|

市場調查報告書

商品編碼

1687172

小型液化天然氣 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Small-scale LNG - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

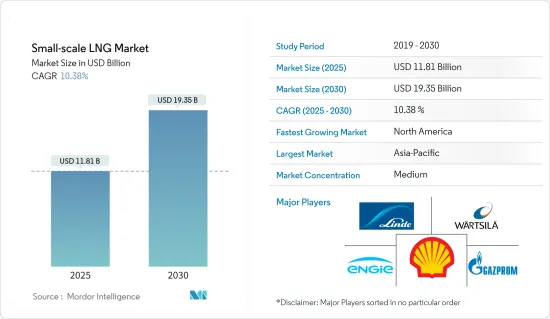

小型液化天然氣市場規模預計在 2025 年為 118.1 億美元,預計到 2030 年將達到 193.5 億美元,預測期內(2025-2030 年)的複合年成長率為 10.38%。

關鍵亮點

- 從長遠來看,燃料庫、道路運輸和離網電力對液化天然氣的需求不斷成長等因素將在未來幾年推動小規模液化天然氣市場的發展。

- 另一方面,小型液化天然氣營業成本高、中東和非洲等地區缺乏配套基礎設施、資本支出要求高以及超過12年的長期回收期等因素預計將阻礙市場成長。

- 然而,由於小型液化天然氣基礎設施所需的資本支出較高,開發具有成本效益的小型液化天然氣基礎設施預計將為小型液化天然氣技術供應商和運輸商提供重大機會。

- 亞太地區佔據市場主導地位,預測期內可能以顯著的複合年成長率成長。

小型液化天然氣市場趨勢

預計運輸領域將主導市場

- LNG主要用作卡車和船舶的燃料,主要是因為它在經濟和環境方面優於柴油和燃料油。 LNG無腐蝕性、無毒,可使車輛的使用壽命延長三倍。此外,由於液化天然氣的沸點極低,因此在高壓下僅需少量的熱量和可忽略不計的機械能即可將其轉化為氣態。這使得液化天然氣成為一種高效率的運輸燃料。

- 處理液化天然氣是一項艱鉅的任務,因為即使是微小的溫差也可能導致燃料沸騰和汽化。這使得乘用車的實用性遠不及商用卡車等大型車輛。這限制了液化天然氣在運輸領域的使用。

- 使用液化天然氣作為運輸燃料在世界各地日益普及。中國、美國和歐洲已經開始部署以液化天然氣為燃料的卡車,主要用於遠距貨運。這主要歸功於政府在脫碳和控制排放氣體方面的政策和舉措,例如中國六號排放標準和歐洲綠色交易。

- 歐盟委員會於2019年制定的《歐洲綠色交易》是一系列舉措舉措,旨在2050年使歐洲實現碳中和。該措施簡潔地強調了液化天然氣在實現目標中的重要性,並強調使用液化天然氣作為卡車和船舶的燃料。

- 根據殼牌《2024年液化天然氣展望》,截至2023年,共有469艘液化天然氣燃料船舶投入營運,另有537艘液化天然氣燃料船舶訂單。隨著越來越多的船東和營運商意識到液化天然氣對環境和氣候的益處,液化天然氣燃料船舶的訂單成長速度比以往任何時候都要快。

- 新興經濟體也計劃為未來運輸使用液化天然氣奠定基礎。例如,Venture World LNG 於 2024 年 3 月開始建造其液化天然氣船隊。該船隊包括目前在韓國建造的 9 艘船舶——其中 6 艘載貨能力為 174,000 立方米,3 艘載貨能力為 200,000 立方米。

- 因此,由於上述因素,預測期內運輸領域對小型液化天然氣基礎設施的需求可能會成長,並在很大程度上主導市場。

亞太地區佔市場主導地位

- 近年來,亞太地區已成為全球實施小型液化天然氣計劃的先驅。隨著中國、印度、新加坡和日本等國家對天然氣的需求不斷成長,近年來人們對使用小型液化天然氣(SSLNG)的興趣也日益濃厚。

- 中國是世界主要國家之一,帶動液化天然氣需求增加。 2022年液化天然氣進口量約6,440萬噸。需求激增使中國成為世界上最大的液化天然氣進口國之一。隨著中國液化天然氣買家簽署每年超過 2,000 萬噸的長期契約,需求也隨之增加。

- 中國的天然氣市場由國內生產和透過管道和液化天然氣終端進口組成。在中國,工業、住宅和發電領域對小型液化天然氣的需求正在成長,其中運輸領域的潛力最大。柴油價格相對於天然氣的高企,推動了道路上液化天然氣卡車數量的增加,預計將成為中國小型液化天然氣設施興起的主要原因。

- 在印度,小規模液化天然氣尚處於起步階段。不過,LNG站有好幾座,而且LNG是用LNG卡車運輸的。為了在2030年將天然氣在其能源結構中的比例提高到15%,印度可能會建造小型液化天然氣設施,向沒有管道基礎設施的偏遠地區供應天然氣。例如,2022 年 6 月,國有天然氣探勘和生產公司 GAIL Limited 宣布,其計劃在未連接液化天然氣管道的地區建立小型液化設施。

- 2024年3月,印度石油和天然氣部長為印度首個小型液化天然氣裝置推出,該裝置由印度天然氣公司在中央邦維賈伊普爾設立。

- 新加坡港的液化天然氣燃料庫設施正在推動新加坡小規模液化天然氣業務。新加坡是一個主要的貿易港口,在國際航運領域中處於世界領先地位。

- 因此,鑑於上述情況,預計亞太地區將在預測期內主導小型市場的成長。

小型液化天然氣產業概況

小型液化天然氣市場較為分散。市場的主要企業(不分先後順序)包括林德集團 (Linde PLC)、瓦錫蘭集團 (Wartsila Oyj ABP)、殼牌集團 (Shell PLC)、Engie SA 和 PJSC Gazprom。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 至2029年的市場規模及需求預測(單位:美元)

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 增加對液化天然氣基礎設施的投資

- 燃料庫、道路運輸和離網電力對液化天然氣的需求不斷增加

- 限制因素

- 中東和非洲等地區缺乏基礎設施

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場區隔

- 類型

- 液化終端

- 再氣化終端

- 供貨形式

- 追蹤

- 轉運和燃料庫

- 管道和鐵路

- 應用

- 運輸

- 工業原料

- 發電

- 其他

- 市場分析:按地區分類的市場規模和到 2028 年的需求預測(按地區分類)

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 俄羅斯

- 西班牙

- 北歐的

- 義大利

- 土耳其

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 越南

- 馬來西亞

- 印尼

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 卡達

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- 小型液化天然氣技術供應商

- Linde PLC

- Wartsila Oyj ABP

- Baker Hughes Company

- Honeywell UoP

- Chart Industries Inc.

- Black & Veatch Holding Company

- 小型液化天然氣海運公司

- Anthony Veder Group NV

- Engie SA

- Evergas AS

- 小型液化天然氣營運商

- Shell PLC

- Eni SpA

- PJSC Gazprom

- TotalEnergies SE

- Gasum Oy

- 市場排名/佔有率(%)分析

- 小型液化天然氣技術供應商

第7章 市場機會與未來趨勢

- 開發具有成本效益的小型液化天然氣基礎設施

簡介目錄

Product Code: 55955

The Small-scale LNG Market size is estimated at USD 11.81 billion in 2025, and is expected to reach USD 19.35 billion by 2030, at a CAGR of 10.38% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as increasing demand for LNG in bunkering, road transportation, and off-grid power will drive the small-scale LNG market in the coming years.

- On the other hand, factors such as the high operation cost of small-scale LNG, lack of supporting infrastructure in regions such as the Middle East and Africa, and high CAPEX requirements, along with a long payback period of more than 12 years, are expected to hinder the growth of the market.

- However, owing to the high capital expenditure required for a small-scale LNG infrastructure, developing cost-efficient small-scale LNG infrastructure is expected to provide significant opportunities to small-scale LNG technology providers and transporters.

- The Asia-Pacific region dominates the market and will likely witness a significant CAGR during the forecast period.

Small-scale LNG Market Trends

The Transportation Segment Expected to Dominate the Market

- LNG is primarily used to fuel trucks and ships, mainly due to its economic and environmental benefits, compared to diesel and fuel oil. Since LNG is non-corrosive and non-toxic, it can extend the life of a vehicle by up to three times. Moreover, since LNG has an extremely low boiling point, very little heat is required to convert it into a gaseous form at high pressure, with negligible mechanical energy. This makes LNG an efficient fuel for transportation.

- Handling LNG is an immense task since even a slight difference in the temperature can lead to the boiling and vaporization of fuel, which, in turn, leads to fuel wastage. Therefore, it makes passenger cars far less viable than heavy vehicles, such as commercial trucks. This has limited the application of LNG in the transportation segment.

- The use of LNG as a transportation fuel is gaining momentum across the world. China, the United States, and Europe have already started deploying LNG-powered trucks, mainly for long-distance freight carriage. This is mainly due to the government policies and regulations on decarbonizing and emission control, such as China VI and the European Green Deal.

- Formed in 2019 by the European Commission, the European Green Deal is a set of policy initiatives to make Europe carbon-neutral by 2050. The policies briefly underline the importance of LNG in reaching the aim, and they emphasize the usage of LNG as fuel for trucks and marine vessels.

- According to Shell LNG Outlook 2024, as of 2023, there were 469 LNG-fueled vessels in operation, and 537 LNG-fueled vessels were on order. The rapidly growing order book for LNG-fuelled vessels has witnessed rapid growth compared to previous years, and increasing numbers of ship owners and operators understand LNG's environmental and climate benefits.

- New emerging economies are also planning to lay the foundation for the future of LNG for transportation. For instance, in March 2024, Venture Global LNG started the construction of a new large fleet of LNG-powered vessels. The fleet includes nine vessels (Six vessels having a cargo capacity of 174,000 m3 and three with a cargo capacity of 200,000 m3) currently under construction in South Korea.

- Hence, owing to the above-mentioned factors, the demand for small-scale LNG infrastructure for the transportation segment will likely grow and significantly dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

- In recent years, Asia-Pacific has been a pioneer in implementing small-scale LNG projects globally. Interest in using small-scale LNG (SSLNG) has increased in recent years as the demand for natural gas increases in countries like China, India, Singapore, and Japan.

- China is one of the world's major countries, which led to the growth in LNG demand. LNG imports totaled around 64.4 million tons in 2022. Due to this surge in demand, China became one of the world's largest LNG importers. The increased demand is due to Chinese LNG buyers signing long-term contracts for more than 20 million tons annually.

- China's natural gas market includes domestic production and import via pipelines and LNG terminals. In China, the rising demand for small-scale LNG is from the industrial, residential, and power generation sectors, with the highest potential being in the transportation sector. Growth in the number of LNG trucks due to the higher price of diesel, compared to natural gas, is expected to be the prime reason small LNG facilities are growing in China.

- In India, small-scale LNG is in a very nascent stage. However, there are a few LNG stations where LNG transportation through LNG trucks is taking place. To increase the share of natural gas to 15% in its energy mix by 2030, India will likely construct small-scale LNG facilities for natural gas supply to remote places with no pipeline infrastructure. For instance, in June 2022, GAIL Limited, a government-owned natural gas explorer and producer company, aimed to set up small liquefaction facilities for areas not connected to LNG pipelines.

- In March 2024, the Union Minister of Petroleum and Natural Gas of India launched the country's first small-scale LNG unit set up by GAIL at Vijaipur in Madhya Pradesh.

- The LNG bunkering facilities in the ports of Singapore majorly drive small-scale LNG business in Singapore. Singapore has one of the leading trade ports and is one of the global leaders in international marine shipping.

- Therefore, owing to the above points, Asia-Pacific is expected to dominate the growth of the small-scale market during the forecast period.

Small-scale LNG Industry Overview

The small-scale LNG market is semi-fragmented. Some of the major players in the market (in no particular order) include Linde PLC, Wartsila Oyj ABP, Shell PLC, Engie SA, and PJSC Gazprom.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investment in LNG Infrastructure

- 4.5.1.2 Rising Demand for LNG in Bunkering, Road Transportation, and Off-grid Power

- 4.5.2 Restraints

- 4.5.2.1 Lack of Supporting Infrastructure in the Regions such as the Middle East and Africa

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Liquefaction Terminal

- 5.1.2 Regasification Terminal

- 5.2 Mode of Supply

- 5.2.1 Truck

- 5.2.2 Transshipment and Bunkering

- 5.2.3 Pipeline and Rail

- 5.3 Application

- 5.3.1 Transportation

- 5.3.2 Industrial Feedstock

- 5.3.3 Power Generation

- 5.3.4 Other Applications

- 5.4 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 NORDIC

- 5.4.2.7 Italy

- 5.4.2.8 Turkey

- 5.4.2.9 Rest of the Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Vietnam

- 5.4.3.6 Malaysia

- 5.4.3.7 Indonesia

- 5.4.3.8 Australia

- 5.4.3.9 Rest of the Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of the Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Small-scale LNG Technology Providers

- 6.3.1.1 Linde PLC

- 6.3.1.2 Wartsila Oyj ABP

- 6.3.1.3 Baker Hughes Company

- 6.3.1.4 Honeywell UoP

- 6.3.1.5 Chart Industries Inc.

- 6.3.1.6 Black & Veatch Holding Company

- 6.3.2 Small-scale LNG Marine Transporter

- 6.3.2.1 Anthony Veder Group NV

- 6.3.2.2 Engie SA

- 6.3.2.3 Evergas AS

- 6.3.3 Small-scale LNG Operators

- 6.3.3.1 Shell PLC

- 6.3.3.2 Eni SpA

- 6.3.3.3 PJSC Gazprom

- 6.3.3.4 TotalEnergies SE

- 6.3.3.5 Gasum Oy

- 6.3.4 Market Ranking/Share (%) Analysis

- 6.3.1 Small-scale LNG Technology Providers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Development of Cost-efficient Small-scale LNG Infrastructure

02-2729-4219

+886-2-2729-4219

2025 年小型液化天然氣全球市場報告

2025 年小型液化天然氣全球市場報告 2025 年至 2033 年小型液化天然氣市場報告,按終端類型、供應方式、儲槽類型(加壓槽、常壓槽、浮動儲槽)、應用和地區分類

2025 年至 2033 年小型液化天然氣市場報告,按終端類型、供應方式、儲槽類型(加壓槽、常壓槽、浮動儲槽)、應用和地區分類 小型液化天然氣市場規模、佔有率、成長分析,按類型、供應模式、儲存槽容量、應用、最終用途、地區 - 產業預測,2025-2032

小型液化天然氣市場規模、佔有率、成長分析,按類型、供應模式、儲存槽容量、應用、最終用途、地區 - 產業預測,2025-2032 亞太地區小型液化天然氣 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)小型液化天然氣市場:按特徵、類型、應用和供應模式分類 - 2025-2030 年全球預測

亞太地區小型液化天然氣 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)小型液化天然氣市場:按特徵、類型、應用和供應模式分類 - 2025-2030 年全球預測 全球小型液化天然氣市場 - 2024-2031

全球小型液化天然氣市場 - 2024-2031 小型液化天然氣市場規模/佔有率/趨勢分析報告:按類型、供應形式、應用、地區、細分市場預測,2024-2030

小型液化天然氣市場規模/佔有率/趨勢分析報告:按類型、供應形式、應用、地區、細分市場預測,2024-2030 小型液化天然氣市場 - 全球產業規模、佔有率、趨勢、機會和預測,2018-2028F 按類型、供應方式、儲槽容量(常壓、加壓和浮動儲存)、應用、按地區、競爭細分

小型液化天然氣市場 - 全球產業規模、佔有率、趨勢、機會和預測,2018-2028F 按類型、供應方式、儲槽容量(常壓、加壓和浮動儲存)、應用、按地區、競爭細分 全球小型液化天然氣市場:按類型、應用、供應方式和地區劃分 - 預測(至 2028 年)

全球小型液化天然氣市場:按類型、應用、供應方式和地區劃分 - 預測(至 2028 年)