|

市場調查報告書

商品編碼

1644499

印度老年生活市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)India Senior Living - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

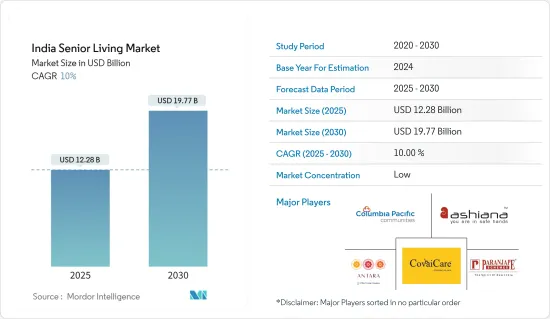

印度老年住宅市場規模預計在 2025 年為 122.8 億美元,預計到 2030 年將達到 197.7 億美元,預測期內(2025-2030 年)的複合年成長率為 10%。

關鍵亮點

- 人口老化正在推動市場發展。此外,老年生活社區提供的服務也正在推動市場的發展。

- 隨著老年人口的增加,老年人住宅需求將持續成長。隨著產業的發展,我們預計這些計劃提供的服務和設施類型將會增加。此類計劃目前已在各大城市興起。然而,從長遠來看,即使在郊區和層級城市,供應預計也將充足。層級城市包括比瓦迪、哥印拜陀、本地治裡、巴羅達、博帕爾、齋浦爾、邁索爾、德拉敦和卡索利。清奈、普納(拉瓦薩)和班加羅爾已開始提供供應。

- 此外,印度老年人口的不斷成長、預期壽命的延長、核心家庭數量的增加、經濟獨立且受過良好教育的老年人、老年人醫療需求的增加以及退休後返回印度的非居民印度人都是推動老年人住宅市場發展的一些因素。此外,南部城市佔據了全國老年住宅市場的大部分佔有率,其次是西部和北部。同時,班加羅爾、清奈奈、本地治里和海德拉巴是最受歡迎的南部退休定居城市,其次是德里國家首都轄區、昌迪加爾和德拉敦。在印度西部,孟買、普納、艾哈默德巴德、帕納吉和蘇拉特是最受歡迎的移民目的地。

- 印度是一個福利國家,在老年人問題上落後於已開發國家,制定了許多針對老年人的法律。根據印度統計和計畫實施部的報告,本會計年度印度老年人口數量將達到近1.394億人。此外,1961 年,5.6% 的印度人年齡在 60 歲或以上。官員表示,這一比率將在 2021 年上升至 10.1%,八年後達到 13.1%。

- 預計未來四到五年,大城市以外的老年住宅需求將增加兩倍以上。造成這種情況的原因如下:由於具有吸引的融資選擇、可用的土地和建造大型綜合體的充足空間,這些城市變得更具吸引力。老年人也喜歡開放的空間。雖然各地區的成長率有所不同,但大多數老年人越來越傾向於居住在人口密度較低的城市。老年人遷往人口密度較低的城市的趨勢也推動了這一成長。對於開發商來說,這是一個在競爭不那麼激烈的市場推出新計劃的機會。中長期市場預測表明,與大都市相比,這些市場將出現更多的老年生活社區。

印度老年住宅市場趨勢

加大對老年住宅領域的投資

新冠疫情讓印度人意識到了付費老人安養院的必要性,從而刺激了該國老年住宅市場的需求。此外,許多原本住在雙薪家庭的老人現在也選擇住在老人住宅。這兩個因素都增加了老人對多用戶住宅的需求。

為了滿足印度日益成長的老年人住宅需求,印度政府宣布了一項名為「Atal Vayo Abhyuday Yojana」(AVYAY)的 2021-2022 年計劃。根據該計劃,政府希望建立一個老年人健康、快樂、有權力、有尊嚴、獨立生活、擁有緊密社會和代際聯繫的社會。

根據 AVYAY 計劃,政府將投資超過 53 億印度盧比(6.4287 億美元)用於老年人福利。該預算將為老年人居住和健康計劃下的老年人投資超過 30 億印度盧比(3.6389 億美元),該計劃包括老年人綜合計劃(IPSrC)和老年人國家行動計劃(SAPSrC)計劃。

此外,IPSrC 旗下計劃還包括 25 個老人安養院、50 個老人安養院、持續照護之家、阿茲海默症/失智症老人安養院以及社區資源和培訓中心。該計劃已啟動180計劃計劃,惠及175,800名老年人。

南方可望實現成長

班加羅爾、清奈、科欽和哥印拜陀等印度南部城市正成為老年生活社區的中心,其次是該國西部和北部地區。這種成長得益於宜人的氣候條件、便利的交通和知名的醫療保健提供者的存在。此外,南方城市佔全國老年人住宅計劃的 70% 以上,其中包括獨立住宅、輔助住宅、輔助住宅和持續照護退休社區。

此外,2021年退休住宅開發商將透過買賣、租賃和混合模式(包括銷售和租賃)營運。例如,班加羅爾是印度採用購買模式的領先城市之一。同時,哥印拜陀和清奈等其他城市正在採用購買和租賃相結合的方式來滿足客戶需求。

在南部地區,售價在 400 萬盧比(48,518 美元)至 500 萬盧比(60,648 美元)之間的中型計劃佔據了銷售額的大部分。同時,高階計劃提供大型公寓和別墅,特別注重醫療保健、酒店和設計元素,以滿足老年人退休後享受舒適豪華生活的需要,這也促進了老年住宅市場的銷售成長。

印度老年住宅產業概況

印度老年住宅市場較為分散,許多本土企業進入市場。分散的參與企業之間的競爭非常激烈。此外,參與企業還透過合併、收購、策略夥伴關係以及推出新計畫來擴大業務,以滿足客戶需求。市場的主要參與企業包括 Antara Senior Care、Columbia Pacific Communities、Ashiana Housing Ltd、Paranjape Schemes (Construction) Ltd 和 Covai Property Centre (I) Pvt. Ltd。任何老年住宅計劃的成功在很大程度上取決於其提供的便利設施和設備。政府需要宣布具體措施,確保這項資產類別能為所有相關人員帶來成功。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 研究範圍

第2章調查方法

第3章執行摘要

第 4 章 市場考量與動態

- 市場概況

- 市場動態

- 市場促進因素

- 加大對老年住宅領域的投資

- 南部地區可望實現成長

- 市場限制

- 老年人缺乏經濟資源

- 缺乏對老化問題的認知與接受

- 市場機會

- 對醫療服務和產品的需求增加

- 提高技術採用率促進市場成長

- 市場促進因素

- 洞察養老生活領域的技術創新

- 政府法規和舉措

- 供應鏈/價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響

第5章 市場區隔

- 房產類型

- 支撐類型

- 自主型

- 記憶護理

- 護理

第6章 競爭格局

- 公司簡介

- AntaraSeniorCare

- Columbia Pacific Communities

- Ashiana Housing Ltd

- Paranjape Schemes(Construction)Ltd

- Covai Property Centre(I)Pvt. Ltd

- Oasis Senior Living

- Primus Lifespaces Pvt. Ltd

- The Golden Estate

- Vedaanta Retirement Communities

- Bahri Realty Management Services Pvt.Ltd

- Ananya's NanaNaniHomes

- Athashri*

第7章:市場的未來

第 8 章 附錄

The India Senior Living Market size is estimated at USD 12.28 billion in 2025, and is expected to reach USD 19.77 billion by 2030, at a CAGR of 10% during the forecast period (2025-2030).

Key Highlights

- The market is driven by the aging population. Furthermore, the services provided by the communities for senior citizens are driving the market.

- The demand for senior living housing will continue to rise as the population of seniors grows. As the industry grows, so will the types of services and amenities available in these projects. There has already been an increase in such projects in major cities. However, supply will be plentiful in suburbs and tier II cities in the long run. Tier-II cities include, among others, Bhiwadi, Coimbatore, Puducherry, Vadodara, Bhopal, Jaipur, Mysuru, Dehradun, and Kasauli. We have seen supply in Chennai, Pune (Lavasa), and Bengaluru.

- Furthermore, the senior living market is driven by the increasing aged population in the country, growth in life expectancy, rise in nuclear families, financially independent and educated senior citizens, increasing medical needs of the senior citizens, and NRIs coming back to India after retirement. Moreover, southern cities account for a major share of the senior living market in the country, followed by the west and north regions. Meanwhile, Bengaluru, Chennai, Puducherry, and Hyderabad are the most preferred southern cities for post-retirement settlement, followed by Delhi-NCR, Chandigarh, and Dehradun, which emerged as popular areas to settle in north India. Mumbai, Pune, Ahmedabad, Panaji, and Surat are some of the most opted retirement destinations in west India.

- Even though India is a welfare state and has several senior citizen-focused laws, it is still lagging behind developed nations in providing for its aged people. The Ministry of Statistics and Programme Implementation reported that there will be close to 139.4 million senior persons living in India in the current year. In addition, 5.6% of Indians were 60 years of age or older in 1961. This proportion rose to 10.1% in 2021 and is expected to reach 13.1% in eight years, according to official figures.

- It is anticipated that demand for senior living projects in non-metro cities will more than triple over the next four to five years. There are several reasons for this. These cities have become more appealing as a result of attractive financing options, the availability of land, and plenty of space to build sprawling complexes. And seniors appreciate the open spaces. Although growth rates vary by region, a growing trend indicates that the majority of seniors prefer to live in cities with low population densities. This growth is also being aided by the trend of seniors moving to cities with low population densities. It provides opportunities for developers to create new projects in less competitive markets. Predictions for the medium to long term market indicate that, when compared to metros, many more senior living communities would come up in these markets.

India Senior Living Market Trends

Increasing Investments in the Senior Living Sector

The COVID-19 pandemic made Indians realize the need for assisted-care homes, which increased the demand in the country's senior living market. In addition, many elders who stayed in joint families are now opting to live in senior living homes. Both these factors resulted in the demand for residential complexes for senior citizens.

To meet the increasing demand for senior living in the country, the Government of India announced a scheme called Atal Vayo Abhyuday Yojana (AVYAY) for 2021-2022. Under this scheme, the government offers a society where senior citizens live a healthy, happy, empowered, dignified, and self-reliant life, along with strong social and inter-generational bonding.

Under the AVYAY scheme, the government is investing more than INR 530 crore (USD 642.87 million) in the welfare of senior citizens. From this budget, more than INR 300 core (USD 363.89 million) are invested in seniors living under the Shelter and Health for Senior Citizens scheme, which includes the Integrated Programme for Senior Citizens (IPSrC) and State Action Plan for Senior Citizens (SAPSrC) programs.

In addition, the projects under IPSrC include Senior Citizen Homes 25, Senior Citizen Homes 50, Continuous Care Homes and Homes for senior citizens with Alzheimer's disease/ Dementia, and Regional Resource and Training Centers. More than 180 projects were initiated under this scheme, and 1,75,800 senior citizens benefit from these programs and projects.

The Southern Part of the Country is Expected to Witness Growth

Southern cities in India, such as Bengaluru, Chennai, Kochi, and Coimbatore, are emerging as hubs for senior living communities, followed by the western and northern regions. This growth is driven by pleasant climatic conditions, improved connectivity, and the presence of prominent healthcare providers. In addition, southern cities contribute to more than 70% of senior living projects in the country, which include communities such as independent living, assisted living, skilled or nursing care, and continuing care retirement communities.

Furthermore, in 2021, the developers of senior housing communities operated their businesses through outright purchases or sales, leases or rentals, and the hybrid model (includes both sales and leases). For instance, Bengaluru is one of the prominent cities in India that use the outright purchase model. In contrast, other cities such as Coimbatore and Chennai have a combination of outright purchases and leases to meet customer demand.

Most of the sales in the southern part are observed from medium-end projects, with prices ranging from INR 40 lakh (USD 48,518) to INR 50 lakh (USD 60,648). Meanwhile, high-end projects also contributed to the sales growth in the senior living sector by offering large apartments or villas with particular attention to healthcare, hospitality, and design elements for older adults looking to live in a comfortable and lavish lifestyle post-retirement.

India Senior Living Industry Overview

The Indian senior living market is fragmented, with many local players. There exists high competition among fragmented players. In addition, players expand their businesses using mergers, acquisitions, strategic partnerships, and new project launches to meet customer needs. Some of the major players in the market include AntaraSeniorCare, Columbia Pacific Communities, Ashiana Housing Ltd, Paranjape Schemes (Construction) Ltd, and Covai Property Centre (I) Pvt. Ltd. A senior housing project's potential success would mostly depend on the caliber of its amenities and facilities. The government will need to make specific policy announcements to ensure this asset class is successful for all parties.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increasing Investments in the Senior Living Sector

- 4.2.1.2 The Southern Part of the Country is Expected to Witness Growth

- 4.2.2 Market Restraints

- 4.2.2.1 Lack of financial resources available to seniors

- 4.2.2.2 Lack of awareness and acceptance of ageing related issues

- 4.2.3 Market Opportunities

- 4.2.3.1 Increasing demand for healthcare services and products

- 4.2.3.2 Increasing adoption of technology contributing to the growth of the market

- 4.2.1 Market Drivers

- 4.3 Insights into Technological Innovation in the Senior Living Sector

- 4.4 Government Regulations and Initiatives

- 4.5 Supply Chain/Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Property Type

- 5.1.1 Assisted Living

- 5.1.2 Independent Living

- 5.1.3 Memory Care

- 5.1.4 Nursing Care

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 AntaraSeniorCare

- 6.2.2 Columbia Pacific Communities

- 6.2.3 Ashiana Housing Ltd

- 6.2.4 Paranjape Schemes (Construction) Ltd

- 6.2.5 Covai Property Centre (I) Pvt. Ltd

- 6.2.6 Oasis Senior Living

- 6.2.7 Primus Lifespaces Pvt. Ltd

- 6.2.8 The Golden Estate

- 6.2.9 Vedaanta Retirement Communities

- 6.2.10 Bahri Realty Management Services Pvt.Ltd

- 6.2.11 Ananya's NanaNaniHomes

- 6.2.12 Athashri*

7 FUTURE OF THE MARKET

8 APPENDIX

2025年全球輔助生活科技市場報告

2025年全球輔助生活科技市場報告 美國老年生活:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)全球環境生活協助(AAL) -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030 年)

美國老年生活:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)全球環境生活協助(AAL) -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030 年) 2025-2029 年全球老年住宅市場2024 年老年生活全球市場報告

2025-2029 年全球老年住宅市場2024 年老年生活全球市場報告 環境生活協助市場:按產品類型、按應用、按最終用戶、按地區環境輔助生活市場 - 全球產業規模、佔有率、趨勢、機會和預測,按服務、技術、應用、地區和競爭細分,2019-2029F

環境生活協助市場:按產品類型、按應用、按最終用戶、按地區環境輔助生活市場 - 全球產業規模、佔有率、趨勢、機會和預測,按服務、技術、應用、地區和競爭細分,2019-2029F 環境生活協助市場:按技術、最終用戶、應用、產品類型、功能、用戶群、護理環境 - 2025-2030 年全球預測生活風格輔助科技市場:按類型、部署、最終用戶、技術、應用程式分類 - 2025-2030 年全球預測

環境生活協助市場:按技術、最終用戶、應用、產品類型、功能、用戶群、護理環境 - 2025-2030 年全球預測生活風格輔助科技市場:按類型、部署、最終用戶、技術、應用程式分類 - 2025-2030 年全球預測 全球生活輔助軟體市場

全球生活輔助軟體市場