|

市場調查報告書

商品編碼

1640318

南美聚氯乙烯(PVC) -市場佔有率分析、產業趨勢、成長預測(2025-2030 年)South America Polyvinyl Chloride (PVC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

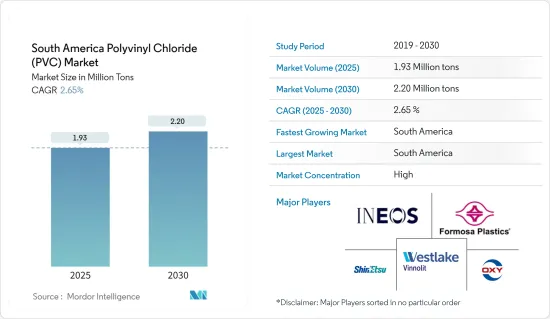

南美聚氯乙烯市場規模預計2025年為193萬噸,預計到2030年將達到220萬噸,預測期內(2025-2030年)複合年成長率為2.65%。

PVC 強度高、重量輕、耐候、耐腐蝕、耐化學腐蝕、耐磨、用途廣泛且易於使用,因為它可以以任何方式切割、成型、焊接和連接。

主要亮點

- 市場研究的主要驅動力是擴大使用塑膠來使汽車更輕、更省油、建築行業需求的增加以及醫療行業應用的增加。

- 然而,對人類健康和環境的有害影響預計將成為市場成長的主要障礙。

- 加速電動車的使用和回收PVC可能是未來的機會。

南美洲聚氯乙烯(PVC)市場趨勢

建築業的需求不斷增加

- PVC 管道已在建築領域使用了 60 多年,因為它們在生產過程中提供了寶貴的節能效果、低成本的配送以及安全、免維護的使用壽命。這些管道廣泛用於水、廢棄物和廢水管道系統,因為它們不會堆積、結垢、腐蝕和點蝕,並且其光滑的表面減少了泵送所需的能量。

- 2022 年第二季度,該地區的酒店建設項目數量為 555 個計劃和 90,496 間客房。經過近兩年因疫情帶來的不確定性後,拉丁美洲酒店業終於出現復甦跡象。隨著全部區域邊境監管和檢疫要求的放鬆,消費者信心增強。

- 在南美洲,2022 年上半年動工了 40 個計劃,總合8,481 間客房。 2022年第二季新計畫共36個計劃、6,208間客房,較去年同期成長57%。

- 2022年12月,巴西聚氯乙烯(PVC)市場等待政府宣布基礎設施和建築領域的新措施,將改善供應鏈和商業環境。

- 2021 年,巴西基礎建設投資達 1,480 億巴西幣(274.5 億美元)。

- 所有上述因素預計將在預測期內推動市場成長。

巴西主導市場

- 在南美洲,巴西在市場上佔據主導地位,並且在預測期內可能會繼續保持這一地位。該國的建築、汽車和電子產業正在崛起。

- 巴西政府推出“基礎設施特許經營計劃”,投資該國道路、機場、港口、能源等基礎設施。根據該計劃,政府宣布對交通、能源和衛生計劃投資 144 億美元。

- 此外,政府計劃平衡經濟適用住宅的供需(由人口成長和快速都市化創造),並利用官民合作關係(PPP)模式來取代老化的交通基礎設施。

- 根據新聞部落格「南美洲門戶」報道,2022年1月至5月,巴西建築業景氣指數(ICEI)有所改善,從4月的55.5和3月的55.3上升至5月的56.2。

- 巴西對汽車的需求量大,被認為是世界十大乘用車製造國之一。根據國際汽車製造工業(OICA) 的數據,2022 年巴西乘用車銷量為 1,824,833 輛。

- 家用電子電器產品的銷售似乎已經飽和狀態。消費者在購買昂貴產品時會持謹慎態度,並且這種行為預計將持續下去。

- 所有這些因素預計將在預測期內推動巴西 PVC 市場的成長。

南美洲聚氯乙烯(PVC)產業概況

南美聚氯乙烯市場具有一體化特徵。頂尖公司專注於為各個最終用戶產業提供更好的材料。南美洲聚氯乙烯的主要生產商包括台塑公司、英力士公司、信越化學公司、西方石油公司和Westlake Vinnolit GmbH &Co.KG。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 增加塑膠的使用使汽車更輕並提高燃油效率

- 擴大在醫療產業的應用

- 建築業的成長

- 抑制因素

- 對人類和環境的有害影響

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模(基於數量))

- 產品類型

- 硬質聚氯乙烯

- 透明硬質PVC

- 不透明硬質PVC

- 軟聚氯乙烯

- 透明軟質PVC

- 不透明軟PVC

- 低煙PVC

- 氯化聚氯乙烯

- 硬質聚氯乙烯

- 穩定劑類型

- 鈣穩定劑(鈣鋅穩定劑)

- 鉛基穩定劑(Pb穩定劑)

- 錫和有機錫穩定劑(Sn穩定劑)

- 鋇基及其他(液態混合金屬)

- 目的

- 管道和配件

- 薄膜片材

- 電線電纜

- 瓶子

- 型材、軟管、管材

- 其他

- 最終用戶產業

- 建築/施工

- 車

- 電力/電子

- 包裝

- 鞋類

- 醫療保健

- 其他

- 地區

- 巴西

- 阿根廷

- 南美洲其他地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)分析**/市場排名分析

- 主要企業策略

- 公司簡介

- Braskem

- Formosa Plastics Corporation

- INEOS

- Occidental Petroleum Corporation

- Orbia

- Shin-Etsu Chemical Co., Ltd.

- Westlake Vinnolit GmbH & Co. KG

- Xinjiang Zhongtai Chemical Co., Ltd.

第7章 市場機會及未來趨勢

- 轉向 PVC 回收

- 加速電動車 (EV) 的普及

The South America Polyvinyl Chloride Market size is estimated at 1.93 million tons in 2025, and is expected to reach 2.20 million tons by 2030, at a CAGR of 2.65% during the forecast period (2025-2030).

PVC is strong and lightweight, durable to weathering, rotting, chemical corrosion and abrasion, versatile, and easy to use, as it can be cut, shaped, welded, and joined in any style.

Key Highlights

- Major factors driving the market studied are the increasing use of plastics to reduce vehicle weight and enhance fuel economy, growing demand from the construction industry, and increasing applications in the healthcare industry

- However, hazardous impacts on humans and the environment are expected to majorly hinder the growth of the market studied.

- The accelerating usage of electric vehicles and PVC recycling are likely to act as an opportunity in the future.

South America Polyvinyl Chloride (PVC) Market Trends

Growing Demand from the Construction Industry

- PVC pipes have been used in building and construction for over 60 years, as they offer valuable energy savings during production, low-cost distribution, and a safe, maintenance-free lifetime of service. These pipes are widely used for pipeline systems for water, waste, and drainage as they suffer no build-up, scaling, corrosion, or pitting, and they provide smooth surfaces reducing energy requirements for pumping.

- In Q2 2022, the region's total hospitality construction pipeline includes 555 projects and 90,496 rooms. Following nearly two years of uncertainty caused by the pandemic, the Latin American hotel industry is finally showing signs of recovery. Consumer confidence has risen as border restrictions and quarantine requirements across the region have been relaxed.

- In South America, 40 projects totaling 8,481 rooms began construction in the first half of 2022. In Q2 2022, new project announcements increased 57% year-on-year to 36 projects or 6,208 rooms.

- In December 2022, Brazil's polyvinyl chloride (PVC) market was awaiting new policies to be announced by the government in the infrastructure and construction sectors, which will improve the supply chain and business conditions.

- Brazil's infrastructure investment amounted to 148 billion Brazilian reals (USD 27.45 billion) in 2021.

- All the above-mentioned factors are likely to drive the market growth during the forecast period.

Brazil to Dominate the Market

- Brazil dominated the market in South America and is likely to continue its dominance during the forecast period. The country is attributed to the rise in construction, automotive, and electronics industries.

- The government of Brazil launched the 'Infrastructure Concessions Program' to invest in infrastructure for roads, airports, ports, and energy, in the country. In this program, the government announced an investment of USD 14.4 billion in transport, energy, and sanitation projects.

- Additionally, the government plans to balance the demand for and supply of affordable housing (created by the increasing population and rapid urbanization) and its efforts to improve the country's aging transport infrastructure using the public-private partnership (PPP) model.

- According to a News Blog, Gateway to South America, Brazil's business confidence indicator (ICEI) in the construction industry improved in the first five months of 2022, rising to 56.2 in May 2022 from 55.5 in April and 55.3 in March 2022.

- Brazil has a high demand for vehicles and is considered among the ten leading passenger vehicle manufacturers across the world. According to the International Organization of Motor Vehicle Manufacturers (French: Organisation Internationale des Constructeurs d'Automobiles (OICA)), Brazil's passenger cars sale was 18,24,833 in 2022.

- Sales of consumer electronics appear to have reached a point of saturation in the country. Consumers are careful while buying expensive products, and this behavior is expected to continue in the upcoming years.

- All such factors are likely to drive the PVC market growth in Brazil over the forecast period.

South America Polyvinyl Chloride (PVC) Industry Overview

South America's polyvinyl chloride market is consolidated in nature. The top companies have been focusing on providing better materials for various end-user industries. Major manufacturers of South American PVCs are Formosa Plastics Corporation, INEOS, Shin-Etsu Chemical Co., Ltd., Occidental Petroleum Corporation, and Westlake Vinnolit GmbH & Co. KG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Plastics to Reduce Vehicle Weight and Enhance Fuel Economy

- 4.1.2 Increasing Application in the Healthcare Industry

- 4.1.3 Growth from the Construction Industry

- 4.2 Restraints

- 4.2.1 Hazardous Impact on Humans and the Environment

- 4.2.2 Other Restrainta

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Rigid PVC

- 5.1.1.1 Clear Rigid PVC

- 5.1.1.2 Non-Clear Rigid PVC

- 5.1.2 Flexible PVC

- 5.1.2.1 Clear Flexible PVC

- 5.1.2.2 Non-Clear Flexible PVC

- 5.1.3 Low-smoke PVC

- 5.1.4 Chlorinated PVC

- 5.1.1 Rigid PVC

- 5.2 Stabilizer Type

- 5.2.1 Calcium-based Stabilizers (Ca-Zn Stabilizers)

- 5.2.2 Lead-based Stabilizers (Pb Stabilizers)

- 5.2.3 Tin- and Organotin-based Stabilizers (Sn Stabilizers)

- 5.2.4 Barium-based and Others (Liquid Mixed Metals)

- 5.3 Application

- 5.3.1 Pipes and Fittings

- 5.3.2 Films and Sheets

- 5.3.3 Wires and Cables

- 5.3.4 Bottles

- 5.3.5 Profiles, Hoses and Tubings

- 5.3.6 Other Applications

- 5.4 End-User Industry

- 5.4.1 Building and Construction

- 5.4.2 Automotive

- 5.4.3 Electrical and Electronics

- 5.4.4 Packaging

- 5.4.5 Footwear

- 5.4.6 Healthcare

- 5.4.7 Other End-User Industries

- 5.5 Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/ Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Braskem

- 6.4.2 Formosa Plastics Corporation

- 6.4.3 INEOS

- 6.4.4 Occidental Petroleum Corporation

- 6.4.5 Orbia

- 6.4.6 Shin-Etsu Chemical Co., Ltd.

- 6.4.7 Westlake Vinnolit GmbH & Co. KG

- 6.4.8 Xinjiang Zhongtai Chemical Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Towards PVC Recycling

- 7.2 Accelerating Usage of Electric Vehicles (EVs)

聚氯乙烯(PVC)管材的全球市場

聚氯乙烯(PVC)管材的全球市場 CPVC(氯化聚氯乙烯)市場評估:依等級、應用、最終用戶和地區劃分的機會和預測(2018-2032年)

CPVC(氯化聚氯乙烯)市場評估:依等級、應用、最終用戶和地區劃分的機會和預測(2018-2032年) 亞太地區聚氯乙烯(PVC) -市場佔有率分析、產業趨勢、成長預測(2025-2030 年)

亞太地區聚氯乙烯(PVC) -市場佔有率分析、產業趨勢、成長預測(2025-2030 年) 歐洲聚氯乙烯(PVC) -市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

歐洲聚氯乙烯(PVC) -市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 聚氯乙烯的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

聚氯乙烯的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 聚氯乙烯的全球市場:各類型,各用途,各終端用戶業界,各地區,機會,預測,2018年~2032年

聚氯乙烯的全球市場:各類型,各用途,各終端用戶業界,各地區,機會,預測,2018年~2032年 聚氯乙烯市場:依產品、應用分類 - 2025-2030 年全球預測

聚氯乙烯市場:依產品、應用分類 - 2025-2030 年全球預測 聚氯乙烯市場:按形式、製造流程、等級分類 - 2025-2030 年全球預測

聚氯乙烯市場:按形式、製造流程、等級分類 - 2025-2030 年全球預測 氯化聚氯乙烯 (CPVC) 市場機會、成長動力、產業趨勢分析和 2025 年至 2034 年預測

氯化聚氯乙烯 (CPVC) 市場機會、成長動力、產業趨勢分析和 2025 年至 2034 年預測 全球聚氯乙烯 (PVC) 市場 - 2024-2031

全球聚氯乙烯 (PVC) 市場 - 2024-2031