|

市場調查報告書

商品編碼

1687899

北美鋰離子電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)North America Lithium-ion Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

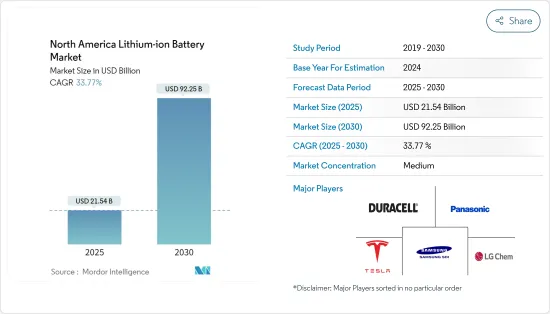

北美鋰離子電池市場規模預計在 2025 年為 215.4 億美元,預計到 2030 年將達到 922.5 億美元,預測期內(2025-2030 年)的複合年成長率為 33.77%。

關鍵亮點

- 從中期來看,預計市場將受到電動和混合動力汽車日益普及的推動,這將增加對能源儲存系統的需求。

- 然而,原料供需不匹配預計會在研究期間阻礙市場成長。

- 預計在預測期內,效率和維護需求的改善將為鋰離子電池帶來巨大的機會。

- 隨著政府在預測期內增加對電動車領域的投資,預計美國將佔據市場主導地位。這將導致基於電池的能源儲存系統的需求增加,主要由鋰離子電池主導。

北美鋰離子電池市場趨勢

汽車電池可望快速成長

- 鋰離子電池系統可滿足OEM對續航里程和充電時間的要求,進而提高插電式混合動力汽車和電動車的性能。高能量密度、快速充電能力和高放電功率使鋰離子電池成為首選技術。鋰離子電池在比能量和重量方面比鉛基牽引電池更具優勢。因此,鋰離子電池已成為全混合動力車和電動車最具競爭力的選擇。

- 鋰離子電池延長了依賴其供電的電動車的使用壽命,並減少了頻繁更換電池的需要。鋰離子電池被認為比其他電池更環保,因為它們不含鉛和鎘等有害物質。這使得它成為一個更乾淨、更安全的選擇。此外,鋰離子電池提供高功率,這對於需要快速加速和高速行駛的電動車至關重要。

- 此外,鋰離子電池的方形電池在電動車電池製造業中越來越受歡迎。這些細胞相當大,比圓柱形細胞大 20 到 100 倍。更大的尺寸使得方形電池能夠在相同體積內輸出更多電力並儲存更多能量。另一方面,圓柱形電池外殼使用的材料較少,限制了其功率輸出和能源儲存容量。

- 此外,隨著電動車銷量的增加,預計預測期內汽車領域對鋰離子電池的需求將大幅成長。例如,根據國際能源總署的數據,2021年至2022年,美國和加拿大的電動車銷量成長了54%以上。

- 此外,通用、福特等美國企業也宣布了2022年電動車產銷目標策略。通用的目標是到2025年在北美生產30款電動車,形成100萬輛純電動車(BEV)的產能,到2040年實現碳中和。福特則宣布了這樣的目標:到2026年,其銷量的三分之一為純電動車,到2030年,這一比例達到50%,到2030年,歐洲市場所有汽車均為電動車。預計北美地區對鋰離子電池的需求將會增加。

- 2023 年 2 月,NanoGraf 宣布了在矽陽極開發方面的最新進展,以提高即將推出的鋰離子電池的能量和功率密度。這項突破性技術有效地解決了與矽陽極相關的挑戰。

- 因此,預計在預測期內,電動車的日益普及將推動北美鋰離子電池市場的發展。

預計美國將主導市場

- 美國是全球電池市場研究和創新的先驅之一。它也是最大的電池消耗國之一,一次電池和二次電池。這是由於電動車的廣泛採用、家用電子電器產品的支出以及消費和製造活動的增加。

- 美國擁有完善的鋰離子電池製造基礎設施,擁有許多電池製造商和專門從事電池技術的研發機構。這些基礎設施使美國在生產能力和技術進步方面具有競爭優勢。

- 例如,2022年10月,本田宣布計畫在美國生產鋰離子電池,成為最新一家這樣做的汽車公司。透過與 LG Energy Solutions 的合資企業,本田旨在向北美市場供應專為本田和謳歌品牌電動車設計的「袋式」電池。該投資 44 億美元的工廠的具體位置尚未披露,但預計合資企業將在今年年底前投入營運,但需獲得監管核准的批准。預計該計畫將於2023年初動工,並預計於2025年底實現先進鋰離子電池單元的量產。

- 此外,在政府獎勵、環境法規和消費者對更清潔交通的需求的推動下,美國是電動車的龐大市場。電動車的興起正在推動對鋰離子電池的需求,而美國在這一市場上具有優勢。

- 新措施要求獲得聯邦資助的計劃在美國生產產品,其中包括2022會計年度2億美元的電池技術援助資金。它也適用於能源部先進技術汽車製造貸款計劃下貸款機構發放的 170 億美元。

- 根據國際能源總署 (IEA) 的數據,該國的電動車銷量為 99,000 輛,而去年為 63,000 輛,2022 年至 2021 年期間的成長率超過 57%。

- 根據美國能源資訊署的數據,截至 2022 年,大型電池的累積容量約為 22,385.1 兆瓦時 (MWh),比 2021 年增加約 80%。在美國,加州獨立系統營運商 (CAISO) 和德克薩斯州電力可靠性委員會 (ERCOT) 負責大部分大型電池容量的新增。 2022 年,CAISO 將擁有 7,561.3 兆瓦時,佔 34%,ERCOT 將擁有 1,684.4 兆瓦時,佔 7.5%。

- 此外,國內電動車製造商正在進一步努力滿足日益成長的需求。預計到 2025 年,美國將有 13 座新的電池超級工廠投入運作。這些超級工廠由福特汽車公司和通用汽車等汽車製造商開發,旨在幫助他們製造和銷售電動車。

- 因此,在都市化和消費者支出成長的推動下,北美很可能主導鋰離子電池市場。鋰離子電池帶來的優勢預計將推動對技術先進設備和汽車的需求。預計這將導致電池使用量增加。

北美鋰離子電池產業概況

北美鋰離子電池市場比較分散。市場的主要企業(不分先後順序)包括特斯拉公司、LG化學有限公司、松下公司、金霸王公司和三星SDI。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 至2029年的市場規模及需求預測(單位:美元)

- 2029年全球鋰離子電池價格趨勢分析

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 鋰離子電池價格下跌

- 電動車日益普及

- 限制因素

- 鋰離子電池安全問題

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 應用

- 消費性電子產品

- 車

- 工業電池(動力、固定(電信、UPS、能源儲存系統(ESS) 等))

- 其他應用(電動工具、國防、醫療設備等)

- 市場分析:依地區{市場規模及需求預測至2028年(按地區)

- 美國

- 加拿大

- 北美其他地區

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- BYD Company Ltd

- Contemporary Amperex Technology Co. Limited

- EnerSys

- Duracell Inc.

- Clarios(原江森自控國際有限公司)

- LG Chem Ltd.

- Panasonic Corporation

- VARTA AG

- Samsung SDI Co. Ltd.

- Sony Corporation

- Tesla Inc.

第7章 市場機會與未來趨勢

- 效率改善和維護需求

簡介目錄

Product Code: 66743

The North America Lithium-ion Battery Market size is estimated at USD 21.54 billion in 2025, and is expected to reach USD 92.25 billion by 2030, at a CAGR of 33.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the market is expected to be driven by the increasing adoption of electric and hybrid vehicles and the increasing demand for energy storage systems.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market growth during the study period.

- Nevertheless, the improvements in efficiency and maintenance requirements are expected to provide significant opportunities for lithium-ion batteries during the forecast period.

- The United States is expected to dominate the market due to the government's increasing investments in electric vehicle segments in the forecast period. It will result in increased demand for battery-based energy storage systems, primarily led by lithium-ion batteries.

North America Lithium-ion Battery Market Trends

Automotive Batteries Expected to be the Fastest-growing Segment

- Lithium-ion battery systems drive the performance of plug-in hybrid and electric vehicles by meeting OEM requirements for driving range and charging time. Their high energy density, fast recharge capability, and high discharge power make lithium-ion batteries the preferred technology. They outperform lead-based traction batteries in terms of specific energy and weight. As a result, lithium-ion batteries are the most competitive option for total hybrid electric vehicles and electric vehicles.

- Lithium-ion batteries offer a longer lifespan for electric vehicles, which rely on these batteries for power, reducing the frequency of battery replacements. Lithium-ion batteries are considered environmentally friendly compared to other batteries as they do not contain toxic materials like lead or cadmium. It makes them a cleaner and safer choice. Additionally, lithium-ion batteries provide a high power output, which is crucial for electric vehicles that require rapid acceleration and high speeds.

- Moreover, within the electric vehicle battery manufacturing industry, there is a growing popularity of lithium-ion battery prismatic cells. These cells are significantly larger, ranging from 20 to 100 times the size of cylindrical cells. This larger size allows prismatic cells to deliver more power and store greater energy within the same volume. Cylindrical cells, on the other hand, use less material for their casing, which can limit their power and energy storage capabilities.

- Additionally, with the growing sales of electric vehicles, the demand for lithium-ion batteries for the automotive segment is expected to increase significantly during the forecasted period. For instance, according to the International Energy Agency, the sales of electric vehicles in the United States and Canada grew by more than 54% between 2021 and 2022.

- Moreover, in 2022, General Motors & Ford, and American companies announced their targeted strategy to manufacture and sell EVs. General Motors declared its target to manufacture 30 EV models and set up a Battery Electric Vehicle (BEV) production capacity of 1 million units in North America by 2025, plus carbon neutrality in 2040. In comparison, Ford declared its target of One-third of sales to be fully electric by 2026 and 50% by 2030, with all-electric sales in Europe by 2030. It will drive the need for lithium-ion batteries in North America.

- In February 2023, NanoGraf's latest advancement in deploying silicon anodes is positioned to enhance the energy and power densities of forthcoming lithium-ion batteries. This breakthrough technology effectively addresses the challenges associated with silicon anodes.

- Therefore, the increasing shift towards electric vehicles is expected to drive the North America Lithium-ion Battery Market during the forecast period.

The United States Expected to Dominate the Market

- The United States is one of the pioneers in research and innovation in the global battery market. The region also remains one of the largest consumers of batteries, i.e., both primary and secondary battery types. It is owing to increased electric vehicle deployment, spending on consumer electronics, and consumer and manufacturing activities.

- The United States includes a well-established manufacturing infrastructure for lithium-ion batteries, a significant number of battery manufacturers, and research and development facilities focused on battery technologies. This infrastructure gives the United States a competitive edge regarding production capacity and technological advancements.

- For instance, in October 2022, Honda announced its plans to manufacture lithium-ion batteries in the United States, making it the latest car company to do so. In a joint venture with LG Energy Solutions, Honda aims to supply the North American market with "pouch type" batteries designed to power electric vehicles under its Honda and Acura brands. While the exact location of the USD 4.4 billion factory is not disclosed, the joint venture is expected to commence by the end of this year, pending regulatory approval. Construction is planned to begin in early 2023 to achieve mass production of advanced lithium-ion battery cells by the end of 2025.

- Moreover, the United States holds a large market for electric vehicles driven by government incentives, environmental regulations, and consumer demand for cleaner transportation options. The increasing adoption of EVs fuels the demand for lithium-ion batteries, giving the United States an advantage in the market.

- The new policies mandate that projects receiving federal support, including the USD 200 million in the agency's 2022 budget to support battery technology, must manufacture their products within the United States. It also applies to the USD 17 billion issued by the lending authority under DOE's Advanced Technology Vehicles Manufacturing Loan Program.

- According to the International Energy Agency, the country's electric vehicle sales were around 990000 compared to 630000, registering a growth rate of more than 57% between 2022 and 2021.

- Moreover, as of 2022, the cumulative large-scale battery storage capacity was around 22,385.1 megawatt-hours (MWh), which was approximately 80% more than in 2021, as per the United States Energy Information Administration. In the United States, the California Independent System Operator (CAISO) and Electric Reliability Council of Texas (ERCOT) include most of the large-scale battery storage capacity additions. In 2022, CAISO had 7561.3 MWh or 34 % share, and ERCOT had 1684.4 MWh capacity or 7.5% share in the country's overall installed capacity.

- Further, the country's EV manufacturers are undertaking further initiatives to cater to the rising demand. Thirteen new battery cell giga-factories are expected to come online in the United States by 2025. These giga-factories are being developed by various automobile manufacturers, like Ford Motor Company and General Motors Company, to support their electric vehicle manufacturing and sales.

- Therefore, the country is likely the dominant player in the North American lithium-ion battery market, supported by increasing urbanization and consumer spending. These are expected to ramp up the demand for technically advanced devices and vehicles due to the benefits provided by the same. Consecutively, this is expected to boost the usage of batteries.

North America Lithium-ion Battery Industry Overview

The North American lithium-ion battery market is semi-fragmented. Some of the key players in the market (in no particular order) include Tesla Inc., LG Chem Ltd, Panasonic Corporation, Duracell Inc., and Samsung SDI Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Global Lithium-ion Battery Price Trend Analysis, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Lithium-Ion Battery Prices

- 4.6.1.2 Increasing Adoption Of Electric Vehicles

- 4.6.2 Restraints

- 4.6.2.1 Safety Concerns Related To Lithium-Ion Battery

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Consumer Electronics

- 5.1.2 Automotive

- 5.1.3 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.))

- 5.1.4 Other Applications (Power Tools, Defense, Medical Devices, etc.)

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 EnerSys

- 6.3.4 Duracell Inc.

- 6.3.5 Clarios (Formerly Johnson Controls International PLC)

- 6.3.6 LG Chem Ltd.

- 6.3.7 Panasonic Corporation

- 6.3.8 VARTA AG

- 6.3.9 Samsung SDI Co. Ltd.

- 6.3.10 Sony Corporation

- 6.3.11 Tesla Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Improvement In Efficiency And Maintenance Requirements

02-2729-4219

+886-2-2729-4219

全球Z-L-Valine NCA市場、實績和預測(2020-2031年)

全球Z-L-Valine NCA市場、實績和預測(2020-2031年) 全球鋰離子電池市場

全球鋰離子電池市場 印度鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)東南亞鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

印度鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)東南亞鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)鋰離子電池:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球工業鋰離子電池市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球工業鋰離子電池市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 鋰離子電池材料市場(按材料、應用、電池化學和地區分類)- 2029 年預測

鋰離子電池材料市場(按材料、應用、電池化學和地區分類)- 2029 年預測 2025年可充電鋰離子聚合物電池全球市場報告全球鋰離子電池市場評估:依類型、容量、配置、最終用戶、通路、機會和預測2018年至2032年

2025年可充電鋰離子聚合物電池全球市場報告全球鋰離子電池市場評估:依類型、容量、配置、最終用戶、通路、機會和預測2018年至2032年 全球鋰離子電池市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球鋰離子電池市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

▼