|

市場調查報告書

商品編碼

1687880

數位雙胞胎(DT):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Digital Twin (DT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

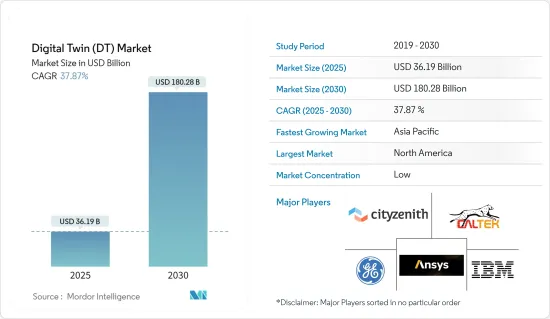

2025 年數位雙胞胎市場規模預估為 361.9 億美元,預計到 2030 年將達到 1,802.8 億美元,預測期內(2025-2030 年)的複合年成長率為 37.87%。

主要亮點

- 新冠疫情使得數位雙胞胎技術的採用顯著增加。受社交距離和旅行限制的限制,公司正在轉向數位雙胞胎進行遠端流程監控和最佳化。醫療保健領域也出現了數位雙胞胎應用激增的情況,用於模擬病患流量和改善醫院資源分配。人們對數位雙胞胎日益成長的興趣不僅限於醫療保健領域。工廠也採用該技術來控制生產線並確保工人安全。

- 數位雙胞胎將人工智慧(AI)、巨量資料、機器學習(ML)和物聯網(IoT)融入工業4.0,主要用於工業物聯網(IIoT)、工程和製造業務領域。物聯網的廣泛使用使得數位雙胞胎技術更具成本效益,並可供商業世界使用。

- 數位數位雙胞胎的日益廣泛使用有望改變製造流程並提供創新方法來降低成本、最佳化維護、監控資產、減少停機時間和開發新的連網產品。數位雙胞胎模型並不新鮮,但它們正在迅速進入製造業和其他行業。物聯網和雲端基礎的平台等技術正在推動數位雙胞胎解決方案的廣泛採用。

- 預計市場成長將受到低度開發國家使用的傳統系統存在的阻礙。大多數舊有系統都已經開發完成,但主要是為無需連接即可運行而設計和構建的。無法融入提供即時資料的先進感測器技術限制了新興技術的採用。

- 然而,自疫情爆發以來,企業開始轉向數位孿生來建模和增強其營運的彈性。這種積極主動的方法將幫助您制定強力的應對和恢復策略,使您能夠更好地為未來的市場混亂做好準備。

數位雙胞胎(DT)市場趨勢

製造業是最大的應用

- 數位雙胞胎將應用於從設計開發到生產和售後服務的整個產品生命週期。這使得製造商能夠根據即時回饋不斷改進他們的產品和流程。透過創建機械設備的數位複製品,製造商可以預測潛在故障並在問題發生之前安排維護,從而最大限度地減少停機時間並延長資產的使用壽命。透過使用複製產品或生產系統的數位雙胞胎,製造商可以減少在工廠車間組裝、安裝和檢驗生產系統的成本和時間。

- 物聯網 (IoT) 設備的迅速普及和人工智慧 (AI) 的進步使得更詳細的即時資料收整合為可能,這對於創建準確的數位雙胞胎至關重要。根據 GSMA 預測,到 2025 年,北美消費者和工業IoT連接總數將成長到 54 億。

- 此外,據愛立信稱,到 2023 年,全球短距離物聯網設備數量將達到 123.9 億。預計到 2027 年,這一數字將成長到 250 億。物聯網技術的這些發展有可能催生出數位雙胞胎市場。

- 隨著製造業變得越來越複雜以及對更先進技術的需求不斷成長,公司設計、檢驗和確認其半導體晶片產品變得越來越困難。數位雙胞胎可以實現更快、更完整的 IC檢驗和確認週期,從而顯著提高最終產品品質並縮短上市時間。例如,西門子使用數位雙胞胎技術來檢驗和確認積體電路。

- 此外,製造業的成長可能會進一步刺激市場需求。達拉斯聯邦儲備銀行的數據顯示,2024年2月,美國以外全球工業生產以三個月移動平均計算年增1.1%。此外,根據世界銀行的數據,2024年4月全球PMI新出口訂單為50.5,製造業PMI為50.3。

北美佔有最大市場佔有率

- 隨著數位領域與實體世界不斷融合,數位雙胞胎技術已成為轉變產業和營運的重要工具。製造業、航空航太、石油和天然氣以及汽車等行業正在有效利用數位雙胞胎技術的優勢。區域市場採用率的提高和供應商的積極參與預計將推動市場擴張。

- 例如,美國聯邦政府機構已經開始探索數位雙胞胎應用,顯示該技術的接受度越來越高。Accenture最近的發展表明,空軍、海軍、能源部、農業部和國家海洋與大氣管理局等不同機構都已採用或對數位雙胞胎開發表現出濃厚的興趣。這些措施顯示美國政府越來越意識到數位雙胞胎所能帶來的好處。

- 此外,該地區的製造業預計將大幅推動對數位雙胞胎技術的需求。數位雙胞胎技術使製造商能夠在實體生產之前開發工具工具機的虛擬複製品。這有助於在數位環境中進行測試和原型製作,使工程師能夠在開始實際生產之前識別並解決潛在問題。預計該地區製造業的投資增加和生產能力的增強將在預測期內推動市場大幅成長。

- 加拿大的製造業、建設業和汽車業正在廣泛應用數位雙胞胎技術。這些產業正在利用數位雙胞胎技術來評估其實物資產的性能,找出需要改進的領域,並最終取得更有利的結果。此外,加拿大醫療保健領域對數位雙胞胎技術的日益廣泛應用有望推動市場成長。

- 此外,該國在多個領域都擁有巨大的成長潛力,並有望在未來幾年大幅增加市場佔有率。隨著航太和石油天然氣行業投資的激增,市場將利用這些機會。此外,電力產業對可再生能源的日益關注是市場成長的驅動力。

數位雙胞胎(DT)市場概覽

數位雙胞胎市場由 ANSYS Inc.、Cal-Tek SRL、Cityzenith Inc.、通用電氣公司和 IBM 公司等主要企業分割。市場參與者正在採取合作和收購等策略來增強其服務產品並獲得永續的競爭優勢。

- 2024 年 3 月:IBM Consulting 與 NVIDIA 合作,在開放生態系統中引領客戶實現 AI主導的轉型。該策略聯盟將利用 IBM Consulting 深厚的產業洞察力和技術力,並協同效應NVIDIA 的服務產品,包括 NVIDIA AI Enterprise 軟體。值得注意的組件包括 NVIDIA NIM 微服務的引入和多功能 NVIDIA Omniverse 平台。該策略的核心是生成式人工智慧、機器人和數位雙胞胎,它們對於無縫整合到生產環境至關重要。 IBM Consulting 在利用 NVIDIA 的 Isaac Sim 和 Omniverse 建置和部署數位雙胞胎應用程式方面處於領先地位。這些應用程式正在編配複雜的多智慧體機器人設定並徹底改變供應鏈和製造業格局。

- 2024 年 3 月:微軟公司和 NVIDIA 透過強大的新整合擴大了他們長期的合作,這些整合利用了 Microsoft Azure、Azure AI 服務、Microsoft Fabric 和 Microsoft 365 中最新的 NVIDIA 生成 AI 和 Omniverse 技術。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- COVID-19 產業影響評估

第5章 市場動態

- 市場促進因素

- 物聯網和雲端基礎平台的成長

- 3D 列印技術在製造業的應用激增

- 計劃成本降低目標

- 市場挑戰

- 低度開發國家基礎設施不足和資料安全問題

第6章 市場細分

- 按應用

- 製造業

- 能源和電力

- 航太

- 石油和天然氣

- 車

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 亞洲

- 中國

- 日本

- 印度

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- ANSYS Inc.

- Cal-Tek SRL

- Cityzenith Inc.

- General Electric Company

- IBM Corporation

- Lanner Group Limited(Royal Haskoning DHV)

- Mevea Ltd

- Microsoft Corporation

- Rescale Inc.

- SAP SE

第8章投資分析

第9章:市場的未來

簡介目錄

Product Code: 66631

The Digital Twin Market size is estimated at USD 36.19 billion in 2025, and is expected to reach USD 180.28 billion by 2030, at a CAGR of 37.87% during the forecast period (2025-2030).

Key Highlights

- The adoption of digital twin technology witnessed significant growth due to the COVID-19 pandemic. Constrained by social distancing and travel limitations, businesses increasingly turned to digital twins for remote process monitoring and optimization. The healthcare sector also witnessed a sharp rise in the use of digital twins to simulate patient flows and enhance resource allocation in hospitals. This heightened interest in digital twins was not limited to healthcare. Factories also embraced the technology to manage production lines and ensure workers' safety.

- Digital twins incorporate artificial intelligence (AI), Big Data, machine learning (ML), and the Internet of Things (IoT) in Industry 4.0 and are predominantly used in the industrial Internet of Things (IIoT), engineering, and manufacturing business space. The widespread usage of IoT has made digital twin technology more cost-effective and accessible for the business world.

- The growth in the use of digital twins is anticipated to transform the manufacturing processes and offer innovative approaches to reducing costs, optimizing maintenance, monitoring assets, reducing downtime, and creating new connected products. Although not new, the digital twin model has been entering manufacturing and other industries rapidly. Technologies such as IoT and cloud-based platforms have been major drivers for the increased adoption of digital twin solutions.

- The market's growth is expected to be hampered by the presence of traditional systems used in underdeveloped countries. Most of these legacy systems had already been developed but were primarily designed and built to function without connectivity. They cannot incorporate advanced sensor technology that offers real-time data, limiting the adoption of advanced technologies.

- However, post-pandemic, companies are increasingly turning to digital twins to model and enhance their operational resilience. This proactive approach helps them craft robust response and recovery strategies, better preparing them for future market disruptions.

Digital Twin (DT) Market Trends

Manufacturing to be the Largest Application

- Digital twins are used throughout the life cycle of a product, ranging from design and development to production and after-sales service. This allows manufacturers to improve products and processes continuously based on real-time feedback. By forming digital replicas of machinery and equipment, manufacturers can predict potential failures and schedule maintenance before issues arise, minimizing downtime and extending the life of assets. Manufacturers can reduce the cost and time associated with assembling, installing, and validating factory production systems using digital twins replicating the product and production systems.

- The rapid spread of Internet of Things (IoT) devices and advancements in artificial intelligence (AI) enable more detailed and real-time data collection, crucial for creating accurate digital twins. According to GSMA, North America's total number of consumer and industrial IoT connections is forecast to grow to 5.4 billion by 2025.

- In addition, according to Ericsson, in 2023, the number of short-range IoT devices reached 12.39 billion worldwide. This number is forecast to increase to 25 billion by 2027. Such growing IoT technologies may develop the market for digital twins.

- As manufacturing complexity and demand for more advanced technology grows, it has become more difficult for companies to design, verify, and validate products of semiconductor chips. Digital twins enable faster and more complete IC verification and validation cycles, leading to significantly higher quality end-products and faster market time. For example, Siemens uses digital twins' technology for IC verification and validation.

- Furthermore, the manufacturing sector's growth may further propel the market's demand. According to the Dallas Fed, in February 2024, global industrial production, excluding the United States, increased by 1.1% compared to the same time in the previous year, based on three-month moving averages. Furthermore, according to the World Bank, in April 2024, the global PMI amounted to 50.5 for new export orders and 50.3 for manufacturing.

North America Holds Largest Market Share

- With the continuous integration of the digital realm into the physical world, digital twin technology has become a crucial tool for transforming industries and operations. Sectors such as manufacturing, aerospace, oil and gas, automobile, and others in the area effectively utilize the advantages of digital twin technology. The rise in adoption rates and the active involvement of vendors in the regional market are projected to propel the market's expansion.

- For instance, federal agencies in the United States have begun exploring the applications of digital twins, showcasing a significant embrace of this technology. Recent reports from Accenture reveal that various entities such as The Air Force, Navy, the Department of Energy, the Department of Agriculture, and the National Oceanic and Atmospheric Administration have introduced the development of digital twins or shown keen interest in doing so. These advancements indicate a growing recognition within the US government of the advantages that digital twins can offer.

- Moreover, the region's manufacturing sector is expected to drive the demand for digital twin technology at a significant rate. Digital twin technology allows manufacturers to develop virtual replicas of machine tools prior to their physical fabrication. This facilitates testing and prototyping in a digital setting, empowering engineers to identify and resolve potential issues before the start of real production. The increasing investments in the region's manufacturing sector and extensive production capabilities will enable the market to grow significantly during the forecast period.

- Canadian manufacturing, construction, and automotive sectors are witnessing a substantial adoption of digital twins. These industries leverage digital twin technology to assess the performance of their physical assets, pinpoint areas for enhancement, and ultimately achieve more favorable results. Furthermore, the healthcare sector in Canada is increasingly embracing digital twin technology, poised to propel the market's growth.

- Moreover, the nation presents substantial growth potential across multiple sectors and is poised to bolster its market share significantly in the coming years. With escalating investments in the aerospace and O&G industries, the market is set to capitalize on these opportunities. Furthermore, the growing attention on renewable energy sources within the power sector is primed to propel the market's growth.

Digital Twin (DT) Market Overview

The digital twin market is fragmented with major players like ANSYS Inc., Cal-Tek SRL, Cityzenith Inc., General Electric Company, and IBM Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- March 2024: IBM Consulting, in collaboration with NVIDIA, spearheaded AI-driven transformations for its clients within an open ecosystem. This strategic alliance leverages IBM Consulting's profound industry insights and technological prowess, synergizing with NVIDIA's offerings, such as the NVIDIA AI Enterprise software. Noteworthy components include the introduction of NVIDIA NIM microservices and the versatile NVIDIA Omniverse platform. Central to their strategy are generative AI, robotics, and digital twins, pivotal for seamless integration into production environments. IBM Consulting is at the forefront, harnessing NVIDIA's Isaac Sim and Omniverse to craft and deploy digital twin applications. These applications are revolutionizing supply chain and manufacturing landscapes, orchestrating intricate multi-agent robotic setups.

- March 2024: Microsoft Corp. and NVIDIA expanded their longstanding collaboration with powerful new integrations that leverage the latest NVIDIA generative AI and Omniverse technologies across Microsoft Azure, Azure AI services, Microsoft Fabric, and Microsoft 365.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in IoT and Cloud-based Platforms

- 5.1.2 Surge in Adoption of 3D Printing Technology in the Manufacturing Industry

- 5.1.3 Objective to Reduce Project Cost

- 5.2 Market Challenges

- 5.2.1 Inadequate Infrastructure in Under-developed Countries and Data Security-related Concerns

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Manufacturing

- 6.1.2 Energy and Power

- 6.1.3 Aerospace

- 6.1.4 Oil and Gas

- 6.1.5 Automobile

- 6.1.6 Others Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ANSYS Inc.

- 7.1.2 Cal-Tek SRL

- 7.1.3 Cityzenith Inc.

- 7.1.4 General Electric Company

- 7.1.5 IBM Corporation

- 7.1.6 Lanner Group Limited (Royal Haskoning DHV)

- 7.1.7 Mevea Ltd

- 7.1.8 Microsoft Corporation

- 7.1.9 Rescale Inc.

- 7.1.10 SAP SE

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

數位雙胞胎市場規模、佔有率及成長分析(按解決方案、部署、公司規模、應用、最終用途和地區)-2025 年至 2032 年產業預測醫療保健的數位雙胞胎市場:各治療領域,數位雙胞胎類別,各應用領域,各終端用戶,各主要地區:2035年前的產業趨勢與全球預測

數位雙胞胎市場規模、佔有率及成長分析(按解決方案、部署、公司規模、應用、最終用途和地區)-2025 年至 2032 年產業預測醫療保健的數位雙胞胎市場:各治療領域,數位雙胞胎類別,各應用領域,各終端用戶,各主要地區:2035年前的產業趨勢與全球預測 按產品類型、業務功能、應用程式、部署類型和最終用戶行業分類的數位線程市場 - 2025-2030 年全球預測

按產品類型、業務功能、應用程式、部署類型和最終用戶行業分類的數位線程市場 - 2025-2030 年全球預測 2025年醫療保健數位雙胞胎全球市場報告2025 年至 2033 年數位孿生市場規模、佔有率、趨勢及預測(按類型、技術、最終用途和地區)2025 年數位雙胞胎金融服務與保險全球市場報告

2025年醫療保健數位雙胞胎全球市場報告2025 年至 2033 年數位孿生市場規模、佔有率、趨勢及預測(按類型、技術、最終用途和地區)2025 年數位雙胞胎金融服務與保險全球市場報告 醫療保健市場的全球數位孿生 - 2024-2031

醫療保健市場的全球數位孿生 - 2024-2031 數位雙胞胎市場:2025-2029 年全球2025-2033 年日本數位孿生市場規模、佔有率、趨勢和預測(按類型、技術、最終用途和地區分類)

數位雙胞胎市場:2025-2029 年全球2025-2033 年日本數位孿生市場規模、佔有率、趨勢和預測(按類型、技術、最終用途和地區分類) 全球醫療保健數位雙胞胎市場,2025-2029

全球醫療保健數位雙胞胎市場,2025-2029

▼