|

市場調查報告書

商品編碼

1645051

中東和非洲助焊劑 Stack -市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)Middle-East And Africa Frac Stack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

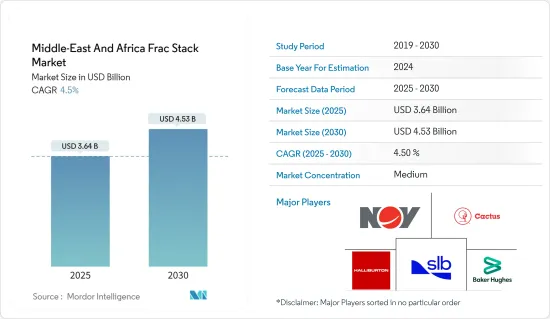

中東和非洲助焊劑市場規模預計在 2025 年為 36.4 億美元,預計到 2030 年將達到 45.3 億美元,預測期內(2025-2030 年)的複合年成長率為 4.5%。

關鍵亮點

- 從中期來看,預計非傳統資源產量增加和能源需求成長等因素將在預測期內推動助焊劑市場的發展。

- 同時,環境問題以及資本市場和獎勵的缺乏也限制了市場的成長。

- 隨著採用物聯網 (IoT) 分析探勘和生產 (E&P) 期間收集的大量資料,進階分析和模擬軟體在解決安全問題和提高水力壓裂過程效率方面變得越來越重要。水力壓裂作業中的巨量資料分析和物聯網系統可能為助焊劑堆疊市場創造巨大的商機。

- 由於頁岩氣的繁榮,沙烏地阿拉伯預計將成為最大的助焊劑設備市場。這導致頁岩蘊藏量的開發增加,而頁岩儲量需要壓裂才能實現經濟生產。

中東和非洲的助焊劑堆疊市場趨勢

陸上部門預計主導市場

- 受凸顯產業動態的幾個關鍵因素的推動,中東和非洲助焊劑市場預計將由陸上部門主導。這項優勢的關鍵催化劑之一是該地區大量的陸上石油和天然氣生產活動。

- 中東地區尤其擁有豐富的陸上蘊藏量,需要使用助焊劑堆疊來提高油井的產量。陸上計劃的可及性和成本效益對這一領域的持續成長貢獻巨大。

- 根據能源研究所《2023年世界能源統計評論》,該地區2022年的石油產量將達到約3,778.6萬桶/日,較2021年增加6%以上。隨著該地區水力壓裂活動的增加,預計產量也將同時增加。

- 此外,陸基作戰提供的後勤優勢對其優勢發揮了關鍵作用。陸上在運輸和基礎設施方面面臨的挑戰通常比海上少。這種物流的簡化意味著助焊劑堆疊的更有效率放置,從而降低了操作的複雜性和成本。隨著中東和非洲的石油和天然氣工業不斷擴張,陸上作業的實際優勢使這一領域成為助焊劑應用的中心位置。

- 此外,陸上採礦技術的進步和創新進一步增強了該領域的主導地位。水力壓裂和儲存管理技術的不斷改進,提高了陸上作業的效率,推動了對水力壓裂堆疊的需求。與不斷發展的採礦方法和水力壓裂堆疊的利用協同效應,使陸上部門鞏固了主導地位。

- 因此,許多公司將重點轉向開發非常規傳統型蘊藏量,例如頁岩氣和緻密氣,因為與大型海上計劃相比,這些儲備風險更低,所需資本投入也更少。預計在預測期內,傳統型陸上蘊藏物水力壓裂的增加將增加對助焊劑裝置的需求。

- 例如,2022 年 9 月,TAG Oil Ltd儲存了Badr Petroleum Company(“BPCO”)的一份石油服務契約,以開發 Badr 油田(“BED-1”)內的傳統型Abu Roash“F”油藏(“ARF”),該油田訂單埃及西部沙漠,佔地 107 平方公里(26,000 英畝)。

- 因此,鑑於上述情況,預計在預測期內陸上市場將佔據主導地位。

沙烏地阿拉伯:預計大幅成長

- 沙烏地阿拉伯作為全球石油生產國發揮關鍵作用,是石油和天然氣探勘和生產活動的中心樞紐。沙烏地阿拉伯豐富的陸上蘊藏量需要高效、先進的開採方法,而助焊劑堆疊已成為最佳化油井性能的關鍵組成部分。因此,強勁的陸上石油和天然氣產業是沙烏地阿拉伯在助焊劑市場佔據主導地位的主要原因。

- 例如,根據能源研究所《2023年世界能源評論》,沙烏地阿拉伯的天然氣產量從2021年到2022年增加了5.2%以上。預計 2022 年天然氣產量將達到 1,204 億立方米,而 2021 年為 1,145 億立方米,這表明該國石油和天然氣產業將成長,從而推動壓縮機市場的發展。

- 此外,沙烏地阿拉伯政府在其「2030願景」框架中提出的戰略舉措發揮關鍵作用。作為經濟多元化策略的一部分,該公司專注於加強陸上石油和天然氣業務,這與對助焊劑裝置的日益成長的需求相吻合。沙烏地阿拉伯為實現採礦工藝的現代化和最佳化所做的努力強化了人們的觀點:該國將有望在中東和非洲的助焊劑市場中佔據主導地位。

- 沙烏地阿拉伯的地理位置進一步增強了其在助焊劑市場的優勢。沙烏地阿拉伯位於中東和非洲地區的中心位置,擁有成本效益的運輸和物流,使陸上計劃對投資者更具可行性和吸引力。這項戰略定位有助於沙烏地阿拉伯在陸上石油和天然氣作業中有效部署助焊劑裝置,鞏固其在區域市場的領先地位。

- 此外,沙烏地阿拉伯對石油和天然氣領域技術進步和創新的關注與陸上開採方法日益複雜化相吻合。隨著營運商尋求更有效率、更永續的解決方案,對先進助焊劑堆疊的需求正在不斷成長。沙烏地阿拉伯致力於採用最尖端科技,這使其在中東和非洲的助焊劑堆疊市場中處於領先地位。

- 2023年5月,沙烏地阿拉伯石油巨頭阿美公司接受了石油精製巨頭中國石化和法國石油巨頭道達爾能源的提案,表示有興趣投資部分價值約100億美元的賈富拉頁岩氣開發計劃。中石化和道達爾能源公司正在就投資沙烏地阿拉伯賈富拉油田開發案的可能性進行單獨談判。沙烏地阿美採用創新的水力壓裂工藝,從附近的墨西哥灣沿岸抽水,預計到 2030 年,賈富拉氣田每天將生產約 20 億立方英尺的天然氣,總投資額為 240 億美元。

- 沙烏地阿拉伯法規環境的穩定性和可預測性進一步支持了其在助焊劑市場的優勢。穩定的法規結構將增強投資者信心並支持陸上石油和天然氣計劃的長期規劃。這種穩定性對於助焊劑市場持續成長至關重要,因為它使沙烏地阿拉伯營運商能夠實施結構化和可靠的部署策略。

- 因此,鑑於上述情況,預計沙烏地阿拉伯在預測期內將經歷顯著成長。

中東和非洲助焊劑堆疊產業概況

中東和非洲的助焊劑堆疊市場正在變得半固體。主要參與企業(不分先後順序)包括哈里伯頓公司、斯倫貝謝有限公司、NOV 公司、貝克休斯公司和 Cactus 公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 至2029年的市場規模及需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 提高非傳統資源產量

- 該地區能源需求不斷增加

- 限制因素

- 環境問題

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場區隔

- 部署位置

- 陸上

- 海上

- 井型

- 水平/偏差

- 按行業

- 2028 年市場規模與需求預測(按地區)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 其他中東和非洲地區

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Halliburton Company

- Schlumberger Limited

- NOV Inc.

- Baker Hughes Company

- Cactus Inc.

- National Energy Services Reunited Corp.

- Oil States International Inc.

- The Weir Group PLC

- SPM Oil & Gas Inc.

- Superior Energy Services Inc.

第7章 市場機會與未來趨勢

- 先進分析與模擬技術

簡介目錄

Product Code: 50001813

The Middle-East And Africa Frac Stack Market size is estimated at USD 3.64 billion in 2025, and is expected to reach USD 4.53 billion by 2030, at a CAGR of 4.5% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing production from unconventional resources and growing energy demand are expected to drive the frac stack market during the forecast period.

- On the other hand, environmental concerns and a lack of capital markets and incentives are restraining market growth.

- Nevertheless, with the adoption of the Internet of Things (IoT) to analyze a large amount of data collected during exploration and production (E&P), advanced analytics and simulation software have become increasingly important in addressing safety concerns and improving the efficiency of the fracking process. Big Data analytics and IoT systems in fracking operations are likely to lead to significant opportunities for the frac stack market.

- Due to the shale boom, Saudi Arabia is expected to be the largest market for frac stacks. This has led to increased exploitation of shale reserves that need to be fractured for economic production.

Middle-East And Africa Frac Stack Market Trends

The Onshore Sector is Expected to Dominate the Market

- The dominance of the onshore segment is anticipated in the Middle-East and African frac stack market, driven by several key factors that underscore the industry dynamics. One primary catalyst for this dominance is the considerable onshore oil and gas production activities in the region.

- The Middle East, in particular, hosts extensive onshore reserves, and the prevalent exploration and extraction operations necessitate the use of frac stacks to enhance well productivity. The accessibility and cost-effectiveness associated with onshore projects contribute significantly to the sustained growth of this segment.

- According to the Energy Institute Statistical Review of World Energy 2023, in 2022, the oil production in the region was around 37,786 thousand barrels per day, which was a growth of over 6% compared to 2021. As the fracking activities increase in the region, the production is expected to increase simultaneously.

- Additionally, the logistical advantages offered by onshore operations play a crucial role in their dominance. Onshore sites generally present fewer challenges in terms of transportation and infrastructure compared to offshore counterparts. This logistical ease translates into more efficient deployment of frac stacks, reducing operational complexities and costs. As the oil and gas industry in Middle-East and Africa continues to expand, the practical advantages associated with onshore operations position this segment as a focal point for frac stack utilization.

- Moreover, the technological advancements and innovations in onshore extraction techniques further bolster the dominance of this segment. Continuous improvements in hydraulic fracturing technologies and reservoir management techniques enhance the efficiency of onshore operations, driving the demand for frac stacks. The synergy between evolving extraction methods and frac stack utilization reinforces the onshore segment's leading position in the market.

- As a result, a number of operating companies have shifted their focus to the exploitation of unconventional onshore reserves, such as shale and tight gas reserves, which present lower risk and require a lower capital investment than large offshore projects. During the forecast period, there is expected to be an increase in the demand for frac stacks due to the increased hydraulic fracking of unconventional onshore reserves.

- For instance, in September 2022, TAG Oil Ltd was awarded a petroleum services contract by Badr Petroleum Company ("BPCO") to develop the unconventional Abu Roash "F" reservoir ("ARF") within the Badr Oil Field ("BED-1"), a 107 km2 (26,000 acres) concession located in the Western Desert of Egypt.

- Therefore, as per the points mentioned above, the onshore segment is expected to dominate the market during the forecast period.

Saudi Arabia is Expected to Witness Significant Growth

- The Kingdom's prominent role as a global oil producer positions it as a central hub for oil and gas exploration and production activities. Saudi Arabia's vast onshore reserves necessitate efficient and advanced extraction methods, with frac stacks emerging as crucial components to optimize well performance. The robust onshore oil and gas sector, therefore, contributes significantly to the expected dominance of Saudi Arabia in the frac stack market.

- For instance, according to the Energy Institute Review of World Energy 2023, gas production in Saudi Arabia increased by more than 5.2% between 2021 and 2022. In 2022, gas production was 120.4 bcm compared to 114.5 bcm in 2021, signifying the country's increasing oil and gas sector, which drives the compressor market.

- Furthermore, the strategic initiatives outlined in the Vision 2030 framework by the Saudi Arabian government play a pivotal role. As part of this economic diversification strategy, the focus on enhancing onshore oil and gas operations aligns with the growing demand for frac stacks. Saudi Arabia's commitment to modernizing and optimizing its extraction processes reinforces the notion that the country is poised to dominate the frac stack market in Middle-East and Africa.

- The geographical advantage of Saudi Arabia further enhances its dominance in the frac stack market. The country's central location in the region facilitates cost-effective transportation and logistics, making onshore projects more feasible and attractive for investors. This strategic positioning contributes to Saudi Arabia's ability to efficiently deploy frac stacks in its onshore oil and gas operations, solidifying its position as a frontrunner in the regional market.

- Additionally, Saudi Arabia's focus on technological advancements and innovation in the oil and gas sector aligns with the increasing complexity of onshore extraction methods. As operators seek more efficient and sustainable solutions, the demand for advanced frac stacks rises. The Kingdom's commitment to adopting cutting-edge technologies positions it at the forefront of the evolving frac stack market in the Middle East and Africa.

- In May 2023, Saudi Arabia's oil behemoth, Aramco, is receptive to proposals from refining giant Sinopec Corp and the French oil major TotalEnergies, considering their interest in investing in a portion of the Jafurah shale gas development project valued at approximately USD 10 billion. Both Sinopec and TotalEnergies are engaged in separate discussions regarding potential investments in the Jafurah development situated in Saudi Arabia. Leveraging an innovative fracking method utilizing seawater from the nearby Gulf coast, Saudi Aramco anticipates the Jafurah field to yield around 2 billion cubic feet of gas daily by 2030, with a projected total investment of USD 24 billion.

- The stability and predictability of Saudi Arabia's regulatory environment further support its dominance in the frac stack market. A stable regulatory framework enhances investor confidence and encourages long-term planning for onshore oil and gas projects. This stability is a crucial factor for the sustained growth of the frac stack market, as operators in Saudi Arabia can implement well-structured and reliable deployment strategies.

- Therefore, as per the above-mentioned points, the country is expected to witness significant growth during the forecasted period.

Middle-East And Africa Frac Stack Industry Overview

The Middle-East and African frac stack market is semi-consolidated. Some of the major players (in no particular order) include Halliburton Company, Schlumberger Limited, NOV Inc., Baker Hughes Company, and Cactus Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Production from Unconventional Sources

- 4.5.1.2 Growing Energy Demand in the Region

- 4.5.2 Restraints

- 4.5.2.1 Environmental Concerns

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Well Type

- 5.2.1 Horizontal and Deviated

- 5.2.2 Vertical

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Nigeria

- 5.3.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Halliburton Company

- 6.3.2 Schlumberger Limited

- 6.3.3 NOV Inc.

- 6.3.4 Baker Hughes Company

- 6.3.5 Cactus Inc.

- 6.3.6 National Energy Services Reunited Corp.

- 6.3.7 Oil States International Inc.

- 6.3.8 The Weir Group PLC

- 6.3.9 SPM Oil & Gas Inc.

- 6.3.10 Superior Energy Services Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advance Analysis and Simulation Technology