|

市場調查報告書

商品編碼

1642025

金屬加工設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Metal Fabrication Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

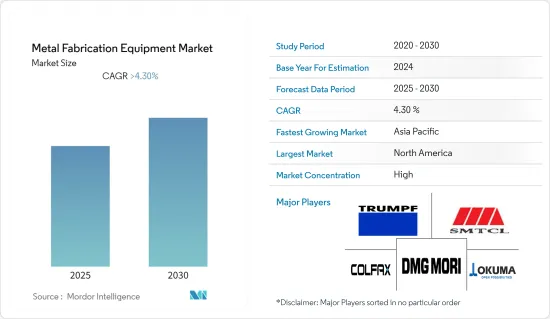

預測期內,金屬加工設備市場預計將以超過 4.3% 的複合年成長率成長。

主要亮點

- 冠狀病毒的爆發給金屬製造市場帶來了困難。政府為防止疾病傳播而實施的進出口禁令、社交距離要求和限制措施嚴重擾亂了製造流程,中斷了原料的跨境供應鏈並影響了市場。結果,市場遭受了嚴重的財務挫折。上述決定因素可能會考慮預測期內市場的收益走勢。

- 印度、中國和印尼等新興經濟體以及日本和韓國等已開發工業國家正在幫助亞太地區 (APAC) 佔據製造業主導地位,尤其是在金屬加工設備的需求方面。

- 歐洲是第二大金屬加工設備市場。預計德國、法國和義大利等工業國家將在不久的將來推動進一步的需求。

- 德國憑藉其龐大的汽車及配套產業成為歐洲最大的市場,其次是義大利、瑞士和俄羅斯等市場。

- 需求不斷成長是全球工業和金融領域格局變化的直接結果。由於該地區人口不斷成長且某些行業市場規模龐大,企業被迫將製造地遷至這些新興經濟體。

- 汽車產業及其支援產業是製造設備的最大消費者,其次是製造業企業。預計預測期內金屬加工市場關鍵產業(如航太和國防)的需求和供應將會恢復。

- 能源的使用和需求是由世界人口的成長所驅動的。快速的工業化預計將增加對加工設備的需求。然而,原物料價格上漲預計將成為市場擴張的一大障礙。然而,技術改進和設計客製化設備的努力預計將在不久的將來為生產商帶來新的機會。

金屬加工設備市場趨勢

更加重視工業 4.0 的實施

關鍵趨勢工業 4.0 或物聯網 (IoT) 的發展預計將對工具和製造設備產生重大影響,因為它與工具機和工程師/操作員的資訊流有關。智慧工具有望提供即時回饋並向工程師發出振動等問題警報。

向工業 4.0 的過渡始於日常運作中一致的處理環境。在這個過程的開始階段,刀具預設至關重要。一旦刀架組件被預設,資料就可以直接髮送到工具機(節省時間並防止潛在的加工錯誤)或傳輸到附在刀架上的 RFID 晶片。

製造商發現預設過程是減少生產過程中廢品的重要因素。隨著企業轉向更一致、更有效率的加工,對工業 4.0 解決方案的需求也日益成長。

市場的成長潛力是由數位化和網路普及率不斷提高的趨勢所推動的,這導致各個行業都注重效率和盈利生產力。

數位技術和工業電腦化的最新趨勢開始有可能顛覆工業價值鏈。隨著第四次工業革命(4.1)的到來,企業受益於更高的生產力、個人化的產品、成本的降低,最重要的是,新的收入和經營模式的產生。

隨著全球市場環境受到新冠疫情衝擊,各產業數位化正快速加速。這為數位領導者創造了新的機會來開發和採用創造性的解決方案,以加速企業各層面的數位轉型。

冠狀病毒流行加速了第四次工業革命(工業 4.0)的採用,推動各行業的公司走向更先進的物聯網 (IoT) 技術和工作流程。新冠肺炎疫情影響全球,全球供應鏈陷入前所未有的不確定性。一些製造公司已經完全停止生產,其他公司的需求大幅下降,許多公司的需求甚至增加。

加工中心和工具機市場的成長

加工中心市場的發展受到製造業自動化程度不斷提高的推動。近年來,金屬加工業務大幅成長。

隨著對高精度、低誤差和大規模生產的需求不斷成長,對加工中心的需求也日益成長。此外,製造商希望大幅降低營業成本以增加其產品的吸引力。由於可用於生產的空間越來越小,製造商正致力於減少週期時間和物料輸送、提高品質和消除轉換時間。所有這些因素都有望增加對加工中心的需求。

未來幾年,亞太地區金屬加工市場可能會顯著成長,這得益於各應用產業(主要是汽車、航太和國防市場)的強勁成長。

另一個預期的好處是,由於 CNC 加工中心的普及,加工中心市場的收益將增加。這進一步歸因於生產過程控制的加強和透明度的提高,從而改善了工具的移動。

先進的 CNC 編程可以精確控制位置、速度、進給速率和同步等眾多變數。此外,CNC技術的普及還在於它能夠輕鬆加工複雜的表面。

由於對操作員安全性、高精度、即時監控、更大靈活性和更高切削參數的需求不斷增加,加工中心市場正在不斷擴大。此外,工業4.0解決方案的使用將增加對智慧設備的需求。因此,連桿型加工中心的市場預計將擴大。

2021年全球工具機市場由中國、德國和日本主導。同年,中國生產了全球31%的工具機,而德國和日本分別佔13%和12%。

金屬加工設備產業概況

據稱全球金屬加工設備市場正在整合。該報告介紹了金屬加工設備市場的主要國際參與者。從市場佔有率來看,目前少數幾家大公司佔據著市場主導地位。然而,它面臨著來自區域參與者和專注於提供自訂設備的中小型企業的激烈競爭。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

- 分析方法

- 研究階段

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 市場限制

- 市場機會

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 市場技術趨勢

第5章 市場區隔

- 按地區

- 北美洲

- 拉丁美洲

- 亞太地區 (APAC)

- 歐洲

- 中東和非洲 (MEA)

- 按服務類型

- 加工和切割

- 加工中心

- 車床

- 鑽床、研磨、搪光機、研磨機

- 雷射、離子束、超音波加工機

- 齒輪加工機

- 鋸切機

- 其他搬運和切割設備

- 焊接

- 電弧焊接

- 富氧燃燒焊接

- 雷射焊接

- 其他焊接

- 成型

- 鍛造機和錘子

- 折彎機、折彎機、矯正機

- 剪切機、沖孔機和開槽機

- 線材成型機

- 其他壓力機及金屬成型機

- 其他服務類型

- 加工和切割

- 按最終用戶產業

- 汽車

- 建造

- 航太

- 電氣和電子

- 其他最終用戶產業

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- Trumpf

- Shenyang Machine Tool

- Amada

- Okuma

- DMG MORI

- FANUC Corp.

- Colfax

- Atlas Copco

- BTD Manufacturing*

第7章:市場的未來

第8章 免責聲明

The Metal Fabrication Equipment Market is expected to register a CAGR of greater than 4.3% during the forecast period.

Key Highlights

- The market for metal manufacturing suffered as a result of the coronavirus outbreak. Government-imposed import/export prohibitions, social distance requirements, and a plethora of regulations meant to prevent the spread of illness have severely disrupted manufacturing processes and stopped the cross-border supply chains for raw materials, which impacted the market. The market suffered a severe financial setback as a result. The aforementioned determinants will take the market's revenue trajectory into consideration over the projection period.

- Developing economies, such as India, China, and Indonesia, among others, along with industrialized countries, such as Japan and South Korea, have assisted the Asia-Pacific (APAC) region to dominate the manufacturing industry, in terms of demand, particularly with the demand for metal fabrication equipment.

- Europe is the second-largest market for metal fabrication equipment. Industrialized countries, such as Germany, France, and Italy, are expected to fuel the demand further in near future.

- Germany is the largest market in Europe, owing to the presence of huge automotive and ancillary industries, followed by Italy, and other markets, such as Switzerland and Russia.

- Growing demand is a direct result of global industrial and finance sectors experiencing changing patterns. Companies were pushed to relocate their manufacturing operations to these emerging economies by the growing population in the Asia Pacific region and the sizeable markets for several industry verticals.

- The automotive industry and its auxiliary sectors are the biggest consumers of fabrication equipment, closely followed by manufacturing companies. Over the course of the forecast period, demand and supply for key industries in the metal fabrication market, such as aerospace & defense, are anticipated to pick up.

- The use and demand for energy are being driven by the growing world population. The demand for fabrication equipment is expected to increase due to rapid industrialization. The high price of raw materials, however, is anticipated to be a significant barrier to the market's expansion. Nevertheless, it is projected that in the near future, new opportunities will be opened up for the producers thanks to technical improvements and efforts to design customized equipment.

Metal Fabrication Equipment Market Trends

Increasing Focus on the Implementation of Industry 4.0

The growth of Industry 4.0, or the Internet of Things (IoT), which is a key trend, is expected to have a profound influence on tooling and fabricating equipment, as it relates to the flow of information to machine tools and engineers/operators. Smart tooling is expected to provide real-time feedback about problems, such as vibration, and send alerts to the engineer.

The transition to Industry 4.0 starts with machining environments that are highly consistent in day-to-day operations. Tool presetting is vital to the beginning of this process. Once the tool holder assembly is preset, data can be sent directly to the machine tool (saving time and preventing potential machining mistakes) or it can be transferred to an RFID chip installed in the tool holder.

Manufacturers find the presetting process to be a huge factor in reducing scrap during production. The demand for Industry 4.0 solutions is increasing as companies move toward consistent, highly productive machining.

The market's growth potential are being driven by rising trends of digitization and internet penetration brought on by various sectors' increased focus on effectiveness and profitable productivity.

The potential for disrupting the industrial value chain has started to grow as a result of recent developments in digital technologies and industrial computerization. With the arrival of the fourth industrial revolution (4.1), businesses are benefiting from higher productivity, individualized products, decreased costs, and, most crucially, the creation of new income and business models.

With the global market environment being ravaged by the COVID-19 pandemic, digitalization across industries are accelerating at a rapid rate. This presents a new opportunity for digital leaders to develop and adopt creative solutions to accelerate digital transformation at all levels of the company.

The outbreak of the coronavirus is hastening the introduction of the fourth industrial revolution (Industry 4.0), propelling businesses across sectors to a higher level of Internet of Things (IoT) technology and workflow. The global supply chain is undergoing unprecedented instability as a result of the COVID-19 pandemic that has affected the entire planet. Some manufacturing firms have completely stopped production while others have seen a significant decrease in demand and a few witnessed an increase in demand

Growth of Machining Centers and the Machine Tools Market

The market for machining centers is being driven by the manufacturing industry's growing automation. Over the past few years, there have been substantial developments in the metal fabrication business.

The demand for machining centers is rising as a result of increased demand for high accuracy, decreased mistakes, and mass manufacturing. Additionally, manufacturers anticipate that a large reduction in operating costs will increase the attractiveness of their products. With less space available for production, manufacturers are concentrating on reducing cycle times and material handling, improving quality, and doing away with changeover times. It is anticipated that all of these causes will increase demand for machining centers.

The metal fabrication market in Asia-Pacific is likely to experience substantial growth over the next few years, owing to the robust growth in various application industries, especially in the automotive, aerospace, and defense markets.

Further anticipated effects include an increase in machining centers market revenue due to rising CNC machining center adoption. This is further due to the improved tool movement brought about by greater control and growing production process transparency.

Numerous variables, including position, speed, feed rate, and synchronization, can be precisely controlled thanks to the sophisticated CNC programming. Furthermore, the popularity of CNC technology is being driven by the simplicity of producing complicated surfaces.

The market for machining centers is expanding as a result of the rising demand for worker safety, high precision, real-time monitoring, higher flexibility, and high cutting parameters. Additionally, when Industry 4.0 solutions are used, there is an increase in there is an increase in demand for smart instruments. Thus, the market for linked machine centers is anticipated to expand.

China, Germany, and Japan dominated the global machine tool market in 2021. China produced 31% of the world's machine tools in that year, compared to 13% produced by Germany and 12% produced by Japan.

Metal Fabrication Equipment Industry Overview

The Global metal Fabrication Equipment Market is said to be consolidated. The report covers major international players operating in the metal fabrication equipment market. In terms of market share, a few of the major players currently dominate the market studied. However, they face stiff competition from regional players and mid-size and smaller companies that are focused on providing custom equipment in the market studied.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Market Opportunities

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Technological Trends in the Market

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 North America

- 5.1.2 Latin America

- 5.1.3 Asia-Pacific (APAC)

- 5.1.4 Europe

- 5.1.5 Middle East and Africa (MEA)

- 5.2 Service Type

- 5.2.1 Machining and Cutting

- 5.2.1.1 Machining Centres

- 5.2.1.2 Lathe Machines

- 5.2.1.3 Drilling, Grinding, Horning, and Lapping Machines

- 5.2.1.4 Laser, Ion Beam, and Ultrasonic Machines

- 5.2.1.5 Gear Cutting Machines

- 5.2.1.6 Sawing and Cutting-off Machines

- 5.2.1.7 Other Handling and Cutting Equipment

- 5.2.2 Welding

- 5.2.2.1 ARC Welding

- 5.2.2.2 Oxy-fuel Welding

- 5.2.2.3 Laser Beam Welding

- 5.2.2.4 Other Types of Welding

- 5.2.3 Forming

- 5.2.3.1 Forging Machines and Hammers

- 5.2.3.2 Bending, Folding, and Straightening Machines

- 5.2.3.3 Shearing, Punching, and Notching Machines

- 5.2.3.4 Wire Forming Machines

- 5.2.3.5 Other Presses and Metal Forming Machines

- 5.2.4 Other Service Types

- 5.2.1 Machining and Cutting

- 5.3 End-user Industries

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Aerospace

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Trumpf

- 6.2.2 Shenyang Machine Tool

- 6.2.3 Amada

- 6.2.4 Okuma

- 6.2.5 DMG MORI

- 6.2.6 FANUC Corp.

- 6.2.7 Colfax

- 6.2.8 Atlas Copco

- 6.2.9 BTD Manufacturing*

7 FUTURE OF THE MARKET

8 DISCLAIMER

金屬加工設備市場報告,按類型(切割、機械加工、焊接、折彎等)、應用(加工車間、汽車、航太和國防、機械應用等)和地區,2025 年至 2033 年

金屬加工設備市場報告,按類型(切割、機械加工、焊接、折彎等)、應用(加工車間、汽車、航太和國防、機械應用等)和地區,2025 年至 2033 年 金屬加工,全球市場 2025-2029

金屬加工,全球市場 2025-2029 歐洲金屬加工設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲金屬加工設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 金屬加工,全球市場 2025-2029

金屬加工,全球市場 2025-2029 線圈繞線機市場:按操作、機器類型、錠數、產能和最終用戶 - 2025-2030 年全球預測

線圈繞線機市場:按操作、機器類型、錠數、產能和最終用戶 - 2025-2030 年全球預測 鈑金加工設備市場:按設備類型、技術和應用分類 - 2025-2030 年全球預測

鈑金加工設備市場:按設備類型、技術和應用分類 - 2025-2030 年全球預測 全球專用機械市場,2024-2028

全球專用機械市場,2024-2028 特種模具/工具、晶粒、夾具/固定固定裝置、機會和策略到 2033 年

特種模具/工具、晶粒、夾具/固定固定裝置、機會和策略到 2033 年 特殊模具/工具、晶粒、夾具/夾具市場:按產品、功能、應用和最終用途行業 - 2025-2030 年全球預測

特殊模具/工具、晶粒、夾具/夾具市場:按產品、功能、應用和最終用途行業 - 2025-2030 年全球預測 世界金屬加工市場

世界金屬加工市場