regional cloud network development in Germany.

- The growing usage of the cloud and investments encourage many players in the country to improve cloud infrastructure in Germany, which drives the market's growth. For instance, in August 2021, Google announced it would invest EUR 1 billion by 2030 to enhance renewable energy use and develop its cloud computing infrastructure in Germany.

- In June this year, Vantage data centers announced the start of operations at two greenfield campuses in Berlin and Warsaw. The new sites are part of Vantage's USD 2 billion European expansion to offer hyperscalers and cloud providers with data center campuses in two sought-after markets.

- Moreover, in February this year, A 112-megawatt, 1.2 million sqft (108k sqm), hyper-scale data center campus is being built by Cloud HQ, a hyper-scale data center developer and operator in the US and Europe, in Offenbach, Germany, a city that borders Frankfurt to the southeast. With a total investment of EUR 1.1 billion (USD 1.15 billion), CloudHQ's Frankfurt data center campus will be one of Germany's biggest hyperscale data centers once fully constructed.

Hyperscale Data Center Industry Overview

The hyperscale data center market is moderately fragmented, with the presence of both global players and small and medium-sized enterprises. Moreover, hyperscale data centers are used in various industries to provide vendors with growth opportunities. Players in the market are adopting strategies, such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Growing Demand for Cloud Computing and Other High-Performance Technologies

- 4.2.1.2 Rising Generative AI capabilities driving the demand for hyperscale facilities

- 4.2.2 Market Restraints

- 4.2.2.1 Data Center Security Challenges

- 4.2.2.2 Excessive Energy Consumption and Inefficient Capacity Planning

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Data Center Type

- 5.1.1 Enterprises/ Hyperscale Self-builds

- 5.1.2 Hyperscale Colocation

- 5.2 By Region

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 Netherlands

- 5.2.2.4 France

- 5.2.2.5 Ireland

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Singapore

- 5.2.3.4 Japan

- 5.2.3.5 Australia

- 5.2.3.6 Indonesia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.5 South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Digital Realty Trust, Inc.

- 6.1.2 Equinix, Inc.

- 6.1.3 CyrusOne, Inc.

- 6.1.4 NTT Ltd

- 6.1.5 Quality Technology Services

- 6.1.6 Vantage Data Centers, LLC

- 6.1.7 Amazon Web Services, Inc.

- 6.1.8 Microsoft Corporation

- 6.1.9 Alphabet Inc.

- 6.1.10 Meta Platforms Inc.

7 INVESTMENTS ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 ABOUT US

全球超大規模資料中心市場(至 2030 年):按電力容量(10-50MW、50-100MW、101MW 以上)、 IT基礎設施(伺服器、儲存、網路)、電氣基礎設施(PDU、UPS 系統)和機械基礎設施(冷卻系統、機架)分類

全球超大規模資料中心市場(至 2030 年):按電力容量(10-50MW、50-100MW、101MW 以上)、 IT基礎設施(伺服器、儲存、網路)、電氣基礎設施(PDU、UPS 系統)和機械基礎設施(冷卻系統、機架)分類 全球超大規模資料中心市場:市場規模、市場佔有率、趨勢、產業分析(依組件、部署類型、電力容量、最終用戶和地區)、未來預測(2025-2034年)

全球超大規模資料中心市場:市場規模、市場佔有率、趨勢、產業分析(依組件、部署類型、電力容量、最終用戶和地區)、未來預測(2025-2034年) 2025-2033 年按組件、最終用戶、垂直產業(銀行、金融服務和保險、電信和 IT、媒體和娛樂、政府和公眾等)和地區分類的大型資料中心市場

2025-2033 年按組件、最終用戶、垂直產業(銀行、金融服務和保險、電信和 IT、媒體和娛樂、政府和公眾等)和地區分類的大型資料中心市場 2025 年至 2029 年全球超大規模資料中心市場超級資料中心:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)超大規模資料中心市場:按組件、設施規模、最終用戶和行業分類 - 2025-2030 年全球預測超級資料中心市場:按組件、最終用戶、行業分類 - 2025-2030 年全球預測

2025 年至 2029 年全球超大規模資料中心市場超級資料中心:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)超大規模資料中心市場:按組件、設施規模、最終用戶和行業分類 - 2025-2030 年全球預測超級資料中心市場:按組件、最終用戶、行業分類 - 2025-2030 年全球預測 超大規模資料中心市場 - 按組件、用戶類型、最終用戶、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測,2019-2029F2024 年超級資料中心世界市場報告

超大規模資料中心市場 - 按組件、用戶類型、最終用戶、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測,2019-2029F2024 年超級資料中心世界市場報告 超大規模資料中心市場 - 全球展望與預測(2023-2028)

超大規模資料中心市場 - 全球展望與預測(2023-2028)