|

市場調查報告書

商品編碼

1644484

亞太內容服務平台-市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Asia Pacific Content Services Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

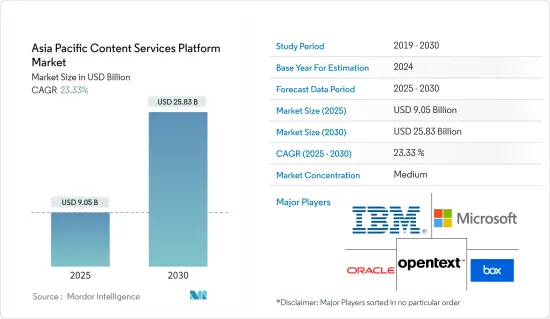

亞太內容服務平台市場規模預計在 2025 年為 90.5 億美元,預計到 2030 年將達到 258.3 億美元,預測期內(2025-2030 年)的複合年成長率為 23.33%。

由於中國和印度等開發中國家的資料流量不斷增加,以及需要組織的資料和資訊持續增加,預計亞太地區的市場將呈現指數級成長。

關鍵亮點

- 網路使用者數量的增加、中小企業數量的增加以及雲端服務供應商數量的增加為亞太地區帶來了巨大的成長機會。該地區的互聯頻寬也正在快速擴張。例如,根據 Equinix 的數據,受都市化進程加快的推動,亞太地區的網路容量預計將以每年 51% 的速度成長,佔全球互連頻寬的 27% 以上。

- 此外,對提供更好的客戶體驗的需求不斷成長、民眾對智慧技術的採用不斷增加、提供情境化用戶體驗的需求不斷成長以及跨多個業務的數位內容數量不斷增加都是推動市場發展的一些關鍵因素。此外,預測期內端到端跨平台解決方案的採用率不斷提高、RPA 和 CSP 解決方案的整合度不斷提高以及技術發展和服務現代化的進步將為亞太內容服務平台市場提供新的成長潛力和機會。

- 此外,行動、社群媒體、分析和雲端技術的日益普及,以及數位內容在各個企業的普及,正在加強該地區的內容服務平台產業。亞太地區的雲端運算應用正在快速成長,預計在預測期內對研究市場的成長產生正面影響。新加坡也是亞太地區雲端運算最發達的地區之一。在亞洲雲端運算協會(ACCA)最新發布的雲端運算就緒指數(CRI)中,中國超越香港,奪得榜首。此外,新加坡政府作為以更便宜、更快捷的方式提供公民服務的持續努力的一部分,預計將在預測期內將其大部分 IT 系統遷移到商業雲端服務,從而對市場成長產生積極影響。

- 然而,對資料隱私和安全的日益擔憂是阻礙市場成長的一個主要因素。此外,在整個預測期內,CSP 策略與組織策略舉措的不斷加強的協調也可能對內容服務平台市場構成額外的挑戰。

- COVID-19 疫情對市場研究產生了積極影響,因為人們已經轉向雲端基礎的技術,並且隨著維護和實施向員工的內容流的需求不斷增加,整個流程得到了增強。政府機構也被迫將業務電腦化數位化。例如在印度,Aarogya Setu 和國家電子健康局及新的遠端醫療指南等相關舉措正在共同建構國家健康堆棧,預計將於 2022 年完成。

亞太地區內容服務平台市場趨勢

解決方案軟體領域預計將佔據最大的市場佔有率

- 雲端運算徹底改變了資料儲存方式,並對文件管理系統產生了深遠的影響。亞太地區正迅速採用數位化文件管理,以盡量減少對紙張的依賴。此外,在中國等一些國家,降低人事費用、提高工作效率已成為企業管理的重要動機。

- 近日,海關總署啟動海關無紙化試驗改革,允許海關申報資訊透過電腦等多種電子媒體傳輸、儲存和自動審核。海關總署也大力推行價格審核通關單證無紙化,支持全國海關一體化改革,提升通關整體效率。此外,中國也越來越需要採用文件管理解決方案來遏制運輸和貿易領域的非法採伐,這預計將推動DMS的整體需求。

- 此外,印度日益成長的環境問題以及數位轉型和智慧設備的廣泛應用正在推動印度走向無紙化並迅速採用文件管理解決方案。印度政府的關鍵部門正在全部或部分遷移到離線-線上文件管理系統。最近,印度人民院宣布議會將無紙化辦公,以節省樹木和削減成本,議員現在使用數位文件來撰寫議題。出於安全原因,印度的教育機構也採用了文件管理解決方案。例如,印度教育機構馬尼帕爾高等教育學院(MAHE)已轉向無紙化文件管理系統,以更有效地管理和組織記錄和資訊並儲存資料。

- 此外,在日本等國家,由於人口減少和老化,人們越來越關注生產力和勞動力短缺,從而刺激了各領域的數位化。此外,日本政府計劃在2026年日本新國立檔案館開放時將大部分公共文件轉為數位化管理,目的是防止限制政府整體發展的記錄管理問題。此外,澳洲比其他亞太國家更早獲得無紙化辦公室的支持。例如,澳洲稅務局(ATO)於2002年認可了數位化申報。它建立了一套稅務法規,為電子記錄保存提供指導方針。

- 此外,由澳洲政府理事會(COAG)醫學委員會核准的《國家數位健康戰略》優先消除醫療保健產業的紙本通訊。該部門一直在與軟體產業和醫療保健提供者合作制定標準,以改善醫療資訊的安全交換。該系統使個人和客戶受益,因為它避免了向五個不同的人反覆解釋病情的麻煩,並允許醫療專業人員安全、快速地共用資訊。

IT、電訊、零售和電子商務產業將快速成長

- 通訊產業正在經歷重大結構性變革,包括內容、客戶管道和通訊服務的數位化,以及新的價值生態系統的形成。在當今數位時代,各種供應商都在建立高效能網路以滿足客戶的需求。這些結構性變化為該領域的工作流程管理服務創造了新的機會。隨著網路技術和設備越來越強大,市場上不同物聯網內容服務平台的範圍也不斷擴大。根據GSMA預測,到2026年,物聯網和綜合電力廣域網路的早期採用預計將產生總計1.8兆美元的收入。

- 隨著數位轉型的實施和擁有,很大一部分是由IT部門廣泛推動的。隨著資料連接性的提升,供應商正在廣泛地將雲端和基於物聯網的內容服務平台引入企業,以幫助他們管理和創建網路內容。 CMS 還允許您追蹤和管理網路流量,包括訪客活動和搜尋。

- 此外,Archive One 是一款文件管理軟體,可自動搜尋、保護、分類和儲存重要文檔,並充當審核工具。這在 IT-BPM 領域非常有用,因為該領域通常有數千名員工和大量資料需要追蹤。此外,Paperless Trail Inc. 強調接受商業新常態以及有效地將文件管理和合規性轉變為數位空間的重要性,以應對組織因技術進步而面臨的挑戰。

- 市場正看到銷售交易正在進行中,主要在亞太地區,涉及雲端、內部部署和混合模型。例如,2021年7月,Tech 資料和Cinity在亞太地區建立了新的經銷合作夥伴關係。該合作夥伴關係將使亞太地區的企業能夠以多種方式部署 Syniti 資料複製,包括雲端、本地和混合模式。

- 此外,Syniti 資料複製是一種低感性、靈活的解決方案,可為資料倉儲、分析和其他應用程式提供一致的資料副本,而不會中斷業務關鍵型系統的回應能力。其多功能的變更資料擷取(CDC) 可確保業務資料更新,以支援即時效能報告和分析系統。這將有助於企業加強資料和分析能力並實現大規模的行銷舉措。

亞太內容服務平台產業概覽

亞太地區內容服務平台市場整體分化程度適中,微軟公司、IBM 公司、甲骨文公司、OpenText 公司等少數幾家參與企業佔據了相當大的市場佔有率。這些公司正在利用各種策略創新和合作措施來提高盈利和最大限度地擴大市場佔有率。預計企業廣泛採用數位內容將顯著擴大所審查的市場。

- 2022 年 3 月-Adobe 宣布全面推出 Adobe Experience Cloud for Healthcare,可協助醫療保健公司提供客製化、安全的數位體驗和無縫的客戶旅程。

- 2021 年 9 月 - Intalio 宣布與 On-OneTech (Pty) Ltd 建立合作夥伴關係,將其地理範圍擴大到非洲。該合作夥伴關係將使 Intalio 能夠向非洲醫療保健行業銷售產品並為其提供支持,並改變整個非洲的醫療保健組織,從而提供超出其主要市場的更廣泛的地理覆蓋範圍。

- 2021 年 7 月-安永和 IBM 宣佈建立增強的全球多年期聯盟,主要旨在協助組織推動數位轉型並改善客戶成果。此次合作將包括利用 Red Hat OpenShift、IBM Watson、IBM Blockchain 以及 IBM 的 5G 和邊緣技術的各種混合雲端功能。我們的專家將共同致力於幫助客戶業務。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

第5章 市場動態

- 市場促進因素

- SMAC 技術的應用日益廣泛

- 企業數位內容的興起

- 情境化使用者體驗的需求

- 市場限制

- 資料隱私和安全問題

第6章 市場細分

- 按組件

- 解決方案/軟體

- 文件和記錄管理

- 資料擷取

- 工作流程管理

- 資訊安全與管治

- 案件管理

- 其他解決方案

- 按服務

- 解決方案/軟體

- 依實施類型

- 本地

- 雲

- 按組織規模

- 中小型企業

- 大型企業

- 按最終用戶產業

- BFSI

- 政府及公共機構

- 醫學生命科學

- IT、通訊、零售、電子商務

- 運輸和物流

- 其他

- 按國家

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

第7章 競爭格局

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- OpenText corporation

- Box Inc.

- Oracle Corporation

- Hyland Software Inc.

- Laserfiche Inc.

- Hewlett Packard enterprise(Micro Focus)

- Adobe Systems Inc.

- M-Files Inc.

第8章投資分析

第9章:市場的未來

The Asia Pacific Content Services Platform Market size is estimated at USD 9.05 billion in 2025, and is expected to reach USD 25.83 billion by 2030, at a CAGR of 23.33% during the forecast period (2025-2030).

In the Asia Pacific region, the market is expected to witness exponential growth, owing to increasing data traffic and continously growing data and information that requires to be organized in economically developing countries, such as China and India.

Key Highlights

- The rising growth of Internet-connected users, with a growing number of SMEs and cloud service vendors, provides significant growth opportunities in the Asia Pacific region. The interconnection bandwidth is also accelerating drastically in the region. For instance, according to Equinix, the Asia Pacific region is expected to expand by 51% per annum, accounting for over 27% of interconnection bandwidth globally, owing to a rise in urbanization.

- In addition, the rising demand to provide better customer experience, as well as rising usage of smart technologies among the population, growing need for delivering contextualized user experience, and rise in the of digital content across several enterprises, are among the vital factors enhancing the market. Moreover, during the projection period, rising adoption of end-to-end, cross-platform solutions, rise in the integration of RPA with CSP solutions, and growing technological developments and modernization in the services will offer new growth possibilities and apportunities for the market for Asia Pacific content services platform.

- Further, the rise in the adoption of mobile, social media, analytics, cloud technologies and the proliferation of digital content across various companies are enhancing the content services platform industry in the region. Cloud adoption in the Asia Pacific region is growing at a very rapid pace, which is anticipated to impact the growth of the market studied positively over the forecast period. In addition, Singapore is one of the most cloud-ready regions within the Asia-Pacific region. It overtook the position of Hong Kong in the latest iteration of the Asia Cloud Computing Association's (ACCA) Cloud Readiness Index (CRI). Additionally, Singapore's government is expected to move the bulk of its IT systems to commercial cloud services over the projection period as part of ongoing efforts to provide citizen services in a cheaper and faster and way, thereby positively influencing the growth of the market.

- In contrast, rising data privacy and security related concerns are significant factors, among others impeding the market growth. Also, the continously increasing aligning of CSP strategy with the strategic initiatives of organizations may further challenge the content services platforms market throughout the forecasted time period.

- The COVID-19 pandemic impacted the market studied positively, as people move to the cloud- based technologies and the whole process was enhanced with the rising need to maintain and implement content flow to employees. Also, government bodies were forced to adopt electronic means of operations and digitalization. For instance, in India, Aarogya Setu and other allied initiatives, like the National e-Health Authority and new tele-medicine guidelines, are coalescing toward a National Health Stack, which is aimed to be completed by 2022.

APAC Content Services Platform Market Trends

The Solution and Software Segment is Expected to Accounted for the Largest Market Share

- Cloud computing has well revolutionized data storage in general and has a profound impact on document management systems, thus, ensuring that documents are well available at any time, anywhere, allowing for scalability, making it a solution for both large and small businesses. The Asia Pacific region is experiencing rapid adoption of digital management of documents to minimize its dependence on paper. Also, in a several few countries, such as China, it has resulted in cutting labor costs and fueled work efficiency, which are the significant motives to run businesses.

- In the recent times, China's General Administrative of Customs (GAC) launched the Paperless Customs Clearance Pilot Reform, enabling customs declaration information to be transferred and stored through computers and various other electronic media that can be reviewed automatically. GAC also had promoted paperless customs documents for price reviews to assist China's national customs clearance integration reform and improvise customs clearance's overall efficiency. Moreover, China has also been seeing an increased need to adopt document management solutions to curtail the illegal logging in the transport and trade sectors, which is anticipated to enhance the overall demand for DMS.

- Further, there have been rising environmental concerns in line with digital transformation and growing adoption of intelligent devices in India, which is enhancing the paperless trend in India and resulting in the quick adoption of document management solutions. Some of the key sectors of the Indian Government have either entirely or partially moved to Offline and Online Document Management Systems. In the recent times, Lok Sabha declared that the lower house has become paperless to save trees and cut costs, with Members of Parliaments utilising digital documents to write questions. Educational institutions in India have also been executing document management solutions for safety purposes. For example, Manipal Academy of Higher Education (MAHE), an educational institution in India, moved to a paperless document management system to manage and organize their records and information and to build up data more effectively.

- Also, the rising concern about productivity and the lack of labor with a shrinking and greying population in countries like Japan are fueling such nations toward digitalization in every sector. Additionally, the Japanese Government plans to shift toward digital management of most public records by the time the new National Archives of Japan building opens in 2026, aiming to prevent the record management problems that have restricted the overall growth of the Government. Moreover, Australia gained the support for a paperless way back than other Asia-Pacific countries. For instance, the Australian Taxation Office (ATO) affirmed its support of digital filing in 2002. It executed a series of Tax Rulings that would act as a guideline for electronic record keeping.

- Moreover, the National Digital Health Strategy, approved by all the territories and states through the Council of Australian Governments (COAG) Health Council, prioritizes eradicating paper-based messaging in the healthcare industry. The Agency has been operating with the software industry and healthcare providers in developing standards that will improvise the secure exchange of healthcare information. This system will benefit the individuals and the customers as it will avoid the frustration of repeatedly explaining their condition to 5 different people and allow healthcare professionals to share information securely and quickly.

IT, Telecom, Retail, and E-commerce Segment to Witness Fastest Growth

- The telecommunications industry is undergoing a significant structural change, with content, customer channels, and communication services becoming digital, thereby resulting in creating a new value ecosystem. In the modern digital era, various providers are executing high-performance networks to fulfill the needs of their customers. Such structural changes are building new opportunities for workflow management services in the entire sector. The increasing enhancement of networking technologies and devices also widens the scope for various IoT content service platforms in the market. As per GSMA, early adoption of power-wide area networks integrated with IoT is anticipated to create a total sum of USD 1.8 trillion by the year 2026.

- With the implementation and ownership of digital transformation, the majority of the digital transformation is widely driven by the IT sector. With the increased data connectivity, vendors are widely adopting cloud and IoT-based content service platforms into the business to assist in managing and creating web content. CMS also allows tracking and management of web traffic, including visitor activities and searches.

- Moreover, Archive One, a document management software that acts as an auditing tool by automatically retrieving, securing, classifying, and storing critical documents. It is highly useful in the IT-BPM sector, where companies typically employ thousands of people, giving them a great amount of data to track. Also, Paperless Trail Inc. emphasizes the importance of embracing the new normal in business and effectively moving document management and compliance to the digital space in response to the challenges organizations face owing to technological advancements.

- The market is seeing an APAC-focused distribution agreement catering to the cloud, on-premises, and hybrid models. For example, in July 2021, Tech Data and Syniti have formed a new distribution alliance in the Asia-Pacific region. The collaboration allows enterprises in the Asia-Pacific to deploy Syniti Data Replication in various ways, including cloud, on-premises, and hybrid models.

- Moreover, Syniti Data Replication, a low-touch, flexible solution that offers a consistent copy of data ready for data warehousing, analytics, and other applications while not interfering with the responsiveness of business-critical systems. Its diversified Change Data Capture (CDC) ensures that business data is kept updated to assist real-time performance reporting and analytics systems. This will help the businesses in terms of strengthening their data and analytics capabilities and enabling large-scale go-to-market initiatives.

APAC Content Services Platform Industry Overview

The entire Asia Pacific content services platform market is moderately fragmented, with few participants like Microsoft Corporation, IBM Corporation, Oracle Corporation, OpenText Corporation, etc., holding a significant market share. These firms are leveraging various strategic innovations and collaborative initiatives to expand their profitability and maximise their market share. The wide adoption of digital content across enterprises is anticipated to be a significant amplifier of the market studied.

- March 2022 - Adobe declared the general availability of Adobe Experience Cloud for Healthcare, a solution that empowers healthcare enterprises to offer secure digital experiences and seamless customer journeys with customised and secured digital experiences.

- September 2021 - Intalio declares its partnership with On-OneTech (Pty) Ltd to expand its geographic reach to Africa. This partnership will provide Intalio with a wider geographic reach to go beyond its key markets, with the ability to sell to and support the African healthcare industry and transform healthcare organizations across Africa.

- July 2021 - EY and IBM stated an enhanced, global, multi-year alliance primarily designed to help organizations boost their digital transformation and improve client outcomes, which include leveraging the various hybrid cloud capabilities of Red Hat OpenShift, as well as IBM Watson, IBM Blockchain, and IBM's 5G and edge technologies. Together, both the company's professionals may focus on helping the clients in modernizing and transforming their businesses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of SMAC Technologies

- 5.1.2 Increase of Digital Content Across the Enterprises

- 5.1.3 Demand for Delivering Contextualized User Experience

- 5.2 Market Restraints

- 5.2.1 Data Privacy and Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Solution/Software

- 6.1.1.1 Document and Records Management

- 6.1.1.2 Data Capture

- 6.1.1.3 Workflow Management

- 6.1.1.4 Information Security and Governance

- 6.1.1.5 Case Management

- 6.1.1.6 Other Solutions

- 6.1.2 Services

- 6.1.1 Solution/Software

- 6.2 By Deployment Type

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Organization Size

- 6.3.1 Small and Medium-sized Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Industry

- 6.4.1 BFSI

- 6.4.2 Government and Public Sector

- 6.4.3 Healthcare and Life Sciences

- 6.4.4 IT, Telecom, Retail, & E-commerce

- 6.4.5 Transportation and Logistics

- 6.4.6 Other End-user Industries

- 6.5 By Country

- 6.5.1 India

- 6.5.2 China

- 6.5.3 Japan

- 6.5.4 South Korea

- 6.5.5 Rest of Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Microsoft Corporation

- 7.1.3 OpenText corporation

- 7.1.4 Box Inc.

- 7.1.5 Oracle Corporation

- 7.1.6 Hyland Software Inc.

- 7.1.7 Laserfiche Inc.

- 7.1.8 Hewlett Packard enterprise (Micro Focus)

- 7.1.9 Adobe Systems Inc.

- 7.1.10 M-Files Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球內容服務平台市場報告

2026年全球內容服務平台市場報告 全球內容服務平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球內容服務平台市場規模、佔有率、趨勢和成長分析報告(2026-2034) 內容服務平台市場規模、佔有率和成長分析(按組件、企業規模、部署類型、業務功能、產業和地區分類)-2026-2033年產業預測

內容服務平台市場規模、佔有率和成長分析(按組件、企業規模、部署類型、業務功能、產業和地區分類)-2026-2033年產業預測 內容服務平台市場:按解決方案類型、部署模式、企業規模、垂直產業和授權類型分類 - 2025-2032 年全球預測多語言字幕服務市場按服務類型、語言對、文件格式、字幕類型、垂直行業和配銷通路分類 - 全球預測 2025-2030

內容服務平台市場:按解決方案類型、部署模式、企業規模、垂直產業和授權類型分類 - 2025-2032 年全球預測多語言字幕服務市場按服務類型、語言對、文件格式、字幕類型、垂直行業和配銷通路分類 - 全球預測 2025-2030 內容服務平台:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

內容服務平台:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)