|

市場調查報告書

商品編碼

1690059

3D 感測和成像:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)3D Sensing And Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

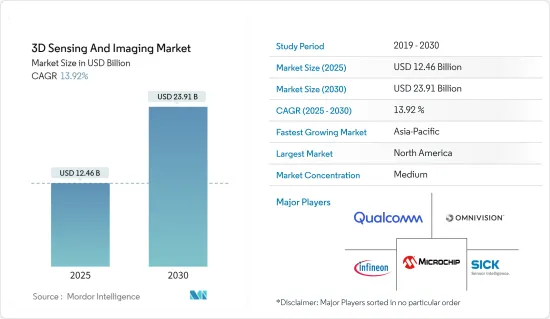

3D 感測和成像市場規模預計在 2025 年為 124.6 億美元,預計到 2030 年將達到 239.1 億美元,預測期內(2025-2030 年)的複合年成長率為 13.92%。

主要亮點

- 隨著感測器擴大被各行各業所採用,能夠即時測量形狀的 3D 技術正在開發中。 3D 感測市場主要由用於臉部辨識和 AR 的 3D 智慧型手機感測器的整合推動,從而增強安全性和用戶體驗。

- 家庭遊戲產業是 3D 感測技術首批實用化消費應用之一。飛行時間(ToF) 感應器捕捉玩家的手勢和動作,以創造新的互動遊戲體驗。然而,3D感應在當今的智慧型手機技術中最為突出。為使用者提供 3D 掃描,透過臉部辨識提高安全性,而為世界提供 3D 感應,為強大的深度感應攝影和擴增實境創造了新的機會。

- 在醫療保健領域,3D感測將提高醫學影像和手術的準確性。此外,工業自動化受益於用於品管和機器人技術的 3D 感測器,而遊戲和娛樂產業則使用 3D 感測器實現身臨其境型AR 和 VR 體驗。預計技術進步和成本下降將進一步推動市場成長機會。

- 此外,影像感測器在汽車中的廣泛應用極大地推動了市場的成長。這些汽車感測器的主要應用領域包括儀表板攝影機、ADAS(高級駕駛輔助系統)、LiDAR 駕駛員監控和手勢姿態辨識系統。在目前的市場狀況下,汽車產業以ADAS(高級駕駛輔助系統)和由5G和物聯網支援的自動駕駛汽車為特色,使得3D感測成為交通安全的重要組成部分。 LiDAR 系統還提供短程和遠距3D 感應,使車輛能夠在即時情境中獨立評估周圍環境。

- 產業主要市場參與者正致力於推出新產品。例如,2024 年 4 月,為實體安全和商業智慧應用提供 3D LiDAR 技術的 Quanergy Solutions Inc. 在其 3D LiDAR 解決方案組合中增加了兩款新產品。全新 Q-Track HD 和 Q-Track Dome 3D LiDAR 感測器加入 Quanergy 的 Q-Track LR(長距離)產品,提供業界最全面的高效能 3D LiDAR 解決方案組合。 Quanergy 3D LiDAR 偵測、分類和追蹤技術的精確度是傳統技術的 20 倍,但成本卻不到傳統技術的一半。

- 然而,影像感測器的製造成本高、與其他設備的整合選項有限、以及維護這些設備所需的高成本是預測期內限制市場成長機會的一些因素。

- 由於消費者支出趨勢下降導致全球經濟宏觀放緩,工業和消費 3D 感測市場在 COVID-19 期間受到負面影響。然而,在後疫情時代,由於 3D 感測和成像技術應用的需求將會增加。

3D 感測和成像市場趨勢

汽車產業可望推動市場成長

- 建立全面的環境 3D 地圖需要捕獲廣泛的資料,從幾百公尺外發生的情況到駕駛員的警覺程度。 LiDAR(光檢測和測距)是遠距和短距離掃描的基本技術之一,因為它比基於傳統掃描的感測器(如攝影機或基於雷達的影像處理)能夠捕捉更多細節並實現更高的精度。

- LiDAR 主要用於汽車的 ADAS(高級駕駛輔助系統),以提高駕駛的便利性。這些系統使用人機介面,實現平穩、安全的引導操作。車輛的自動駕駛特性需要相當高程度的精確度和輔助,特別是在障礙物偵測方面,以確保道路上的安全行駛和避障。

- 汽車產業對 LiDAR 的應用日益廣泛,將大大促進 3D 感測市場的發展。對高解析度、即時環境地圖的需求日益成長,這對於 ADAS(高級駕駛輔助系統)和自動駕駛汽車至關重要。與其他感測技術相比,雷射雷達具有更高的精度和可靠性,將增強汽車的安全性和導航能力。業界的關注將推動技術進步、降低成本並使 3D 感測解決方案更容易獲得。隨著汽車製造商和科技公司對自動駕駛汽車雷射雷達的大力投資,3D 感測的整體市場將會成長,從而刺激各領域的進一步創新和應用。

- 2023 年 7 月,光學半導體先驅 Lumotive 與相機模組專家 Namuga 簽署了商業協議。該協議將利用 Lumotive 的光控制超表面 (LCM) 晶片組為工業、消費性和汽車市場的各種 3D 感測應用創建固體雷達模組解決方案。

- 根據OICA預測,2023年全球乘用車銷售量將達到約6,527萬輛,2022年全球乘用車銷售量將達到約5,864萬輛,全球整體乘用車總銷量將大幅增加。因此,預計預測期內乘用車和汽車的大幅成長將極大地推動市場的成長機會。

預計北美將佔據很大市場佔有率

- 預計北美將佔據大部分市場佔有率。美國是該地區最重要的市場。汽車和電子消費領域對 3D 感測器的需求很高,這些領域正在將 3D 感測器用於各種應用。加拿大也是一個重要的 3D 感測市場,先進技術的應用越來越多,特別是在娛樂、廣告和醫療產業。

- 北美 3D 感測市場受到多種因素推動,主要包括 ADAS(高級駕駛輔助系統)和自動駕駛汽車的快速普及、具有 3D 感測功能(如臉部辨識和擴增實境)的智慧型手機和家用電器的廣泛應用,以及對醫學成像和診斷等醫療保健應用的大量投資。此外,該地區對物聯網的投資不斷增加也推動了市場成長。物聯網已被認定為聯邦研發投資的發展領域之一。

- 此外,強大的研發計劃、強大的技術生態系統以及對安全和監控解決方案的不斷成長的需求進一步推動了該地區的市場成長。這些促進因素,加上技術進步和創新,確保了市場成長機會不斷擴大。

- 該地區的博彩業一直在穩步成長。由於顧客在家中花費的時間越來越多,最近遊戲設備的流行趨勢也越來越明顯,這種情況尤其如此。美國是遊戲產業最重要的市場之一。 AR/VR 裝置、手持操縱桿和其他遊戲裝置大量使用 3D 感測器和 3D 影像攝影機實現螢幕互動。

- 2024 年 2 月,Polyga 推出了其流行的桌上型 3D 掃描器的下一代產品——用於掃描小物體的 Compact S5 Macro 3D 感測器。 Compact S5 Macro 是一款工業 3D 掃描儀,可協助工程師以大約 5 微米的精度將 1 到 5 公分之間的零件數位化。它可以在不到一秒的時間內創建高解析度的 3D 掃描,並且裝在堅固的機殼中。

3D 感測與成像產業概況

3D 感測市場已固體,擁有許多地區性和全球性參與者。此外,隨著技術創新和永續產品的興起,許多公司透過贏得新契約和開拓新市場來擴大其整體市場佔有率,以保持其在全球市場中的地位。主要進展包括:

- 2024 年 5 月,光學半導體技術先驅 Lumotive 和全球感測器和自動化供應商 Hokuyo Auto商業性推出了 YLM-10LX 3D 雷射雷達感測器。該產品主要採用 Lumotive 的光控超表面 (LCM) 光束成形技術,該技術代表著透過應用固體可程式光學技術在服務機器人和工業自動化應用中轉變 3D 感應的重大飛躍。

- 2024年2月,意法半導體推出了具有2.3k解析度的一體化直接飛行時間(dToF)3D LiDAR(光檢測和測距)模組。此模組可用於多種應用,包括攝影機輔助、虛擬實境、3D 網路攝影機、機器人和智慧建築。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- 新冠肺炎疫情的後續影響和其他宏觀經濟因素將影響市場

第5章 市場動態

- 市場促進因素

- 微型電子設備中光學和電子元件的整合

- 對 3D 消費性電子設備的需求不斷成長

- 影像感測器在汽車中的普及率不斷提高

- 安全和監控系統的需求不斷增加

- 市場限制

- 影像感測器製造成本高

- 與其他設備的整合有限

- 維護成本高

第6章 市場細分

- 按組件

- 硬體

- 軟體

- 按服務

- 依技術分類

- 超音波

- 結構光源

- 飛行時間 (ToF)

- 立體視覺

- 其他技術

- 按類型

- 位置感測器

- 影像感測器

- 溫度感測器

- 加速計感測器

- 接近感測器

- 其他類型

- 連結性別

- 有線網路連接

- 無線網路連線

- 按最終用戶產業

- 消費性電子產品

- 車

- 衛生保健

- 航太和國防

- 安全與監控

- 媒體與娛樂

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

第7章 競爭格局

- 公司簡介

- Infineon Technologies AG

- Microchip Technology Inc.

- Omnivision Technologies Inc.

- Qualcomm Inc.

- Sick AG

- Keyence

- Texas Instruments Incorporated

- GE Healthcare

- STMicroelectronics

- Google Inc.

- Adobe Inc.

- Autodesk Inc.

- Panasonic Corporation

- Trimble

- Faro

- Lockheed Martin

- Dassault Systems

第8章投資分析

第9章 市場機會與未來趨勢

簡介目錄

Product Code: 69681

The 3D Sensing And Imaging Market size is estimated at USD 12.46 billion in 2025, and is expected to reach USD 23.91 billion by 2030, at a CAGR of 13.92% during the forecast period (2025-2030).

Key Highlights

- The increasing adoption of sensors in various industry verticals has led to the overall development of 3D technology that can measure shapes in real-time scenarios. The 3D sensing market is primarily driven by integrating 3D smartphone sensors for facial recognition and AR, enhancing security and user experience.

- The home gaming industry presented one of the first practical applications of 3D sensing technology for consumers, with time-of-flight (ToF) sensors that capture players' gestures and movements to build a new interactive gaming experience. However, 3D sensing is most noticeable in today's smartphone technology. User-facing 3D scanning increases security through facial recognition while world-facing 3D sensing establishes new opportunities for high-performance depth-sensing photography and augmented reality.

- In the healthcare sector, 3D sensing improves medical imaging and surgical precision. Additionally, industrial automation benefits from 3D sensors for quality control and robotics, while the gaming and entertainment industries use them for immersive AR and VR experiences. Technological advancements and decreasing costs are expected to further propel the market's growth opportunities significantly.

- Moreover, the growing application of image sensors in automobiles is considerably pushing the market's growth. Some of the key application areas of these automobile sensors involve dash cameras, advanced driver assistance systems (ADAS), LiDAR driver monitoring, and gesture recognition systems, among others. In the current market situation, the automotive industry features advanced driver-assistance systems (ADAS) and autonomous vehicles enabled by 5G and the IoT, making 3D sensing a vital part of transportation safety. The LiDAR systems also provide short- and long-range 3D sensing that allows vehicles to assess their surroundings in real-time scenarios independently.

- The major market players in the industry are focusing on introducing new products. For instance, in April 2024, Quanergy Solutions Inc., a provider of 3D LiDAR technology for physical security and business intelligence applications, launched two new additions to its portfolio of 3D LiDAR solutions. The new Q-Track HD and Q-Track Dome 3D LiDAR sensors join Quanergy's Q-Track LR (Long Range) offering to comprise the industry's most comprehensive portfolio of high-performance 3D LiDAR solutions. Quanergy 3D LiDAR detection, classification, and tracking technology provides 20X the accuracy of legacy technologies at less than half the cost.

- However, factors like the high manufacturing cost of image sensors, limited integration options with other devices, and the involvement of high costs required to maintain these devices are some factors that can restrain the market's growth opportunities during the forecast period.

- The 3D sensing market for industrial and consumer applications was negatively affected during the COVID-19 period due to the decline in consumer spending trends that led to the macro slowdown of the economy across the world. However, during the post-COVID-19 environment, the increasing adoption of 3D sensing and imaging technology, especially in smartphones, gaming consoles, and the automotive industry, is expected to increase the demand for 3D sensing technology applications.

3D Sensing and Imaging Market Trends

The Automotive Segment is Expected to Drive the Market's Growth

- Capturing a wide range of data, from what is happening within hundreds of meters down the road to how cautious the driver is, is required to build a comprehensive 3D map of the environment. LiDAR (light detection and ranging), which catches more detailed information and delivers more accuracy than classic scanning-based sensors like camera and radar-based imaging, is one of the vital technologies for long and short-range scanning.

- LiDAR is mainly used in automobiles for advanced driver assistance systems (ADAS) to facilitate driver convenience. These systems use a human-machine interface for smooth and safe guidance operations. The vehicle's autonomous nature requires considerably high accuracy and assistance, especially for obstacle detection, to ensure safe navigation and avoidance through the roadways.

- The growing use of lidar in the automotive industry significantly boosts the 3D sensing market. It enhances the demand for high-resolution, real-time environmental mapping essential for advanced driver assistance systems (ADAS) and autonomous vehicles. Lidar's superior accuracy and reliability over other sensing technologies enhance vehicle safety and navigation capabilities. This industry focus encourages technological advancements, reducing costs and making 3D sensing solutions more accessible. As automotive manufacturers and tech firms invest heavily in lidar for self-driving cars, the overall market for 3D sensing expands, stimulating further innovation and adoption across various sectors.

- In July 2023, Optical semiconductor pioneer Lumotive signed a commercial agreement with camera module specialist Namuga, which would leverage Lumotive's Light Control Metasurface (LCM) chipsets to build solid-state lidar module solutions for a range of 3D sensing applications in the industrial, consumer, and automotive markets.

- According to the OICA, in 2023, around 65.27 million passenger cars were sold globally, whereas around 58.64 million passenger cars were sold globally in 2022, representing a significant rise in the sales of the total number of passenger cars across the world. This significant rise in passenger cars and vehicles is thus expected to drive the market's growth opportunities significantly during the forecast period.

North America is Expected to Hold a Significant Share in the Market

- North America is expected to hold a significant share of the market. The United States is the most significant market in the region. There is a high demand from the consumer automotive and electronics sectors that employ 3D sensors for various applications in their domains. Canada is another significant 3D sensing market, owing to the increasing adoption of advanced technologies, especially in the entertainment, advertising, and medical industries.

- The 3D sensing market in North America is driven by several factors, primarily the quick adoption of advanced driver assistance systems (ADAS) and autonomous vehicles, the proliferation of smartphones and consumer electronics with 3D sensing capabilities (e.g., facial recognition and augmented reality), and significant investments in healthcare applications like medical imaging and diagnostics. The increasing investments in IoT in the region also aid in the market's growth. IoT has been identified as one of the developing areas of federal R&D investments.

- Additionally, strong R&D initiatives, a robust technology ecosystem, and increasing demand for security and surveillance solutions further propel the market's growth in the region. These drivers, coupled with technological advancements and innovation, ensure the continued expansion of the market's growth opportunities.

- The gaming industry in the region has been recording steady growth, especially due to customers spending a significant amount of time at home and the huge developments in gaming equipment in recent times. The United States has one of the most significant markets in the gaming industry. AR/VR devices, handheld joysticks, and other gaming equipment widely use 3D sensors and 3D imaging cameras for on-screen interactions.

- In February 2024, Polyga launched the Compact S5 Macro 3D Sensor For Scanning Small Objects, the next generation of its popular desktop 3D scanners. The Compact S5 Macro is primarily an industry-ready 3D scanner that allows engineers to digitize parts from 1 to 5 centimeters in size with about 5 microns accuracy. It creates high-resolution 3D scans in under a second and comes in a rugged enclosure.

3D Sensing and Imaging Industry Overview

The 3D sensing market is semi-consolidated with many regional and global players. Moreover, with increased innovations and sustainable products, many companies are expanding their overall market presence by securing new contracts and tapping new markets to maintain their position in the global market. Some of the key developments are:

- May 2024: Lumotive, a pioneer in optical semiconductor technology, and Hokuyo Automatic Co. Ltd, a global provider of sensors and automation, commercially introduced the YLM-10LX 3D lidar sensor. This product is primarily powered by Lumotive's Light Control Metasurface (LCM) optical beamforming technology that represents a major leap forward in terms of applying solid-state, programmable optics to transform 3D sensing throughout service robotics and industrial automation applications.

- February 2024: STMicroelectronics, a global semiconductor provider serving customers across the spectrum of electronics applications, launched an all-in-one, direct Time-of-Flight (dToF) 3D LiDAR (Light Detection and Ranging) module with 2.3k resolution. It can be used in multiple applications, such as camera assist, virtual reality, 3D webcams, robotics, and smart buildings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of the Aftereffects of the COVID-19 Pandemic and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Integration of Optical and Electronic Components in Miniaturized Electronics Devices

- 5.1.2 Rising Demand for 3D-enabled Devices in Consumer Electronics

- 5.1.3 Growing Penetration of Image Sensors in Automobiles

- 5.1.4 Growing Requirement of Security and Surveillance Systems

- 5.2 Market Restraints

- 5.2.1 High Manufacturing Cost of Image Sensors

- 5.2.2 Limited Integration With Other Devices

- 5.2.3 High Cost Required for the Maintenance of these Devices

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 By Technology

- 6.2.1 Ultrasound

- 6.2.2 Structured Light

- 6.2.3 Time of Flight

- 6.2.4 Stereoscopic Vision

- 6.2.5 Other Technologies

- 6.3 By Type

- 6.3.1 Position Sensor

- 6.3.2 Image Sensor

- 6.3.3 Temperature Sensor

- 6.3.4 Accelerometer Sensor

- 6.3.5 Proximity Sensor

- 6.3.6 Other Types

- 6.4 By Connectivity

- 6.4.1 Wired Network Connectivity

- 6.4.2 Wireless Network Connectivity

- 6.5 By End-user Industry

- 6.5.1 Consumer Electronics

- 6.5.2 Automotive

- 6.5.3 Healthcare

- 6.5.4 Aerospace and Defense

- 6.5.5 Security and Surveillance

- 6.5.6 Media and Entertainment

- 6.5.7 Other End-user Industries

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia-Pacific

- 6.6.4 Middle East and Africa

- 6.6.5 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Microchip Technology Inc.

- 7.1.3 Omnivision Technologies Inc.

- 7.1.4 Qualcomm Inc.

- 7.1.5 Sick AG

- 7.1.6 Keyence

- 7.1.7 Texas Instruments Incorporated

- 7.1.8 GE Healthcare

- 7.1.9 STMicroelectronics

- 7.1.10 Google Inc.

- 7.1.11 Adobe Inc.

- 7.1.12 Autodesk Inc.

- 7.1.13 Panasonic Corporation

- 7.1.14 Trimble

- 7.1.15 Faro

- 7.1.16 Lockheed Martin

- 7.1.17 Dassault Systems

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

2025 年 3D 感測器全球市場報告

2025 年 3D 感測器全球市場報告 深度感測市場規模、佔有率和成長分析(按組件、類型、技術、垂直和地區)- 產業預測 2025-20323D 影像感測器市場規模、佔有率、成長分析(按類型、技術、最終用途產業、性別和地區)- 產業預測,2025 年至 2032 年

深度感測市場規模、佔有率和成長分析(按組件、類型、技術、垂直和地區)- 產業預測 2025-20323D 影像感測器市場規模、佔有率、成長分析(按類型、技術、最終用途產業、性別和地區)- 產業預測,2025 年至 2032 年 3D 感測器 -市場佔有率分析、產業趨勢/統計、成長預測 (2025-2030)

3D 感測器 -市場佔有率分析、產業趨勢/統計、成長預測 (2025-2030) 3D 感測器市場:按產品類型、技術和最終用途 – 2025-2030 年全球預測深度感測市場:按組件、類型、技術、深度範圍、最終用戶分類 - 2025-2030 年全球預測

3D 感測器市場:按產品類型、技術和最終用途 – 2025-2030 年全球預測深度感測市場:按組件、類型、技術、深度範圍、最終用戶分類 - 2025-2030 年全球預測 全球 3D 感測器市場:市場規模、佔有率、趨勢分析報告 - 按連接性別、最終用途、類型、技術、地區、展望、預測,2024-2031 年3D 感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、連接性、最終用途、地區和競爭細分,2019-2029 年

全球 3D 感測器市場:市場規模、佔有率、趨勢分析報告 - 按連接性別、最終用途、類型、技術、地區、展望、預測,2024-2031 年3D 感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、技術、連接性、最終用途、地區和競爭細分,2019-2029 年 全球深度感測市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2033)

全球深度感測市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2033) 3D 感測器的全球市場規模:按類型、技術、地區劃分,2024-2031 年

3D 感測器的全球市場規模:按類型、技術、地區劃分,2024-2031 年

▼