|

市場調查報告書

商品編碼

1687289

鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Lithium-ion Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

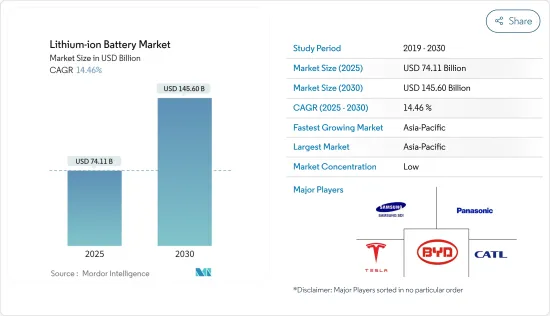

預計 2025 年鋰離子電池市場規模為 741.1 億美元,預計到 2030 年將達到 1,456 億美元,預測期內(2025-2030 年)的複合年成長率為 14.46%。

主要亮點

- 從長遠來看,預計市場將受到電動車、商用和住宅能源儲存系統(ESS) 等新市場的出現、鋰離子電池價格下降以及家用電器銷量增加等因素的推動。

- 另一方面,原料供需不匹配的加劇可能會阻礙市場成長。

- 然而,回收鋰離子電池有望確保鋰和鈷等原料的供應,減少對從礦物來源提取和精製材料的依賴。回收電動車的鋰離子電池為企業利用精製建築材料生產用於能源儲存系統(ESS)的鋰離子電池提供了絕佳機會。

- 亞太地區佔全球市場主導地位,其中中國和印度等國家貢獻最大。隨著電動車的廣泛應用,該地區的市場預計將進一步成長。

鋰離子電池市場趨勢

汽車市場可望佔據市場主導地位

- 鋰離子電池產業發展初期,消費性電子領域是電池的主要消費者。然而近年來,隨著電動車(EV)銷量的成長,電動車(EV)製造商已成為鋰離子電池的最大消費者。

- 電動車對環境的影響比傳統內燃機汽車 (ICE) 小,因為它們不會排放二氧化碳或氮氧化物等溫室氣體。由於這些優勢,許多國家正在推出補貼和政府計劃來鼓勵使用電動車。

- 一些國家已經宣布未來禁止銷售內燃機汽車的計畫。挪威宣布計畫在2025年禁止銷售內燃機汽車,法國計畫在2040年禁止販售,英國計畫在2050年禁止販售。印度也計劃在2030年逐步淘汰內燃機汽車,中國也正處於類似計畫的相關調查階段。

- 此外,鋰離子電池價格下跌可能會對電池市場產生影響。預計至2023年,鋰離子電池價格約為139美元/度,較2013年下降約82.17%。電池成本的大幅下降將使汽車領域受益,並有望長期推動全球鋰離子電池市場的成長。

- 因此,由於上述因素,預計汽車產業將在預測期內佔據市場主導地位。

亞太地區佔市場主導地位

- 由於中國和印度等國家擴大採用可再生能源計劃和電動車,都市化和電力購買平價上升刺激了對電子設備的需求,預計該地區的鋰離子電池將顯著成長。

- 據估計,亞太地區很大一部分人口無法用電力。為了照明和為行動電話充電,我們依靠煤油和柴油等傳統燃料。由於鋰離子電池的技術優勢和價格下降,鋰離子電池整合能源儲存解決方案的採用率預計將增加。因此,預計將為鋰電池製造商創造巨大的商機。

- 中國是最大的電動車市場之一,日益普及符合其清潔能源政策。此外,中國政府也採取財政和非財政獎勵,鼓勵人們使用電動車。

- 印度是世界上鋰離子電池成長最快的國家之一。為了解決這個製造問題,印度國家轉型機構 (NITI) Aayog 於 2020 年 2 月推出了提案,向在印度建立千兆級鋰離子製造工廠的投資者提供補貼。 2020年至2030年間,NITI Aayog可能會邀請競標建立年產能為50 GWh的生產線。因此,預計預測期內鋰離子電池的國內產量將會擴大。

- 根據《巴黎氣候協定》,印度承諾確保2030年其40%的發電能力來自非石化燃料。為實現這一目標,我們計劃在2022年建立175,000MW的可再生能源容量,其中包括100,000kW的太陽能發電。印度的目標是到2030年將可再生能源裝置容量提高到45萬千瓦。為實現這一目標,印度需要龐大的能源儲存解決方案市場,以解決再生能源來源的間歇性問題並提高電網穩定性。

- 根據國際可再生能源機構(IRENA)預測,2023年該地區清潔能源裝置容量將達到2,025萬千瓦,高於上年的1,691.77千萬瓦。

- 因此,由於上述因素,預計亞太地區將在預測期內主導鋰離子電池市場。

鋰離子電池產業概況

鋰離子電池市場比較分散。該市場的主要企業(不分先後順序)包括松下公司、特斯拉公司、三星 SDI、LG 化學有限公司、寧德時代新能源科技(CATL)等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 2029 年市場規模與需求預測

- 2029年鋰離子電池價格趨勢分析

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 政府對可再生能源引進的支持措施和政策

- 鋰離子電池成本下降

- 限制因素

- 原料供需不匹配

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 應用

- 電子產品

- 車

- 固定式儲能(UPS、可再生能源、工業)

- 其他用途(電動工具、醫療設備、其他用途)

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 西班牙

- 北歐的

- 英國

- 俄羅斯

- 土耳其

- 德國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 其他中東和非洲地區

- 北美洲

第6章 競爭格局

- 併購、合資、合作、協議

- 主要企業策略

- 公司簡介

- BYD Company Limited

- Contemporary Amperex Technology Co. Limited

- LG Chem Ltd

- Panasonic Corporation

- Samsung SDI

- Sony Corporation

- Tesla Inc.

- Tianjin Lishen Battery Joint-Stock Co. Ltd

- 市場排名/佔有率分析

第7章 市場機會與未來趨勢

- 鋰離子電池回收需求不斷成長

簡介目錄

Product Code: 60367

The Lithium-ion Battery Market size is estimated at USD 74.11 billion in 2025, and is expected to reach USD 145.60 billion by 2030, at a CAGR of 14.46% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the emergence of new markets via electric vehicles and energy storage systems (ESS) for both commercial and residential applications, declining lithium-ion battery prices, and the increasing sale of consumer electronics are expected to drive the market.

- On the other hand, the rising demand-supply mismatch of raw materials is likely to hinder the market's growth.

- However, recycling Li-ion batteries is expected to secure the supply of raw materials, such as lithium and cobalt, and reduce the reliance on extracting and refining materials from mineral resources. Recycling lithium-ion batteries in electric vehicles offers an excellent opportunity for companies to utilize the refined constituent materials for manufacturing lithium-ion batteries for energy storage systems (ESS).

- Asia-Pacific dominates the market worldwide, with the most significant contributions from countries such as China and India. With the large-scale acceptance of EVs, the market is further expected to grow in the region.

Lithium-ion Battery Market Trends

The Automobile Segment Expected to Dominate the Market

- n the early years of the lithium-ion battery industry, the consumer electronics sector was the major consumer of batteries. However, in recent years, electric vehicle (EV) manufacturers have become the biggest consumers of lithium-ion batteries, owing to the growing sales of EVs.

- EVs do not emit CO2, NOX, or any other greenhouse gases and, hence, have a lower environmental impact than conventional internal combustion engine (ICE) vehicles. Due to this advantage, many countries are encouraging the use of EVs by introducing subsidies and government programs.

- Several countries have announced plans to ban the sales of ICE vehicles in the future. Norway announced plans to ban the sales of ICE vehicles by 2025, France by 2040, and the United Kingdom by 2050. India also has plans to phase out ICE engines by 2030, while China's similar plan is under the relevant research phase.

- Moreover, the decline in lithium-ion battery prices will affect the battery market. In 2023, the lithium-ion battery price was noted to be around USD 139 per kWh, a decrease of around 82.17% from 2013. The plummeting cost of batteries would benefit the automotive segment and propel the growth of the lithium-ion battery market worldwide in the long term.

- Therefore, owing to the above factors, the automobile segment is expected to dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

- With the increasing deployment of renewable energy projects and electric vehicles in countries such as China and India and the high demand for electronics with urbanization and increasing power purchase parity, lithium-ion batteries are expected to witness significant growth in the region.

- A significant fraction of Asia-Pacific's population is estimated to live without electricity access. It depends on conventional fuels, such as kerosene and diesel, for lighting and mobile phone charging. Due to its technical benefits and declining lithium-ion battery prices, lithium-ion battery integrated energy storage solutions are likely to witness an increasing adoption rate. This, in turn, is expected to create significant opportunities for lithium battery manufacturers in the future.

- China is one of the largest markets for electric vehicles, and the country's increasing adoption of electric vehicles has been in line with its clean energy policy. Moreover, the Government of China has been providing financial and non-financial incentives to promote the adoption of electric vehicles.

- India is one of the fastest-growing countries globally for lithium-ion batteries. To counter the manufacturing issue, the National Institution for Transforming India (NITI) Aayog rolled out proposals in February 2020 to provide subsidies for investors setting up giga-scale lithium-ion manufacturing facilities in India. Between 2020 and 2030, the NITI Aayog will likely invite bids to establish production lines with 50 GWh of annual output capacity. Therefore, the indigenous manufacturing of lithium-ion batteries is expected to grow during the forecast period.

- Under the Paris Climate Agreement, India has pledged to have 40% of its electricity generation capacity sourced from non-fossil fuels by 2030. To meet this objective, the nation aimed to establish 175,000 MW of renewable energy capacity, which includes 100,000 MW of solar power, by 2022. A target of 450,000 MW of installed renewable energy capacity by 2030 has been set. To achieve the target, India presents a vast market for energy storage solutions to address the intermittency of renewable energy sources and enhance grid stability.

- According to the International Renewable Energy Agency (IRENA), the installed capacity of clean energy sources in the region in 2023 stood at 2,025 GW, an increase from the previous year's 1,691.77 GW.

- Therefore, owing to the above factors, Asia-Pacific is expected to dominate the lithium-ion battery market during the forecast period.

Lithium-ion Battery Industry Overview

The lithium-ion battery market is fragmented. The major companies in the market (in no particular order) include Panasonic Corporation, Tesla Inc., Samsung SDI, LG Chem Ltd, and Contemporary Amperex Technology Co. Ltd (CATL).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definiton

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Lithium-ion Battery Price Trend Analysis, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Supportive Government Initiatives And Policies To Adopt Renewable Energy

- 4.6.1.2 Declining Cost Of Lithium-ion Batteries

- 4.6.2 Restraints

- 4.6.2.1 Demand-Supply Mismatch of Raw Materials

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Electronic Devices

- 5.1.2 Automobile

- 5.1.3 Stationary Energy Storage (UPS, Renewables, and Industrial)

- 5.1.4 Other Applications (Power Tools, Medical Devices, and Other Applications)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of the North America

- 5.2.2 Europe

- 5.2.2.1 Spain

- 5.2.2.2 Nordic

- 5.2.2.3 United Kingdom

- 5.2.2.4 Russia

- 5.2.2.5 Turkey

- 5.2.2.6 Germany

- 5.2.2.7 Italy

- 5.2.2.8 Rest of the Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Malaysia

- 5.2.3.5 Thailand

- 5.2.3.6 Indonesia

- 5.2.3.7 Vietnam

- 5.2.3.8 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colmbia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Nigeria

- 5.2.5.5 Qatar

- 5.2.5.6 Egypt

- 5.2.5.7 Rest of the Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Limited

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 LG Chem Ltd

- 6.3.4 Panasonic Corporation

- 6.3.5 Samsung SDI

- 6.3.6 Sony Corporation

- 6.3.7 Tesla Inc.

- 6.3.8 Tianjin Lishen Battery Joint-Stock Co. Ltd

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for Recycled Lithium-ion Batteries

02-2729-4219

+886-2-2729-4219

全球Z-L-Valine NCA市場、實績和預測(2020-2031年)

全球Z-L-Valine NCA市場、實績和預測(2020-2031年) 全球鋰離子電池市場

全球鋰離子電池市場 印度鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)東南亞鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

印度鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)東南亞鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球工業鋰離子電池市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球工業鋰離子電池市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 鋰離子電池材料市場(按材料、應用、電池化學和地區分類)- 2029 年預測

鋰離子電池材料市場(按材料、應用、電池化學和地區分類)- 2029 年預測 2025年可充電鋰離子聚合物電池全球市場報告全球鋰離子電池市場評估:依類型、容量、配置、最終用戶、通路、機會和預測2018年至2032年

2025年可充電鋰離子聚合物電池全球市場報告全球鋰離子電池市場評估:依類型、容量、配置、最終用戶、通路、機會和預測2018年至2032年 全球鋰離子電池市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球鋰離子電池市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 工業鋰離子電池市場機會、成長動力、產業趨勢分析及2025-2034年預測

工業鋰離子電池市場機會、成長動力、產業趨勢分析及2025-2034年預測

▼