|

市場調查報告書

商品編碼

1644309

數位銀行平台 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Digital Banking Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

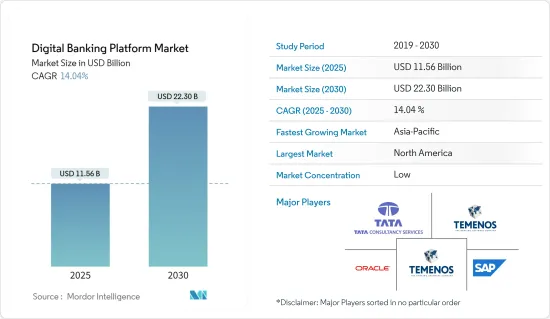

預計 2025 年數位銀行平台市場規模為 115.6 億美元,預計到 2030 年將達到 223 億美元,預測期內(2025-2030 年)的複合年成長率為 14.04%。

隨著消費者對智慧行動裝置和數位銀行服務的需求,銀行業正在迅速數位化。這些是推動市場成長的一些主要因素。

關鍵亮點

- 大多數銀行喜歡數位銀行平台,因為它們提供各種好處,例如降低 IT 成本、加快產品上市時間、開放銀行、開箱即用且可配置的功能、全通路客戶體驗、微服務架構等。例如,2022 年 12 月,德勤宣布與 AWS 合作,解決業務的一個長期挑戰:向涵蓋從客戶端介面到後勤部門業務等所有內容的數位優先系統過渡。

- 儘管新型銀行仍是一個小眾市場,但它們的市場佔有率正在強勁成長,為客戶提供的服務成本僅為傳統銀行的三分之一左右。金融科技瞄準的是價值鏈中利潤豐厚的市場。擁有龐大基本客群的大型科技公司是真正的威脅,而少數現有企業正在大力投資創新,將後進企業推向陰影。

- 然而,數位銀行平台與舊有系統的整合、網路中斷和安全問題等問題可能會阻礙市場成長,因為這些因素可能會對銀行造成嚴重損失。

- 新冠疫情導致網路銀行活動增加,包括數位交易的增加,以及實體銀行分行客流量的減少。疫情迫使個人消費者以及曾經抵制網路銀行的企業採用數位銀行應用程式作為新的預設。疫情增加了消費者的便利性,這可能會在長期內提振需求。在供應商方面,大多數公司都專注於透過提供困難時期所需的服務來贏得客戶。

數位銀行平台市場趨勢

雲端基礎平台的普及推動市場成長

- 2023年1月,菲律賓數位銀行GoTyme Bank與全球雲端銀行平台Mambu合作,打造創新的數位銀行解決方案,旨在增加菲律賓人獲得優質金融服務的機會。

- 許多銀行傾向於利用雲端基礎的服務來降低內部設置所需的IT基礎設施成本。雲端基礎的服務使您能夠快速推出新產品和擴展基礎設施,快速服務於具有多樣化需求的廣泛客戶群,並在保持合規性和安全標準的同時管理即時付款的快速成長。

- 向SaaS供應商支付訂閱費,從而減少系統維護成本和遺留技術問題。 SaaS 使銀行避免在 IT 上花費數十億美元,並重新分配預算以專注於創新、客戶滿意度和業務成長。

- 此外,透過利用雲,行動銀行平台可以提供響應式使用者介面 (UI),以支援銀行客戶在行動裝置上的整個銀行業務流程,從入職到交易銀行請求。由於對行動銀行偏好的改變,銀行正迅速採用行動銀行平台。

- 此外,Whatsapp Pay 和 PhonePay 等第三方即時付款應用程式的採用率不斷提高,也導致銀行對可靠的基礎設施產生需求,以促進 UPI 交易。例如,Visa 最近以 53 億美元完成了對金融科技新興企業Plaid 的收購,該技術使應用程式能夠輕鬆、即時地連接到客戶的銀行帳戶。這項技術轉變正在推動數位銀行業對雲端基礎設施的需求。

預計北美將佔很大佔有率

- 許多大型銀行向北美擴張是數位銀行平台市場不斷擴大的主要原因。該地區的數位銀行公司提供軟體即服務(SaaS)解決方案,以協助數位化舊有系統。例如,Temenos 提供功能最豐富、技術最先進的前端到後端 SaaS 數位銀行產品,幫助美國新數位銀行在 90 天內運作。

- 隨著可提高安全性的區塊鏈技術擴大應用,尤其是在 BSFI 領域,數位銀行平台變得越來越受歡迎。這正在推動國內市場的成長。許多公司正在開發基於區塊鏈的雲端數位銀行平台。

- 北美也是最具創新力和最早採用雲端運算的地區之一。雲端基礎設施供應商已在該地區建立了強大的影響力,幫助市場進一步成長。

- 隨著金融科技應用程式的使用量同樣增加,數位銀行平台的使用量也穩定成長,並成為美國成長最快的應用程式之一。全球冠狀病毒(COVID-19)大流行導致美國人們更多地待在家裡並更多地使用行動電話。這導致了全部區域數位銀行業務的增加。

數位銀行平台產業概況

數位銀行平台市場日益分散。這是因為多家公司和解決方案正在進入市場,造成了數位銀行生態系統的碎片化。然而,隨著技術進步和產品創新,中小企業正在透過贏得新合約和夥伴關係關係來擴大其市場影響力。

2023 年 1 月,Axis Bank 與 OPEN 合作,為其客戶提供完全原生的數位活期帳戶,包括小型企業、自由工作者、自營業者和有影響力的人。此次合作將使更大的商業社區能夠獲得 Axis Bank 的綜合銀行體驗和 OPEN 的端到端財務自動化功能,以用於付款、會計、薪資核算、合規和費用管理等業務營運。

2022 年 11 月,Capco 和 Savana 宣佈建立策略合作,以加速銀行轉型並推動數位產品的持續創新。此次夥伴關係將協助銀行克服所面臨的技術挑戰,滿足客戶對無縫、現代、全通路體驗不斷變化的期望與需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 市場促進因素

- 擴大採用雲端基礎的平台來實現高可擴展性

- 消費者對智慧行動裝置和數位銀行服務的需求日益增加

- 市場限制

- 安全擔憂日益加劇

- COVID-19 工業影響評估

第5章 市場區隔

- 按部署

- 雲

- 本地

- 按類型

- 公司銀行

- 零售銀行

- 按地區

- 北美洲

- 亞太地區

- 歐洲

- 中東和非洲

第6章 競爭格局

- 公司簡介

- Appway AG

- CREALOGIX Holding AG

- EdgeVerve Systems Limited

- Fiserv, Inc.

- Oracle Corporation

- SAP SE

- Sopra Steria

- Tata Consultancy Services Limited

- Temenos Headquarters SA

- Worldline SA

第7章投資分析

第8章 市場機會與未來趨勢

The Digital Banking Platform Market size is estimated at USD 11.56 billion in 2025, and is expected to reach USD 22.30 billion by 2030, at a CAGR of 14.04% during the forecast period (2025-2030).

The banking industry is going through a digital transformation quickly, and consumers want smart mobile devices and digital banking services. These are some of the main things that are driving the market's growth.

Key Highlights

- The majority of the banks prefer digital banking platforms due to the various benefits offered, such as reduced IT cost, fast time to market, open banking, out-of-the box yet configurable capabilities, omnichannel customer experience, and microservice architecture, to name a few. For example, in December 2022, Deloitte announced a collaboration with AWS to address a chronic difficulty in banking: the transition to digital-first systems that span the client interface to back office operations.

- Though neo-banks are still a niche market, they are witnessing a higher growth rate in terms of market share and serving customers at around one-third of the cost of traditional banks. Fintechs are targeting lucrative niches in the value chain. The big tech players, with their large customer bases, pose a real threat, and a few incumbents are investing heavily in innovation, putting laggards in the shade.

- However, issues such as integrating digital banking platforms with legacy systems, network outages, and security concerns can cause banks severe losses, and thus such factors might hamper the growth of the market.

- As a result of the COVID-19 crisis, there was a rise in online banking activity, such as increased digital transactions, and a decline in trips to brick-and-mortar branches. The pandemic forced individual consumers as well as corporations that once resisted online banking to adopt digital banking apps as their new default. The pandemic resulted in increased convenience among consumers, which might grow demand in the long run. On the vendors part, the majority of the vendors have been concentrating on customer acquisition by providing services demanded by the challenging times.

Digital Banking Platform Market Trends

Increasing Adoption of Cloud-Based Platforms to Boost the Market Growth

- In January 2023, the digital bank in the Philippines, GoTyme Bank, collaborated with the worldwide cloud banking platform Mambu to create an innovative digital banking solution that seeks to increase Filipinos' access to high-quality financial services.

- Many banks prefer cutting the IT infrastructure cost needed for on-premise setup by leveraging cloud-based services, which enable them to deploy new products and scale infrastructure quickly, cater to a broader customer base with varied needs at a faster speed, and manage rapidly increasing real-time payments while ensuring compliance and security standards.

- As a subscription fee is paid to a SaaS provider, system maintenance costs and legacy technology issues are reduced. Rather than spending a small fortune on IT, SaaS provides banks with the ability to reallocate budgets so they can focus on innovation, customer satisfaction, and business growth.

- The use of the cloud has also helped mobile banking platforms offer a responsive user interface (UI) and support the bank customers' entire banking journey, right from onboarding to transactional banking requests, on their mobile devices. Banks are rapidly adopting mobile banking platforms, owing to their changing preference toward mobile banking.

- Moreover, increased adoption of third-party applications for real-time payments, such as Whatsapp Pay and PhonePay, has led to increased demand for reliable infrastructure by the banks to carry out UPI transactions smoothly. For instance, Visa recently completed a USD 5.3 billion acquisition of Plaid, a fintech startup that allows applications to connect with customers' bank accounts easily and instantly. Technological shifts such as these have led to increased demand for cloud infrastructure in the digital banking industry.

North America is Expected to Hold Major Share

- Many of the biggest banks are in North America, which is a big reason why the market for digital banking platforms is growing. Digital banking companies in the region offer software as a service so that legacy systems can be turned into digital ones. For instance, Temenos helps new U.S. digital banks go live in 90 days with the most functionally rich and technologically advanced front-to-back SaaS digital banking offering.

- Digital banking platforms are becoming more popular as blockchain technology, which makes security better, is used more and more, especially in the BSFI sector. This factor is fueling the market's growth in the country. Many companies are developing blockchain-based cloud digital banking platforms.

- North America is also one of the most innovative and first places to use the cloud. Cloud infrastructure providers have a strong foothold in the region, which helps the market grow even more.

- The steady rise in the use of digital banking platforms follows a similar rise in the use of fintech apps, which are notable for being one of the fastest-growing types of apps in the US. Due to the global coronavirus (COVID-19) pandemic, people in the United States stayed at home more and used their phones more. This led to more digital banking across the region.

Digital Banking Platform Industry Overview

The market for digital banking platforms is moving toward fragmentation. This is because of the entry of companies and solutions into the market, creating a fragmented landscape within the digital banking ecosystem. However, with technological advancements and product innovation, midsize to smaller companies are increasing their market presence by securing new contracts and partnerships.

In January 2023, Axis Bank collaborated with OPEN to provide its clients, who include SMEs, freelancers, homepreneurs, influencers, and others, with a completely native digital current account. This collaboration gives the larger business community access to Axis Bank's comprehensive banking experience and OPEN's end-to-end financial automation capabilities for business administration, such as payments, accounting, payroll, compliance, expenditure management, and other services.

In November 2022, Capco and Savana announced that they would work together in a strategic way to speed up the transformation of banks and drive continuous innovation in digital products. This partnership will support banks in overcoming the technical challenges they face in meeting evolving customer expectations and needs for seamless modern omnichannel experiences.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Increasing Adoption of Cloud-Based Platforms to Obtain Higher Scalability

- 4.4.2 Rising demand for smart mobile devices and digital banking services among consumers

- 4.5 Market Restraints

- 4.5.1 Increasing Security Concerns

- 4.6 Assessment of Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.2 By Type

- 5.2.1 Corporate Banking

- 5.2.2 Retail Banking

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Asia Pacific

- 5.3.3 Europe

- 5.3.4 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Appway AG

- 6.1.2 CREALOGIX Holding AG

- 6.1.3 EdgeVerve Systems Limited

- 6.1.4 Fiserv, Inc.

- 6.1.5 Oracle Corporation

- 6.1.6 SAP SE

- 6.1.7 Sopra Steria

- 6.1.8 Tata Consultancy Services Limited

- 6.1.9 Temenos Headquarters SA

- 6.1.10 Worldline SA

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

數位銀行平台市場:分析與預測(至 2035 年)-按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能和解決方案分類

數位銀行平台市場:分析與預測(至 2035 年)-按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能和解決方案分類 2026年全球數位銀行平台市場報告

2026年全球數位銀行平台市場報告 全球數位銀行平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球數位銀行平台市場規模、佔有率、趨勢和成長分析報告(2026-2034) 數位銀行平台市場規模、佔有率和趨勢分析報告:按部署方式、模式、組件、服務、類型、地區和細分市場預測(2026-2033 年)

數位銀行平台市場規模、佔有率和趨勢分析報告:按部署方式、模式、組件、服務、類型、地區和細分市場預測(2026-2033 年) 數位銀行平台市場規模、佔有率和成長分析(按類型、組件、銀行模式、部署類型和地區分類)-2026-2033年產業預測

數位銀行平台市場規模、佔有率和成長分析(按類型、組件、銀行模式、部署類型和地區分類)-2026-2033年產業預測 數位銀行平台市場預測至2032年:按組件、部署模式、組織規模、功能、最終用戶和地區分類的全球分析數位銀行平台全球市場:2034 年市場機會與策略全球數位銀行平台市場:按模式、部署、組件、類型、地區、範圍和預測

數位銀行平台市場預測至2032年:按組件、部署模式、組織規模、功能、最終用戶和地區分類的全球分析數位銀行平台全球市場:2034 年市場機會與策略全球數位銀行平台市場:按模式、部署、組件、類型、地區、範圍和預測 數位銀行平台市場報告:2030 年趨勢、預測與競爭分析

數位銀行平台市場報告:2030 年趨勢、預測與競爭分析