|

市場調查報告書

商品編碼

1687280

暖通空調服務:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)HVAC Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

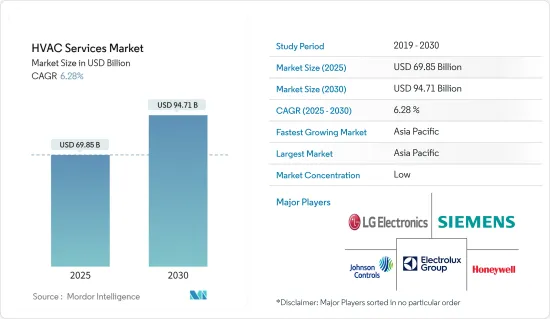

預計 2024 年 HVAC 服務市場規模為 657.2 億美元,到 2029 年將達到 891.1 億美元,預測期內(2024-2029 年)的複合年成長率為 6.28%。

人們對健康的擔憂日益加劇,導致對 HVAC 設備的需求增加、住宅和商業區建設增加以及資料中心市場的成長,從而推動了 HVAC 市場的發展。

關鍵亮點

- 區域供熱、熱泵、使用可再生能源和氫氣供熱等清潔供熱技術正在全球範圍內得到越來越廣泛的應用,以滿足永續發展情景(SDS),這推動了服務的採用並對市場需求產生積極影響。

- 此外,世界各地的建築業也呈指數級成長。公共和私營部門都正在接受綠色建築的概念,為暖通空調服務創造了巨大的成長機會。

- 資料中心的爆炸性需求吸引了各類投資者的關注:成長資本、收購、房地產以及最近的基礎設施投資者。資料中心通常由銀行、雲端供應商、通訊業者等大型公司或主機託管公司擁有和經營,用於各種目的。後者出租空間並列出網路容量、電力和冷卻設備以保持伺服器涼爽。租戶自備 IT 設備。

- 勞動力短缺被視為發展暖通空調服務市場面臨的關鍵挑戰。然而,儘管面臨這些挑戰,但由於製造商和其他服務提供者採取了各種必要措施,市場仍然蓬勃發展。

- 在新冠疫情爆發後,世界各國政府都增加了醫療保健支出並發展了高效的基礎設施。例如,印度政府正在用現代設備和技術維修舊的政府醫院。預計這將增加對 HVAC 服務的需求。然而,通貨膨脹和利率上升進一步減少了消費者支出,阻礙了暖通空調設備的年比銷售,並限制了暖通空調服務的成長。

暖通空調市場趨勢

住宅領域佔據主要市場佔有率

- 人口實驗室估計,世界人口將從2022年的79億增加到2023年的80.1億。預計2023年都市化程度將達57%,並有望在未來幾年繼續增加。由於人口成長、都市化和住宅,住宅領域對暖通空調服務的需求很高,導致新系統的安裝。各個社區正在採取預防性措施來保護住宅,以避免未來出現問題。這包括維護和修理住宅HVAC 系統,包括解決洩漏、腐蝕以及冷熱空氣循環問題。

- 在住宅領域,定期維護和維修對於確保 HVAC 系統的最佳性能至關重要。定期進行 HVAC 維護和維修的主要好處之一是能夠最大限度地提高系統的效率。如果沒有適當的維護,您的系統可能難以正常運行,從長遠來看,這可能會導致能源消費量增加和成本上升。隨著住宅領域對高效實踐的需求不斷增加,對 HVAC 服務的需求也可能增加。

- 在歐洲、美國和亞洲等各個地區,越來越多的消費者正在減少二氧化碳的消費量,以應對全球暖化。為了盡量減少對環境的影響,這些消費者選擇 HVAC 服務來升級或維護現有的 HVAC 系統以用於暖氣和冷氣。

- 例如,在歐洲,永續能源辦公室向安裝熱泵系統的住宅提供財務獎勵,使他們能夠降低能源成本並減少碳排放。這些促進 HVAC 服務採用的措施預計將提升整個住宅領域的市場潛力。

- 印度和中國等國家對節能暖通空調設備的需求激增是由於該地區住宅和人口不斷增加。隨著越來越多的住宅建成,對這些設備和服務的需求也在增加。此外,新基礎設施開發計劃的推出預計將增加對節能 HVAC 解決方案的需求,從而增加對基本 HVAC 服務的需求。

亞太地區預計將創下最快成長

- 中國「十四五」計畫強調水利、能源、交通和都市化等領域的新基礎建設計劃。 「十四五」期間(2021-2025年)新基建投資總額預計將達到約27兆元人民幣(4.2兆美元)。新規劃強調了綠色建築發展和能源效率的九個重點領域。要求維修建築3.5億平方公尺以上,新建淨零能耗建築5000萬平方公尺以上。預計將擴大研究市場。

- 印度的IT基礎設施正在快速發展,各大公司都在積極投資新的資料中心。例如,亞馬遜網路服務宣佈於 2022 年 11 月推出AWS 亞太地區(海得拉巴)區域,這是其在印度的第二個基礎設施區域。第二個基礎設施區域為客戶提供了更多選擇,以更高的彈性和可用性運行他們的工作負載,在印度安全地儲存資料,並以更低的延遲為他們的最終用戶提供服務。 AWS 估計,到 2030 年,海得拉巴地區將透過印度計畫投資超過 44 億美元,每年維持超過 48,000 個全職工作。

- 由於在可再生能源、通訊和製造業領域的多項投資,以及政府到2050年減少溫室氣體排放並實現碳中和的目標,日本的建築業正在經歷強勁成長。

- 印尼是亞洲領先的空調市場之一,隨著經濟成長和中等收入階層的增加,家用空調市場預計將進一步成長。在印度尼西亞,大部分市場由小型車型組成,這些車型很容易適應當地的電力和住宅條件。

- 因此,變頻空調這類節能效果高、能滿足市場需求的產品,市場前景看好。根據EIA預測,到2030年,印尼家庭預計將新增2,000萬台空調。

暖通空調產業概況

HVAC 服務市場分散且競爭激烈,有幾家主要企業。市場參與企業專注於擴大其在消費群。這些公司正在利用策略合作措施來增加市場佔有率和盈利。西門子股份公司、霍尼韋爾國際公司、LG 電子公司、伊萊克斯公司和江森自控國際有限公司等該市場的參與者正在收購從事 HVAC 服務技術的新興企業,以增強其生產能力。

- 2023 年 10 月 - Lennox International Inc. 宣布收購 AES Industries Inc. 和 AES Mechanical Service Group Inc.,併入其建築氣候解決方案部門。 AES 將成為 Lennox Commercial 業務部門的一部分,使該公司能夠為 AES 和 Lennox 客戶提供「前端到後端」生命週期整合服務。

- 2023 年 7 月 - 大金舒適科技公司的子公司 AirReps 收購了兩家公司,Integrated Systems and Controls LLC 和 InControl。這些收購與 AirReps 一起將有助於大金滿足商業市場對整合服務的需求。這些整合功能涵蓋大金的 VRV 和小型商用企業,包括服務功能、遠端監控和預測性維護計劃。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 宏觀經濟因素如何影響市場

第5章市場動態

- 市場促進因素

- 主要新興國家建築業的成長

- 資料中心市場成長

- 市場問題

- 勞力短缺/技術純熟勞工成本高

第6章市場區隔

- 依實施類型

- 新建築

- 維修的建築

- 按最終用戶

- 住宅

- 商業設施

- 工業的

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 比荷盧經濟聯盟

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第7章競爭格局

- 公司簡介

- Siemens AG

- Honeywell International Inc.

- LG Electronics Inc.

- Electrolux AB

- Johnson Controls International PLC

- Lennox International Inc.

- Fujitsu General Ltd

- Robert Bosch GmbH

- Ingersoll-Rand PLC

- Carrier Corporation

- Daikin Industries Ltd

- Nortek Global HVAC

第8章投資分析

第9章:市場的未來

The HVAC Services Market size is estimated at USD 65.72 billion in 2024, and is expected to reach USD 89.11 billion by 2029, growing at a CAGR of 6.28% during the forecast period (2024-2029).

The HVAC market is driven by the growing demand for HVAC equipment due to growing health concerns, increasing construction of residential buildings and commercial spaces, and the growing data center market.

Key Highlights

- Clean heating technologies, including district heating, heat pumps, and renewable and hydrogen-based heating, are gaining traction worldwide to meet the Sustainable Development Scenario (SDS), which drives the implementation services and positively influences the market demand.

- The construction industry across the globe is also growing exponentially. The public and private sectors embrace the concept of green building, which presents a significant growth opportunity for HVAC Services.

- The explosion in demand for data centers has attracted the attention of investors of all types, namely growth capital, buyout, real estate, and, increasingly, infrastructure investors. Data centers are generally owned and operated either by big companies such as banks, cloud vendors, or telcos for their purposes or by co-location companies. The latter leases the space and provides network capacity, power, and cooling equipment to lower server temperatures. Tenants bring their IT equipment.

- Labor shortage may be observed as a significant challenge evolving out of the HVAC services market. However, despite these challenges, the market has flourished due to various essential steps manufacturers and other service-providing companies took.

- Post-COVID-19 pandemic, governments wrdwide have increased healthcare spending and built efficient infrastructure. For example, the Government of India is retrofitting old government hospitals with the latest equipment and technology. This is expected to increase the demand for HVAC services. However, rising inflation and interest rates have further decreased consumer spending and hampered the sales of HVAC equipment in the previous year, restricting the growth of HVAC services.

HVAC Market Trends

Residential Segment Holds Major Market Share

- The Population Reference Bureau estimated the global population to be 8.01 billion in 2023 from 7.9 billion in 2022. The degree of urbanization was 57% in 2023, and it is expected to increase in the coming years. The growing population, urbanization, and residential construction have resulted in a high demand for HVAC services in the residential sector, leading to the installation of new systems. In various regions, a proactive and preventative approach is adopted to maintain residential buildings to avert future problems. This encompasses the maintenance and repair of residential HVAC systems, including resolving leaks, corrosion, and any hot or cold air distribution issues.

- Regular maintenance and repairs are essential in the residential sector to ensure optimal performance of HVAC systems. One of the major advantages of regular HVAC maintenance and repairs is the ability to maximize the system's efficiency. Without proper maintenance, the system may face difficulties in functioning, resulting in increased energy consumption and higher costs in the long run. As the demand for efficient practices continues to rise in the residential sector, the need for HVAC services will also increase.

- In various regions like Europe, the United States, Asia, and others, a growing number of consumers are reducing their carbon consumption to combat global warming. To minimize the environmental impact, these consumers opt for HVAC services to upgrade or maintain their existing HVAC systems for heating and cooling purposes.

- For instance, in Europe, the Sustainable Energy Authority offers financial incentives to homeowners who install heat pump systems, enabling them to reduce their energy costs and decrease their carbon emissions. Such initiatives driving the adoption of HVAC services will increase the market's potential across the residential sector.

- The surge in the requirement for energy-efficient HVAC units in nations like India and China can be attributed to the area's escalating housing and population growth. With the construction of more residential properties, the demand for these equipment and services is rising. Furthermore, introducing new infrastructure development projects is anticipated to amplify the need for energy-efficient HVAC solutions, consequently boosting the demand for essential HVAC services.

Asia-Pacific is Expected to Register the Fastest Growth

- China's 14th Five-Year Plan highlights new infrastructure projects in water systems, energy, transportation, and urbanization. According to estimates, overall investment in new infrastructure during the 14th Five-Year Plan period (2021-2025) is likely to reach approximately CNY 27 trillion (USD 4.2 trillion). The new plan emphasizes nine key items for green building development and energy efficiency. It calls for retrofitting over 350 million sq m of buildings and constructing over 50 million sq m of net zero energy consumption buildings. This is expected to boost the market studied.

- In India, with the rapidly growing IT infrastructure, companies are rigorously investing in new data centers, which is expected to propel the studied market. For example, in November 2022, Amazon Web Services announced the launch of its second infrastructure region in India, the AWS Asia-Pacific (Hyderabad) region. This second infra region offers customers more options to run workloads with greater resilience and availability, securely store data in India, and serve end users with lower latency. AWS has estimated the Hyderabad region will sustain more than 48,000 full-time jobs yearly through a planned investment of more than USD 4.4 billion in India by 2030.

- The construction industry in Japan is witnessing robust growth due to several investments in renewable energy, telecommunication, and manufacturing sectors, as well as the government's aim to cut greenhouse gas emissions and achieve carbon neutrality by 2050.

- Indonesia has one of Asia's major air conditioning markets, with estimates for economic growth and an increase in the middle-income class fueling predictions for additional growth in the air conditioner market, primarily for domestic use. Small-sized models account for most of the market because of their adaptability to the local electric power situation and particular home types in Indonesia.

- As a result, Indonesia is a prospective market for goods that may display great energy-saving efficiency, such as inverter-type air conditioners, while still meeting market demands. According to EIA, Indonesian homes are expected to add another 20 million air conditioners by 2030.

HVAC Industry Overview

The HVAC services market is fragmented, favorably competitive, and has several prominent players. The market performers are focusing on expanding their consumer base across foreign countries. These enterprises leverage strategic collaborative initiatives to boost their market share and profitability. Companies such as Siemens AG, Honeywell International Inc., LG Electronics Inc., Electrolux AB, and Johnson Controls International PLC, performing in the market, are also acquiring start-ups working on HVAC services technologies to strengthen their production capacities.

- October 2023 - Lennox International Inc. announced the acquisition of AES Industries Inc. and AES Mechanical Service Group Inc. to the Building Climate Solutions segment. AES will be a part of the Lennox Commercial business segment and enable the delivery of "front-to-back" life-cycle integrated services to AES and Lennox customers.

- July 2023 - Daikin Comfort Technologies subsidiary AirReps acquired two companies, Integrated Systems and Controls LLC and InControl, enhancing the capabilities of AirReps and allowing the company to provide a more comprehensive array of services for its customers. These acquisitions will help Daikin, in conjunction with AirReps, to meet the commercial market's need for integrated services. These combined capabilities will offer Daikin's VRV and Light Commercial business, including service capability, remote monitoring, and predictive maintenance programs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Construction Business in Major Emerging Economies

- 5.1.2 Growing Data Center Market

- 5.2 Market Challenges

- 5.2.1 Labor Shortage/High Costs of Skilled Labor

6 MARKET SEGMENTATION

- 6.1 By Implementation Type

- 6.1.1 New Construction

- 6.1.2 Retrofit Buildings

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Benelux

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.4.4 Rest of Latin America

- 6.3.5 Middle East & Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Honeywell International Inc.

- 7.1.3 LG Electronics Inc.

- 7.1.4 Electrolux AB

- 7.1.5 Johnson Controls International PLC

- 7.1.6 Lennox International Inc.

- 7.1.7 Fujitsu General Ltd

- 7.1.8 Robert Bosch GmbH

- 7.1.9 Ingersoll-Rand PLC

- 7.1.10 Carrier Corporation

- 7.1.11 Daikin Industries Ltd

- 7.1.12 Nortek Global HVAC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

冷氣和暖氣即服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按服務模式、服務類型、最終用戶、地區、競爭細分,2020-2030 年預測

冷氣和暖氣即服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按服務模式、服務類型、最終用戶、地區、競爭細分,2020-2030 年預測 CaaS 和 HaaS(冷氣和暖氣即服務)市場按服務模式、服務類型和最終用戶分類

CaaS 和 HaaS(冷氣和暖氣即服務)市場按服務模式、服務類型和最終用戶分類 美國暖通空調服務:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國暖通空調設備與服務:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)

美國暖通空調服務:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國暖通空調設備與服務:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年) HVAC 服務管理軟體市場:按功能、部署、公司規模分類 - 2025-2030 年全球預測

HVAC 服務管理軟體市場:按功能、部署、公司規模分類 - 2025-2030 年全球預測 2024-2028 年全球暖通空調服務市場

2024-2028 年全球暖通空調服務市場