|

市場調查報告書

商品編碼

1687471

NAND快閃記憶體快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)NAND Flash Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

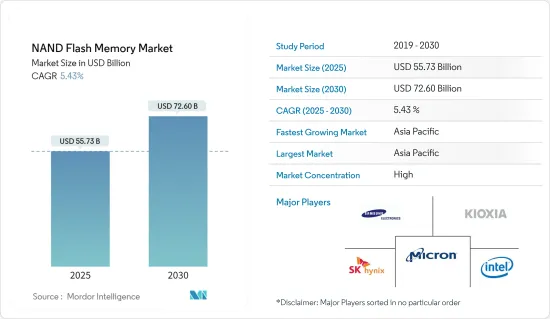

預計 2025 年NAND快閃記憶體市場規模為 557.3 億美元,到 2030 年將達到 726 億美元,預測期內(2025-2030 年)的複合年成長率為 5.43%。

隨著個人電腦和智慧型手機的興起, NAND快閃記憶體的消費量急劇增加,其中很大一部分來自於智慧型手機平均容量的不斷增加。預計這將增加對NAND快閃記憶體封裝的需求,進而影響記憶體封裝需求。

主要亮點

- 市場成長受到多種因素的推動,包括對製造設施的投資增加、邊緣儲存帶來的市場成長以及支援智慧型手機應用的高密度儲存需求不斷成長。

- 3D NAND 需求的不斷成長為晶片製造商、設備製造商和材料供應商等供應鏈成員創造了機會。這推動了對 3D NAND 製造設施的投資。

- 其他消費性產品,如平板電腦、相機、工業設備和感測器、汽車系統和醫療設備與處理器整合在一起,並依靠快閃記憶體來儲存資料和可執行程式碼。隨著人工智慧和機器學習應用對大規模資料處理的需求不斷成長,基於快閃記憶體的儲存趨勢將繼續發展。

- 由於中國是原料和成品的主要供應國之一,預計電子和設備產業將受到 COVID-19 疫情的嚴重影響。該行業面臨產量減少、供應鏈中斷和價格波動等問題。在此期間,知名電子公司的銷售受到了影響。人員和產品旅行限制在短期內阻礙了市場成長。

- 中國NAND快閃記憶體供應商的生產並未受到新型 COVID-19 疫情的嚴重影響。這是因為工廠自動化程度較高,對人力的需求相對較少,經營者也會在農曆新年前囤積原料。由於該半導體製造廠持有特殊的國家許可證,因此代工產品已交貨給中國客戶。這樣,產品就可以運往中國各地,甚至是被隔離的城市。

NAND快閃記憶體的主要市場趨勢

智慧型手機市場預計將出現強勁成長

- 快閃記憶體儲存已經成為智慧型手機不可或缺的元素。 NAND快閃記憶體的需求呈指數級成長,主要原因是智慧型手機平均容量的增加。

- 智慧型手機中的NAND快閃記憶體可以顯著提高網頁瀏覽、電子郵件載入、遊戲甚至 Facebook 等社群網站的效能。隨著智慧型手機越來越受歡迎,各大公司正在增加額外的功能和應用程式,以使自己的產品有別於其他製造商的產品。

- 例如,製造商擴大將手勢控制、指紋掃描器和 GPS 等功能整合到設備中。這推動了對NAND快閃記憶體快閃記憶體的需求,NAND 快閃記憶體被用作智慧型手機的代碼儲存媒體。

- 5G無線通訊的出現使智慧型手機的使用量增加了數倍,推動了不斷升級到最新型號的需求。例如,根據愛立信移動的報告,預計到2024年底,5G用戶將佔北美行動用戶的55%。

亞太地區佔很大市場佔有率

- 亞太地區是全球最大的NAND快閃記憶體快閃記憶體市場之一。受中國、印度和印尼等幾個新興國家對智慧型手機需求的推動,該地區幾乎所有終端用戶應用的需求都非常高。

- 此外,中國、韓國和新加坡等國家擁有運作的半導體製造設施。這尤其受到《中國製造2025》等政府措施的支持。

- 該國雄心勃勃的目標是到 2030 年實現半導體產值 3,050 億美元,滿足至少 80% 的國內半導體需求,預計預測期內對該國的投資將進一步增加。

- 預計將有幾家中國新公司在該地區進行大舉投資,其中包括長江儲存科技、福建晉華、華力和合肥長信儲存。預計這些公司的資本支出還將增加一倍。

- 由於多個國家出現此類發展,該地區的各個競爭對手正在加強擴張力度。

NAND快閃記憶體競爭格局

NAND快閃記憶體市場主要由英特爾、美光科技、三星電子、SanDisk、SK海力士、東芝等主要供應商主導。進入門檻較高,新進入者難以進入市場。市場上現有的供應商正大力投資創新新產品的研發。

- 2023 年 10 月——三星電子表示,它將在 2024 年初在全球率先量產 300 層NAND快閃記憶體晶片,比率先開發出 321 層 NAND 記憶體的 SK 海力士公司提前一年。

- 2023 年 6 月 - SK 海力士公司今天宣布,已開始量產 238 層 4D NAND快閃記憶體,並將開始為智慧型手機供應 238 層 NAND 產品,同時將該技術擴展到其整個產品系列,包括 PCIe 5.0* SSD 和大容量伺服器 SSD。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- COVID-19 產業影響評估

第5章市場動態

- 市場促進因素

- 資料中心需求不斷成長

- 5G和物聯網設備的興起

- 市場限制

- 可靠性問題

第6章市場區隔

- 類型

- SLC(每單元 1 位元)

- MLC(2 位元/單元)

- TLC(每單元 3 位元)

- QLC(四層電池)

- 結構

- 2D結構

- 3D結構

- 應用

- 智慧型手機

- SSD

- 記憶卡

- 藥片

- 其他應用

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Samsung Electronics Co. Ltd

- KIOXIA Corporation

- Micron Technology Inc.

- SK Hynix Inc.

- Intel Corporation

- Yangtze Memory Technologies

- SanDisk Corp.(Western Digital Technologies Inc.)

- Powerchip Technology Corporation

- Cypress Semiconductor Corporation

第 8 章供應商市場定位

第9章投資分析

The NAND Flash Memory Market size is estimated at USD 55.73 billion in 2025, and is expected to reach USD 72.60 billion by 2030, at a CAGR of 5.43% during the forecast period (2025-2030).

With the rise of PCs and smartphones, NAND flash consumption is dramatically increasing, much of which is attributed to the growth of the average capacity of smartphones. This is expected to drive the demand for NAND flash packaging, thus influencing the demand for memory packaging.

Key Highlights

- The growth of the market depends on several factors, including the growing investments in fabrication facilities, the market growth through edge storage, and the growing need for high-density storage to support smartphone applications.

- The rising demand for 3D NAND has created an opportunity for supply chain members such as chip makers, equipment manufacturers, and material suppliers. This is driving investments in 3D NAND fabrication facilities.

- Other consumer products such as tablets and cameras, along with industrial equipment and sensors, automotive systems, and medical devices, rely upon flash memory, which is integrated alongside their processors, and stores both data and the code they execute. As demand for massive data processing for artificial intelligence and machine learning applications grows, the trend for flash-based storage will continue to evolve.

- The electronics device sector was anticipated to be impacted significantly by the COVID-19 outbreak, as China is one of the major suppliers of raw materials and finished products. The industry faced a reduction in production, disruption in the supply chain, and price fluctuations. The sales of prominent electronic companies were affected during the period. The travel restriction on both people and products hampered the market's growth in the short run.

- Production of China-based NAND flash vendors was not severely affected by the outbreak of novel COVID-19. This is because the plants are highly automated, have relatively low demands for manpower, and operators are also stocked up with raw materials before the Chinese Lunar New Year. Foundry output was delivered to customers in China because semiconductor fabrication plants hold national special licenses. These allow them to ship their products throughout domestic China, even with cities under quarantine.

NAND Flash Memory Key Market Trends

The Smartphone Segment is Expected to Witness Significant Growth

- Flash memory storage has become an essential component of smartphones. The NAND flash demand has been growing exponentially, primarily driven by the growth of the average capacity of smartphones.

- NAND flash memory in smartphones can significantly enhance the performance of web browsing, email loading, games, and even social network sites such as Facebook. With the increasing adoption of smartphones, companies are adding extra features and applications to differentiate their products from other manufacturers.

- For instance, manufacturers are integrating features such as gesture control, fingerprint scanners, and GPS into the devices. This is boosting the demand for NAND flash memory, which is used as code storage media for smartphones.

- With 5G wireless communication on its way, the use of smartphones would increase multifold, increasing the need for the latest models to raise the bar continuously. For instance, according to the Ericsson Mobility report, in the North American region, 5G subscriptions are expected to account for 55% of mobile subscriptions by the end of 2024.

Asia-Pacific to Hold a Significant Market Share

- Asia-Pacific is one of the biggest markets for NAND flash memories across the world. The region has a very high demand from almost all end-user applications, primarily led by the demand for smartphones in multiple developing countries in the region, such as China, India, and Indonesia.

- Also, there is high activity from the semiconductor fabrication facilities in countries like China, Korea, and Singapore. An immense amount of capital is directed into the Chinese market by several multinational memory manufacturers, especially boosted by the country's government initiatives, such as Made in China 2025.

- The country's ambitious goal is to reach USD 305 billion in semiconductor output by 2030 and meet at least 80% of the domestic demand for semiconductors, which is expected to draw more investments into the country over the forecast period.

- Multiple new companies in China, such as Yangtze River Storage Technology, Fujian Jin Hua, Hua Li, and Hefei Chang Xin Memory, are expected to invest heavily in the region. These companies are also expected to double their equipment investments.

- Owing to such development in multiple countries, various competitors in the region are intensifying their efforts for expansion.

NAND Flash Memory Competitive Landscape

The NAND flash memory market is consolidated dominated by major vendors, such as Intel, Micron Technology, Samsung Electronics, SanDisk, SK Hynix, and Toshiba. As the entry barriers in the market are high, the entry of new players is difficult. The existing vendors in the market are investing heavily in the R&D of new and innovative products.

- October 2023 - Samsung Electronics Co. announced that it will mass produce 300-layer NAND flash memory chips for the first time in the world in early 2024, advancing the production timeline by one year compared to SK hynix Inc. which was the first to develop 321-layer NAND memory.

- June 2023 - SK hynix Inc. has announced today that it has started mass production of its 238-layer 4D NAND Flash memory, and will begin supplying the 238-layer NAND product for smartphones, and expand the technology across its product portfolio such as PCIe 5.0* SSDs and high-capacity server SSDs going forward.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Data Centers

- 5.1.2 Increasing Proliferation of 5G and IOT Devices

- 5.2 Market Restraints

- 5.2.1 Reliability Issues

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 SLC (One-Bit Per Cell)

- 6.1.2 MLC (Two-Bit Per Cell)

- 6.1.3 TLC (Three-Bit Per Cell)

- 6.1.4 QLC (Quad Level Cell)

- 6.2 Structure

- 6.2.1 2D Structure

- 6.2.2 3D Structure

- 6.3 Application

- 6.3.1 Smartphone

- 6.3.2 SSD

- 6.3.3 Memory Card

- 6.3.4 Tablet

- 6.3.5 Other Applications

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Samsung Electronics Co. Ltd

- 7.1.2 KIOXIA Corporation

- 7.1.3 Micron Technology Inc.

- 7.1.4 SK Hynix Inc.

- 7.1.5 Intel Corporation

- 7.1.6 Yangtze Memory Technologies

- 7.1.7 SanDisk Corp. (Western Digital Technologies Inc.)

- 7.1.8 Powerchip Technology Corporation

- 7.1.9 Cypress Semiconductor Corporation

8 VENDOR MARKET POSITIONING

9 INVESTMENT ANALYSIS

2025年3D NAND快閃記憶體全球市場報告

2025年3D NAND快閃記憶體全球市場報告 NAND 快閃記憶體市場:按類型、結構、應用程式和地區分類

NAND 快閃記憶體市場:按類型、結構、應用程式和地區分類 2025 年至 2029 年全球NAND快閃記憶體市場2030 年 3D NAND快閃記憶體快閃記憶體市場預測:按類型、外形規格、記憶體密度、應用、最終用戶和地區進行的全球分析

2025 年至 2029 年全球NAND快閃記憶體市場2030 年 3D NAND快閃記憶體快閃記憶體市場預測:按類型、外形規格、記憶體密度、應用、最終用戶和地區進行的全球分析 亞太地區 SLC NAND 快閃記憶體市場規模及預測 2021-2031、區域佔有率、趨勢和成長機會分析報告範圍:按類型、應用、密度和國家/地區

亞太地區 SLC NAND 快閃記憶體市場規模及預測 2021-2031、區域佔有率、趨勢和成長機會分析報告範圍:按類型、應用、密度和國家/地區 NAND快閃記憶體市場:按類型、結構、應用和最終用途分類 - 2025-2030 年全球預測

NAND快閃記憶體市場:按類型、結構、應用和最終用途分類 - 2025-2030 年全球預測 全球NAND快閃記憶體體市場Nand Flash市場、機會、成長動力、產業趨勢分析與預測,2024-20323D Nand 快閃記憶體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(單層單元、多層單元、三層單元、四層單元)、按地區和競爭應用分類, 2019-2029F

全球NAND快閃記憶體體市場Nand Flash市場、機會、成長動力、產業趨勢分析與預測,2024-20323D Nand 快閃記憶體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(單層單元、多層單元、三層單元、四層單元)、按地區和競爭應用分類, 2019-2029F 儲存加速器市場,按處理器類型、技術、企業規模、應用程式和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

儲存加速器市場,按處理器類型、技術、企業規模、應用程式和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測