|

市場調查報告書

商品編碼

1641890

複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Composite Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

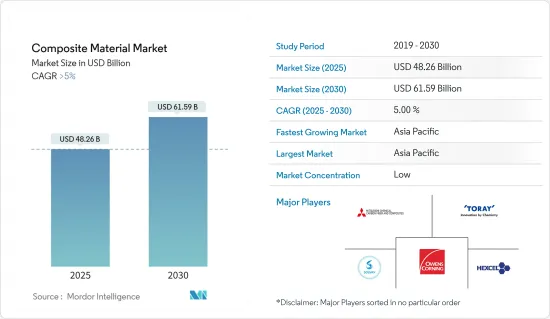

複合材料市場規模在 2025 年預計為 482.6 億美元,預計到 2030 年將達到 615.9 億美元,預測期內(2025-2030 年)的複合年成長率將超過 5%。

2021年的市場相對於2020年來說有所成長。隨著多個國家解除封鎖措施、許多製造業和建築計劃恢復,市場已部分擺脫新冠疫情帶來的不利影響。

主要亮點

- 複合材料製造領域的最新技術進步(如奈米技術、非高壓釜固化等)預計將推動市場成長。

- 另一方面,高製造成本預計將導致終端用戶市場價格上漲,從而阻礙市場成長。

- 預計在預測期內,交通運輸應用將佔據研究市場的主導地位。

- 亞太地區佔據全球整體的最大佔有率。預計該地區在預測期內也將呈現最高的成長率。

複合材料市場趨勢

運輸業需求增加

- 複合材料是由兩種或兩種以上具有不同物理和化學性質的材料構成的。長期以來,聚合物複合材料一直被提案是汽車行業中較重金屬部件的替代品,因為它們可以減輕重量,同時保持機械強度等其他理想特性。碳纖維是最適合此應用的聚合物複合材料。

- 碳纖維是一種先進的複合材料,用途廣泛,從汽車到體育用品,以及航太和國防等尖端產業。

- 由於各市場的需求量大,碳纖維製造商的數量每年都在增加。例如,美國碳纖維製造商從十年前的17家增加到2021年的58家。

- 複合材料由於其高比強度和模量一直被譽為未來材料,成為飛機應用的一個有吸引力的選擇。最新的波音787夢幻飛機由50%的複合材料製成。

- 根據OICA預測,全球汽車產量將從2022年的8,483萬輛增至2023年的9,354萬輛,年與前一年同期比較10.3%。

- 全球努力在 2050 年實現零排放,這也是汽車產業複合材料發展的關鍵驅動力,從而推動電動車 (EV) 的快速發展、創新和生產。

- 為了因應氣候變化,英國政府最近承諾在2030年將二氧化碳排放減少68%。為了實現這一目標,所有新的汽油和柴油汽車都將被禁止,並且同年英國近一半的汽車必須是電動車。這意味著要用電動車 (EV) 取代 1,610 萬輛汽車,但目前英國註冊的電動車僅有 20 萬輛左右。

- 因此,由於上述因素,運輸業在預測期內預計將呈現最高的成長率。

亞太地區成長最快

- 由於建築、汽車、電氣和電子、航太和國防以及工業等終端用戶產業的需求旺盛,亞太地區佔據了複合材料市場的最高佔有率。

- 由於中國、印度和日本等國家工業化的快速發展,亞太地區對複合材料的需求正在急劇成長。

- 由於複合材料在各行業的應用日益增多,其需求量也逐年增加。根據《複合材料世界》報道,到2021年,中國先進複合纖維碳纖維的供應量將達到約19,250噸。

- 根據OICA預測,2023年中國汽車產量約3,016萬輛,與前一年同期比較成長11.6%達到約2,702萬輛。在研究期間,汽車產業的穩定成長可能會推動複合材料市場的成長。

- 根據日本監管事務專業協會估計,日本醫療設備市場規模約300億美元,位居全球第三。因此,新冠疫情後對醫療設備的依賴增加可能會進一步促進複合材料市場的發展。

- 據鋰電池製造商Inverted 稱,印度的ESDM(電子系統設計和製造)產業預計到2025 年將達到2,200 億美元,電子製造業是「印度製造」計畫的關鍵驅動力。關鍵組成部分政府措施包括「數位印度」和「Start-Ups印度」。這被認為代表了所研究市場的一個潛在的成長機會。

- 據JEC Korea稱,韓國擁有強大的複合材料產業,擁有本土加工商和碳纖維和樹脂供應商,該國很可能繼續處於複合材料和施工方法創新的前沿。韓國政府正投入大量資源加強碳纖維產業的發展。

- 預計更嚴格的環境法規和永續目標(SDG)及《巴黎協定》等環境框架的升級將刺激輕質且極硬的碳纖維的使用。據稱亞洲的需求正在增加,特別是在體育和戶外、工業和航空領域。

- 由於這些市場趨勢,預計亞太地區將主導全球市場。

複合材料產業概況

複合材料市場相當分散,市場佔有率被多家參與者瓜分。市場的主要企業(不分先後順序)包括東麗、歐文斯科寧、三菱化學、赫氏、索爾維和帝人。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 材料科學的技術進步

- 複合複合材料在航太和國防工業的應用日益廣泛

- 其他促進因素

- 限制因素

- 複合材料高成本

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 依基質材料

- 聚合物基複合材料 (PMC)

- 熱固性樹脂

- 熱塑性樹脂

- 陶瓷/碳基複合材料 (CMC)

- 其他基質(金屬複合材料)

- 聚合物基複合材料 (PMC)

- 透過增強纖維

- 玻璃纖維

- 碳纖維

- 醯胺纖維

- 其他纖維

- 按最終用途

- 汽車與運輸

- 風力發電

- 航太和國防

- 管道和儲罐

- 建築學

- 電氣和電子

- 運動休閒

- 其他最終用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 土耳其

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- DuPont

- DIT BV

- COMPOSITES UNIVERSAL GROUP

- Hexcel Corporation

- Materion Corporation

- Mitsubishi Chemical Group Corporation

- Owens Corning

- SGL Carbon

- Solvay

- TEIJIN LIMITED.

- TORAY INDUSTRIES, INC.

第7章 市場機會與未來趨勢

The Composite Material Market size is estimated at USD 48.26 billion in 2025, and is expected to reach USD 61.59 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The market increased in 2021 compared to 2020. After the lifting of lockdowns in several countries and the resumption of many manufacturing and construction projects, the market has partially recovered from the negative effects of the COVID-19 pandemic.

Key Highlights

- Recent improvements in technological advancements such as Nanotechnology, Out-of-Autoclave (OOA) Curing, and others in composite material manufacturing are expected to drive the growth of the market.

- On the other hand, high manufacturing costs, which result in a higher price for the end-user market, are expected to hinder market growth.

- Transportation application is expected to dominate the market studied in the forecasted period.

- Asia-Pacific has the largest share across the globe. The region is also expected to have the highest growth rate during the forecasted period.

Composite Materials Market Trends

Rising Demand from Transportation sector

- Composites are made up of two or more materials that have diverse physical and chemical characteristics. Polymer composites have long been proposed as a replacement for heavier metal components in the automobile industry, offering weight savings while retaining other desirable features such as mechanical strength. Carbon Fibre is the most preferred polymer composite for this application.

- Carbon Fiber is an advanced composite material used in a wide range of applications from Automotive to sports equipment and even in the most advanced industries such as Aerospace, Defense, and other industries.

- The number of carbon fiber manufacturers are increasing year on year due to its heavy demand in various markets. For instance, in 2021, there were 58 carbon fiber producers in the United States, up from 17 in the previous decade.

- Because of their high specific strength and/or modulus, composites have long been hailed as the materials of the future, making them appealing choices for aircraft applications. In the latest Boeing 787 Dreamliner aeroplane, the amount of composites has climbed to 50%.

- According to OICA, global automotive production increased from 84.83 million units in 2022 to 93.54 million units in 2023 with a y-o-y growth of 10.3%.

- Global efforts towards zero emissions by 2050 is another significant driver for composites in automotive industry, which in turn is leading to rapid development, innovation, and production of electric vehicles (EVs)

- In an effort to combat climate change, the UK government recently pledged to decrease 68% of CO2 emissions by 2030. To achieve this goal, new petrol and diesel automobiles woulds be be prohibited, and almost half of the UK's vehicles must be electric by the same year. This entails to replacing 16.1 million automobiles with electric vehicles (EVs), with only about 200,000 EVs now registered in the UK.

- Hence, owing to the above-mentioned factors, tranportation sector is expected to witness the highest growth rate during the forecast period.

Asia-Pacific to Witness the Highest Growth Rate

- Asia-Pacific region accounts for the highest share of composite material market owing to high demand from end-user industries like construction, automotive, electrical & electronics, aerospace & defense, Industrial, etc.

- The demand for composite material in the Asia-Pacific region is growing at a staggering rate as a result of rapid industrialization in countries such as China, India, and Japan.

- The demand for composite materials is surging every year with the increase in its application in various industries. In China the supply of Carbon fiber, which is an advanced composite fiber, amounted to around 19,250 metric tonnes in the year 2021 according to CompositesWorld.

- According to OICA, automotive production in China was at around 30.16 million units in 2023, with a y-o-y growth of 11.6% from the previous year, where the production was at around 27.02 million units. The steady increase in the Automotive sector would promote the growth of the composite market during the studied period.

- According to the Regulatory Affairs Professional Society, Japan's medical device market, with an estimated value of around USD 30 billion, ranks as the third biggest across the globe. Thus, increasing dependancy on medical equipments post COVID-19 would further boost the composite market.

- As per Inverted, a lithium battery manufacturer, India's ESDM (Electronics System Design & Manufacturing) sector is expected to reach USD 220 billion by 2025 and electronics manufacturing has been a crucial component of several government initiatives, including "Make in India," "Digital India," and "Start-up India." This factor would act as a potential growth opportunity for the studied market.

- According to JEC Korea, South Korea has a strong composites sector, with local processors and carbon fibre and resin suppliers, and the nation will continue to be at the forefront of composite material and method innovations. The government of South Korea has committed substantial resources to bolstering the country's carbon fibre sector.

- Increased usage of lightweight and extremely stiff carbon fibre is predicted to be stimulated by more rigorous environmental restrictions and the upgrading of environmental frameworks, such as the Sustainable Development Goals (SDGs) and the Paris Agreement. Asia's demand is said to be increasing, particularly in the domains of sports and outdoor activities, industrial, and aircraft.

- Owing to these prevailing market trends, the Asia-Pacific region is expected to dominate the global market.

Composite Materials Industry Overview

The composite material market is moderately fragmented as the market share is divided between many players. Some of the key players in the market (not in any particular order) include TORAY INDUSTRIES, INC., Owens Corning, Mitsubishi Chemical Corporation, Hexcel Corporation, Solvay and Teijin Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Technological Advancement in the Field of Material Science

- 4.1.2 Increasing Use of Composites in the Aerospace and Defense Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Composite Materials

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Matrix Material

- 5.1.1 Polymer Matrix Composites (PMC)

- 5.1.1.1 Thermoset Resins

- 5.1.1.2 Thermoplastic Resins

- 5.1.2 Ceramic/Carbon Matrix Composites (CMCs)

- 5.1.3 Other Matrices (Metal Matrix Composites)

- 5.1.1 Polymer Matrix Composites (PMC)

- 5.2 Reinforcement Fiber

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Aramid Fiber

- 5.2.4 Other Fibers

- 5.3 End-use Application

- 5.3.1 Automotive and Transportation

- 5.3.2 Wind Energy

- 5.3.3 Aerospace and Defense

- 5.3.4 Pipes and Tanks

- 5.3.5 Construction

- 5.3.6 Electrical and Electronics

- 5.3.7 Sports and Recreation

- 5.3.8 Other End-use Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 DuPont

- 6.4.3 DIT B.V.

- 6.4.4 COMPOSITES UNIVERSAL GROUP

- 6.4.5 Hexcel Corporation

- 6.4.6 Materion Corporation

- 6.4.7 Mitsubishi Chemical Group Corporation

- 6.4.8 Owens Corning

- 6.4.9 SGL Carbon

- 6.4.10 Solvay

- 6.4.11 TEIJIN LIMITED.

- 6.4.12 TORAY INDUSTRIES, INC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

PCD 與 PCBN 刀具材料市場:2025 年

PCD 與 PCBN 刀具材料市場:2025 年 聚合物和複合材料市場十大成長機會(2025 年)

聚合物和複合材料市場十大成長機會(2025 年) 碳纖維複合材料市場規模、佔有率和成長分析(按基質材料、最終用戶和地區)- 產業預測 2025-2032

碳纖維複合材料市場規模、佔有率和成長分析(按基質材料、最終用戶和地區)- 產業預測 2025-2032 2025 年全球複合材料市場報告

2025 年全球複合材料市場報告 全球電動車複合材料市場可再生能源塗料市場規模、佔有率和成長分析(按類型、應用、最終用途和地區)- 產業預測 2025-2032

全球電動車複合材料市場可再生能源塗料市場規模、佔有率和成長分析(按類型、應用、最終用途和地區)- 產業預測 2025-2032 全球複合材料市場:依類型、基材(聚合物、金屬、陶瓷)、形式、技術、最終用戶和地區預測至2032年可再生能源複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

全球複合材料市場:依類型、基材(聚合物、金屬、陶瓷)、形式、技術、最終用戶和地區預測至2032年可再生能源複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 全球複合材料市場:樹脂、填料、增強材料、天然纖維、奈米複合材料複合材料市場規模、佔有率、成長分析、按製造程序、按纖維類型、按樹脂類型、按最終用戶、按地區 - 行業預測,2024-2031 年

全球複合材料市場:樹脂、填料、增強材料、天然纖維、奈米複合材料複合材料市場規模、佔有率、成長分析、按製造程序、按纖維類型、按樹脂類型、按最終用戶、按地區 - 行業預測,2024-2031 年