|

市場調查報告書

商品編碼

1644937

歐洲大型風力發電機-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Large Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

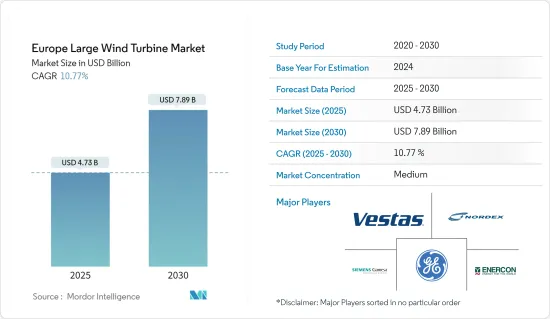

歐洲大型風力發電機市場規模預計在 2025 年為 47.3 億美元,預計到 2030 年將達到 78.9 億美元,預測期內(2025-2030 年)的複合年成長率為 10.77%。

關鍵亮點

- 從中期來看,預計風發電工程投資增加和政府優惠政策等因素將在預測期內推動歐洲大型風力發電機市場的發展。

- 然而,預計在預測期內,替代清潔電力來源(主要是天然氣和太陽能光伏)的採用將擴大阻礙歐洲大型風力發電機市場的需求。

- 預計預測期內,離岸風力發電計劃的發展將為歐洲大型風力發電機市場創造重大機會。

- 近年來,德國一直佔據大型風力發電機市場的主導地位。預計預測期內,風發電工程的增加加上政府的措施將推動市場顯著成長。

歐洲大型風力發電機市場趨勢

陸上市場佔據主導地位

- 過去五年來,陸上風電技術不斷發展,最大程度地提高了每兆瓦裝置容量的發電量並覆蓋了更多風速較低的地區。此外,近年來風力發電機轂高度增加,直徑增大,風力發電機葉片變得更大。

- 在歐洲,超過81%的新增風電位於陸上,總量約14.05吉瓦。瑞典、德國和土耳其正在建造最多的陸上風電裝置容量。 2022年,德國在新建風電場投資方面位居歐洲領先地位。同年,德國投資26億美元興建新風發電工程,全部用於陸域風電場。

- 過去的一年,瑞典陸上風電裝置數量與前一年同期比較增加了一倍多,創下了風電裝置數量的最高紀錄。瑞典目前是歐洲陸上風電裝置容量最大的國家,新增陸上風電裝置容量為2.1吉瓦。

- 2022年7月,瑞典宣布了計劃。三家公司將負責計劃:西門子歌美颯、Arise 和 Foresight,他們將在瑞典合作進行新計畫。

- 瑞典政府計劃在2030年將可再生能源在其電力結構中的比例提高到40%。政府宣布將把可再生能源支出從每年 54 億美元增加到 87 億美元。這很可能在預測期內促進大型風力發電機轉子市場的成長。

- 此外,根據歐洲風能協會預測,到2030年,陸上風力發電將引領歐洲市場需求,實現淨零碳排放。根據GWEC統計,陸上風力發電裝置容量約佔風力發電總量的90%。預計減少碳排放和逐步淘汰傳統電力系統的嚴格政府法規將推動市場發展。

- 因此,預計預測期內該地區的此類發展將支持大型風力發電機市場。

德國佔據市場主導地位

- 德國是風力發電領域的大國。離岸風力發電電場的興起,由於其風速比陸上風電場更快,創造了一個利潤豐厚的市場。因此,離岸風力發電預計將實現大幅成長。

- 此外,德國政府、沿海國家和輸電系統營運商(TSO)已就擴大北海和波羅的海上風電開發的聯合計劃達成一致,將該國的海上裝機容量目標提高到2030年的20GW。這將推動大型風力發電機市場的成長。

- 根據歐洲風能協會(WindEurope)的數據,截至 2021 年,歐洲風電裝置容量為 236 吉瓦。德國繼續擁有最大的裝置容量,其次是西班牙、英國、法國和瑞典。

- 截至年終年底,德國陸上風力發電機總數將達28,443台。此外,2022 年將安裝 551 台新的陸上風力發電機,容量為 2.4 吉瓦。陸域風電總設備容量5816千萬瓦。

- 2022年,歐盟風電發電量總合419.5兆瓦時。這比與前一年同期比較成長了約 8.4%。德國是歐盟成員國中風力發電量最多的國家,當年風力發電量約125兆瓦瓦。

- 2022年6月,德國議會通過了新的陸域風電法i.WindLandG,目標從2025年起每年開發10吉瓦的大型陸上風電場。這是德國所謂「復活節包裝」的一部分,將再生能源擴張是最高公共利益的原則納入法典。

- 因此,考慮到以上幾點,德國很可能在預測期內佔據市場主導地位。

歐洲大型風力發電機產業概況

歐洲大型風力發電機市場是半分割的。沼氣市場的主要企業(不分先後順序)包括 Vestas Wind Systems A/S、Nordex SE、Siemens Gamesa Renewable Energy SA、Enercon GmbH 和通用電氣公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 至2029年的市場規模及需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 加大對風發電工程的投資

- 政府優惠政策

- 限制因素

- 越來越多採用替代清潔電力來源

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場區隔

- 部署位置

- 土地

- 海上

- 地區

- 德國

- 法國

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Vestas Wind Systems A/S

- Nordex SE

- Siemens Gamesa Renewable Energy SA

- Enercon GmbH

- General Electric Company

- Suzlon Energy Limited

- Vensys Energy AG

- Xinjiang Goldwind Science & Technology Co., Ltd.

- JSC NovaWind

- Envision Energy

- Market Player Ranking

第7章 市場機會與未來趨勢

- 海上風力發電迅猛成長

簡介目錄

Product Code: 93219

The Europe Large Wind Turbine Market size is estimated at USD 4.73 billion in 2025, and is expected to reach USD 7.89 billion by 2030, at a CAGR of 10.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing investments in wind power projects and favorable government policies are anticipated to drive the Europe large wind turbine market during the forecast period.

- On the other hand, the growing adoption of alternate sources of clean power generation, mainly natural gas power and solar power is expected to hamper the demand for the Europe large wind turbine market during the forecast period.

- Nevertheless, the offoshore wind energy projects development are expected to create considerable opportunities for the Europe large wind turbine market during the forecast period.

- Germany is expected to dominate the large turbine wind market in recent years. It is expected to witness significant market growth in the forecast period due to the increasing wind energy projects coupled with the government's policies.

Europe Large Wind Turbine Market Trends

Onshore Segment to Dominate the Market

- Onshore wind energy power generation technology has evolved over the last five years to maximize electricity produced per megawatt capacity installed and to cover more sites with lower wind speeds. Besides this, in recent years, wind turbines have become more extensive with taller hub heights, broader diameters, and larger wind turbine blades.

- In Europe, over 81% of the new wind installations were the onshore wind, with around 14.05 GW. Sweden, Germany, and Turkey are building the most onshore wind installations. In 2022, Germany was the European leader in terms of investment in new wind farms. That year, Germany invested USD 2.6 billion in new wind projects, all of which went toward onshore wind installations.

- During the past year, Sweden has seen a record number of wind installations as onshore installations have more than doubled year-over-year. Sweden now has the most onshore wind capacity in Europe, with 2.1 GW of new onshore installations.

- In July 2022, a project was announced in Sweden to build a new 277 MW wind farm starting in 2025. Three companies will be in charge of the project; Siemens Gamesa, Arise and Foresight are likely to collaborate on a new project in Sweden.

- Sweden government has planned to increase the share of renewable energy in the power mix to 40% by 2030. The government announced an increase in the expenditure on renewables, from USD 5.4 billion to USD 8.7 billion annually. This, in turn, is likely to aid the growth of the large wind turbine rotor market during the forecast period.

- Furthermore, according to WindEurope, onshore wind energy will lead the market demand in the European region to achieve net-zero carbon emissions by 2030. According to GWEC, onshore wind energy capacity takes around 90% of the total wind energy. The strict government regulations to reduce carbon emissions and phase out conventional power systems are expected to drive the market.

- Thus, such developments in the region are expected to support the large wind turbine market during the forecast period.

Germany to Dominate the Market

- Germany is rich in wind power generation. Growing wind power plants in the offshore area are becoming a lucrative market due to higher wind speed in comparison to onshore wind. Thus, offshore wind-based electricity generation is expected to witness significant growth.

- Also, the German government, coastal states, and transmission system operators (TSOs) have agreed on a joint plan to expand offshore wind development in the North and Baltic Seas and lift the country's offshore installed capacity target to 20 GW by 2030. This in turn culminates in the growth of the large wind turbine rotor market.

- According to WindEurope, as of 2021, 236 GW of wind energy capacity is installed in Europe. Germany continues to have the largest installed capacity, followed by Spain, the United Kingdom, France, and Sweden.

- At the end of the year 2022, there were a total of 28,443 onshore wind turbines in Germany. Also, 551 new onshore wind turbines with a capacity of 2.4 GW were newly installed in the year 2022. The total installed capacity of onshore wind energy is 58.106 GW.

- The amount of electricity generated from wind power in the European Union (EU) totaled 419.5 terawatt hours in 2022. This was an increase of about 8.4 percent in comparison to the previous year. Among EU member states, Germany produced the most electricity from wind power, generating nearly 125 terawatt hours that same year..

- In June 2022, the German Parliament adopted a new Onshore Wind Law, i.e., WindLandG, which aims to develop onshore wind-based power plants by a massive 10 GW a year starting from 2025. It's part of Germany's "Easter Package" of measures that enshrines the principle that the expansion of renewables is a matter of overriding public interest.

- Therefore considering the above-mentioned points, Germany is likely to dominate the market during the forecast period.

Europe Large Wind Turbine Industry Overview

Europe Large Wind Turbine Market is semi fragmented. Some of the key players in the biogas market (not in particular order) include Vestas Wind Systems A/S, Nordex SE, Siemens Gamesa Renewable Energy S.A., Enercon GmbH, and General Electric Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Investments in Wind Power Projects

- 4.5.1.2 Favorable Government Policies

- 4.5.2 Restraints

- 4.5.2.1 The Growing Adoption of Alternate Sources of Clean Power Generation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Geography

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 Spain

- 5.2.4 NORDIC

- 5.2.5 Turkey

- 5.2.6 Russia

- 5.2.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems A/S

- 6.3.2 Nordex SE

- 6.3.3 Siemens Gamesa Renewable Energy S.A

- 6.3.4 Enercon GmbH

- 6.3.5 General Electric Company

- 6.3.6 Suzlon Energy Limited

- 6.3.7 Vensys Energy AG

- 6.3.8 Xinjiang Goldwind Science & Technology Co., Ltd.

- 6.3.9 JSC NovaWind

- 6.3.10 Envision Energy

- 6.4 Market Player Ranking

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Aggressive Growth of Offshore Wind Energy

02-2729-4219

+886-2-2729-4219

2024 年中國風力渦輪機訂單排名分析

2024 年中國風力渦輪機訂單排名分析 風力發電機監測系統市場:全球 2025-2029

風力發電機監測系統市場:全球 2025-2029 水平軸風力發電機市場規模、佔有率和成長分析(按類型、營運、應用和地區)- 產業預測 2025-2032

水平軸風力發電機市場規模、佔有率和成長分析(按類型、營運、應用和地區)- 產業預測 2025-2032 風力發電機退役服務市場,全球 2025-2029

風力發電機退役服務市場,全球 2025-2029 風力發電機市場分析及預測至 2033 年:依類型、產品、服務、技術、組件、應用、材料類型、安裝類型、設備、最終用戶

風力發電機市場分析及預測至 2033 年:依類型、產品、服務、技術、組件、應用、材料類型、安裝類型、設備、最終用戶 亞太大型風力發電機市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太大型風力發電機市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 北美大型風力發電機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美大型風力發電機:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2024 年陸域風力發電機全球市場報告

2024 年陸域風力發電機全球市場報告 風力發電機市場規模、佔有率、成長分析、按軸、按安裝、按連接性別、按輸出、按應用、按地區 - 行業預測,2024-2031 年

風力發電機市場規模、佔有率、成長分析、按軸、按安裝、按連接性別、按輸出、按應用、按地區 - 行業預測,2024-2031 年 風力發電機的美國市場的評估:各軸類型,安裝,各用途,各地區,機會,預測(2017年~2031年)

風力發電機的美國市場的評估:各軸類型,安裝,各用途,各地區,機會,預測(2017年~2031年)

▼