|

市場調查報告書

商品編碼

1685698

虛擬實境 (VR) - 市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Virtual Reality (VR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

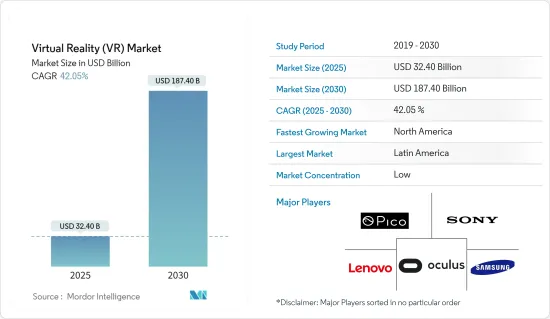

虛擬實境市場規模預計在 2024 年為 228.1 億美元,預計到 2029 年將達到 1319.3 億美元,預測期內(2024-2029 年)的複合年成長率為 42.05%。

主要亮點

- 虛擬實境主要利用科技來創造模擬環境。與傳統使用者介面不同,VR 讓使用者置身於體驗之中。這意味著用戶無需看著面前的顯示器螢幕,而是可以沉浸在 3D 世界中並與之互動。透過模擬盡可能多的感官,包括視覺、觸覺、聽覺甚至嗅覺,這項技術正在改變世界。

- 學校利用 VR 技術最常見的原因之一是允許學生進行虛擬實地考察。實地考察是教育機構的悠久傳統。這是因為它允許教師在身臨其境型環境中教育學生,提供課堂上難以實現的實踐學習機會。然而,實地考察對於一些學生來說可能會在經濟上造成困難。對於行動不便的學生來說,這也會很困難。

- 隨著遠端工作和虛擬協作的興起,對能夠讓人們在虛擬空間中進行互動和協作的 VR 軟體的需求日益成長。 VR 會議平台、虛擬活動空間和協作設計工具可讓使用者無論身處何處,都可以在沉浸式虛擬環境中協同工作。它也用於醫療保健等各種行業,用於醫療培訓、手術模擬、疼痛管理、暴露療法和復健。醫療保健領域對 VR 軟體的需求源於其改善病患治療效果、加強醫學教育和降低醫療成本的潛力。

- 虛擬實境正在成為一項革命性的技術,能夠對各種終端使用者產業產生顯著影響。該技術正在持續發展,導致使用案例的廣泛擴展。

- VR 通常透過追蹤頭部和眼球運動的耳機來實現。有些系統使用其他周邊設備(例如手套)來模擬額外的感覺。對於許多消費者來說,這項技術價格昂貴,高階 VR 設備需要功能強大的 PC 和遊戲機,這限制了該技術的廣泛應用。

- 自從新冠疫情爆發以來,我們看到遠距協作和團隊建立練習增加。與傳統視訊會議工具相比,VR技術帶來了更具沉浸感和互動性的體驗。此外,該技術迎合了全球日益成長的遊戲趨勢,促進遊戲成為一種娛樂形式,並有助於提供虛擬實境遊戲體驗。

虛擬實境(VR)市場趨勢

遊戲是一個蓬勃發展的終端用戶產業

- 全球 AR 和 VR 遊戲玩家的快速成長正在拓寬市場視野。據人工智慧、機器學習、巨量資料分析和 AR/VR 解決方案提供商 NewGenApps 稱,到 2025 年,全球 AR 和 VR 遊戲用戶群預計將成長到 2.16 億。

- 此外,對電玩遊戲的需求不斷成長,為供應商提供VR頭戴裝置創造了機會。 Uswitch 的 2023 年線上遊戲統計數據顯示,全球約有 40% 的人口參與線上遊戲。在過去的幾十年裡,元宇宙已經從本地的單人和多人體驗發展成為一個跨越國家和大洲的全球舞台。

- 夥伴關係、協作和併購等策略性舉措為主要市場參與者擴大市場佔有率提供了重要機會。例如,2023年10月,總部位於印度艾哈默德巴德的主要企業Yudiz Solutions宣布與主要通訊業者沃達豐印度(Vi)合作推出一款VR戰鬥射擊遊戲,並在2023年印度行動通訊大會上展示了其功能。 5G技術將用於為VR戰鬥射擊遊戲提供動力,用戶可以期待在虛擬實境中獲得響應迅速、互動性強且身臨其境的低延遲體驗。

- VR 遊戲在各個年齡層的玩家中越來越受歡迎,擴大了消費者群體。 Oculus Quest 系列等價格實惠的 VR 裝置的出現,使得更廣泛的消費者可以玩 VR 遊戲。開發人員擁有巨大的機會來創建更引人注目的 VR 遊戲,並利用 VR 技術的獨特功能。

- 遊戲產業認知到VR的市場潛力。隨著科技變得越來越普及和價格越來越便宜,對 VR 遊戲體驗的需求也越來越大。遊戲開發商和發行商將 VR 視為創造令人興奮、身臨其境的體驗的機會,可以吸引新的受眾並在擁擠的市場中脫穎而出。

北美佔最大市場佔有率

- 北美對虛擬實境 (VR) 的需求正在快速成長,這在很大程度上是由於各個行業的個人擴大參與這項技術。這種需求的成長是由 VR 技術的多樣化用途所推動的,這些用途涵蓋娛樂和遊戲、教育、醫療保健和企業解決方案。

- 技術進步使得 VR 設備更加易於存取和方便用戶使用,進一步推動了對 VR 的需求。 VR頭戴裝置價格低廉且效能不斷提升,促使其在北美廣泛普及,從技術愛好者到尋求新穎有趣體驗的普通用戶。因此,許多公司正在推出新產品以增加市場佔有率。

- 隨著虛擬實境變得越來越容易取得和使用,它為政府探索創新方法提供了巨大的潛力。因此,美國政府正在將 VR 作為跨產業的一種有價值的工具。例如,美國食品藥物管理局於2023年9月宣布,一些通常僅在醫生辦公室或醫院提供的臨床服務可以透過VR提供給在家中或其他非臨床環境中的患者。

- 此外,在終端用戶產業中,教育領域預計在預測期內將大幅成長。北美各地的教育機構正在將 VR 納入其課程,為學生提供實踐體驗式學習機會。虛擬實地考察、模擬和互動課程增強了學習體驗,使複雜的概念更容易理解,並促進了對一系列學科的更深入的理解。

- 這些因素顯示對 VR 的需求正在成長。隨著 VR 的發展及其在各個行業的普及,它可能會改變個人和行業與數位時代的互動方式。北美 VR 應用的發展軌跡表明,未來身臨其境型體驗將成為日常生活中不可或缺的一部分。因此,上述因素可能會促進所研究市場的成長。

虛擬實境(VR)產業概覽

虛擬實境市場是分散的。隨著 VR 公司專注於透過遊戲、娛樂、培訓和行銷等用途為更廣泛的大眾受眾帶來可及性,市場競爭正在加劇。在這個行業中,由於各公司的成長,競爭對手之間的敵意很高。預計競爭將繼續加劇。主要企業包括 Oculus VR LLC、聯想Group Limited、三星電子、Sony Corporation和 Pico Interactive Inc.

- 2024 年 1 月,高通技術公司宣布與 RayNeo 和應用材料公司建立策略合作夥伴關係,共同開發並向市場推出領先的下一代 AR 眼鏡。此次合作預計將匯集領先科技供應商的專業知識,重新定義 AR 眼鏡的未來。 RayNeo 的 AR 眼鏡利用高通的驍龍 AR1 Gen1 平台和應用材料的輕量全彩波導管,為消費級 AR 產品打造全面的軟體和硬體生態系統。

- 2023 年 11 月,Pico 宣布推出其下一代一體式VR頭戴裝置PICO 4,旨在透過結合舒適性和性能讓每個人都能享受虛擬實境。 PICO 4 基於 Snapdragon XR2 平台,具有超輕機身、薄餅光學系統、4K 顯示器和直覺的使用者介面。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 產業價值鏈分析

- 評估影響市場的宏觀經濟因素

第5章市場動態

- 市場促進因素

- VR 的商業應用日益增多

- 不同終端使用者群體對 VR 培訓設備的需求不斷成長

- 市場挑戰/限制

- 長期使用VR頭戴裝置的健康風險

- 暈動症的影響

第6章市場區隔

- 按類型

- 硬體

- 系留式 HMD

- 獨立式 HMD

- 無螢幕檢視器

- 軟體

- 硬體

- 按最終用戶產業

- 遊戲

- 媒體與娛樂

- 零售

- 衛生保健

- 軍事和國防

- 房地產

- 教育

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Oculus VR LLC

- Sony Corporation

- Samsung Electronics Co. Ltd

- Lenovo Group Ltd

- Pico Interactive Inc.

- Qualcomm Technologies Inc.

- FOVE Inc.

- Unity Technologies Inc.

- Unreal Engine(Epic Games Inc.)

- Apple Inc.

- DPVR(Lexiang Technology Co. Ltd)

- Autodesk Inc.

- Eon Reality Inc.

- 3D Systems Corporation

- Dassault Systemes SE

- HTC Vive(HTC Corporation)

第8章投資分析

第9章:市場的未來

The Virtual Reality Market size is estimated at USD 22.81 billion in 2024, and is expected to reach USD 131.93 billion by 2029, growing at a CAGR of 42.05% during the forecast period (2024-2029).

Key Highlights

- Virtual reality primarily uses technology to create a simulated environment. Unlike the traditional user interface, VR places the user inside an experience, which means that instead of viewing a monitor screen in front of them, users are immersed and can interact with the 3D world. With the simulation of as many senses as possible, such as vision, touch, hearing, and even smell, the technology has been transformed worldwide.

- One of the most popular reasons schools are taking advantage of VR technology is its ability to let students take field trips virtually. Field trips are a time-honored tradition for educational institutions. They allow teachers to educate their students in immersive environments and provide hands-on learning opportunities that would otherwise be difficult to achieve within the classroom. However, field trips can be financially prohibitive for some students. They can also be challenging for students with mobility limitations.

- With the rise of remote work and virtual collaboration, there is a growing demand for VR software that enables users to interact and collaborate in virtual spaces. VR meeting platforms, virtual event spaces, and collaborative design tools allow users to work together in immersive virtual environments regardless of physical location. It is also used in various industries, including healthcare, for medical training, surgical simulations, pain management, exposure therapy, and rehabilitation. The demand for VR software in healthcare is driven by its potential to improve patient outcomes, enhance medical education, and reduce healthcare costs.

- Virtual reality is emerging as a revolutionary technology that can notably impact various end-user industries. The technology is witnessing continuous growth, leading to significant expansion in the number of use cases.

- VR is usually accessed using a headset that tracks the movement of the head and eye. Some systems also use other peripherals (e.g. gloves) to simulate additional senses. This technology is expensive for many consumers, and high-end VR sets require powerful PCs or gaming consoles, which is restricting widespread adoption of the technology.

- Since the COVID-19 pandemic, remote collaboration and team-building exercises have increased. VR technology facilitated immersive and interactive experiences more than traditional videoconferencing tools. Moreover, this technology caters to the growing gaming trend globally, which facilitates gaming as a form of entertainment and helps in providing VR gaming experiences.

Virtual Reality (VR) Market Trends

Gaming to be the Fastest-growing End-user Industry

- Rapid growth in AR and VR gamers worldwide has expanded the market's horizon. According to NewGenApps, a provider of artificial intelligence, machine learning, big data analytics, and AR/VR solutions, the global user base of AR and VR games is estimated to increase to 216 million users by 2025.

- Moreover, the increasing demand for video games creates an opportunity for vendors to offer VR headsets. Uswitch's 2023 online gaming statistics revealed that approximately 40% of the global population engages in online gaming. Over the past few decades, the metaverse has evolved from local single and multiplayer experiences to a global stage, spanning countries and continents.

- Strategic initiatives like partnerships, collaborations, and mergers and acquisitions give major market players a significant chance to expand their market presence. For instance, in October 2023, Yudiz Solutions, a leading digital transformation and game development company based in Ahmedabad, India, showcased its capabilities at the India Mobile Congress 2023 by unveiling a VR combat shooting game in partnership with leading telecom operator Vodafone India (Vi). 5G technology is used to power VR combat shooting games, and users can expect a low latency experience that allows them to be responsive and interactively immersed in virtual reality.

- The increasing popularity of VR gaming among various age groups is expanding the consumer base. Introducing affordable VR handsets like the Oculus Quest series has made VR gaming accessible to a more extensive consumer base. There is a significant opportunity for developers to create more engaging VR games that can employ the unique capabilities of VR technology.

- The gaming industry recognizes the market potential of VR. As the technology becomes more accessible and affordable, the demand for VR gaming experiences is increasing. Game developers and publishers see VR as an opportunity to reach new audiences and create exciting, immersive experiences that stand out in a crowded market.

North America Holds the Largest Market Share

- The demand for VR in North America has experienced rapid growth owing to the significant shift in individuals across various sectors engaging with technology. This increasing demand is fueled by the various applications of VR technology, ranging from entertainment and gaming to education, healthcare, and enterprise solutions.

- The demand for VR is further propelled by technological advancements, making VR devices more accessible and user-friendly. The affordability and improved performance of VR headsets have contributed to broader adoption across North America, from tech enthusiasts to casual users seeking novel and engaging experiences. Hence, many companies are launching new products to increase their market share.

- Also, as VR becomes more accessible and easier to use, it offers a lot of great possibilities for the government to explore innovative approaches. Hence, the US government uses VR as a valuable tool across multiple industries. For instance, in September 2023, the US Food and Drug Administration announced that VR could deliver some clinical services, normally delivered only in clinics and hospitals, to patients in their homes or other non-clinical settings.

- Moreover, among end-user industries, the education segment is expected to grow significantly during the forecast period. North American educational institutions are integrating VR into their curricula to provide students with hands-on, experiential learning opportunities. Virtual field trips, simulations, and interactive lessons enhance the learning experience, making complex concepts more accessible and fostering a deeper understanding of various subjects.

- These factors indicate the growing demand for VR. As VR evolves and becomes more accessible, various industries will shape how individuals and industries interact with the digital era. The trajectory of VR adoption in North America suggests a future where immersive experiences become an integral part of everyday life. Hence, the abovementioned factors will boost the growth of the market studied in the future.

Virtual Reality (VR) Industry Overview

The virtual reality market is fragmented in nature. It is witnessing a rise in competitiveness among companies as VR companies are focused on providing accessibility to larger masses through gaming, entertainment, training, and marketing, among other applications. The competitive rivalry is high in this industry, owing to growth among various companies. Competition is expected to increase in the future. Some major players include Oculus VR LLC, Lenovo Group Ltd, Samsung Electronics Co. Ltd, Sony Corporation, and Pico Interactive Inc.

- In January 2024, Qualcomm Technologies announced strategic collaborations with RayNeo and Applied Materials to develop and bring the next generation of market-leading AR glasses to market. This collaboration is expected to bring together the expertise of industry-leading technology providers to redefine the future of AR glasses. RayNeo's AR glasses will utilize Qualcomm's Snapdragon AR1 Gen1 platform and Applied Materials' lightweight full-color waveguides to create a comprehensive software and hardware ecosystem for consumer-grade AR products.

- In November 2023, Pico announced the launch of PICO 4, a next-generation, all-in-one VR headset designed to make virtual reality accessible to everyone by combining comfort and performance. PICO 4 is based on the Snapdragon XR2 platform and features an ultra-light body, pancake optics, a 4K display, and an intuitive user interface.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of VR in Commercial Applications

- 5.1.2 Growing Demand for VR Setups for Training Across Various End-user Segments

- 5.2 Market Challenges/Restraints

- 5.2.1 Health Risks from Using VR Headsets in the Longer Run

- 5.2.2 Impact of Cybersickness

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hardware

- 6.1.1.1 Tethered HMD

- 6.1.1.2 Standalone HMD

- 6.1.1.3 Screenless Viewer

- 6.1.2 Software

- 6.1.1 Hardware

- 6.2 By End-user Industry

- 6.2.1 Gaming

- 6.2.2 Media and Entertainment

- 6.2.3 Retail

- 6.2.4 Healthcare

- 6.2.5 Military and Defense

- 6.2.6 Real Estate

- 6.2.7 Education

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oculus VR LLC

- 7.1.2 Sony Corporation

- 7.1.3 Samsung Electronics Co. Ltd

- 7.1.4 Lenovo Group Ltd

- 7.1.5 Pico Interactive Inc.

- 7.1.6 Qualcomm Technologies Inc.

- 7.1.7 FOVE Inc.

- 7.1.8 Unity Technologies Inc.

- 7.1.9 Unreal Engine (Epic Games Inc.)

- 7.1.10 Apple Inc.

- 7.1.11 DPVR (Lexiang Technology Co. Ltd)

- 7.1.12 Autodesk Inc.

- 7.1.13 Eon Reality Inc.

- 7.1.14 3D Systems Corporation

- 7.1.15 Dassault Systemes SE

- 7.1.16 HTC Vive (HTC Corporation)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025 年至 2033 年虛擬實境市場規模、佔有率、趨勢及預測(按設備類型、技術、組件、應用和地區)

2025 年至 2033 年虛擬實境市場規模、佔有率、趨勢及預測(按設備類型、技術、組件、應用和地區) 協作 VR 環境市場按技術、組件、設備類別、應用和最終用戶分類 - 2025-2030 年全球預測

協作 VR 環境市場按技術、組件、設備類別、應用和最終用戶分類 - 2025-2030 年全球預測 基於 VR 的遠端協助市場(按組件、服務交付模式、應用和最終用戶分類)- 2025-2030 年全球預測

基於 VR 的遠端協助市場(按組件、服務交付模式、應用和最終用戶分類)- 2025-2030 年全球預測 教育虛擬實境市場規模、佔有率和成長分析(按類型、應用、最終用戶、設備類型和地區)- 2025-2032 年產業預測

教育虛擬實境市場規模、佔有率和成長分析(按類型、應用、最終用戶、設備類型和地區)- 2025-2032 年產業預測 零售業虛擬實境的全球市場

零售業虛擬實境的全球市場 遊戲領域的虛擬實境 (VR),全球市場 2025-2029

遊戲領域的虛擬實境 (VR),全球市場 2025-2029 教育中的虛擬實境 (VR) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

教育中的虛擬實境 (VR) -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 零售市場中的虛擬實境 - 全球產業規模、佔有率、趨勢、機會和預測,按硬體、軟體相容性、類型、地區和競爭細分,2019-2029F

零售市場中的虛擬實境 - 全球產業規模、佔有率、趨勢、機會和預測,按硬體、軟體相容性、類型、地區和競爭細分,2019-2029F VR(虛擬實境)硬體

VR(虛擬實境)硬體 VR(虛擬實境)硬體產業預測

VR(虛擬實境)硬體產業預測