|

市場調查報告書

商品編碼

1683127

生物乙酸市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Bio-Acetic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

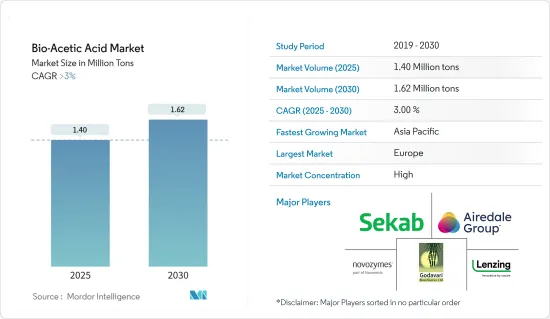

生物乙酸市場規模預計在 2025 年為 140 萬噸,預計在 2030 年達到 162 萬噸,預測期內(2025-2030 年)的複合年成長率將超過 3%。

2020 年,生物乙酸市場受到 COVID-19 的不利影響。受疫情影響,建設活動和汽車製造活動暫停,導致對用於配製黏合劑、油漆、被覆劑、塑膠、複合材料等終端用戶工業產品的醋酸乙烯單體的需求減少,從而對生物乙酸的市場需求產生負面影響。不過,隨著各產業恢復生產,市場仍維持了成長軌跡。

預計預測期內對生物基和可再生化學品以及醋酸乙烯單體(VAM) 的需求不斷增加將推動市場需求。

另一方面,替代原料的可用性和原料價格的波動預計會阻礙市場成長。

在預測期內,開發新的分離技術以提高生產效率很可能成為市場發展的機會。

亞太地區貢獻了最高的市場佔有率,預計將在預測期內佔據市場主導地位。

生物乙酸市場趨勢

醋酸乙烯單體(VAM) 佔據市場主導地位

- 乙酸主要用於生產醋酸乙烯單體(VAM)。乙酸的伯酯,例如乙酸乙酯和醋酸丁酯,通常用作油漆和塗料的溶劑。

- 醋酸乙烯單體(VAM) 用於製造水性塗料、黏合劑、防水被覆劑以及紙和紙板被覆劑,並用於各種終端行業,包括建築、油漆和塗料、塑膠、溶劑、黏合劑和紡織品。

- 從全球來看,醋酸乙烯單體消費量的成長受到中國和美國的需求所推動。

- 在印度,亞洲塗料有限公司 (Asian Paints Ltd) 的完全子公司亞洲塗料 (聚合物) 私人有限公司 (APPPL) 宣布,將於 2023 年在古吉拉突邦赫吉建立醋酸乙烯酯-乙烯乳液 (VAE) 和醋酸乙烯單體(VAM) 製造工廠。建立該製造工廠的預計成本為 210 億印度盧比(2.5124 億美元)。

- 據 Motilal Oswal Financial Services(MOFSL)稱,醋酸乙烯單體(VAM)是最大的醋酸衍生物,佔全球需求的 40%。

- 2023年10月,美國跨國承包商KBR及其日本乙醯技術合作夥伴昭和電工被亞洲塗料公司選中,為印度的一家基層醋酸乙烯單體(VAM) 工廠提供服務。根據協議條款,KBR將為該年產10萬噸的工廠提供技術許可、基礎工程和專有設施。另一方面,昭和電工列出了催化劑和操作技術。

- 因此,預計 VAM 市場中的所有這些趨勢將在預測期內推動生物乙酸市場的需求。

亞太地區佔市場主導地位

- 亞太地區是全球最大的生物乙酸消費地區和成長最快的市場。

- 乙酸是一種重要的化學試劑和工業化學品,用於製造塑膠軟飲料瓶、照相膠片、油漆和被覆劑。建設活動的增加增加了對所用油漆和被覆劑的需求,從而增加了對乙酸的需求。

- 亞太地區對醋酸乙烯單體(VAM) 的需求正在成長,其中中國發揮關鍵作用。中國和印度人口眾多,全球市場消費潛力大。

- 在印度,國內VAM需求100%依賴進口。最大的衍生物醋酸乙烯單體(VAM)佔醋酸消費量的34%。新加坡是印度VAM主要進口國,佔印度VAM進口總量的一半以上。

- 2023年12月,中國江蘇蘇寶化工宣佈在鎮江新區投資醋酸乙烯酯和EVA綜合計劃。該雄心勃勃的計劃將分兩個階段進行,首先建造一座年產能為 33 萬噸的 VAM 生產工廠。

- 2023年初,INEOS與樂天株式會社宣布,計畫在韓國蔚山興建第三家VAM廠,將VAM產能從45萬噸擴大至70萬噸。

- 上述因素導致亞太地區對生物乙酸消費的需求不斷增加。

生物乙酸產業概況

生物乙酸市場正在整合。主要參與企業(不分先後順序)包括 LENZING AG、Godavari Biorefineries Ltd、Airedale Group、Novozymes A/S(Novonesis 集團的一部分)和 Sekab。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 對生物基和可再生化學品的需求不斷增加

- 醋酸乙烯單體(VAM)需求增加

- 限制因素

- 替代產品的可用性

- 原物料供應和價格的波動;

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(市場規模(基於數量))

- 原料

- 生質能

- 玉米

- 玉米

- 糖

- 其他成分

- 應用

- 醋酸乙烯單體(VAM)

- 醋酸酯

- 精對苯二甲酸(PTA)

- 乙酸酐

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AFYREN SA

- Airedale Group

- btgbioliquids

- GODAVARI BIOREFINERIES LTD

- Jubilant Ingrevia Limited

- LanzaTech

- LENZING AG

- Novozymes A/S(Novonesis Group)

- Sekab

- SUCROAL SA

第7章 市場機會與未來趨勢

- 開發新型分離技術以提高生產效率

The Bio-Acetic Acid Market size is estimated at 1.40 million tons in 2025, and is expected to reach 1.62 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The bio-acetic acid market was negatively impacted by COVID-19 in 2020. Construction activities and automotive manufacturing activities were on a temporary halt owing to the pandemic scenario, which had minimized the demand for vinyl acetate monomer used in the formulation of these end-user industry products such as adhesives, paints, coatings, plastics, and composites, in turn, negatively impacted the market demand for bio-acetic acid. However, the market retained its growth trajectory due to all the industries' resumed production processes.

Increasing demand for bio-based and renewable chemicals and vinyl acetate monomers (VAM) is expected to drive market demand during the forecast period.

On the flip side, the availability of alternatives and volatility in the feedstock availability and prices are expected to hinder the growth of the market.

Developing new separation technologies to increase production efficiency is likely to act as an opportunity for the market studied over the forecast period.

Asia-Pacific accounts for the highest market share and is expected to dominate the market during the forecast period.

Bio-Acetic Acid Market Trends

The Vinyl Acetate Monomer (VAM) Segment to Dominate the Market

- Acetic acid is mainly used to manufacture vinyl acetate monomer (VAM). The major esters of acetic acid, such as ethyl acetate and butyl acetate, are commonly used as solvents for paints and coatings.

- Vinyl acetate monomer (VAM) is used to produce water-based paints, adhesives, waterproofing coatings, and paper and paperboard coatings that can be used in various end-use industries such as construction, paints and coatings, plastic, solvents, adhesives, and textiles.

- On the Global front, growth in vinyl acetate monomer consumption is driven by demand in China and the United States.

- In India, in 2023, Asian Paints (Polymers) Private Limited (APPPL), a wholly-owned subsidiary of Asian Paints Ltd, announced the setting up of a manufacturing facility of vinyl acetate-ethylene emulsion (VAE) and vinyl acetate monomer (VAM) at Dahej, Gujarat. The approximate cost of setting up the manufacturing facility would be INR 2,100 crore (USD 251.24 million).

- According to the Motilal Oswal Financial Services (MOFSL), vinyl acetate monomer (VAM) is the largest acetic acid derivative, accounting for 40% of its global demand.

- In October 2023, US-based multinational contractor KBR and its Japanese acetyls technology partner, Showa Denko, were selected by Asian Paints to provide services for a grassroots vinyl acetate monomer (VAM) plant in India. Under the contract terms, KBR will provide a technology license, basic engineering, and proprietary equipment for a 100,000 t/y plant. In contrast, Showa Denko will provide the catalysts, along with its technical operating know-how.

- Thus, all such trends in the VAM market are expected to drive the demand for the bio-acetic acid market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is the largest consumer of bio-acetic acid globally and is the fastest-growing market.

- Acetic acid is an important chemical reagent and industrial chemical used in producing plastic soft drink bottles, photographic films, paints, and coatings. The increasing construction activities boost the demand for paints and coatings to be used, boosting the demand for acetic acid.

- Asia-Pacific accounts for the growing demand for vinyl acetate monomer (VAM), a crucial role that China is playing. Due to the huge population in China and India, they pose a huge consumption potential for the global market.

- In India, 100% of domestic VAM demand is met through imports. The largest derivative, vinyl acetate monomer (VAM), accounts for 34% of acetic acid consumption. Singapore is a major importer, with more than half the share of the total quantity of VAM imported by India.

- In December 2023, Jiangsu Sopo Chemical in China announced investing in a vinyl acetate and EVA-integrated project in the Zhenjiang New District. This ambitious project will unfold in two stages, beginning with the construction of a VAM production plant with a substantial capacity of 330 thousand tons per year.

- In early 2023, INEOS and LOTTE Corporation announced plans to expand VAM production capacity from 450 kilotons to 700 kilotons by adding a third VAM plant in Ulsan, South Korea, with expectations for completion by the end of 2025.

- The factors above contribute to the increasing demand for bio-acetic acid consumption in Asia-Pacific.

Bio-Acetic Acid Industry Overview

The bio-acetic acid market is consolidated. Some major players (not in any particular order) include LENZING AG, Godavari Biorefineries Ltd, Airedale Group, Novozymes A/S (Novonesis Group), and Sekab.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Bio-based and Renewable Chemicals

- 4.1.2 Increasing Demand for Vinyl Acetate Monomers (VAM)

- 4.2 Restraints

- 4.2.1 Availability of Alternatives

- 4.2.2 Volatility in the Feedstock Availability and Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material

- 5.1.1 Biomass

- 5.1.2 Corn

- 5.1.3 Maize

- 5.1.4 Sugar

- 5.1.5 Other Raw Materials

- 5.2 Application

- 5.2.1 Vinyl Acetate Monomer (VAM)

- 5.2.2 Acetate Esters

- 5.2.3 Purified Terephthalic Acid (PTA)

- 5.2.4 Acetic Anhydride

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Qatar

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.6 Middle East and Africa

- 5.3.6.1 Saudi Arabia

- 5.3.6.2 South Africa

- 5.3.6.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AFYREN SA

- 6.4.2 Airedale Group

- 6.4.3 btgbioliquids

- 6.4.4 GODAVARI BIOREFINERIES LTD

- 6.4.5 Jubilant Ingrevia Limited

- 6.4.6 LanzaTech

- 6.4.7 LENZING AG

- 6.4.8 Novozymes A/S (Novonesis Group)

- 6.4.9 Sekab

- 6.4.10 SUCROAL SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of New Separation Technologies to Increase Production Efficiency

中國的生物醋酸市場:來歷,各用途,終端用戶各業界,各地區,機會,預測,2018年~2032年生物醋酸的日本市場評估:各原料,各用途,各最終用途產業,各地區,機會,預測(2019年度~2033年度)

中國的生物醋酸市場:來歷,各用途,終端用戶各業界,各地區,機會,預測,2018年~2032年生物醋酸的日本市場評估:各原料,各用途,各最終用途產業,各地區,機會,預測(2019年度~2033年度) 生物乙酸市場:按原料、應用和最終用戶分類 - 全球預測 2025-2030

生物乙酸市場:按原料、應用和最終用戶分類 - 全球預測 2025-2030 全球生物乙酸市場(2024-2028)

全球生物乙酸市場(2024-2028) 全球生物醋酸市場(2016-2036)

全球生物醋酸市場(2016-2036) 生物醋酸的全球市場的評估:各原料,不同生產過程,各終端用戶,各地區,機會,預測(2016年~2030年)

生物醋酸的全球市場的評估:各原料,不同生產過程,各終端用戶,各地區,機會,預測(2016年~2030年) 生物醋酸市場 - 2018-2028年全球行業規模、佔有率、趨勢、機遇和預測,按來源、按應用、地區和競爭細分

生物醋酸市場 - 2018-2028年全球行業規模、佔有率、趨勢、機遇和預測,按來源、按應用、地區和競爭細分 生物醋酸市場:趨勢,機會,競爭分析【2023-2028年】

生物醋酸市場:趨勢,機會,競爭分析【2023-2028年】 生物醋酸市場規模、份額和趨勢分析報告:按應用、按地區、細分市場趨勢,2023-2030 年

生物醋酸市場規模、份額和趨勢分析報告:按應用、按地區、細分市場趨勢,2023-2030 年