|

市場調查報告書

商品編碼

1687930

非揮發性記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Non-Volatile Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

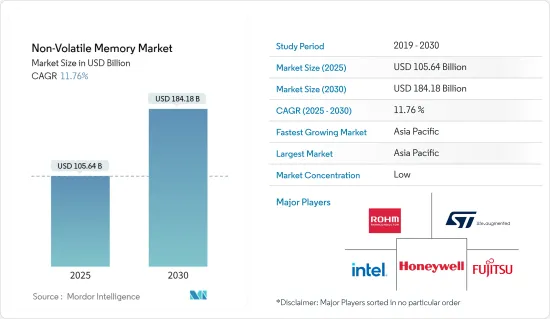

非揮發性記憶體市場規模預計在 2025 年為 1,056.4 億美元,預計到 2030 年將達到 1,841.8 億美元,預測期內(2025-2030 年)的複合年成長率為 11.76%。

在過去十年中,可攜式系統市場的成長推動了半導體產業對用於大容量儲存應用的非揮發性記憶體 (NVM) 技術的興趣。對更高效率、更快記憶體存取和更低功耗的需求正在推動 NVM 市場的成長。

主要亮點

- 在蓬勃發展的消費性電子產業中,用戶期望他們的設備能夠不斷改進,以閃電般的速度提供新功能,並儲存更多的電影、照片和音樂。儘管閃存在過去幾十年中實現了重大創新,但由於快閃記憶體遇到了阻礙其進一步擴展的技術障礙,因此需要新一代記憶體。

- 快閃記憶體的低成本和低功耗使其在消費性電子產品中廣泛應用,成為市場成長的關鍵。 NVM 用於智慧型手機和穿戴式設備,以實現更大的儲存空間和更快的記憶體存取。

- 該領域研究活動的活性化也推動了市場的成長。例如,2021年3月,英飛凌科技有限責任公司宣布推出符合QML-Q和高可靠性工業規範的第二代非揮發性靜態RAM,主要支援航太和工業應用等惡劣環境下的非揮發性程式碼儲存。

- 同樣,三星在 2021 年初宣布改進其 MRAM 的 MTJ 功能,推進其 14nm 製程以支援旨在提高寫入速度和密度的快閃記憶體型嵌入式 MRAM。此外,該公司還瞄準穿戴式裝置、微控制器和物聯網裝置中的 IC 新興 NVM 應用。

- 然而,目前市面上非揮發性記憶體的問題往往源自於其讀寫耐久性和資料保存特性。例如,相變記憶體 (PCM) 和快閃記憶體就是耐久性有限的 NVM 的例子。這些 NVM 的耐久性較低,因為經過幾個寫入週期(對於 PCM 來說為 RESET 週期,對於快閃記憶體來說為程式設計/擦除週期)之後,儲存單元就會磨損,無法再可靠地儲存資訊。

- COVID-19 疫情對智慧型手機產業等多個非揮發性記憶體的終端用戶產業產生了負面影響。在雲端運算、人工智慧和物聯網等主要大趨勢的推動下,家庭辦公室活動對伺服器和 PC 記憶體的需求激增,預計在預測期內支援非揮發性記憶體的成長。

非揮發性記憶體市場趨勢

快閃記憶體可望佔據較大市場佔有率

- 隨著消費性電子產品的需求不斷成長和普及,設備快閃記憶體的用途也越來越廣泛。這種記憶體類型存在於筆記型電腦、GPS、電子樂器、數位相機、行動電話和許多其他設備中。此外,它也被資料中心解決方案供應商廣泛採用。隨著雲端解決方案的快速採用,對資料中心的需求也在快速成長。

- 此外,隨著人工智慧/機器學習應用和物聯網設備的日益成長,低延遲、高吞吐量的雲端儲存、快閃記憶體和企業資料中心都針對訓練深度神經網路進行了最佳化。預計資料中心數量和規模的增加將進一步推動需求。

- 為了滿足日益成長的需求,市場上的供應商正專注於開發具有更好功能的更新的解決方案。例如,2021年2月,鎧俠株式會社與西部數據公司宣布開發第六代162層3D快閃記憶體技術。這是該公司密度最高、最先進的3D快閃記憶體技術,採用了多項技術和製造創新。

- 此外,NOR快閃記憶體因超低功耗的需求也越來越受歡迎。例如,英飛凌科技於 2022 年 1 月宣布增加開發工具以支援其 SEMPER NOR 快閃記憶體裝置系列。這使開發人員能夠快速設計安全關鍵且固有安全的汽車、工業和通訊系統。

- 同樣,旺宏國際於2021年11月宣布,它是業界第一家開始量產1.2V設備的串行NOR快閃製造商。根據該公司介紹,超低功耗(ULP)和高速120MHz MX25S串行NOR快閃記憶體將迎來新一代產品,這些產品針對的是物聯網(IoT)、無線通訊技術、WiFi、窄頻物聯網系統、手持設備、藍牙設備和消費性應用等應用。

亞太地區預計將佔據主要市場佔有率

- 線上娛樂、在家工作以及視訊和語音通話服務的需求激增,推動了亞太地區各國包括資料中心在內的新基礎設施建設。數位經濟的快速發展,使得中國、印度等國家都有建置大型巨量資料中心的需求。

- 中國積極進軍NAND記憶體市場,已成為主要參與者。例如,中國領先的記憶體公司之一長江儲存科技(YMTC)正在國內出貨少量 64 層 NAND,包括用於 SSD,並且正在開發 128 層生產,計劃於 2021 年出貨。

- 此外,該地區也吸引了多家致力於非揮發性記憶體相關技術開發的新興企業進行投資。例如,2021年4月,上海創星半導體有限公司在A輪前資金籌措中籌集了約1億美元。本輪資金籌措由上海聯和投資主導,Atlas Capital 和 KQ Capital 參投。該公司計劃利用這筆投資生產電阻式隨機存取記憶體(ReRAM)晶片和其他用於儲存應用的晶片。

- 該地區的公司正在利用非揮發性記憶體實現各種工業應用。 2021年11月,非揮發性記憶體(NVM)技術供應商富達科技宣佈在上海華虹中半導體製造有限公司的180BCD(Z8)平台上推出產品名稱為ZT的高品質eNVM(嵌入式非揮發性記憶體),支援10年150°C保存時間。

- 此外,該地區在非揮發性記憶體(NVM)方面的研發活動正在增加。 2022年1月,三星電子宣布全球首次展示以MRAM(磁阻隨機存取記憶體)為記憶體內運算。預計這些趨勢將在預測期內推動亞太地區研究市場的成長。

非揮發性記憶體產業概況

非揮發性記憶體市場競爭激烈,有幾家大型企業在競爭。本產業競爭對手之間的競爭主要取決於透過技術創新、市場滲透和競爭策略的強度來獲得永續的競爭優勢。這是一個資本密集型市場,因此退出障礙較高。該市場的主要參與者包括ROHM、意法半導體、富士通和英特爾公司。最近的市場發展趨勢包括:

- 2022年1月,SK海力士宣布完成收購英特爾NAND和固態硬碟(SSD)業務交易的第一階段。該公司表示,已透過收購英特爾的SSD業務及其在中國大連的NAND快閃記憶體製造工廠完成了交易的第一階段。

- 2021 年 10 月 - NSCore Inc. 推出了 OTP+(一次性可編程),這是一種適用於物聯網技術應用的非揮發性記憶體解決方案。根據該公司介紹,其40nm超低功耗OTP NVM IP解決方案可最大限度地減少新興市場對關鍵物聯網晶片進行再製造的需要。此外,與標準 OTP IP 解決方案不同,NSCore OTP+ 解決方案具有可重新編程和變更的功能。

- 2021 年 7 月—美光科技宣布已開始批量出貨全球首款 176 層 NAND 通用快閃儲存 (UFS) 3.1 行動解決方案。美光的 UFS 3.1 獨立行動 NAND 記憶體專為高階和旗艦行動電話而設計,與前幾代產品相比,連續式寫入和隨機讀取速度提高了 75%,釋放了5G 的潛力。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響

- 產業價值鏈分析

第5章 市場動態

- 市場促進因素

- 連網型設備和穿戴式裝置對非揮發性記憶體的需求不斷增加

- 企業儲存應用需求不斷成長

- 市場挑戰

- 低寫入耐久性

第6章 市場細分

- 按類型

- 傳統非揮發性記憶體

- 快閃記憶體

- EEPROM

- SRAM

- EPROM

- 其他常規非揮發性記憶體

- 下一代非揮發性記憶體

- MRAM

- FRAM

- 電阻式記憶體

- 3D-X 點

- 奈米RAM

- 其他下一代非揮發性記憶體

- 傳統非揮發性記憶體

- 按最終用戶產業

- 消費性電子產品

- 零售

- 資訊科技和電訊

- 衛生保健

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 其他亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- ROHM Co. Ltd

- STMicroelectronics NV

- Maxim Integrated Products Inc.

- Fujitsu Ltd

- Intel Corporation

- Honeywell International Inc.

- Micron technologies Inc.

- Samsung Electronics Co. Ltd

- Crossbar Inc.

- Infineon Technologies AG

- Avalanche Technologies Inc.

- Adesto Technologies Corporation(Dialog Semiconductor PLC)

第8章投資分析

第9章:市場的未來

The Non-Volatile Memory Market size is estimated at USD 105.64 billion in 2025, and is expected to reach USD 184.18 billion by 2030, at a CAGR of 11.76% during the forecast period (2025-2030).

In the last decade, the growth of the portable systems market attracted the interest of the semiconductor industry in non-volatile memory (NVM) technologies for mass storage applications. Demand for greater efficiency, faster memory access, and low-power consumption drive the NVM market growth.

Key Highlights

- In the flourishing consumer electronics industry, users expect their devices to continually become more powerful, provide new functionality with incredible speed, and store more movies, pictures, and music. While flash enabled substantial innovation during the past few decades, a new generation of memory is required as flash hits technology roadblocks, preventing it from scaling much further.

- The adoption of flash memories in consumer electronics due to their low price and power consumption is significant for the market's growth. NVM is used in smartphones and wearable devices to enable more storage and faster memory access.

- The increasing research activities in this space are also driving the market's growth. For instance, in March 2021, Infineon Technologies LLC announced the launch of second-generation non-volatile Static RAMs that are qualified for QML-Q and high-reliability industrial specifications to mainly support non-volatile code storage in harsh environments, including aerospace and industrial applications.

- Similarly, in early 2021, Samsung announced the improvement of its MRAM's MTJ function and advanced its 14 nm process to support its flash-type embedded MRAM designed to increase the write speed and density. In addition, the company targets the IC emerging NVM's application in wearables, microcontrollers, and IoT devices.

- However, troubles with non-volatile memories in the market are often caused by the read/write endurance and data retention characteristics. For instance, Phase-change memories (PCMs) and flash memories are examples of NVM's with limited endurance. These NVM's have little endurance because after undergoing several writing cycles (RESET cycles for PCM, program/erase cycles for flash memory), the memory cells wear out and can no longer reliably store information.

- The COVID-19 outbreak negatively impacted several end-user industries of non-volatile memories, such as the smartphone industry. Spurred demand for server and PC memory for stay-at-home activities, driven by important megatrends like cloud computing, AI, and the IoT, is expected to support the growth of non-volatile memory during the forecast period.

Non-Volatile Memory Market Trends

Flash Memory is Expected to Hold a Significant Market Share

- The growing demand and penetration of consumer electronics led to device flash memory applications. This memory type finds applications in laptops, GPS, electronic musical instruments, digital cameras, cell phones, and many others. Additionally, it is extensively adopted by data center solution vendors. With exponential growth in the adoption of cloud solutions, the demand for data centers is also surging.

- Further, with increasing propensity toward AI/ML applications and IoT devices that require high low latency and high throughput cloud storage, flash storage and enterprise data centers are optimized to train deep neural networks. The growing number and size of data centers are expected to augment demand further.

- To cater to the growing demand, vendors operating in the market focus on developing new solutions with better capabilities. For instance, in February 2021, Kioxia Corporation and Western Digital Corp. announced the development of a sixth-generation, 162-layer 3D flash memory technology. This was the company's highest density and most advanced 3D flash memory technology that utilizes many technology and manufacturing innovations.

- Furthermore, NOR Flash memory is also gaining traction due to ultra-low-power needs. For instance, in January 2022, Infineon Technologies announced additional development tools to support its family of SEMPER NOR Flash devices. It will further help developers to quickly design safety-critical and inherently secure automotive, industrial, and communication systems.

- Similarly, in November 2021, Macronix International Co., Ltd. announced itself as the industry's first Serial NOR Flash memory manufacturer to bring 1.2V devices to mass production. According to the company, the ultra-low-power (ULP), high-speed 120MHz MX25S Serial NOR Flash memories are poised to usher in a new generation of products targeted at applications that include Internet of Things (IoT), wireless communications technologies, WiFi, and Narrowband IoT systems, hand-held and Bluetooth devices, and consumer applications.

Asia Pacific is Expected to Account for a Significant Market Share

- The construction of new infrastructure, including data centers, has been growing across various countries of the Asia Pacific region, owing to a surge in demand for online entertainment, telecommuting, and video and voice call services. With the fast development of the digital economy, building large big data centers in countries such as China and India is becoming necessary.

- China has emerged as the leading country owing to its aggressive approach to the NAND memory business. For instance, Yangtze Memory Technologies Co. Ltd (YMTC), one of China's major memory companies, had shipped 64 layers of NAND domestically in low volumes, including SSDs, with 128-layer production in development and shipments in 2021.

- Furthermore, startups in the region that are engaged in developing technologies related to non-volatile memory are receiving several investments. For instance, in April 2021, InnoStar Semiconductor (Shanghai) Co. Ltd raised around USD 100 million in a pre-series A financing round. The funding round was led by Shanghai Lianhe Investment, and new investors who joined the round included state-backed Atlas Capital and KQ Capital. The company aims to use the investment to produce resistive random-access memory (ReRAM) chips and other chips for storage applications.

- Companies in the region are utilizing non-volatile memory for various industrial applications. In November 2021, Floadia Corporation, a provider of Non-Volatile Memory (NVM) technology, announced the availability of its high-quality eNVM (embedded Non-volatile Memory), with product name ZT, supporting 150 degrees C retention of 10 years, in Shanghai Huahong Grace Semiconductor Manufacturing Corporation 180BCD (Z8) platform.

- Furthermore, the region is also witnessing an increase in R&D activities in Non-Volatile Memory (NVM). In January 2022, Samsung Electronics announced the demonstration of one of the world's first in-memory computing based on MRAM (Magnetoresistive Random Access Memory). Such trends are expected to drive the growth of the studied market in the Asia Pacific region during the forecast period.

Non-Volatile Memory Industry Overview

The non-volatile memory market is competitive and consists of several major players. The competitive rivalry in this industry is primarily dependent on sustainable competitive advantage through innovation, levels of market penetration, and power of competitive strategy. Since the market is capital intensive, the barriers to exit are high as well. Some of the major players operating in the market include Rohm Co. Ltd, STMicroelectronics NV, Fujitsu ltd, and Intel Corporation. Some of the recent developments in the market are:

- January 2022 - SK Hynix Inc. announced the completion of the first phase of the transaction to acquire Intel's NAND and solid-state drive (SSD) business. According to the company, it has closed the first phase of the transaction by acquiring Intel's SSD business and the Dalian NAND flash manufacturing facility in China.

- October 2021 - NSCore Inc. introduced OTP+, One-Time-Programmable Plus, a non-volatile memory solution for IoT technology applications. According to the company, the 40 nm Ultra-Low-Power OTP NVM IP Solution can minimize the need to re-spin the fabrication of an IoT chip, which is critical in the emerging market. In addition, the NSCore OTP+ solution can be reprogramed and modified, unlike standard OTP Ip solutions.

- July 2021 - Micron Technology announced that it began mass shipping the world's first 176-layer NAND Universal Flash Storage (UFS) 3.1 mobile solution. Designed for high-end and flagship phones, Micron's UFS 3.1 discrete mobile NAND memory unlocks the potential of 5G with sequential write and random read speeds of up to 75% compared to previous generations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Non-volatile Memory in Connected and Wearable Devices

- 5.1.2 Increasing Demand for Enterprise Storage Applications

- 5.2 Market Challenges

- 5.2.1 Low Write Endurance Rate

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Traditional Non-volatile Memory

- 6.1.1.1 Flash Memory

- 6.1.1.2 EEPROM

- 6.1.1.3 SRAM

- 6.1.1.4 EPROM

- 6.1.1.5 Other Traditional Non-volatile Memories

- 6.1.2 Next-generation Non-volatile Memory

- 6.1.2.1 MRAM

- 6.1.2.2 FRAM

- 6.1.2.3 ReRAM

- 6.1.2.4 3D-X Point

- 6.1.2.5 Nano RAM

- 6.1.2.6 Other Next-generation Non-volatile Memories

- 6.1.1 Traditional Non-volatile Memory

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Retail

- 6.2.3 IT and Telecom

- 6.2.4 Healthcare

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 South Korea

- 6.3.3.4 India

- 6.3.3.5 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ROHM Co. Ltd

- 7.1.2 STMicroelectronics NV

- 7.1.3 Maxim Integrated Products Inc.

- 7.1.4 Fujitsu Ltd

- 7.1.5 Intel Corporation

- 7.1.6 Honeywell International Inc.

- 7.1.7 Micron technologies Inc.

- 7.1.8 Samsung Electronics Co. Ltd

- 7.1.9 Crossbar Inc.

- 7.1.10 Infineon Technologies AG

- 7.1.11 Avalanche Technologies Inc.

- 7.1.12 Adesto Technologies Corporation (Dialog Semiconductor PLC)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

非揮發性雙列直插式記憶體模組市場規模、佔有率、趨勢分析報告:按產品、容量、最終用途、地區和細分市場預測,2025 年至 2030 年

非揮發性雙列直插式記憶體模組市場規模、佔有率、趨勢分析報告:按產品、容量、最終用途、地區和細分市場預測,2025 年至 2030 年 非揮發性雙列直插式記憶體模組市場規模、佔有率及成長分析(按產品、容量、應用、最終用戶和地區)-2025 年至 2032 年產業預測

非揮發性雙列直插式記憶體模組市場規模、佔有率及成長分析(按產品、容量、應用、最終用戶和地區)-2025 年至 2032 年產業預測 2025 年非揮發性記憶體全球市場報告2025 年非揮發性記憶體標準 (NVMe) 全球市場報告

2025 年非揮發性記憶體全球市場報告2025 年非揮發性記憶體標準 (NVMe) 全球市場報告 新興非揮發性記憶體:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)嵌入式非揮發性記憶體市場 - 按產品、垂直產業、地區和競爭細分的全球產業規模、佔有率、趨勢、機會和預測,2019-2029 年新一代非揮發性記憶體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、晶圓尺寸、組織規模、最終用戶、地區和競爭細分,2019-2029F

新興非揮發性記憶體:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)嵌入式非揮發性記憶體市場 - 按產品、垂直產業、地區和競爭細分的全球產業規模、佔有率、趨勢、機會和預測,2019-2029 年新一代非揮發性記憶體市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、晶圓尺寸、組織規模、最終用戶、地區和競爭細分,2019-2029F NVDIMM(Non-volatile Dual In-line Memory Module)市場:成長、未來展望與競爭分析(2025-2033)

NVDIMM(Non-volatile Dual In-line Memory Module)市場:成長、未來展望與競爭分析(2025-2033) NanoRAM 市場:按類型、應用分類 - 2025-2030 年全球預測下一代非揮發性記憶體市場:按產品類型、晶圓尺寸和最終用戶分類 - 2025-2030 年全球預測

NanoRAM 市場:按類型、應用分類 - 2025-2030 年全球預測下一代非揮發性記憶體市場:按產品類型、晶圓尺寸和最終用戶分類 - 2025-2030 年全球預測