|

市場調查報告書

商品編碼

1687465

功率半導體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Power Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

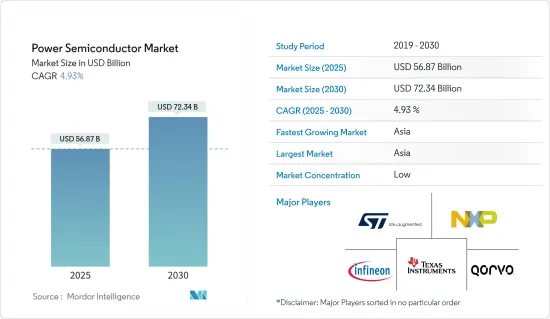

功率半導體市場規模預計在 2025 年達到 568.7 億美元,預計在 2030 年達到 723.4 億美元,在市場估計和預測期(2025-2030 年)內複合年成長率為 4.93%。

功率半導體設計用於處理高電流和功率,通常額定電流為 1A 以上。這些設備用途廣泛,包括消費性電子產品、視聽設備和汽車。

功率半導體徹底改變了電子和能源管理領域。功率半導體的主要優點之一是能夠顯著提高能源效率。透過最大限度地減少轉換和控制過程中的能量損失,功率半導體使系統運作更高效,降低能耗並節省成本。這些裝置具有更高的功率密度、更低的導通電阻和更低的開關損耗,從而提高了整體系統效率。

此外,功率半導體具有更高的功率密度,使其能夠在更小的物理尺寸內處理更多的功率,這對於電動車和工業自動化等空間受限的應用有利。功率半導體透過最大化功率輸出同時最小化空間需求,實現了緊湊、高效的系統的開發。

科技的快速進步是推動家用電子電器和無線通訊需求激增的主要因素之一。科技的不斷發展導致了創新、功能豐富的設備的推出,徹底改變了個人與世界互動的方式。更智慧的智慧型手機、超薄筆記型電腦、高清晰度電視(HDTV)和穿戴式裝置已經成為我們個人和職業生活中不可或缺的工具。這些進步改善了用戶體驗,並促進了對此類設備的需求不斷成長。

矽晶圓是生產功率半導體的基礎。薄圓盤狀矽晶型可作為製造半導體裝置的基板。矽的獨特性質,包括其豐富性、高熱導率和優異的電學性能,使其成為這些應用的理想材料。由於矽晶片適用於高功率應用,因此功率半導體市場嚴重依賴矽晶片。

美國美國預算辦公室預計,2033年,美國國防支出將逐年增加。 2023年,美國國防支出將達7,460億美元。預測顯示,到2033年,國防支出將增加至1.1兆美元。國防支出佔國內生產總值的比例將從2023年的3.9%和2021年的2.7%上升到2024年的6%。全球國防預算的增加預計將為該市場的成長提供有利機會。

功率半導體市場趨勢

汽車產業作為最終用戶正在快速成長

- 在分析汽車領域的功率半導體時,應用包括用於主動車距控制巡航系統、車道偏離警示系統和防撞的 ADAS、用於流暢音樂播放和精確 GPS 功能的資訊娛樂系統、遠端資訊處理和聯網汽車等。它們也用於電動車中,以調節馬達的運作。

- 汽車是功率半導體市場中新興的領域之一,由於自動駕駛汽車、電動車和混合動力汽車的日益普及,預計汽車將佔據主要佔有率。

- 電力電子廣泛應用於汽車電氣和電子系統,以提高燃油效率並解決熱問題。這是透過實施矽基功率 MOSFET 和 IGBT 等組件來實現的,這些組件充當動力傳動系統系統中的電力電子開關。透過採用這些技術,可以利用高功率,同時減少整體系統尺寸。

- 此外,絕緣柵雙極電晶體(IGBT)已成為電動車發展中不可或缺的組成部分。由於電動車銷量的成長,預計未來幾年對 IGBT 的需求將大幅成長。例如,國際能源總署最近的一份報告預測,電動車市場將經歷強勁成長,到2023年銷售量將接近1,400萬輛。電動車的市場佔有率將從2020年的4%左右飆升至2023年的18%,這標誌著消費者偏好向更永續的交通途徑發生重大轉變。

- 預計到2024年,電動車銷量將強勁成長。光是第一季,全球電動車銷量就超過300萬輛,比2023年成長25%。預測顯示,2024年底,電動車總合銷量將達到約1,700萬輛,較去年同期成長20%以上,預計與前一年同期比較新車購買量將大幅加速。這種快速成長主要歸功於國家政策、獎勵和價格競爭加劇等因素的共同作用,這些因素共同增強了銷售並推動了市場向前發展。

中國正在經歷快速成長

- 功率半導體擴大被安裝在電動車中。 MOSFET 和 IGBT 等元件在汽車動力傳動系統系統中充當電力電子開關。市場顯著成長的動力來自於對節能混合動力電動車日益成長的需求,尤其是在中國等國家,以應對日益嚴重的環境污染影響。

- 其中中國是全球最大的汽車市場,年產銷量均居世界之冠。到 2025 年,預計本地生產的汽車數量將達到 3,500 萬輛,這是一個重要的里程碑。

- 展望未來,中國的目標是到2060年實現碳中和,政府措施將推動對電力電子產品的需求。這種成長與更廣泛的市場擴張相吻合,特別是在電動車領域。 《中國新能源汽車產業發展規劃(2021-2035)》預測,到2025年,電動車的市場佔有率將達到25%。因此,中國正在加強獎勵購買電動車,此舉預計將進一步刺激電動車電力電子設備的發展和應用。

- 中國與政府合作在全國推廣5G網路方面取得了長足進步。全國主要通訊業者中國移動、中國聯通、中國電信已在城市中心區和重點區域主導建設完善的5G基礎設施。這項舉措使中國各地數百萬用戶能夠享受快速、可靠的網路服務。目前,基地台部署已進入關鍵階段。

- 預計2023年底,我國5G基地台數量將達338萬個。由於大規模的基礎設施投資和雄心勃勃的推廣計劃,中國已經實現了廣泛的5G覆蓋範圍。預測顯示,到2024年基地台數量將達到600多萬個。

功率半導體產業概況

功率半導體市場較為分散,由幾家全球知名公司組成,包括英飛凌科技股份公司、德州儀器公司、意法半導體公司、恩智浦半導體公司和 Qorvo 公司。此外,在透過創新獲得永續競爭優勢的市場中,隨著終端用戶產業新客戶需求的激增,競爭預計只會加劇。

2024 年 6 月 -美國半導體巨頭德克薩斯和台灣電子專家Delta電子聯手加強電動汽車電力電子技術。兩家公司最初專注於開發更輕、更具成本效益的 11kW 車載充電器,但這只是合作的開始。從長遠來看,TI 和Delta將在台灣平鎮的聯合創新實驗室中結合各自的電源管理和電力傳輸專業知識。兩家公司的目標是透過提高功率密度、增強性能和縮小尺寸來加速更安全、更快、更實惠的電動車的問世。

2024 年 4 月 - 英飛凌科技股份公司與逆變器和能源儲存系統專家 FOXESS 合作。此次合作旨在推動綠色能源舉措。英飛凌的貢獻包括向 FOXESS 提供額定電壓為 1,200 V 的最先進的 CoolSiC MOSFET。這些 MOSFET 與專為工業能源儲存應用而設計的 EiceDRIVER 閘極驅動器結合。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 新冠疫情和其他宏觀經濟因素的後續影響將影響市場

- 技術簡介

第5章市場動態

- 市場促進因素

- 消費性電子產品和無線通訊的需求不斷成長

- 對節能、電池供電攜帶式設備的需求不斷增加

- 市場限制

- 矽晶圓短缺和驅動需求波動

第6章市場區隔

- 按組件

- 離散的

- 整流器

- 雙極

- MOSFET

- IGBT

- 其他分立元件(閘流體和HEMT)

- 模組

- 閘流體

- IGBT

- MOSFET

- 電源IC

- 多通道PMICS

- 開關穩壓器(AC/DC、DC/DC、隔離和非隔離)

- 線性穩壓器

- BMIC

- 其他部分

- 離散的

- 按材質

- 矽/鍺

- 碳化矽(SiC)

- 氮化鎵(GaN)

- 按最終用戶產業

- 車

- 消費性電子產品

- 資訊科技/通訊

- 軍事和航太

- 力量

- 產業

- 其他最終用戶產業

- 按地區

- 美國

- 歐洲

- 日本

- 中國

- 韓國

- 台灣

第7章競爭格局

- 公司簡介

- Infineon Technologies AG

- Texas Instruments Inc.

- Qorvo Inc.

- STMicroelectronics NV

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- Broadcom Inc.

- Toshiba Corporation

- Mitsubishi Electric Corporation

- Fuji Electric Co. Ltd

- Semikron International

- Wolfspeed Inc.

- Rohm Co. Ltd

- Vishay Intertechnology Inc.

- Nexperia Holding BV(Wingtech Technology Co. Ltd)

- Alpha & Omega Semiconductor

- Magnachip Semiconductor Corp.

- Microchip Technology Inc.

- Littlefuse Inc.

8.供應商市場佔有率分析

第9章投資分析

第10章:投資分析市場的未來

The Power Semiconductor Market size is estimated at USD 56.87 billion in 2025, and is expected to reach USD 72.34 billion by 2030, at a CAGR of 4.93% during the forecast period (2025-2030).

Power semiconductors are designed to handle or process large currents and power, and they are typically categorized as having a rated current of 1A or greater. These devices are used in a wide range of applications, including home appliances, audiovisual equipment, automobiles, etc.

Power semiconductors have revolutionized the field of electronics and energy management. One of the key advantages of power semiconductors is their ability to improve energy efficiency significantly. By minimizing energy losses during the conversion and control processes, power semiconductors enable systems to operate more efficiently, reducing energy consumption and saving costs. These devices offer higher power density, lower on-resistance, and reduced switching losses, resulting in higher overall system efficiency.

Moreover, power semiconductors offer higher power density, allowing more power to be handled within a smaller physical footprint, which is beneficial in applications where space is limited, such as electric vehicles and industrial automation. Power semiconductors enable the development of compact and efficient systems by maximizing power output while minimizing space requirements.

Rapid technological advancement is one of the primary drivers of the surging demand for consumer electronics and wireless communication. The continuous evolution of technology has led to the introduction of innovative and feature-rich devices that have revolutionized the way an individual interacts with the world. Smarter smartphones, ultra-slim laptops, high-definition televisions, and wearable gadgets have become essential tools for both personal and professional purposes. These advancements have enhanced the user experience and contributed to the increasing demand for such devices.

Silicon wafers are the foundation of power semiconductor manufacturing. These thin, circular discs of crystalline silicon serve as the substrate upon which semiconductor devices are built. Silicon's unique properties, such as its abundance, high thermal conductivity, and excellent electrical properties, make it an ideal material for these applications. The power semiconductor market heavily relies on silicon wafers due to their suitability for high-power applications.

According to the US Congressional Budget Office, defense spending in the United States is predicted to increase every year until 2033. Defense outlays in the United States amounted to USD 746 billion in 2023. The forecast predicts an increase in defense outlays up to USD 1.1 trillion in 2033. The defense spending would comprise 6% of the country's gross domestic product in 2024, up from 3.9% in 2023 and 2.7% in 2021. The increasing defense budgets globally are expected to offer lucrative opportunities for the growth of the market studied.

Power Semiconductor Market Trends

Automotive Industry to be the Fastest Growing End User

- Analyzing power semiconductors in the automotive segment includes ADAS for adaptive cruise control, lane assistance, collision avoidance, infotainment systems for smooth music playback and accurate GPS functionality, telematics and connected vehicles, and others. Furthermore, they are also used in electric vehicles to coordinate the operations of electric motors.

- Automotive is one of the emerging sectors of the power semiconductors market and is estimated to have a significant share with the increase in the adoption of autonomous vehicles, EVs, and HEVs.

- Power electronics is widely utilized in automotive electrical and electronic systems to enhance fuel efficiency and address thermal concerns. This is achieved by implementing components like silicon-based power MOSFETs and IGBTs, which serve as power electronic switches in the power train system. By employing these technologies, the system's overall size can be reduced while utilizing high power in the kilowatt range.

- Moreover, the Insulated Gate Bipolar Transistor (IGBT) has emerged as an essential component in the development of electric vehicles. In the upcoming years, it is anticipated that the demand for IGBTs will rise significantly due to the rise in EV sales. For instance, according to a recent report from the International Energy Agency, electric car markets experienced robust growth, with sales approaching 14 million in 2023. The market share of electric vehicles surged from approximately 4% in 2020 to 18% by 2023, indicating a significant shift in consumer preferences toward more sustainable transportation options.

- Electric vehicle sales are poised for robust growth through 2024. In the first quarter alone, global sales of electric cars surpassed 3 million, marking a 25% surge compared to 2023. Forecasts suggest a total of approximately 17 million electric vehicles will be sold by the close of 2024, indicating a notable 20%+ year-on-year uptick, with a significant acceleration in new purchases anticipated in the latter half of this year. This surge is largely attributed to a combination of national policies, incentives, and intensifying price competition, all working in tandem to bolster sales and drive the market forward.

China to Witness Major Growth

- Power semiconductors are increasingly prevalent in EVs, as these vehicles demand high-power energy for their electric motors. Components like MOSFETs and IGBT serve as power electronic switches in the vehicles' power train systems. The market's notable growth is fueled by the escalating demand for energy-efficient hybrid electric vehicles, particularly in nations like China, as they combat the effects of mounting environmental pollution.

- Notably, China stands as the world's premier vehicle market, boasting the highest annual sales and manufacturing output. By 2025, the nation is expected to be on track to achieve a significant milestone, with an estimated 35 million vehicles slated for domestic production.

- Looking ahead, as China aims for carbon neutrality by 2060, the government's initiatives are set to bolster the demand for power electronics. This push aligns with the broader market expansion, especially in the electric vehicle segment. China's Development Plan for the New Energy Automobile Industry (2021-2035) projects that EVs could capture a 25% market share by 2025. Consequently, China is intensifying efforts to incentivize EV purchases, a move expected to further propel the development and adoption of power electronics in the EV landscape.

- In collaboration with its government, China made substantial progress in expanding its 5G network nationwide. The country's major telecom operators, China Mobile, China Unicom, and China Telecom, led the construction of robust 5G infrastructure in urban centers and key regions. This initiative enabled millions of users to access high-speed, reliable internet services across China. The deployment of base stations has now reached a critical stage.

- By the end of 2023, the number of 5G base stations in China amounted to 3.38 million. With extensive infrastructure investments and ambitious rollout plans, China has achieved significant 5G coverage. According to forecasts, the number of base stations is projected to reach over six million by 2024.

Power Semiconductor Industry Overview

The power semiconductor market is fragmented and comprises several global and popular players, such as Infineon Technologies AG, Texas Instruments Inc., STMicroelectronics NV, NXP Semiconductors NV, Qorvo Inc., and others. Furthermore, in a market where the sustainable competitive advantage through innovation is considerably high, the competition is expected only to increase, considering the anticipated surge in demand from new customers from the end-user industries.

June 2024 - US semiconductor giant Texas Instruments and Taiwanese electronics expert Delta Electronics joined forces to enhance power electronics for electric vehicles. Their initial focus was on crafting a lighter, more cost-efficient 11 kW onboard charger; this marked just the beginning of their partnership. In the long run, the two firms, TI and Delta, will leverage their joint innovation lab in Pingzhen, Taiwan, pooling their expertise in power management and supply. Their goal is to boost power density, enhance performance, and shrink sizes, all in a bid to hasten the arrival of safer, speedier, and more affordable electric vehicles.

April 2024 - Infineon Technologies AG partnered with FOXESS, which specializes in inverters and energy storage systems. The collaboration was geared toward advancing green energy initiatives. Infineon's contribution includes supplying FOXESS with its cutting-edge CoolSiC MOSFETs rated at 1,200 V. These will be paired with EiceDRIVER gate drivers, tailored explicitly for industrial energy storage applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain/supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Consumer Electronics and Wireless Communications

- 5.1.2 Growing Demand for Energy-Efficient Battery-powered Portable Devices

- 5.2 Market Restraints

- 5.2.1 Shortage of Silicon Wafers and Variable Driving Requirement

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Discrete

- 6.1.1.1 Rectifier

- 6.1.1.2 Bipolar

- 6.1.1.3 MOSFET

- 6.1.1.4 IGBT

- 6.1.1.5 Other Discrete Components (Thyristor and HEMT)

- 6.1.2 Modules

- 6.1.2.1 Thyristor

- 6.1.2.2 IGBT

- 6.1.2.3 MOSFET

- 6.1.3 Power IC

- 6.1.3.1 Multichannel PMICS

- 6.1.3.2 Switching Regulators (AC/DC, DC/DC, Isolated and Non-isolated)

- 6.1.3.3 Linear Regulators

- 6.1.3.4 BMICs

- 6.1.3.5 Other Components

- 6.1.1 Discrete

- 6.2 By Material

- 6.2.1 Silicon/Germanium

- 6.2.2 Silicon Carbide (SiC)

- 6.2.3 Gallium Nitride (GaN)

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Consumer Electronics

- 6.3.3 IT and Telecommunication

- 6.3.4 Military and Aerospace

- 6.3.5 Power

- 6.3.6 Industrial

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 United States

- 6.4.2 Europe

- 6.4.3 Japan

- 6.4.4 China

- 6.4.5 South Korea

- 6.4.6 Taiwan

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Texas Instruments Inc.

- 7.1.3 Qorvo Inc.

- 7.1.4 STMicroelectronics NV

- 7.1.5 NXP Semiconductors NV

- 7.1.6 ON Semiconductor Corporation

- 7.1.7 Renesas Electronics Corporation

- 7.1.8 Broadcom Inc.

- 7.1.9 Toshiba Corporation

- 7.1.10 Mitsubishi Electric Corporation

- 7.1.11 Fuji Electric Co. Ltd

- 7.1.12 Semikron International

- 7.1.13 Wolfspeed Inc.

- 7.1.14 Rohm Co. Ltd

- 7.1.15 Vishay Intertechnology Inc.

- 7.1.16 Nexperia Holding BV (Wingtech Technology Co. Ltd)

- 7.1.17 Alpha & Omega Semiconductor

- 7.1.18 Magnachip Semiconductor Corp.

- 7.1.19 Microchip Technology Inc.

- 7.1.20 Littlefuse Inc.

8 VENDORS MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

功率半導體模組市場按產品類型、材料、額定功率和最終用戶產業分類 - 2025 年至 2030 年全球預測

功率半導體模組市場按產品類型、材料、額定功率和最終用戶產業分類 - 2025 年至 2030 年全球預測 雙極結型電晶體市場,按極性、按性能特徵、按材料類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

雙極結型電晶體市場,按極性、按性能特徵、按材料類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 世界功率半導體市場、材料與技術

世界功率半導體市場、材料與技術 矽 (Si) 電力設備市場規模、佔有率和成長分析(按類型、應用和地區)- 產業預測 2025-2032雙極接面電晶體 (BJTS) 市場規模、佔有率、成長分析、按極性、按性能特徵、按材料類型、按地區 - 行業預測,2025-2032 年全球功率半導體市場:按材料、組件、應用和最終用戶分類 - 2025-2030 年預測全球氧化鎵功率元件市場按類型和最終用途分類 - 機會分析和產業預測(2024-2033)BCD 電源 IC 市場,按產品類型、額定電壓、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

矽 (Si) 電力設備市場規模、佔有率和成長分析(按類型、應用和地區)- 產業預測 2025-2032雙極接面電晶體 (BJTS) 市場規模、佔有率、成長分析、按極性、按性能特徵、按材料類型、按地區 - 行業預測,2025-2032 年全球功率半導體市場:按材料、組件、應用和最終用戶分類 - 2025-2030 年預測全球氧化鎵功率元件市場按類型和最終用途分類 - 機會分析和產業預測(2024-2033)BCD 電源 IC 市場,按產品類型、額定電壓、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 TRIAC 市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測

TRIAC 市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測 全球功率半導體市場(2024-2028)

全球功率半導體市場(2024-2028)