|

市場調查報告書

商品編碼

1683411

超薄玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Ultra-thin Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

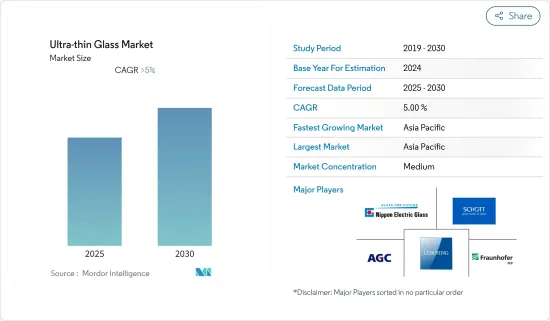

預計預測期內超薄玻璃市場複合年成長率將超過 5%。

主要亮點

- 預計預測期內超薄玻璃在電子產業的廣泛應用將佔據市場主導地位。它的柔韌性、彈性和出色的抗刮性等特性使其適合用於智慧型裝置。

- 正在進行的使用超薄玻璃作為太陽能計劃專用鏡子的研究預計將在預測期內為市場成長提供各種機會。

- 由於家電行業規模龐大,而家電行業是超薄玻璃的主要應用領域,因此亞太地區預計將成為超薄玻璃的最大市場。

超薄玻璃市場趨勢

消費性電子產品需求不斷成長

- 超薄玻璃在消費性電子領域的廣泛應用,正刺激市場區隔的需求。由於重量輕、平整度高、柔韌性好、表面品質好等特性,這些玻璃適用於個人電腦 (PC)、電子閱讀器、智慧型手機和其他電子設備。

- 預計 2020 年全球消費性電子領域收益將達到 4,260 億美元,到 2024年終將達到約 5,650 億美元。

- 2019年桌上型電腦、筆記型電腦及平板電腦的總銷量分別約為8,840萬台、1.66億台和1.368億台。預計2020年全球銷售給終端用戶的智慧型手機數量將達到15.6億支。隨著對電子設備的需求不斷增加,預計未來幾年這些電子產品的生產和銷售將進一步增加。

- 預計所有上述因素都將在預測期內推動超薄玻璃市場的發展。

亞太地區佔市場主導地位

- 由於中國、印度、日本和韓國等國家的超薄玻璃消費量不斷增加,亞太地區是全球最大且成長最快的超薄玻璃市場。

- 預計到 2020 年該地區的消費電子產品總合收入將達到 2,270 億美元,到 2024年終預計將成長到 2,627 億美元。

- 2019年全球售出的智慧型手機為15億部,其中僅在中國就售出了4.2億部以上。

- 由於該地區的一些新興國家對智慧型設備的需求很高,因此該地區未來市場成長潛力巨大。

- 2019年,中國、印度等主要國家的汽車產銷量均大幅下滑,預計對市場成長將產生輕微影響。

- 因此,基於上述因素,預計預測期內亞太地區對超薄玻璃的需求將會成長。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 家電需求不斷成長

- 其他促進因素

- 限制因素

- 原料高成本

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 按應用

- 半導體基板

- 觸控螢幕

- 指紋感應器

- 汽車嵌裝玻璃

- 其他用途

- 按最終用戶產業

- 消費性電子產品

- 車

- 生物技術

- 其他最終用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率分析

- 主要企業策略

- 公司簡介

- AGC Glass Europe

- Central Glass Co. Ltd

- Changzhou Almaden Co. Ltd

- Corning Incorporated

- CSG Holding Co. Ltd

- Emerge Glass

- Fraunhofer FEP

- Nippon Electric Glass Co. Ltd

- Nitto Boseki Co., Ltd

- Novalglass

- Schott AG

- Taiwan Glass Industry Corporation

第7章 市場機會與未來趨勢

- 為太陽能計劃開發高性能玻璃

- 其他機會

簡介目錄

Product Code: 68544

The Ultra-thin Glass Market is expected to register a CAGR of greater than 5% during the forecast period.

Key Highlights

- Extensive applications of ultra-thin glasses in the electronics industry are anticipated to govern the market during the forecast timeline. Its properties like flexibility, elasticity, and superior scratch resistance ability make them suitable for use in smart devices.

- On-going research is being done to use ultra-thin glasses as special mirrors for solar energy projects are expected to offer various opportunities for the growth of the market over the forecast period.

- The Asia-Pacific region is expected to be the largest market for the ultra-thin glass market because of the gigantic consumer electronics industry of the region where these glasses find their major application.

Ultra-Thin Glass Market Trends

Growing Demand from Consumer Electronics

- The extensive use of ultra-thin glass in the consumer electronics segment has surged the demand of the market studied. Its properties such as lightweight, perfect flatness, flexibility, good surface quality, etc. make these glasses suitable for Personal Computers (PCs), e-readers, smartphones, and other electronic gadgets.

- Global revenue from the consumer electronics segment is projected to be USD 426 billion in 2020 and is estimated to reach around USD 565 billion by the end of 2024.

- The total number of sales of desktop PCs, laptops, and tablets in 2019 was about 88.4 million, 166 million and 136.8 million units respectively. The number of smartphones sold to end users globally in 2020 is anticipated to be 1.560 billion units. With the increasing demand for electronics, the production and sales of these electronic goods are expected to further increase over the coming years.

- All the aforementioned factors are expected to drive the ultra-thin glass market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region accounts for the largest and fastest-growing market in the ultra-thin glass market globally owing to the increasing consumption from countries such as China, India, Japan, and South Korea.

- The region is projected to amass a total of USD 227 billion from its consumer electronics segment by 2020 and is forecasted to grow up to USD 262.7 billion by the end of 2024.

- China alone accounts for the sale of more than 420 million units of smartphones sold out of 1.5 billion units sold globally in 2019.

- The region holds great potential for the future growth of the market studied as some emerging countries from the region have a high demand for smart devices.

- The automotive production and sales in major countries such as China and India have witnessed huge downfall in 2019 and this is expected to slightly affect the growth of the market.

- Hence, from the above mentioned factors, the demand for ultra-thin glass in Asia-Pacific region is expected to grow over the forecast period.

Ultra-Thin Glass Industry Overview

The Ultra-Thin Glass Market is partially fragmented. Some of the players in the market include Nippon Electric Glass Co. Ltd, Schott AG, AGC Glass Europe, Corning Incorporated, and Fraunhofer FEP.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Consumer Electronics

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Semiconductor Substrate

- 5.1.2 Touch Panel Displays

- 5.1.3 Fingerprint Sensors

- 5.1.4 Automotive Glazing

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive

- 5.2.3 Biotechnology

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Glass Europe

- 6.4.2 Central Glass Co. Ltd

- 6.4.3 Changzhou Almaden Co. Ltd

- 6.4.4 Corning Incorporated

- 6.4.5 CSG Holding Co. Ltd

- 6.4.6 Emerge Glass

- 6.4.7 Fraunhofer FEP

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Nitto Boseki Co., Ltd

- 6.4.10 Novalglass

- 6.4.11 Schott AG

- 6.4.12 Taiwan Glass Industry Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Advanced Glass for Solar Energy Projects

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

超薄玻璃市場規模、佔有率和成長分析(按厚度、製造程序、應用、最終用途行業和地區)- 2025-2032 年行業預測

超薄玻璃市場規模、佔有率和成長分析(按厚度、製造程序、應用、最終用途行業和地區)- 2025-2032 年行業預測 超薄玻璃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

超薄玻璃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 超薄玻璃市場:按厚度、製造流程、材料、應用和最終用途 - 2025-2030 年全球預測

超薄玻璃市場:按厚度、製造流程、材料、應用和最終用途 - 2025-2030 年全球預測 2024-2032 年按厚度類型、製造流程、應用、最終用途產業和地區分類的超薄玻璃市場報告

2024-2032 年按厚度類型、製造流程、應用、最終用途產業和地區分類的超薄玻璃市場報告 超薄玻璃市場,按製造流程、按應用、按最終用戶、按國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

超薄玻璃市場,按製造流程、按應用、按最終用戶、按國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 超薄透明玻璃市場報告:2030 年趨勢、預測與競爭分析

超薄透明玻璃市場報告:2030 年趨勢、預測與競爭分析 全球超薄玻璃市場:預測至 2029 年

全球超薄玻璃市場:預測至 2029 年 超薄玻璃市場:按厚度類型、按應用、按地區 - 規模、份額、展望、機會分析,2023-2030 年

超薄玻璃市場:按厚度類型、按應用、按地區 - 規模、份額、展望、機會分析,2023-2030 年![超薄玻璃市場:趨勢、機遇和競爭分析[2023-2028]](/sample/img/cover/42/1300081.png) 超薄玻璃市場:趨勢、機遇和競爭分析[2023-2028]

超薄玻璃市場:趨勢、機遇和競爭分析[2023-2028]