|

市場調查報告書

商品編碼

1683755

美國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)United States Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

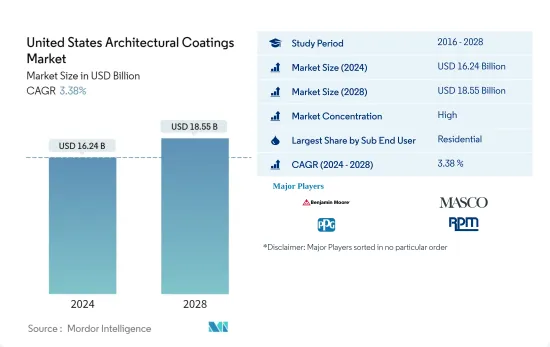

預計 2024 年美國建築塗料市場規模為 162.4 億美元,到 2028 年將達到 185.5 億美元,預測期內(2024-2028 年)的複合年成長率為 3.38%。

主要亮點

- 按最終用戶分類的最大細分市場:住宅:由於住宅建築的數量比商業建築多,因此住宅領域的建築塗料消費量更高。

- 以科技分類的最大細分市場-水性塗料:在美國,由於環保署(EPA)的嚴格監管和大量消費者對環保健康產品的偏好,水性塗料的消費量和成長率很高。

- 樹脂最大的市場:丙烯酸:丙烯酸是主要的樹脂類型,因為它成本低且可用於許多水性塗料。美國市場水性塗料的使用也正在增加。

美國建築塗料市場的趨勢

按終端用戶細分,住宅是最大的。

- 建築塗料的成長自 2016 年以來一直在下降,但在 2020 年有所恢復。 2020 年的成長主要是由於消費者待在家中完成 DIY計劃導致 DIY 領域銷售額大幅成長。住宅存量的老化是市場需求的主要驅動力,平均房齡從 2001 年的約 31 年達到 2019 年的 41 年。

- 該國住宅部門佔比最高,約78-79%。但這趨勢在2020年發生了明顯變化,住宅領域的重新粉刷需求大幅增加,而商業領域的重新粉刷需求則大幅減少,導致商業領域的佔比降至17.4%以下。

- 預計商業部門的佔有率將在預測期內恢復,但由於住宅部門的持續需求,短期內可能無法達到大流行前的水平。

美國建築塗料產業概況

美國建築塗料市場相當集中,前五大公司佔了77.70%的市場。該市場的主要企業是:Benjamin Moore & Co.、Masco Corporation、PPG Industries, Inc.、RPM International Inc. 和 The Sherwin-Williams Company(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第 2 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第3章 產業主要趨勢

- 占地面積趨勢

- 法律規範

- 價值鏈與通路分析

第 4 章 市場細分

- 子終端用戶

- 商業的

- 住宅

- 技術領域

- 溶劑型

- 水性

- 樹脂

- 丙烯酸纖維

- 醇酸

- 環氧樹脂

- 聚酯纖維

- 聚氨酯

- 其他樹脂類型

第5章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 業務狀況

- 公司簡介

- Beckers Group

- Benjamin Moore & Co.

- Diamond Vogel

- Dunn-Edwards Corporation

- Kelly-Moore Paints

- Masco Corporation

- PPG Industries, Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第6章 執行長的關鍵策略問題

第7章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The United States Architectural Coatings Market size is estimated at USD 16.24 billion in 2024, and is expected to reach USD 18.55 billion by 2028, growing at a CAGR of 3.38% during the forecast period (2024-2028).

Key Highlights

- Largest Segment by End-user - Residential : Compared to commercial building stock, the country's high volume of residential building stock resulted in high architectural paint consumption from the residential sector.

- Largest Segment by Technology - Waterborne : High EPA regulations and consumer preference toward green and healthy products contributed to the high consumption and growth of waterborne coatings in the United States.

- Largest Segment by Resin - Acrylic : Acrylic is a leading type of resin, owing to its low cost and high usage in waterborne coatings. Waterborne coatings are also increasingly used in the US market.

US Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

- The growth rate of architectural coatings declined since 2016 before bouncing back in 2020. The growth registered in 2020 was due to a huge sales increase from the DIY segment, driven by consumers "nesting" at home and completing DIY projects. The aging housing stock, which reached an average age of 41 years in 2019 from around 31 years in 2001, was a major driver for the market demand.

- The country's residential sector held the highest share, registering around 78-79%. However, this trend changed drastically in 2020 due to a major increase in residential repaint demand in parallel with a huge decline in the commercial sector, thus reducing the commercial sector's share to less than 17.4%.

- Though the commercial sector's share is expected to recover during the forecast period, it may not reach the pre-pandemic levels in the short term due to sustained demand in the residential segment.

US Architectural Coatings Industry Overview

The United States Architectural Coatings Market is fairly consolidated, with the top five companies occupying 77.70%. The major players in this market are Benjamin Moore & Co., Masco Corporation, PPG Industries, Inc., RPM International Inc. and The Sherwin-Williams Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

- 4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

- 4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

- 4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles

- 5.4.1 Beckers Group

- 5.4.2 Benjamin Moore & Co.

- 5.4.3 Diamond Vogel

- 5.4.4 Dunn-Edwards Corporation

- 5.4.5 Kelly-Moore Paints

- 5.4.6 Masco Corporation

- 5.4.7 PPG Industries, Inc.

- 5.4.8 RPM International Inc.

- 5.4.9 The Sherwin-Williams Company

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

中國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印尼建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印尼建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 德國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

德國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 新加坡建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

新加坡建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 日本建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

日本建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 法國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

法國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 泰國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

泰國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 義大利建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

義大利建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 英國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

英國建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)