|

市場調查報告書

商品編碼

1686224

電動車充電站:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Electric Vehicle Charging Station - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

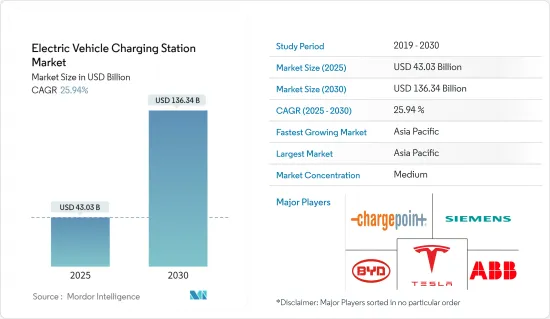

預計 2025 年電動車充電站市場規模將達到 430.3 億美元,到 2030 年將達到 1,363.4 億美元,預測期內(2025-2030 年)的複合年成長率為 25.94%。

電動車充電站市場正在蓬勃發展,因為越來越多的人轉向電動車,因為電動車具有成本效益、環境友好、嚴格的排放和燃油效率標準、政府激勵措施以及經濟實惠的車型可供選擇,這些都刺激了對充電站的需求。

因此,電動車在汽車行業的普及和汽車銷售的增加正在推動市場成長。此外,政府迅速實施嚴格的法規以減少汽車排放並提高電池效率,正在刺激汽車產業對電動車的需求,從而增加對充電基礎設施的需求。

儘管最初遭遇挫折,但電動車充電站市場已證明具有韌性。自新冠疫情爆發以來,世界各國政府都優先考慮永續的交通解決方案,包括投資電動車充電基礎設施以刺激經濟成長和創造就業機會。

到目前為止,消費者對電動車充電站的態度一直很積極,對快速充電和便利使用的需求不斷成長。然而,人們仍然擔心充電基礎設施的成本和可靠性,這為企業創新和改進服務提供了機會。

電動車充電站市場趨勢

乘用車推動電動車充電站市場

乘用車市場是電動車充電站市場中最大的部分。這主要是因為乘用車的數量相對於商用車而言較大,而且全球電動乘用車的採用率日益提高。乘用車佔電動車銷售的很大一部分,因此對充電基礎設施的需求不斷成長,以滿足其充電需求。

- 國際能源總署(IEA)預測,儘管2022年汽車銷量整體疲軟,但預計2023年全球電動車銷量將成長約32.38%,首次突破1,300萬輛。

隨著越來越多的人意識到傳統汽油動力汽車對環境的影響,人們對電動車的興趣日益濃厚。燃料價格上漲也推動了汽車產業對電動車的採用,並在刺激充電站需求方面發揮了關鍵作用。

此外,叫車和汽車共享市場預計也將推動充電站的需求。與私家車相比,叫車和共乘汽車的使用時間通常更長,利用率也更高。這意味著他們需要更頻繁地充電,從而增加對充電站的需求。

儘管這種成長顯示了汽車電氣化的趨勢,但這還不足以減少全球二氧化碳排放。根據國際能源總署估計,到 2022 年,最普遍購買的車輛 SUV 的二氧化碳排放將達到近 10 億噸。這些擔憂促使主要汽車製造商推出電動 SUV 來吸引市場注意力。

- 例如,沃倫·巴菲特的比亞迪於 2023 年 1 月在印度推出了其首款乘用車——一款電動運動型多功能車 (SUV),標誌著其作為更廣泛的全球擴張的一部分進入主流市場。比亞迪推出了電動 SUV Atto 3,搭載其成熟的 Blade 電池技術,目標是到 2030 年佔領印度電動車市場 40% 的佔有率。此舉是中國汽車製造商全球擴張計畫的一部分,中國汽車製造商已開始在挪威、紐西蘭、新加坡、巴西、哥斯大黎加和哥倫比亞等國家銷售電動車和插電式混合動力汽車。

上述發展預計將促進電動車充電站市場乘用車領域的成長。

亞太地區將成為預測期內成長最快的地區

電動車 (EV) 充電站市場成長最快的地區是亞太地區 (APAC)。幾項關鍵發展推動該地區走在電動車應用和充電基礎設施發展的前沿。尤其是中國和印度,對亞太地區電動車充電市場的成長做出了重大貢獻。

亞太地區市場成長的關鍵催化劑之一是政府的大力支持和鼓勵電動車和充電基礎設施部署的政策。中國、印度、日本和韓國等國家正在實施雄心勃勃的目標和獎勵,以加速電動車的普及和充電基礎設施網路的擴張。例如

- 中國的新能源汽車(NEV)信貸計畫和補貼計畫引發了對電動車充電基礎設施的投資激增,導致全國充電站數量迅速增加。

- 同樣,日本經濟產業省的《促進電動車充電基礎設施發展的指南》設定了2035年安裝多達30萬個電動車充電埠的目標。

此外,亞太地區國家快速的都市化和人口成長正在推動對永續交通解決方案的需求,包括電動車和充電站。人口稠密、污染嚴重的都市區尤其鼓勵人們轉向更清潔的交通方式,導致電動車的採用和充電基礎設施的部署激增。

電動車充電技術的進步和創新正在促進亞太市場的成長。該地區的主要參與者正在開發先進的充電解決方案,包括快速充電系統、無線充電技術和智慧充電網路,以滿足消費者和企業不斷變化的需求。

- 例如,英國汽車製造商 Lotus 於 2023 年 11 月推出了一系列電動車 (EV) 充電解決方案,包括超高速 450kW 直流充電器、電源櫃和可同時為多達四輛汽車充電的模組化裝置。這些新的充電解決方案是專為印度市場設計的。液冷一體成型直流充電器是一款尖端充電器,可提供高達 450kW 的超快速充電速度。

總體而言,由於政府支持、都市化趨勢和技術創新,預計亞太地區市場在未來幾年將實現顯著的複合年成長率。

電動車充電站產業概況

電動車充電站市場適度整合。該市場由 ABB、西門子、比亞迪、西門子股份公司和特斯拉等主要企業主導。主要企業致力於透過研發投資、先進技術的整合、產品合作以及現有產品線的創新來不斷改進產品。

- 2023 年 1 月:ABB E-Mobility 簽署全球框架協議,為斯堪尼亞提供全球電動車充電解決方案支援。 ABB 的電動車產品組合將使斯堪尼亞能夠為客戶提供完整的電動車解決方案,為他們的車輛提供電氣化,並在全球範圍內供應車輛、充電器、服務和軟體。

- 2023 年 2 月,FLO 推出了 FLO Ultra,這是一款超快速充電器,旨在最大限度地提高能量輸送,同時提供面向未來的性能和時尚的設計,以提供終極電動車充電體驗。

- 2023年3月,岡谷電力集團旗下的岡谷電機與電動車(4W車輛)車隊營運商Prakriti E-Mobility建立策略夥伴關係,為該公司的車隊業務提供充電站。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 電動車銷量成長和電動車價格下降正在推動市場

- 市場限制

- 安裝和維護標準電動車充電站的初始成本高是一個問題

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 按車輛類型

- 搭乘用車

- 商用車

- 按充電器類型

- 交流充電站

- 直流充電站

- 按充電所有者類型

- 公共

- 私人的

- 按充電服務類型

- 電動車充電服務

- 電池更換服務

- 按充電基礎設施類型

- CHAdeMO

- CCS

- 國標快速充電器

- 特斯拉超級充電站

- 其他充電基礎設施類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東和非洲

- 北美洲

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- ABB Ltd

- ChargePoint Inc.

- Schneider Electric SE

- Siemens AG

- Tesla Motors Inc.

- Evbox(ENGIE)

- BYD Company

- Leviton Manufacturing Co. Inc.

- SemaConnect Inc.

- The Newmotion BV(Acquired by Shell)

- EFACEC Power Solutions SGPS

- EV Solutions(Webasto)

- Chargemaster Limited(BP Pulse)

- Qingdao Tgood Electric Co. Ltd

- Wanbang Digital Energy Pte. Ltd(Star Charge)

第7章 市場機會與未來趨勢

- 未來 V2G 和物聯網充電基礎設施的採用將會增加

第8章 市場規模和基於數量的預測

第9章 各地區/國家電動車充電相關法規結構分析

The Electric Vehicle Charging Station Market size is estimated at USD 43.03 billion in 2025, and is expected to reach USD 136.34 billion by 2030, at a CAGR of 25.94% during the forecast period (2025-2030).

The electric vehicle charging station market is gaining momentum as more people are turning toward electric vehicles due to their cost-effectiveness and eco-friendliness, enactment of stringent emission and fuel economy norms, government incentives, and availability of budget-friendly models, which is generating demand for charging stations.

Thus, the increasing penetration of electric vehicles in the automotive industry and rising vehicle sales have augmented the market's growth. Moreover, the rapid implementation of stringent government regulations to curb automobile emissions and increase battery efficiency has catalyzed the demand for electric vehicles in the automobile industry, increasing the demand for charging infrastructure.

Despite the initial setbacks, the electric vehicle charging station market has shown resilience. Governments worldwide started prioritizing sustainable transportation solutions after COVID-19, which include investments in electric vehicle charging infrastructure to stimulate economic growth and create jobs.

Consumers' stance toward EV charging stations has been positive so far, with a growing demand for fast charging and easy accessibility. However, there are still concerns about the cost and reliability of charging infrastructure, which presents an opportunity for companies to innovate and improve their offerings.

Electric Vehicle Charging Station Market Trends

Passenger Cars are Leading the Electric Vehicle Charging Station Market

The passenger car segment is the largest in the electric vehicle charging stations market. This is primarily due to the higher volume of passenger cars compared to commercial vehicles and the increasing adoption of electric passenger vehicles globally. Passenger cars account for a significantly higher portion of EV sales, driving the demand for charging infrastructure to support their charging needs.

- According to the International Energy Agency (IEA), global sales of electric vehicles increased by around 32.38% in 2023, surpassing 13 million for the first time, even though car sales broadly were soft in 2022.

As more people become aware of the environmental impacts of traditional gasoline-powered cars, there is a growing interest in electric cars. Rising fuel prices have also driven the penetration of electric vehicles in the automobile industry, which plays a significant role in stimulating the demand for charging stations.

Moreover, the ride-hailing and car-sharing markets are expected to increase the demand for charging stations. Ride-hailing and car-sharing vehicles are typically used for longer periods and experience higher utilization rates than privately owned vehicles. This means that they need to be charged more frequently, which increases the demand for charging stations.

Even though the rise does point to a trend in the drive toward electrifying vehicles, it is insufficient to reduce global CO2 emissions. According to the IEA, CO2 emissions from SUVs, the most common type of vehicle purchased, were estimated to reach almost a billion tons by 2022. Owing to this concern, key automakers are offering electric SUVs to gain market traction.

- For instance, in January 2023, BYD, by Warren Buffet, launched its first passenger car in India, an electric sport-utility vehicle (SUV), marking its entry into the mainstream market as part of a broader global expansion. BYD introduced the Atto 3 electric SUV, which is equipped with its renowned Blade battery technology, with the goal of capturing 40% of the country's electric car market by 2030. The move is part of a larger global push by the Chinese automaker, which has begun selling EVs and plug-in hybrids in countries such as Norway, New Zealand, Singapore, Brazil, Costa Rica, and Colombia.

The above-mentioned developments and factors are expected to contribute to the growth of the passenger cars segment of the EV charging station market.

Asia-Pacific to be the Fastest Growing Region During the Forecast Period

The fastest-growing region in the electric vehicle (EV) charging stations market is Asia-Pacific (APAC). Several key factors have propelled the region to the forefront of EV adoption and charging infrastructure development. China and India, in particular, stand out as major contributors to the growth of the EV charging market in APAC.

One of the primary catalysts of the market's growth in the APAC region is the strong government support and policies promoting electric mobility and charging infrastructure deployment. Countries like China, India, Japan, and South Korea have implemented ambitious targets and incentives to accelerate the adoption of electric vehicles and the expansion of charging infrastructure networks. For example,

- China's New Energy Vehicle (NEV) credit system and subsidy programs have led to a surge in investments in EV charging infrastructure, leading to a rapid increase in the number of charging stations across the country.

- Similarly, Japan's METI's "Guidelines for Promoting the Development of EV Charging Infrastructure" have set targets for the installation of up to 300,000 EV charging ports by 2035.

Furthermore, the rapid urbanization and population growth in APAC countries have increased the demand for sustainable transportation solutions, including electric vehicles and charging stations. Urban areas with dense populations and high levels of pollution are particularly incentivized to transition to cleaner transportation alternatives, leading to a surge in EV adoption and charging infrastructure deployment.

Technological advancements and innovation in EV charging technology have contributed to the growth of the market in APAC. Key players operating in the region are developing advanced charging solutions, including fast-charging systems, wireless charging technology, and smart charging networks, to address the evolving needs of consumers and businesses.

- For instance, in November 2023, Lotus, the UK-based automaker, introduced its suite of electric vehicle (EV) charging solutions, including an ultra-fast 450 kW DC charger, a power cabinet, and a modular unit capable of charging up to four vehicles simultaneously. These new charging solutions are specifically designed for the Indian market. The Liquid-Cooled All-in-One DC Charger is a cutting-edge charger that provides ultra-fast charging at rates of up to 450 kW.

Overall, the market studied in Asia-Pacific is expected to record a significant CAGR in the coming years, owing to government support, urbanization trends, and technological innovations.

Electric Vehicle Charging Station Industry Overview

The electric vehicle charging station market is moderately consolidated. The market is led by a few companies, such as ABB, Siemens, BYD Company, Siemens AG, and Tesla Inc. The key players are engaged in continuously improving their product offerings through R&D investments, integration of advanced technology, product collaboration, and innovation of existing product lines.

- January 2023: ABB E-mobility signed a global framework agreement to support Scania globally with EV charging solutions. ABB's E-mobility portfolio will enable Scania to provide complete EV solutions for customers, electrifying its fleet and supplying vehicles, chargers, services, and software globally.

- February 2023: FLO announced the FLO Ultra, an ultra-fast charger designed to maximize energy delivery while providing future-proof performance and a smart design for the ultimate EV charging experience.

- March 2023: Okaya, a subsidiary of Okaya Power Group, established a strategic alliance with Prakriti E-Mobility, a fleet operator of electric 4 W cars, to provide charging stations for its fleet operations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising EV Sales and Decreasing EV Prices are Driving the Market

- 4.2 Market Restraints

- 4.2.1 High Initial Cost of Installing and Maintaining a Standard EV Charging Station is a Challenge

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD billion)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Charger Type

- 5.2.1 AC Charging Station

- 5.2.2 DC Charging Station

- 5.3 By Charging Ownership Type

- 5.3.1 Public

- 5.3.2 Private

- 5.4 By Charging Service Type

- 5.4.1 EV Charging Services

- 5.4.2 Battery Swapping Services

- 5.5 By Charging Infrastructure Type

- 5.5.1 Chademo

- 5.5.2 CCS

- 5.5.3 GB/T Fast Charge

- 5.5.4 Tesla Superchargers

- 5.5.5 Other Charging Infrastructure Types

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 South America

- 5.6.4.2 Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 ABB Ltd

- 6.2.2 ChargePoint Inc.

- 6.2.3 Schneider Electric SE

- 6.2.4 Siemens AG

- 6.2.5 Tesla Motors Inc.

- 6.2.6 Evbox (ENGIE)

- 6.2.7 BYD Company

- 6.2.8 Leviton Manufacturing Co. Inc.

- 6.2.9 SemaConnect Inc.

- 6.2.10 The Newmotion BV (Acquired by Shell)

- 6.2.11 EFACEC Power Solutions SGPS

- 6.2.12 EV Solutions (Webasto)

- 6.2.13 Chargemaster Limited (BP Pulse)

- 6.2.14 Qingdao Tgood Electric Co. Ltd

- 6.2.15 Wanbang Digital Energy Pte. Ltd (Star Charge)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 There will be an Increased Adoption of V2G and IoT-enabled Charging Infrastructure in Coming Years

8 MARKET SIZE AND FORECAST IN TERMS OF VOLUME

9 ANALYSIS OF REGULATORY FRAMEWORKS RELATED TO EV CHARGING ACROSS DIFFERENT REGIONS/COUNTRIES

直流快速電動車充電站市場規模、佔有率和成長分析(按充電基礎設施、充電類型、最終用戶和地區)- 產業預測 2025-2032

直流快速電動車充電站市場規模、佔有率和成長分析(按充電基礎設施、充電類型、最終用戶和地區)- 產業預測 2025-2032 電動車 (EV) 充電站市場:全球 2025-2029 年

電動車 (EV) 充電站市場:全球 2025-2029 年 印度的電動車充電站市場評估:各類型,各充電器類型,各充電所有者類型,各連接器類型,各終端用戶,各地區,機會,預測,2018年~2032年

印度的電動車充電站市場評估:各類型,各充電器類型,各充電所有者類型,各連接器類型,各終端用戶,各地區,機會,預測,2018年~2032年 電動車充電站市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

電動車充電站市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 全球固定式電動車充電槍市場:產業分析、規模、佔有率、成長、趨勢與預測,2025-2032年

全球固定式電動車充電槍市場:產業分析、規模、佔有率、成長、趨勢與預測,2025-2032年 2025-2033 年電動車充電站市場報告(按充電站類型、車輛類型、安裝類型、充電水平、連接器類型、應用和地區分類)電動車充電站能源基礎設施市場規模、佔有率和成長分析(按充電器類型、應用、連接器類型、充電等級和地區)- 2025-2032 年產業預測全球太陽能充電台市場分析與預測(至2033年):類型、產品、服務、技術、組件、應用、材料類型、部署、最終用戶、功能電動車 (EV) 充電站市場規模、佔有率、成長分析、按充電等級、按模式、按連接階段、按直流快速充電類型、按充電點類型、按安裝類型、按地區- 產業預測,2025-2032年年

2025-2033 年電動車充電站市場報告(按充電站類型、車輛類型、安裝類型、充電水平、連接器類型、應用和地區分類)電動車充電站能源基礎設施市場規模、佔有率和成長分析(按充電器類型、應用、連接器類型、充電等級和地區)- 2025-2032 年產業預測全球太陽能充電台市場分析與預測(至2033年):類型、產品、服務、技術、組件、應用、材料類型、部署、最終用戶、功能電動車 (EV) 充電站市場規模、佔有率、成長分析、按充電等級、按模式、按連接階段、按直流快速充電類型、按充電點類型、按安裝類型、按地區- 產業預測,2025-2032年年 住宅電動車充電市場分析與預測(2024-2033):單戶與多戶建築的智慧電動車充電技術

住宅電動車充電市場分析與預測(2024-2033):單戶與多戶建築的智慧電動車充電技術