|

市場調查報告書

商品編碼

1644367

拉丁美洲資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Latin America Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

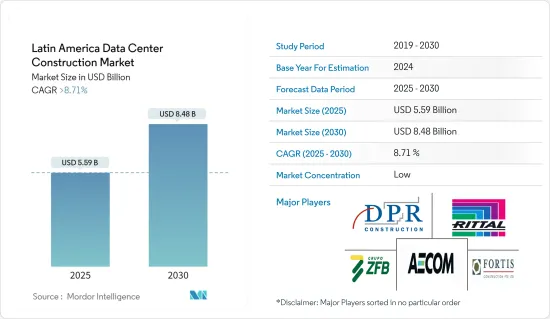

拉丁美洲資料中心建設市場規模預計在 2025 年為 55.9 億美元,預計到 2030 年將達到 84.8 億美元,預測期內(2025-2030 年)的複合年成長率將超過 8.71%。

軟體定義資料中心、物聯網(IoT)、災難復原等新興技術的成長推動了拉丁美洲對資料中心建設的需求。

主要亮點

- 建立資料中心是一項非常複雜的工作,需要對電氣、位置和機械要求進行廣泛的規劃。此外,由於資料中心執行任務,不良的電源管理和建築設計可能導致災難性的後果,給企業帶來巨大損失。

- 近年來,隨著雲端服務的普及,數位基礎設施的成長以及對資料中心的需求也日益增加。在此期間,資料中心可用的儲存量有限,限制了雲端服務的擴展。

- 隨後,超大規模和資料資料的概念出現了。超大規模和主機託管資料資料的資料預計將推動未來資料中心建置的需求。

- 行動裝置和高速寬頻連線的快速普及正在推動拉丁美洲資料中心建設市場的成長。此外,對連網型設備的需求不斷成長以及物聯網、雲端基礎的服務和巨量資料分析等新技術的採用正在推動該地區對新設施的需求。

- 2023 年 9 月,超大規模市場領先的拉丁美洲永續資料中心平台之一 Saala Data Centers 宣布成為 Datacloud USA 2023 的獨家永續性合作夥伴。與 Datacloud USA 的合作加強了其永續舉措,並凸顯了 Scala 在拉丁美洲超大規模永續資料中心的發展。

- 預計在預測期內,包括巴西在內的拉丁美洲國家對新資料中心建設的投資增加將推動市場成長。作為與管理系統供應商 Sankhya 合作擴張的一部分,巴西現代技術機構 (AMT) 選擇 CenturyLink 為其里約熱內盧提供資料中心服務,以滿足日益成長的雲端服務需求。 CenturyLink 位於里約熱內盧的模組化資料中心為客戶提供了旨在提供高可用性、更高品質和更快速存取世界其他地區的處理環境。

- 儘管遭遇新冠疫情危機,拉丁美洲對資料中心和先進資訊處理結構的投資仍在加速。在這個市場,各家公司都宣布了建造資料中心的措施。

拉丁美洲資料中心建設市場趨勢

IT和通訊領域佔據了很大的市場佔有率

- 該地區正吸引來自 IT 和通訊供應商的大量投資。事實證明,大規模採用數位科技可以透過各種管道有效減少家庭層面的收入不平等,包括提高連結性和數位服務的可及性。數位金融服務克服了資格和負擔能力障礙,使企業能夠為人們提供安全可靠的儲蓄、借貸和防範風險的方式。

- 雲端處理、物聯網服務和巨量資料的大規模採用,以及對社交網路和線上視訊服務日益成長的需求,正在推動該地區的通訊服務供應商建立網路主幹網路。谷歌已將其海底電纜「居里」停靠在智利瓦爾帕萊索。這條電纜直接連接到位於加州洛杉磯的 Equinix LA4資料中心。預計約有 10 個海底電纜計劃將推動資料中心投資與前一年同期比較。

- 拉丁美洲的資料中心設計能夠承受高機架密度。 IT基礎設施利用率的提高使得拉丁美洲資料中心的機架功率密度達到平均4-6kW。對高效能運算 (HPC) 和虛擬等解決方案的需求不斷成長,將推動拉丁美洲資料中心建設市場的發展,預測期內機架功率密度將增加到 8-10 kW 之間。

- 拉丁美洲國家在強大數位經濟所需的幾個支柱方面擁有強勁前景。有意義的——安全、高效和負擔得起的——網際網路連接和資料訪問是數位經濟的基礎。併購也有助於提升拉丁美洲 IT 和電信公司的市場佔有率。

巴西可望佔據主導市場佔有率

- 雲端運算的擴張(由於 COVID-19 而進一步加速)、外國雲端供應商的不斷滲透、政府對資料安全的監管以及國內參與者的投資增加是推動該國資料中心需求的一些主要因素。該國大約有 120 個資料中心。

- 對低延遲和高效能的需求,加上最近由於全國封鎖而產生的在家工作文化,加速了將資料中心部署到更靠近客戶和企業的舉措,主要是為了實現混合多重雲端生態系統。

- 據巴西軟體協會(ABES)稱,巴西是拉丁美洲最大的技術生態系統。此外,根據Equinix發布的資料,拉丁美洲的IT支出與前一年同期比較增1.3%,預計未來幾年將成長4-5%。巴西在IT和通訊領域的投資預計分別達到400至500億美元左右。預計這將極大地激發雲端處理市場,並最終激發資料中心市場。

- 巴西政府在發展當地資料中心基礎設施方面也發揮著重要作用。據政府稱,該國的《通用資料保護法》(LGPD)即將生效,預計將迫使該國許多公司將雲端存取轉移到私人網路並更新其加密服務以加強用戶資料保護。

- 此外,COVID-19 也給終端用戶企業帶來了巨大壓力,迫使他們支援遠端工作,加快雲端運算數位化進程。 IBM 和微軟等公司聲稱,這將促進巴西的資料中心市場,因為資料中心的擴張將使組織和政府機構能夠透過合法的方式管理資料資料維護資料主權。

- 隨著合規性和保護條例不斷加強,巴西企業尋求資料獲得更大的控制權,IBM 等資料中心供應商正透過提供雲端功能以及混合多重雲端環境來瞄準客戶。

拉丁美洲資料中心建設產業概況

拉丁美洲資料中心建設市場分散且競爭激烈。該市場的主要企業包括 AECOM、Cisco、Kogan Corporation、DPR Construction、Holder Construction 和戴爾科技。這個市場對多種應用的差異化產品的需求日益成長,讓您透過技術創新創造永續的競爭優勢。透過研發、併購和策略聯盟,這些公司在市場上取得了更強的地位。這些參與者透過提供最尖端科技不斷擴大其市場佔有率,從而提高了其市場收益。

2022年11月,拉丁美洲資料中心市場領導者Ascenty宣布開始建造五個新設施,進一步鞏固了其在巴西、智利、墨西哥和現在的哥倫比亞總合33個基礎設施的領導地位。新的資料中心將位於聖地牙哥 3 號資料中心(面積 21,000 平方米,容量 16MW)、波哥大 1 號和 2 號資料中心(面積 9,000 平方米,容量 12MW)以及聖保羅 5 號和 6 號資料中心(面積 7,000 平方米,容量 19MW)。

2022 年 8 月,該地區超大規模市場領先的綠色資料中心平台 Scala Data Centers推出了拉丁美洲最大的垂直資料中心 SGRUTB04,總容量為 18 兆瓦。 SGRUTB04所在的坦博爾校區是該公司在巴西大聖保羅地區擁有的一棟綜合大樓。 SGRUTB04 將分配給單一超大規模客戶,預計將全面運作10 年以上。新的 Scala資料中心高五米,共有七層,其中四層為資料廳專用,總建築面積超過 140,000 平方英尺,擁有超過 1,500 個機架。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 該地區網路連接改善,數位轉型相關技術的採用增加

- 地方政府推出稅收優惠政策,吸引更多外資

- 領先的資料中心建設公司繼續整合以支持業務擴張

- 提高對模組化配置和增加機架密度的認知

- 市場挑戰(成本和基礎設施問題)

- 成本和基礎設施仍是問題

- 勞動力挑戰

- 市場機會

- 電力、冷凍和能源技術進步推動建設活動

- 對邊緣資料中心的需求不斷增加

- 巴西和墨西哥繼續成為該地區最大的市場

- COVID-19 對資料中心建設產業的影響

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 技術簡介

第5章 市場區隔

- 依基礎設施類型

- 電力基礎設施

- UPS 系統

- 其他電力基礎設施

- 機械基礎設施

- 冷卻系統

- 架子

- 其他機械基礎設施

- 一般建築

- 電力基礎設施

- 依層級類型

- 層級和二級

- 第三層級

- IV層級

- 按公司規模

- 中小型企業

- 大型企業

- 按最終用戶

- 銀行、金融服務和保險

- 資訊科技/通訊

- 政府和國防

- 衛生保健

- 其他最終用戶

- 按國家

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲國家

第6章 競爭格局

- 公司簡介

- Turner Construction Co.

- DPR Construction Inc.

- Fortis Construction

- ZFB Group

- Aceco TI

- AECOM Limited

- Constructora Sudamericana SA

- HostDime Brasil

- CyrusOne Inc.

- RITTAL Sistemas Eletromecanicos Ltda.(Rittal GmbH & Co. KG)

- Legrand

- Delta Group

- Ascenty Data Centers E Telecomunicacoes

- Equnix Inc.

第7章投資分析

第8章 市場機會與未來趨勢

The Latin America Data Center Construction Market size is estimated at USD 5.59 billion in 2025, and is expected to reach USD 8.48 billion by 2030, at a CAGR of greater than 8.71% during the forecast period (2025-2030).

The growth of advanced technologies such as software-defined data centers, the Internet of Things (IoT), and disaster recovery fed the demand for the construction of data centers in Latin America.

Key Highlights

- Data center construction is a very complex task requiring extensive planning of electrical, location, and mechanical requirements. Moreover, the data centers carry out mission tasks, due to which any imperfection in power management to building design could be catastrophic and could result in increased costs to the companies.

- The need for data centers has increased in recent years, with the growth of digital infrastructure due to the high adoption of cloud services. During that period, the widespread expansion of cloud services was restrained by the limited storage available at the data centers.

- Subsequently, the concept of hyperscale data centers and colocation data centers emerged. The construction of hyperscale data centers and colocations data centers is expected to drive the demand for data center construction in the future.

- The rapid proliferation of mobile devices and high-speed broadband connectivity is attributed to the growth of the data center construction market in the Latin American region. Moreover, the increasing demand for connected devices and the introduction of new technologies, such as IoT, cloud-based services, and big data analytics, are boosting the demand for new facilities in the region.

- In September 2023, Saala Data Centers, one of the leading Latin American platforms of sustainable data centers in the Hyperscale market, announced its role as the exclusive Sustainability Partner at Datacloud USA 2023. The collaboration with Datacloud USA reinforces sustainable initiatives and underscores scala's hyperscale sustainable data center evolution in Latin America

- The increasing investment in building new data centers in Latin American countries, such as Brazil, is expected to drive market growth over the forecast period. Brazilian company AMT (Agencia Moderna Tecnologia) selected CenturyLink to meet its growing demand for cloud services as part of business expansion with management systems provider Sankhya for data center services in Rio de Janeiro. The CenturyLink modular data center in Rio de Janeiro provides customers with a processing environment designed to offer high levels of availability, improved quality, and greater access speeds to the rest of the world.

- The investments in data centers and advanced information processing structures have accelerated in Latin America, despite the COVID-19 crisis. Various companies in the market have announced their moves for the construction of data centers.

Latin America Data Center Construction Market Trends

IT and Telecommunications Segment to Hold a Significant Share of the Market

- The region is undergoing some massive investment from IT & Telecom providers. Adoption of digital technology at a large scale has been demonstrated to have good effects on lowering income inequality at the household level through a variety of routes, including increased connection and access to digital services. Digital financial services assist companies in overcoming eligibility and affordability barriers and give people secure and dependable ways to save money, borrow money, and insure against risk.

- The massive adoption of cloud computing, IoT services, and big data, along with the growth in social networking and the need for online video services, has aided telecommunication service providers in the region to establish their internet backbone. Google docked its private submarine cable, Curie, in Valparaiso, Chile. The cable is directly joined to the Equinix LA4 data center in Los Angeles, California. About 10 submarine cable projects will yield high data center investments year-over-year.

- The data centers in Latin America are being designed to withstand high rack density. The increasing utilization of IT infrastructure has increased the rack power density to an average of 4-6 kW among data centers in Latin America. The growing need for solutions such as high-performance computing (HPC) and virtualization will continue to grow the rack power density between 8-10 kW during the forecast period, consequently driving the data center construction market in Latin America.

- Latin American nations have excellent prospects across several essential pillars of a strong digital economy. Access to a meaningful (safe, productive, and inexpensive) internet connection and data is the foundation of the digital economy. Owing to mergers and acquisitions, the increase in market share of IT & Telecom companies is also rising sharply in Latin America.

Brazil is expected to Dominate Market Share

- The growing cloud computing (further fuelled due to COVID-19), increasing penetration of foreign cloud vendors, government regulations for local data security, and increasing investment by domestic players are some of the major factors driving the demand for data centers in the country. There are almost 120 data centers in the country.

- The demand for low latency and high performance, along with the recent work-from-home culture due to nationwide lockdown, is mainly accelerating the adoption of data centers near customers and businesses to enable hybrid multi-cloud ecosystems.

- According to the Brazilian Software Association (ABES), Brazil is Latin America's largest technology ecosystem. Also, according to the data published by Equinix, the IT investment in Latin America witnessed a 1.3% growth in previous years and is expected to have an upswing of 4-5% in the coming years. Brazilians' investment in the IT industry and telecom sector will be around USD 40-50 billion, respectively. This is expected to provide a massive boost to the cloud computing market and hence to the data center market too.

- The Brazilian government is also playing a significant role in developing local data center infrastructure. According to the government, the country's General Data Protection Act (LGPD) will implement, which is expected to force many enterprises in the country to migrate their cloud access to private networks and update their encryption services to extend user data protection.

- Furthermore, COVID-19 put high pressure on end-user companies to support remote working and are fast-tracking their cloud and digitization journeys. Companies like IBM and Microsoft claim that this will boost the data center market in the country as data center expansion enables organizations and government institutions to uphold data sovereignty by keeping data within their legal basis.

- As companies in Brazil look to gain greater control of their data in the face of upcoming tighter compliance and protection regulations, data center vendors, like IBM, are targeting customers by providing cloud capabilities along with a hybrid multi-cloud environment.

Latin America Data Center Construction Industry Overview

The Latin America Data Center Construction Market is fragmented, and the competitive rivalry is high. The key players in this market are AECOM, Cisco Systems, Inc., Corgan Inc., DPR Construction, Holder Construction Company, and Dell Technologies Inc., among others. Sustainable competing advantage can be accomplished through innovation in this market, owing to the increasing need for differentiated products for multiple applications. Through research & development, mergers & acquisitions, and strategic partnerships, they have been able to gain a stronger hold in the market. These players are continually expanding their presence in the market by offering the most advanced technologies, thereby boosting their revenues in the market.

In November 2022, Ascenty, the market leader in Latin America for datacenters, announced the commencement of construction on five new facilities, further solidifying its dominance with a total of 33 infrastructures across Brazil, Chile, Mexico, and now Colombia. The new data centers are located in Santiago 3, with 21,000 m2 and 16 MW; Bogota 1 and 2, with 9,000 m2 and 12 MW each; and So Paulo 5 and 6, with an area of 7,000 m2 and a capacity of 19 MW each.

In August 2022, The largest vertical data center in Latin America, SGRUTB04, with a total capacity of 18MW, was launched by Scala Data Centers, the region's top platform for environmentally friendly data centers in the hyperscale market. The Tambore Campus, a complex owned by the firm in Greater So Paulo, Brazil, is where SGRUTB04 is situated. It is devoted to a single hyperscale client and will operate at full capacity for more than ten years. This new Scala data center is 5 meters tall, has seven floors, four of which are dedicated to data halls, and has a total built-out space of over 140,000 square feet, or more than 1,500 racks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Network Connectivity and Increased Adoption of Digital Transformation Related Technologies in the Region

- 4.2.2 Favorable tax Incentive Structure Introduced by Local Governments has Led to the Higher Participation from International Players

- 4.2.3 Ongoing Consolidation Efforts by Major Data Center Construction Companies to Aid their Expansion Activities

- 4.2.4 Growing Awareness on Modular Deployments and Increasing Rack Density

- 4.3 Market Challenges (Cost and Infrastructural Concerns)

- 4.3.1 Cost and Infrastructural Concerns Continue to be a Concern

- 4.3.2 Workforce-Related Challenges

- 4.4 Market Opportunities

- 4.4.1 Technological Advancements in Power, Cooling & Energy Segments to Drive Construction Activity

- 4.4.2 Growing Demand for Edge Data Center Deployments

- 4.4.3 Brazil & Mexico to Continue their Emergence as the Largest Markets in the Region

- 4.5 Impact of COVID-19 on the Data center Construction Industry

- 4.6 Industry Attractiveness -Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Technology Snapshot

5 MARKET SEGMENTATION

- 5.1 Infrastructure Type

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 UPS Systems

- 5.1.1.2 Others Electrical Infrastructure

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

- 5.1.1 Electrical Infrastructure

- 5.2 Tier Type

- 5.2.1 Tier-I and II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

- 5.3 Size of Enterprise

- 5.3.1 Small and Medium-scale Enterprise

- 5.3.2 Large-Scale Enterprise

- 5.4 End User

- 5.4.1 Banking, Financial Services, and Insurance

- 5.4.2 IT and Telecommunications

- 5.4.3 Government and Defense

- 5.4.4 Healthcare

- 5.4.5 Other End Users

- 5.5 Country

- 5.5.1 Mexico

- 5.5.2 Brazil

- 5.5.3 Argentina

- 5.5.4 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Turner Construction Co.

- 6.1.2 DPR Construction Inc.

- 6.1.3 Fortis Construction

- 6.1.4 ZFB Group

- 6.1.5 Aceco TI

- 6.1.6 AECOM Limited

- 6.1.7 Constructora Sudamericana S.A

- 6.1.8 HostDime Brasil

- 6.1.9 CyrusOne Inc.

- 6.1.10 RITTAL Sistemas Eletromecanicos Ltda. (Rittal GmbH & Co. KG)

- 6.1.11 Legrand

- 6.1.12 Delta Group

- 6.1.13 Ascenty Data Centers E Telecomunicacoes

- 6.1.14 Equnix Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 2025年資料中心建置全球市場報告2025年資料中心解決方案全球市場報告

2025年資料中心建置全球市場報告2025年資料中心解決方案全球市場報告 資料中心建設市場按層級類型、基礎設施、最終用途和地區分類資料中心建置市場規模、佔有率和成長分析(按資料中心類型、基礎設施、層級類型、最終用途和地區)- 2025-2032 年產業預測

資料中心建設市場按層級類型、基礎設施、最終用途和地區分類資料中心建置市場規模、佔有率和成長分析(按資料中心類型、基礎設施、層級類型、最終用途和地區)- 2025-2032 年產業預測 2025-2033 年按建設類型、資料中心類型、層級標準、垂直產業和地區分類的資料中心建置市場報告

2025-2033 年按建設類型、資料中心類型、層級標準、垂直產業和地區分類的資料中心建置市場報告 資料中心建設,全球市場,2025-20292024-2032 年日本資料中心建置市場報告(依建設類型、資料中心類型、層級標準、垂直產業和地區)全球資料中心建立市場(按建設類型、層級標準、組織規模和最終用戶):未來預測(2025-2030)資料中心解決方案市場:按解決方案、按使用者類型、按產業 - 2025-2030 年全球預測

資料中心建設,全球市場,2025-20292024-2032 年日本資料中心建置市場報告(依建設類型、資料中心類型、層級標準、垂直產業和地區)全球資料中心建立市場(按建設類型、層級標準、組織規模和最終用戶):未來預測(2025-2030)資料中心解決方案市場:按解決方案、按使用者類型、按產業 - 2025-2030 年全球預測