|

市場調查報告書

商品編碼

1644298

通訊管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Correspondence Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

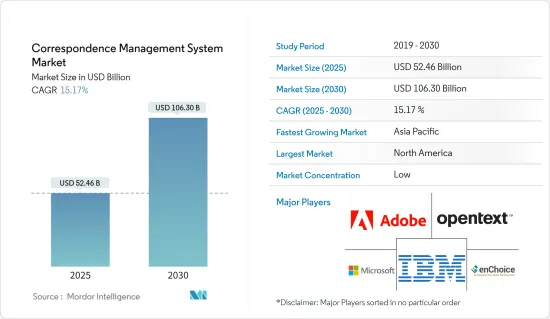

通訊管理系統市場規模預計在 2025 年為 524.6 億美元,預計到 2030 年將達到 1063.0 億美元,預測期內(2025-2030 年)的複合年成長率為 15.17%。

CMS 中技術採用趨勢的上升,例如 CMS 中對 AI 的需求上升、基於語音的搜尋最佳化的使用增加以及內容管理中聊天機器人的使用增加,是預計在預測期內推動市場成長的一些因素。

主要亮點

- 自動化刺激了通訊管理系統的選擇,特別是在遵循基於規則的流程的企業中,減少了業務環境中的不一致性並終止通訊,從而實現了高效的內部和外部通訊系統。

- 由於全球各組織擴大採用數位化工作文化以及產業內容的擴展,通訊管理系統市場正在全球迅速擴張。此外,巨量資料和分析解決方案的發展正在提高內部和外部通訊的自動化程度。此外,企業正在迅速轉向即時通訊系統來有效管理所有通訊。

- 此外,隨著雲端基礎的技術的出現和業務數位化的日益發展,企業經常轉向郵件室自動化來實現其內部和外部業務溝通流程的自動化。這使得企業能夠根據通訊的內容、外觀和類別對其進行分類,然後將其發送給適當的部門或個人。

- 此外,通訊管理系統可實現自動化,提供速度和靈活性,從而更好地洞察客戶和內部業務。企業正在實施數位轉型以更快地滿足客戶需求。透過定期溝通讓股東和消費者了解情況可以幫助公司增加收益並提高採用率。巨量資料和進階分析等新 IT 應用和基礎設施的採用也是推動通訊管理系統市場成長的因素之一。此外,企業還可以利用具有預測能力的通訊管理系統解決方案,利用巨量資料來改善決策。

- 然而,限制和約束市場成長的挑戰包括資料孤立、資料整合平台不同以及缺乏技術能力。

- COVID-19 對依賴客戶互動的企業產生了深遠的影響。數位化轉換、互動性和收益成長現在比以往任何時候都更加重要。因此,許多企業將內容管理系統和數位體驗平台(管理線上體驗的平台)視為關鍵任務軟體。

- 投資、管理和營運這些平台的個人需要重新評估他們的平台需求,並確保他們的 CMS 能夠跟上延長的 WFH、增加的網路流量和不斷變化的行銷策略。此外,借助具有生產力、協作、效能和安全性等功能的現代雲端託管 CMS,將大大減輕由於 COVID-19 導致的業務需求增加、緊迫的期限和增加的行銷需求所帶來的負擔。

通訊管理系統市場趨勢

便利、安全的內部和外部通訊推動市場成長

- 內容管理系統旨在供所有人存取。這些程式通常具有方便用戶使用的介面並且易於操作。不需要技術或程式設計知識,但根據 CMS 平台可能需要一些協助和專業知識。這些獨特的優勢正是推動 CMS 採用率成長的動力。

- 私人、個人化、互動性強的商業文件的開發、編輯和分發透過通訊管理系統進行集中管理。該技術使公司能夠透過從製作到歸檔的簡化流程,使用預先核准或自訂的材料快速創建通訊,從而提高客戶的便利性。

- 從而,客戶能夠快速、準確、簡單、安全且適當地收到正確的訊息。這使企業能夠最大限度地提高消費者互動的價值,同時降低與複雜流程相關的成本和風險,有助於推動市場成長。

- 此外,Storyblok 進行的一項調查發現,2023 年最大量使用 CMS 的團隊將是行銷團隊(17%),緊隨其後的是銷售團隊(17%)和財務團隊(15%)。設計團隊(7%)和高階主管(6%)是最不可能使用企業 CMS 的兩個團隊。如此顯著的採用率可能意味著 CMS 技術提供的便利性和安全性正在促進跨組織內部和外部溝通的有效性。

北美佔據主要市場佔有率

- 由於零售、電子商務、垂直行業和政府組織等各個垂直行業對自動化的應用日益廣泛,以及對有效的內部和外部溝通以提高保留率的需求日益增加,北美佔據了主要的市場佔有率。北美最大的兩個市場—美國和加拿大,正在見證通訊管理系統解決方案等先進技術的採用。

- 例如,據微軟稱,由於自動化和簡化的協作,該地區的時間和資源管理變得更加有效和富有成效。例如,美國透過簡化任務管理和部門與團隊之間的溝通,每年節省了近 140 萬美元。

- 預計企業將在 IT 和電訊等關鍵產業中廣泛使用通訊管理系統,以防止手動業務流程中斷。信函管理系統可以有效管理、搜尋、追蹤和報告信函和行動計劃。預計各新興產業間日益增多的通訊交流將推動整個全部區域CMS 供應商的崛起。

- 該地區著名的國際通訊管理系統供應商包括 IBM、Microsoft、Adobe、Open Text、Pitney Bowes、Micropact、Xerox 和 Top Down Systems。這些大公司的存在是該全部區域產生可觀收益的主要原因。

通訊管理系統產業概況

通訊管理系統市場競爭適中,由幾個主要參與者組成。全球主要供應商包括 IBM Corporation、Microsoft Corporation、OpenText Corporation 和 Adobe, Inc.服務供應商正嘗試透過與軟體公司合作、提供端到端解決方案以及充當通訊管理解決方案一站式商店的解決方案方式進入市場。目前,通訊管理系統市場中的參與者正在以實惠的價格提供各種雲端基礎的解決方案,預計將為提供這些系統的公司創造巨大的商機。

- 2023 年 2 月-數位文件和合約生命週期管理公司 SignDesk 與微軟和 G7 CR Technologies 合作,以增強公司的雲端部署能力。透過這種合作關係,企業將能夠利用與 SignDesk 產品套件整合的 Microsoft Azure 的功能。 SignDesk 文件自動化套件也將在 Microsoft Marketplace 上亮相。產品組合中的解決方案解決數位化入職、合約生命週期管理和數位化文件執行等問題。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

第5章 市場動態

- 市場促進因素

- 對通訊系統自動化和個人化的需求日益增加

- 方便、安全的內部和外部通訊

- 市場限制

- 由於賣家資料和資料系統脫節,缺乏技術專業知識影響資料整合

- 初期投資高且缺乏認知

第6章 市場細分

- 按組件

- 軟體

- 按服務

- 按分銷管道

- 基於網路

- 基於電子郵件

- 其他交付管道(基於 SMS/MMS 等)

- 按部署模型

- 本地

- 雲

- 按組織規模

- 中小型企業

- 大型企業

- 按行業

- BFSI

- 政府及公共機構

- 電信和 IT

- 衛生保健

- 零售與電子商務

- 其他行業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- IBM Corporation

- Adobe Inc.

- Microsoft Corporation

- OpenText Corporation

- Rosslyn Data Technologies Inc.(enChoice, Inc.)

- Pitney Bowes Inc.

- Newgen Software Technologies Limited

- Fabasoft AG

- MicroPact Inc.

- Everteam SAS

- Ademero, Inc.

- Blue Project Software Inc.

- Xerox Holdings Corporation

- Palaxo International Ltd.

- Top Down Systems Corporation

- Harvest Technology Group

第8章投資分析

第9章 市場機會與未來趨勢

The Correspondence Management System Market size is estimated at USD 52.46 billion in 2025, and is expected to reach USD 106.30 billion by 2030, at a CAGR of 15.17% during the forecast period (2025-2030).

The rising trends of technology adoption in CMS, such as rising demand for AI in CMS, increasing use of Voice-based search optimization, and rising chatbot usage for content management, are a few factors anticipated to drive the market growth during the forecast period.

Key Highlights

- Automation stimulates the selection of a correspondence management system, especially for businesses that follow rule-based processes, diminishing inconsistencies and terminating correspondences in the business environment, thereby allowing efficient internal and external communication systems.

- The correspondence management system market is expanding rapidly on a global scale due to the rise in the adoption of a digital working culture in organizations worldwide and the expansion of content in industries. In addition, developing big data and analytics solutions has increased internal and external communication automation. Additionally, businesses are fast using real-time communication systems to manage all correspondences effectively.

- Moreover, businesses frequently use mailroom automation to automate their internal and external business communication processes as a result of the emergence of cloud-based technologies and the growing digitalization of businesses. This helps businesses to classify their incoming correspondence according to its content, appearance, and category and send it to the appropriate department or individual.

- Further, a correspondence management system automates, providing speed and agility to generate superior customer and internal affairs insights. Organizations are using digital transformation to satisfy client demands more quickly. By keeping shareholders and consumers informed through regular contact, the solutions allow businesses to increase revenues, which raises the adoption rate. Introducing new IT applications and infrastructure, such as big data and sophisticated analytics, is another driver fueling the market's growth for correspondence management systems. Additionally, businesses may use big data to improve decision-making with solutions for a correspondence management system that has predictive capabilities.

- However, some challenges limiting and constraining the market's growth include segregated data, different platforms for data integration, and a lack of technical competence.

- COVID-19 has severely impacted businesses relying on customer interaction to generate income. Conversion, interactivity, and revenue growth through digital are being prioritized more than ever. As a result, many organizations view content management systems and digital experience platforms-platforms that govern online experiences-as mission-critical software.

- Individuals investing in, administering, and operating on these platforms need to reassess their platform needs and ensure their CMS can sustain them during prolonged WFH periods, more internet traffic, and changing marketing strategies. Moreover, the strain of increasing business requirements, tight deadlines, and increased marketing demands due to COVID-19 significantly lessened with the help of a contemporary cloud-hosted CMS with features surrounding productivity, collaboration, performance, and security.

Correspondence Management System Market Trends

Convenient and Secured Internal and External Communications to Drive the Market Growth

- Content management systems are intended to be used by everyone. The program typically has a user-friendly interface and is simple to navigate. While no technical or programming knowledge is necessary, some CMS platforms can require some assistance or expertise. Such characteristic benefits are factors responsible for the growth of CMS adoption.

- The development, compilation, and distribution of private, personalized, and interactive business correspondences are centralized and managed by correspondence management systems. The technology allows businesses to rapidly create communication using pre-approved and custom-written material in a simplified process from production to archive, thereby enhancing convenience to the clients.

- As a result, clients receive the appropriate message quickly, accurately, easily, securely, and relevantly. This enables companies to lower costs and risks related to a complicated process while maximizing the value of consumer interactions, thereby driving market growth.

- Moreover, according to a survey conducted by Storyblok, in 2023, the team that used the CMS most frequently was marketing, with 17%, closely followed by sales, 17%, and finance, 15%. Design teams and executives, with 7% and 6%, respectively, were the two teams that were least likely to use a company's CMS. Such significant adoption rates might signify the convenience and security offered by the CMS technology driving the effectiveness of internal and external communication across the organization.

North America to Hold Significant Market Share

- North America accounts for one of the significant market shares due to the growing use of automation and the increasing demand for effective internal and external communication for improved retention in several business verticals, such as retail and eCommerce, BFSI, and government. The adoption of advanced technology, such as solutions for correspondence management systems, has been increasing in the two strongest markets in North America: the United States and Canada.

- For instance, according to Microsoft Corporation, automation and simplified collaboration in the region make time and resource management more effective and productive. For example, the United States Air Force significantly saved nearly USD 1.4 million yearly by streamlining task management and communication among departments and teams.

- Businesses are expected to use the correspondence management system significantly to prevent manual business procedures from disrupting operations in crucial industry verticals like IT & telecom. The correspondence management system effectively maintains, searches, tracks, and reports correspondence and action plans. The rising communication exchange across various emerging industries are expected to create CMS vendors across the region.

- The region's prominent international providers of correspondence management systems include IBM, Microsoft, Adobe, OpenText, Pitney Bowes, MicroPact, Xerox, and Top Down Systems. The presence of such large enterprises are primarily responsible for the considerable revenue generation across the region.

Correspondence Management System Industry Overview

The Correspondence Management System Market is moderately competitive and consists of several major players. Some of the key providers across the globe include IBM Corporation, Microsoft Corporation, OpenText Corporation, and Adobe, Inc., among others. The Service Providers are trying to go to the market through a solution approach by tying up with software houses, providing it as an end-to-end solution, and behaving like a one-stop-shop for the correspondence management solution. The players operating in the correspondence management system market are now offering various cloud-based solutions at affordable prices, which are expected to provide considerable opportunities to the companies providing these systems.

- February 2023 - SignDesk, a digital documents and contract lifecycle management player, partnered with Microsoft and G7 CR Technologies to enhance the company's cloud deployment capabilities. Through this relationship, businesses can use the Microsoft Azure features integrated with the SignDesk suite of products. The document automation suite from Sign Desk will also be featured in the Microsoft marketplace. The solutions in this portfolio address digital onboarding, contract lifecycle management, and digital document execution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Need for Automating and Personalizing Communication Systems

- 5.1.2 Convenient and Secured Internal and External Communications

- 5.2 Market Restraints

- 5.2.1 Cellar Data and Disparate Data Systems Impacting Data Integration augmented by Lack of Technical Expertise

- 5.2.2 Higher Initial Investments and Lack of Awareness

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Delivery Channel

- 6.2.1 Web-based

- 6.2.2 Email-based

- 6.2.3 Other Delivery Channels (SMS/MMS-based, etc.)

- 6.3 By Deployment Model

- 6.3.1 On-Premises

- 6.3.2 Cloud

- 6.4 By Organization Size

- 6.4.1 Small & Medium Enterprises

- 6.4.2 Large Enterprises

- 6.5 By Industry Vertical

- 6.5.1 BFSI

- 6.5.2 Government & Public Sector

- 6.5.3 Telecom & IT

- 6.5.4 Healthcare

- 6.5.5 Retail & E-commerce

- 6.5.6 Other Industry Verticals

- 6.6 Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia Pacific

- 6.6.4 Latin America

- 6.6.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Adobe Inc.

- 7.1.3 Microsoft Corporation

- 7.1.4 OpenText Corporation

- 7.1.5 Rosslyn Data Technologies Inc. (enChoice, Inc.)

- 7.1.6 Pitney Bowes Inc.

- 7.1.7 Newgen Software Technologies Limited

- 7.1.8 Fabasoft AG

- 7.1.9 MicroPact Inc.

- 7.1.10 Everteam SAS

- 7.1.11 Ademero, Inc.

- 7.1.12 Blue Project Software Inc.

- 7.1.13 Xerox Holdings Corporation

- 7.1.14 Palaxo International Ltd.

- 7.1.15 Top Down Systems Corporation

- 7.1.16 Harvest Technology Group

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年兒童照護管理軟體市場報告(按解決方案、部署、最終用戶和地區分類)

2025 年至 2033 年兒童照護管理軟體市場報告(按解決方案、部署、最終用戶和地區分類) 2025 年至 2033 年飯店和飯店管理軟體市場報告(按類型、飯店類型、部署和地區)

2025 年至 2033 年飯店和飯店管理軟體市場報告(按類型、飯店類型、部署和地區) 永續性管理軟體市場:全球 2025-2029

永續性管理軟體市場:全球 2025-2029 全球教育圖書館管理系統 (LMS) 市場

全球教育圖書館管理系統 (LMS) 市場 娛樂管理軟體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施類型、部署、最終用途、地區和競爭細分,2020-2030 年

娛樂管理軟體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施類型、部署、最終用途、地區和競爭細分,2020-2030 年 2025-2033 年績效評估與管理軟體市場(按類型、部署模式、組織規模、垂直產業和地區)

2025-2033 年績效評估與管理軟體市場(按類型、部署模式、組織規模、垂直產業和地區) 俱樂部管理軟體市場規模、佔有率、按俱樂部規模、部署模式、應用和地區分類的成長分析 - 產業預測,2025 年至 2032 年

俱樂部管理軟體市場規模、佔有率、按俱樂部規模、部署模式、應用和地區分類的成長分析 - 產業預測,2025 年至 2032 年 檢驗室管理服務的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2025年~2032年)

檢驗室管理服務的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2025年~2032年) 2024 年宣傳軟體全球市場報告

2024 年宣傳軟體全球市場報告 2024 年筆記管理軟體全球市場報告

2024 年筆記管理軟體全球市場報告