|

市場調查報告書

商品編碼

1651025

生質燃料-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Biofuels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

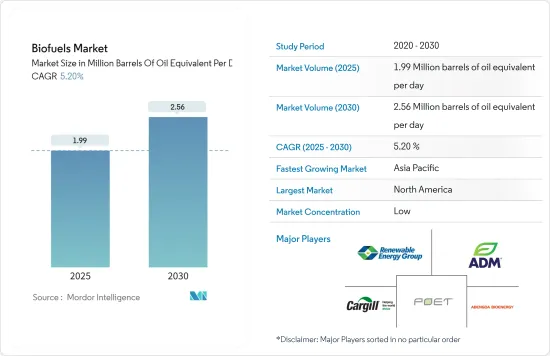

預計2025年生質燃料市場規模為199萬桶油當量/天,預估2030年將達256萬桶油當量/天,預測期間(2025-2030年)複合年成長率為5.2%。

關鍵亮點

- 從中期來看,對安全、永續、清潔能源的需求不斷成長,加上政府要求增加將生物燃料混合到機動車輛燃料中,預計將推動全球對生質燃料的需求。

- 另一方面,儘管生質燃料具有許多好處,生質燃料的高生產成本可能會抑制市場成長。

- 隨著近年來技術的進步,生質燃料產量正在上升,這代表著市場擴張的機會。

- 北美佔據市場主導地位,並可能在預測期內實現最高的複合年成長率。該地區的成長是由生產能力的快速成長和生質燃料需求的不斷成長所推動的。

生質燃料市場趨勢

乙醇:預期大幅成長

- 在全球範圍內,交通運輸業是內燃機燃燒石化燃料產生的溫室氣體最大的排放。為了限制溫室氣體排放,世界各國都在採取標準來促進可再生能源的使用。乙醇等生質燃料是運輸業的更清潔的能源來源,並可能在未來促進生質燃料市場的發展。

- 根據可再生燃料協會(RFA)預測,2022年,美國將生產1,540億加侖燃料乙醇,成為全球最大的生質燃料生產國。

- 全球對生質燃料的需求受到北美、印度、巴西、歐洲、印尼、馬來西亞和其他地區的主要混合義務的推動。例如,印度已規定到2025年乙醇混合物的含量為20%。在印度尼西亞,35%的生質柴油混合燃料計畫於 2023 年開始使用,而在巴西,現有的乙醇混合燃料規定為 27%。這些措施凸顯了各國日益廣泛的使用生質燃料。

- 此外,2022年3月,巴西經濟部宣布取消乙醇等產品的進口關稅,以緩解通膨壓力。預計此舉將鼓勵更多乙醇混合到汽油中,從而刺激市場。

- 2022年,SGP BioEnergy宣布將與巴拿馬政府合作,在巴拿馬開發全球最大的生質燃料分銷和生產中心,預計每日產能為18萬桶生質燃料。同樣,美國能源局已在 2023 年向 17 個計劃撥款 1.18 億美元,以擴大乙醇和其他生質燃料,滿足美國交通和製造業的需求。這些趨勢可能會促進生質燃料市場的發展。

- 因此,鑑於上述情況,預計預測期內乙醇部分將在生質燃料市場中見證顯著成長。

北美可望主導市場

- 北美是最大的航空市場之一,主要以石化燃料為動力,交通基礎設施發達。北美地區一直處於減少排放、抑制溫室效應的前線。

- 根據美國能源資訊署的數據,到 2022 年,美國生物柴油總產量將達到 16 億加侖。

- 2022年1月,美國環保署宣布了一項新舉措,旨在簡化對可大幅替代溫室氣體排放高的石化燃料的生質燃料和化學品的審查,為生質燃料市場提供重大推動力。同樣,美國能源局宣布,對2022年12月後安裝的使用天然氣、丙烷、液化氫、電力、E85或含有20 %或以上生物柴油的柴油混合物的加油設施,可享受30%的替代燃料基礎設施稅收抵免。預計此類激勵措施將促進生質燃料市場的發展。

- 同樣,加拿大政府計劃從2022年4月起將碳排放稅從每噸排放10美元提高到50美元,旨在鼓勵使用溫室氣體排放較低的生質燃料。

- 鑑於上述情況,由於政府措施和生產能力,北美很可能主導生質燃料市場。

生質燃料產業概況

生質燃料市場十分分散。主要企業包括(不分先後順序)Archer Daniels Midland Company、Abengoa Bioenergy SA、Renewable Energy Group Inc.、Cargill Incorporated、POET LLC。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 生質燃料生產歷史及 2028 年預測

- 生質燃料消費的歷史趨勢與 2028 年預測

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 對安全、永續和清潔能源的需求不斷增加

- 限制因素

- 生質燃料生產成本高

- 驅動程式

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 燃料類型

- 乙醇

- 生質柴油

- 其他燃料類型

- 原料

- 棕櫚油

- 痲瘋樹

- 糖料作物

- 粗粒

- 其他成分

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 丹麥

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 印尼

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Abengoa Bioenergy SA

- Cargill Incorporated

- Shell PLC

- Wilmar International Ltd.

- Renewable Energy Group Inc.

- Archer Daniels Midland Company

- BP PLC

- POET LLC

- Neste Oyj

- Verbio Vereinigte BioEnergie AG

第7章 市場機會與未來趨勢

- 生質燃料生產的技術進步

簡介目錄

Product Code: 49858

The Biofuels Market size is estimated at 1.99 million barrels of oil equivalent per day in 2025, and is expected to reach 2.56 million barrels of oil equivalent per day by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing demand for secure, sustainable, and clean energy coupled with government mandates for increasing blending in automotive fuels is expected to propel the demand for biofuels across the globe.

- On the other hand, the high cost of production of biofuels, even with all the benefits associated with them, is likely to restrain the growth of the market.

- Nevertheless, with the recent technological advancements, the production of biofuels has increased, which is going to act as an opportunity for the market's expansion.

- North America dominates the market, and it is likely to witness the highest CAGR during the forecast period. The growth is attributed to the rapid increase in production facilities coupled with the increase in demand for biofuels in the region.

Biofuels Market Trends

Ethanol Likely to Experience a Significant Growth

- Globally, the transportation sector is the biggest emitter of greenhouse gases due to the combustion of fossil fuels in its internal combustion engines. To limit the emission of greenhouse gases, countries worldwide have adopted norms to promote the use of renewable energy resources. Biofuels such as ethanol affirm themselves as a cleaner energy source for the transportation sector, which could lead to a developed biofuel market in the future.

- According to the Renewable Fuels Association (RFA), in 2022, the United States produced 15,4 billion gallons of fuel ethanol, making it the leading producer of biofuel in the world.

- Primary blending mandates that drive the global demand for biofuels are set in North America, India, Brazil, Europe, Indonesia, Malaysia, etc. For instance, in India, there is a mandate to begin 20% ethanol blending by 2025. In Indonesia, a commission of 35% biodiesel blending is expected to start in 2023, whereas in Brazil, the existing order for ethanol blending is 27%. Such measures highlight the increase in the use of biofuels across countries.

- Furthermore, in March 2022, Brazil's Ministry of Economy announced the withdrawal of import tariffs on ethanol, including other products, to alleviate inflationary pressures. This is expected to boost the ethanol blend in gasoline and drive the market.

- In 2022, SGP BioEnergy announced the development of the world's most extensive biofuel distribution and production hub in Panama, in association with the country's government, which is estimated to produce 180,000 barrels per day of biofuel. Similarly, in 2023, the US Department of Energy awarded USD 118 million for 17 projects to scale up ethanol and other biofuels to help America's transportation and manufacturing needs. Such trends are likely to ramp up the biofuel market.

- Therefore, owing to the above points, the ethanol segment is expected to experience significant growth in the biofuels market during the forecast period.

North America is Expected to Dominate the Market

- The North American region houses one of the biggest aviation markets, primarily fossil fuels, and a well-established transportation infrastructure. The North American region has been at the forefront of lowering emissions to limit the greenhouse effect.

- According to the U.S. Energy Information Administration, the total production volume of biodiesel production in the United States was 1.6 billion gallons by 2022

- In January 2022, the US Environmental Protection Agency announced a new initiative for streamlining the review of biofuels and chemicals that can significantly replace higher GHG-emitting fossil fuels, providing a significant push to the biofuels market. Similarly, the US Department of Energy announced an Alternative Fuel Infrastructure Tax Credit of 30% for the fueling equipment for natural gas, propane, liquefied hydrogen, electricity, E85, or diesel fuel blends containing a minimum of 20% biodiesel installed on or after December 2022. Such incentive measures would likely promote the biofuel market.

- Similarly, in Canada, the government aimed to increase carbon taxes by CAD 10 to CAD 50 per ton of emissions from April 2022, thereby pushing for wider adoption of biofuels that emit less GHG.

- Hence, owing to the above points, the North American region is likely to dominate the biofuels market due to government policies and production capacity.

Biofuels Industry Overview

The biofuels market is fragmented. Some of the major players include (in no particular order) Archer Daniels Midland Company, Abengoa Bioenergy SA, Renewable Energy Group Inc., Cargill Incorporated, and POET LLC., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Biofuel Production Historic and Forecast, till 2028

- 4.3 Biofuel Consumption Historic and Forecast, till 2028

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Increasing Demand for Secure, Sustainable, and Clean Energy

- 4.6.2 Restraints

- 4.6.2.1 High Cost of Production of Biofuels

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Ethanol

- 5.1.2 Biodiesel

- 5.1.3 Other Fuel Types

- 5.2 Feedstock

- 5.2.1 Palm Oil

- 5.2.2 Jatropha

- 5.2.3 Sugar Crop

- 5.2.4 Coarse Grain

- 5.2.5 Other Feedstock

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States of America

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Denmark

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Indonesia

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Abengoa Bioenergy SA

- 6.3.2 Cargill Incorporated

- 6.3.3 Shell PLC

- 6.3.4 Wilmar International Ltd.

- 6.3.5 Renewable Energy Group Inc.

- 6.3.6 Archer Daniels Midland Company

- 6.3.7 BP PLC

- 6.3.8 POET LLC

- 6.3.9 Neste Oyj

- 6.3.10 Verbio Vereinigte BioEnergie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Production of Biofuels

02-2729-4219

+886-2-2729-4219

2032 年下一代菸草市場預測:按產品類型、設備類型、組件、系統、最終用戶和地區進行的全球分析生質燃料市場規模、佔有率及成長分析(依燃料類型、發電方式、最終用途及地區)-2025-2032 年產業預測2030 年單細胞油市場預測:按微生物、等級、原料、應用和地區進行的全球分析

2032 年下一代菸草市場預測:按產品類型、設備類型、組件、系統、最終用戶和地區進行的全球分析生質燃料市場規模、佔有率及成長分析(依燃料類型、發電方式、最終用途及地區)-2025-2032 年產業預測2030 年單細胞油市場預測:按微生物、等級、原料、應用和地區進行的全球分析 全球生物燃料市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年全球運輸生物燃料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球生物燃料市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年全球運輸生物燃料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年先進生質燃料全球市場報告2025 年全球單細胞油市場報告2025年生質燃料測試服務全球市場報告B5 燃料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按原料、應用、地區和競爭細分,2020-2030F2025 年廢油全球市場報告

2025 年先進生質燃料全球市場報告2025 年全球單細胞油市場報告2025年生質燃料測試服務全球市場報告B5 燃料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按原料、應用、地區和競爭細分,2020-2030F2025 年廢油全球市場報告

▼