|

市場調查報告書

商品編碼

1689739

東南亞電池:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Southeast Asia Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

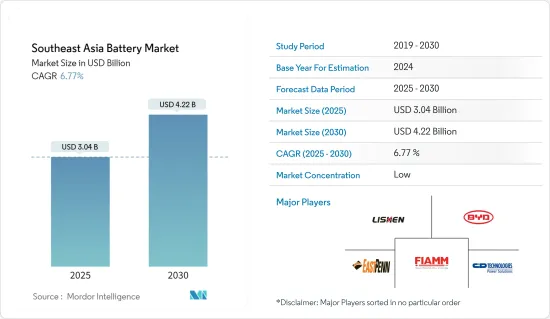

預計2025年東南亞電池市場規模為30.4億美元,到2030年將達到42.2億美元,預測期內(2025-2030年)的複合年成長率為6.77%。

儘管2020年新冠疫情對市場產生了負面影響,但目前已恢復至疫情前的水準。

主要亮點

- 從中期來看,汽車產業需求成長、鋰離子電池價格下降以及將東南亞定位為資料中心樞紐的計畫等因素預計將在預測期內推動市場發展。

- 儘管汽車、資料中心和通訊領域對電池的需求不斷成長,但由於大多數國家依賴其他形式的能源儲存,預計電池能源儲存產業仍將保持低迷。這可能會在預測期內抑制能源儲存領域電池市場的成長。

- 此外,預計在預測期內,將可再生能源納入各國電網的計畫將為鋰離子電池製造商和供應商帶來巨大的商機。

- 由於汽車、資料中心和其他終端用戶領域的需求不斷增加,預計泰國將在預測期內佔據市場主導地位。

東南亞電池市場趨勢

預計汽車產業將主導市場

- 以前僅使用內燃機車輛(ICE)。內燃機汽車使用鉛酸電池,並且很可能繼續使用而不需要進行大規模更換。

- 但現在,由於人們對環境問題的日益關注,科技正在轉向電動車。電動車主要使用鋰離子電池,這種電池能量密度高、自放電低,幾乎不需要維護。

- 鋰離子電池系統為插電式混合動力汽車和混合動力汽車車提供動力。鋰離子電池具有高能量密度、快速充電能力和高放電功率,是唯一能夠滿足OEM對車輛續航里程和充電時間要求的技術。鉛基牽引電池比能量低、重量大,在全混合動力汽車和電動車上使用不具競爭力。

- 此外,鋰離子電池價格大幅下跌,導致其價值下降了 81.5%,從 2013 年的 668 美元/千瓦時跌至 2021 年的 123 美元/kWh。預計這一趨勢將持續下去,使該地區更廣泛的經濟人群能夠更負擔得起電動車。

- 在混合動力汽車中,有多種電池技術可以以各種組合提供這些功能,但鎳氫和鋰離子電池由於其快速充電能力、良好的放電性能和持久的壽命,在高電壓下更受青睞。

- 隨著多個地區政府制定排放計劃,預計預測期內電動車(EV)的區域佔有率將會增加。

- 因此,基於上述因素,預計預測期內汽車產業將主導東南亞電池市場。

泰國可望主導市場

- 泰國佔據大部分市場佔有率。由於汽車、資料中心和通訊業的需求不斷增加,預計這一趨勢將在預測期內持續下去。

- 泰國的汽車產業具有巨大的投資潛力。該國是東南亞國家聯盟主要汽車生產基地之一。五十年來,中國從一個汽車零件組裝發展成為汽車製造和出口的頂級中心。

- 此外,預計該國的電動車領域將實現高速成長,尤其是插電式混合動力車 (PHEV) 和混合動力車 (HEV)。 2022年9月,比亞迪宣布計畫在曼谷羅勇府興建海外首個電動乘用車工廠。

- 國家電動車政策委員會 (NEVPC) 發布的藍圖顯示,泰國到 2025 年將增加 10 萬至 30 萬輛汽車,到 2026 年最終將增加 40 萬至 75 萬輛汽車。

- 此外,2022 年 4 月,泰國政府同意資助生產為電動車 (EV)動力來源的鋅離子電池。泰國將在當地建立電動車電池工廠,利用天然資源鋅。

- 此外,泰國在資訊通訊技術行業的發展方面取得了長足進步,迅速將該國從技術領域的二流參與者提升為地區領先者之一。過去十年,泰國的數位化足跡加速發展,並在勞動力教育和技能建設方面取得了長足的進步。

- 政府已在泰國4.0計劃下規劃了一個商業模組。該計劃推動雲端處理、互動媒體、巨量資料和物聯網等新技術的使用。因此,該國對資料中心的需求很高,預計預測期內對資料中心電池的需求將增加。

- 因此,基於上述因素,預計泰國將在預測期內主導東南亞電池市場。

東南亞電池產業概況

東南亞電池市場較為分散,主要企業包括天津力神電池股份有限公司、FIAMM Energy Technology SpA、比亞迪、C&D Technologies Inc. 和 East Penn Manufacturing Co. Inc.(排名不分先後)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 2028 年市場規模與需求預測

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 限制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 依電池類型

- 鉛酸電池

- 鋰離子電池

- 其他電池類型

- 按最終用戶

- 車

- 資料中心

- 通訊

- 能源儲存

- 其他最終用戶

- 按地區

- 印尼

- 馬來西亞

- 菲律賓

- 新加坡

- 泰國

- 越南

- 緬甸

- 其他東南亞地區

第6章 競爭格局

- 併購、合資、合作、協議

- 主要企業策略

- 公司簡介

- BYD Co. Ltd.

- C&D Technologies Inc.

- East Penn Manufacturing Co. Inc.

- Tianjin Lishen Battery Joint-Stock Co. Ltd.

- Exide Industries Ltd.

- FIAMM Energy Technology SpA

- GS Yuasa Corporation

- LG Chem Ltd.

- Panasonic Corporation

- Saft Groupe SA

- Samsung SDI Co. Ltd.

- Clarios

- Tesla Inc.

- Leoch International Technology Limited

第7章 市場機會與未來趨勢

The Southeast Asia Battery Market size is estimated at USD 3.04 billion in 2025, and is expected to reach USD 4.22 billion by 2030, at a CAGR of 6.77% during the forecast period (2025-2030).

Though COVID-19 negatively impacted the market in 2020, it has reached pre-pandemic levels.

Key Highlights

- Over the medium term, factors such as growing demand from the automotive sector, declining lithium-ion battery prices, and plans to make Southeast Asia a data center hub are expected to drive the market during the forecast period.

- Despite the growing demand for batteries in the automotive, data centers, and telecommunications sectors, the battery energy storage segment is expected to witness stagnant growth, as most countries depend on other energy storage alternatives. This, in turn, is likely to restrain the growth of the battery market in the energy storage segment during the forecast period.

- Moreover, plans to integrate renewable energy with the national grids in respective countries are expected to create significant opportunities for lithium-ion battery manufacturers and suppliers during the forecast period.

- Thailand is expected to dominate the market during the forecast period due to the increasing demand from the automotive, data center, and other end-user sectors.

Southeast Asia Battery Market Trends

Automotive Sector is Expected to Dominate the Market

- Vehicles with internal combustion engines (ICE) were the only types used earlier. ICE vehicles have been using lead-acid batteries, which may continue with no significant replacement available.

- However, nowadays, technology has been shifting toward electric vehicles due to rising concerns about the environment. In EVs, mostly lithium-ion batteries are used, as they provide high energy density, have low self-discharge, and require little maintenance.

- Lithium-ion battery systems propel plug-in hybrid and electric vehicles. Due to their high energy density, fast recharge capability, and high discharge power, lithium-ion batteries are the only available technology that meets the OEM requirements for vehicles' driving range and charging time. Lead-based traction batteries are not competitive for use in full-hybrid electric cars or electric vehicles because of their lower specific energy and higher weight.

- Moreover, the exponential decline in lithium-ion batteries' prices reduced their value by 81.5% from USD 668/kWh in 2013 to USD 123/kWh in 2021. The trend is likely to continue in the future, making EVs affordable to a broader range of economic groups in the region.

- For hybrid vehicles, several battery technologies can provide these functions in different combinations, with nickel-metal hydride and lithium-ion batteries preferred at higher voltages due to their fast recharge capability, good discharge performance, and lifetime endurance.

- Several regional governments developed plans to reduce emissions, which are expected to increase the region's share of electric vehicles (EV) during the forecast period.

- Therefore, owing to the abovementioned factors, the automotive sector is expected to dominate the Southeast Asian battery market during the forecast period.

Thailand is Expected to Dominate the Market

- Thailand accounts for the majority share of the market. This trend is expected to continue during the forecast period, owing to the increasing demand from the automotive, data center, and telecom sectors.

- Thailand provides great investment potential for the automotive sector. The country has a leading automotive production base in the Association of Southeast Asian Nations. The country has developed from an assembler of auto components into a top automotive manufacturing and export hub in over 50 years.

- Moreover, the country is expected to witness high growth in the EV segment, particularly in plug-in hybrid electric vehicles (PHEVs) and hybrid electric vehicles (HEVs). In September 2022, BYD Co. announced plans to build its first overseas electric passenger car plant in Rayong, Bangkok.

- Under the National Electric Vehicle Policy Committee (NEVPC) roadmap, Thailand is expected to add between 100,000 and 300,000 vehicles by 2025 and finally between 400,000 and 750,000 vehicles by 2026.

- Further, in April 2022, the Thai government agreed to fund the manufacturing of zinc-ion batteries to power electric vehicles (EVs). Thailand will develop a local EV battery plant worth using zinc as a natural resource.

- Furthermore, Thailand has made great progress in growing its ICT sector, moving quickly from being a secondary player in the world of technology to one of the regional leaders. Over the past decade, the digital share in Thailand has been closing at an ever-increasing speed, with the country making significant gains in labor force education and skills building.

- The government planned its business module under Thailand's 4.0 Program. This program helps increase the use of new technologies such as cloud computing, interactive media, big data, and the internet of things. Hence, the country is expected to have a high demand for data centers, which is expected to increase the demand for batteries in its data centers during the forecast period.

- Therefore, owing to the abovementioned factors, Thailand is expected to dominate the Southeast Asian battery market during the forecast period.

Southeast Asia Battery Industry Overview

The Southeast Asian battery market is partially fragmented due to the presence of key players, including (in no particular order) Tianjin Lishen Battery Joint-Stock Co. Ltd., FIAMM Energy Technology SpA, BYD Co. Ltd., C&D Technologies Inc., and East Penn Manufacturing Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery Type

- 5.1.1 Lead-acid Battery

- 5.1.2 Lithium-ion Battery

- 5.1.3 Other Battery Types

- 5.2 By End-User

- 5.2.1 Automotive

- 5.2.2 Data Centers

- 5.2.3 Telecommunication

- 5.2.4 Energy Storage

- 5.2.5 Other End-Users

- 5.3 By Geography

- 5.3.1 Indonesia

- 5.3.2 Malaysia

- 5.3.3 Philippines

- 5.3.4 Singapore

- 5.3.5 Thailand

- 5.3.6 Vietnam

- 5.3.7 Myanmar

- 5.3.8 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd.

- 6.3.2 C&D Technologies Inc.

- 6.3.3 East Penn Manufacturing Co. Inc.

- 6.3.4 Tianjin Lishen Battery Joint-Stock Co. Ltd.

- 6.3.5 Exide Industries Ltd.

- 6.3.6 FIAMM Energy Technology SpA

- 6.3.7 GS Yuasa Corporation

- 6.3.8 LG Chem Ltd.

- 6.3.9 Panasonic Corporation

- 6.3.10 Saft Groupe SA

- 6.3.11 Samsung SDI Co. Ltd.

- 6.3.12 Clarios

- 6.3.13 Tesla Inc.

- 6.3.14 Leoch International Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年電池市場報告,按類型(一次電池、二次電池)、產品(鋰離子電池、鉛酸電池、鎳氫電池、鎳鎘電池等)、應用(汽車電池、工業電池、攜帶式電池)和地區分類

2025 年至 2033 年電池市場報告,按類型(一次電池、二次電池)、產品(鋰離子電池、鉛酸電池、鎳氫電池、鎳鎘電池等)、應用(汽車電池、工業電池、攜帶式電池)和地區分類 量子電池市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按技術類型、按原料、按應用、按地區、按競爭,2020-2030F

量子電池市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按技術類型、按原料、按應用、按地區、按競爭,2020-2030F NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)亞太地區 NMC 電池組市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美 NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)拉丁美洲電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)日本電池市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲 NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)

NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)亞太地區 NMC 電池組市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美 NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)拉丁美洲電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)日本電池市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲 NMC 電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年) 燃料電池與電池組研究回顧:2024 年

燃料電池與電池組研究回顧:2024 年