|

市場調查報告書

商品編碼

1690934

北美食品服務包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)North America Foodservice Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

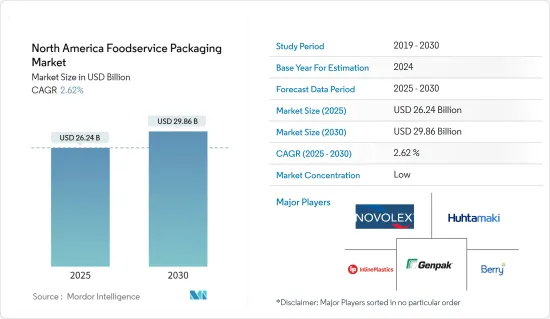

北美食品服務包裝市場規模預計在 2025 年為 262.4 億美元,預計到 2030 年將達到 298.6 億美元,預測期內(2025-2030 年)的複合年成長率為 2.62%。

主要亮點

- 市場成長的擴大得益於消費者對包裝食品的高度依賴以及食品加工企業強大的區域影響力。隨著越來越多的食品服務者成功實現業務數位化,線上食品訂購需求的不斷成長預計將振興該行業,為北美創造市場成長機會。

- 過去十年,由於基材選擇的變化、新市場的擴張、所有權的動態以及瓦楞紙箱、紙箱和塑膠包裝市場的眾多發展,北美食品服務包裝業務一直經歷著持續的成長。尤其是在美國,永續性和環境問題仍然是優先事項。

- 瓦楞紙箱是用於運輸各種食品的一種產品類型。它們通常由紙板製成,紙板主要由木材中的纖維素纖維製成。這些盒子堅固、剛性、靈活、耐用、輕巧且美觀。它還是環保的,因為它可回收並且在生產過程中不使用有害化學物質。瓦楞紙箱用於北美食品服務業包裝產品。 寶特瓶包裝是聚乙烯的主要用途。聚乙烯是一種半結晶質、輕質熱塑性樹脂,具有優異的隔音性能、耐化學性和低吸濕性。

- 該行業最大的擔憂是該地區嚴格的環境法規。預計在預測期內,國家和州一級禁止使用塑膠製品將對該行業構成重大挑戰。此外,由於宏觀經濟因素導致的原料價格上漲和聚合物樹脂供應鏈的不確定性可能會對預測期內的市場成長構成挑戰。

- 餐飲業的利潤率受到了新冠肺炎疫情的嚴重影響。該行業內的公司已經看到消費量大幅下降,並伴隨供應鏈中斷。受新冠疫情影響,美國餐飲業停業嚴重,導致包裝食品銷售暫時下降,但儘管面臨經濟挑戰,該產業已逐步復甦。預計疫情過後,有限服務餐廳和全方位服務餐廳將增加面向消費者的包裝。隨著經濟重新開放和消費者養成新的飲食習慣,食品包裝必須適應這些不斷變化的需求,從而推動市場成長。

北美食品服務包裝市場趨勢

瓦楞紙箱和紙盒板塊成長最快

- 瓦楞紙箱僅使用一次然後回收,最大限度地減少了交叉污染的風險。此外,生產過程中採用的高溫可確保其不含細菌和其他污染物。由於它為食品在運輸、儲存和分銷過程中提供了一個清潔、安全的環境,因此它在北美食品服務包裝市場的採用正在加速。

- 瓦楞紙箱以其安全性而聞名,並被批准可以直接接觸食物。此外,這些盒子可以塗上食品安全材料,使其成為更具吸引力的食品包裝。食品安全塗層的一個標準選擇是符合直接食品接觸監管標準的水性或植物性塗層。該塗層可充當保護層,並可防止盒子中的物質潛在地遷移到食物中。它們無毒、防潮,旨在確保包裝保持完好且食品安全,支持其在研究市場中的成長。

- 永續性在所有行業中發揮關鍵作用,包括食品包裝。瓦楞紙箱在這方面得分很高,因為它們是由可再生資源製成的。大多數瓦楞紙箱都是用可回收材料製成的,易於重複使用,支持循環經濟並減少環境影響,從而支持預測期內北美市場的成長。

- 根據美國紙漿和造紙公司國際紙業公司的報告,美國瓦楞包裝的出貨量隨著該國包裝產品出貨量的增加而增加,這表明該領域在所研究市場中的未來成長潛力。

- 此外,瓦楞紙箱和紙板的堅固結構、多功能性和安全性使其成為食品包裝的首選。它們保護和保存裡面的食物並確保其安全地運送到消費者手中。瓦楞紙箱加上其永續的特性,是一種合適的雙贏解決方案,它將使食品業受益,並支持所研究市場中這一領域的成長。

快餐店佔最高市場佔有率

- 在 QSR 中使用永續食品服務包裝已變得至關重要。越來越多的人選擇速食作為晚餐,因為他們沒有時間在家做飯。餐飲企業可以使用永續的包裝方式來安全且經濟地包裝餐食,為顧客提供快速簡便的餐點運輸方式。

- 快餐店使用的大多數食品服務產品都是由塑膠製成的,例如發泡聚苯乙烯 (EPS)、聚對苯二甲酸乙二醇酯 (PET)、聚丙烯 (PP) 和聚乳酸,或由紙、紙板和模製紙漿製成。與傳統餐廳或咖啡館相比,QSR 能夠更快地提供更高品質的食品和飲料。為了確保公平分配和提供這些服務的高度一致性,一些快餐店引入了分配控制份量的分配器,以支持市場的成長。

- 一些 QSR 將餐廳的便利性與顧客透過容量控制分配器的自助服務自由結合起來,幫助 QSR 提供卓越的客戶服務,消除產品浪費並降低成本。該地區的 QSR 對這些小袋和小包的包裝解決方案的需求不斷增加,預計將在預測期內為市場創造成長機會。

- 美國的速食和 QSR 連鎖店正在擴大其在加拿大的業務,以滿足日益成長的包裝食品需求,這將支持市場成長。例如,以漢堡和薯條聞名的美國速食連鎖店 Shake Shack 預計將於 2024 年 6 月在多倫多開設其第一家加拿大門市,預計將在預測期內推動食品服務業對包裝解決方案的需求。

- 此外,2023 年 8 月,上下文行動廣告公司 Inmobi 報告稱,越來越多的人選擇訂購披薩和漢堡作為美國最受歡迎的速食。這些因素可能會在預測期內創造該國食品服務包裝市場的需求並支持區域市場的成長。

北美食品服務包裝產業概況

預測期內,北美食品包裝市場高度分散,有 Inline Plastics、Berry Global Inc.、Novolex Holdings LLC、Genpak LLC 和 Huhtamaki America Inc. 等多家公司。該地區本地供應商之間的競爭正在加劇。食品服務包裝供應商範圍廣泛,買家可以從多個供應商中進行選擇。

- 2024 年 5 月-食品服務製造公司 Genpak 投資 2,280 萬美元對其位於阿拉巴馬州蒙哥馬利的工廠維修。此次升級將使工廠的當地員工數量增加一倍,升級重點包括增強安全性和提高製造商為便利商店到餐廳等廣泛客戶提供食品包裝解決方案的效率。

- 2024 年 4 月 - 北美公司 Novolex Holdings LLC 宣布對羅德島的可重複使用系統和容器品牌 OZZI 進行策略性投資。作為投資的一部分,Novolex 的業務部門和食品服務業循環解決方案的領導者 Eco Products 將加速 OZZI 的發展。 OZZI 系列產品和解決方案包括用於食品服務包裝的 O2GO 容器、杯子和刀叉餐具。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 美國對簡便食品的需求仍然很高

- 對永續性的日益關注促使供應商轉向再生塑膠

- 市場挑戰

- 環境壓力導致政府加強對包裝的監管,以及聚合物定價的不確定性

- 市場機會

- 產業生態系統分析 – 材料供應商、轉換器、經銷商、最終使用組織、客戶、回收商

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估微觀經濟因素對市場的影響

第5章 市場區隔

- 按包裝類型

- 瓦楞紙箱和紙箱

- 塑膠瓶

- 托盤、盤子、食品容器、碗

- 杯子和蓋子

- 泡殼

- 其他包裝形式(刀叉餐具、攪拌器/吸管等)

- 按最終用戶

- 速食店

- 全方位服務餐廳

- 咖啡和小吃

- 零售商

- 公共及款待

- 其他最終用戶

- 按國家

- 美國

- 加拿大

第6章 競爭格局

- 公司簡介

- Pactiv Evergreen Inc.

- Dart Container Corporation

- Amhil North America

- Genpak LLC

- Huhtamaki America Inc.

- Berry Global Inc.

- Inline Plastics

- Novolex Holdings LLC

- Sabert Corporation

- Silgan Plastic Food Container

- Bennett Plastics Inc.

- B&R Plastics Inc.(Gilster-Mary Lee Corp.)

- Graphic Packaging

- Amcor PLC

- Sonoco Products Company

第7章食品服務包裝產業經銷商及供應商名單

The North America Foodservice Packaging Market size is estimated at USD 26.24 billion in 2025, and is expected to reach USD 29.86 billion by 2030, at a CAGR of 2.62% during the forecast period (2025-2030).

Key Highlights

- The market's growth expansion has been brought on by consumers' heavy reliance on packaged foods and the significant regional presence of food processing businesses. The rising number of foodservice suppliers successfully digitalizing their operations is expected to fuel the industry, supported by the increasing demand for online food ordering, creating an opportunity for market growth in North America.

- The North American foodservice packaging business has experienced consistent growth over the last decade due to changes in substrate choice, new market expansion, ownership dynamics, and numerous developments serving the market for corrugated boxes, cartons, and plastic packaging. Sustainability and environmental issues will continue to be prioritized, especially in the United States.

- Corrugated boxes are types of packaging used to ship different food products. They are often constructed of paperboard, primarily made of cellulose fibers from wood. These boxes are strong, stiff, flexible, long-lasting, light, and attractive. Due to their recyclable nature and lack of use of hazardous chemicals during production, the boxes are advantageous for the environment. Corrugated boxes are used in the North American foodservice industry to package goods. Plastic bottle packing is the principal application for polyethylene. It is a semi-crystalline, lightweight thermoplastic resin with excellent sound insulation, chemical resistance, and low moisture absorption.

- The industry's most significant source of worry is the region's strict environmental restrictions. Over the projection period, bans on plastic items at the national and state levels are projected to present significant difficulties to the industry. Additionally, the growth of raw material prices and the supply chain uncertainty in polymer resins due to macroeconomic factors may challenge the market's growth during the forecast period.

- The foodservice industry's profit margins have been significantly affected by the COVID-19 pandemic. Businesses in this industry are witnessing a notable drop in consumption, coupled with disruptions in their supply chains. The COVID-19 pandemic-induced lockdowns substantially impacted the US foodservice industry with a temporary dip in packaging volumes, and the industry gradually recovered, defying economic challenges. Limited and full-service restaurants are expected to ramp up their consumer-facing packaging post-pandemic. As the economies reopen and diners embrace new eating habits, foodservice packaging must adapt to cater to these evolving needs, driving market growth.

North America Foodservice Packaging Market Trends

Corrugated Boxes and Cartons Segment to Exhibit the Highest Growth Rate

- Corrugated boxes are used only once and then recycled, minimizing the risk of cross-contamination. Additionally, the high heat used in manufacturing ensures they are free from bacteria and other contaminants. They provide a clean, safe environment for food items during transit, storage, and delivery, which is boosting their adoption in the foodservice packaging market in North America.

- Corrugated boxes boast a safety feature and are approved for direct food contact. Moreover, these boxes can be coated with food-safe materials, bolstering their appeal for food packaging. One standard option for a food-safe coating is a water-based or vegetable-based coating that complies with regulatory standards for direct food contact. This coating can be used as a protective layer, preventing any potential migration of substances from the box to the food. It is designed to be non-toxic and moisture-resistant, ensuring the packaging remains intact and safe for food items, supporting its growth in the market studied.

- Sustainability plays a crucial role in all industries, including food packaging. Corrugated boxes score highly in this regard as they are made from renewable resources. Most are manufactured from recycled materials and support circular economies as they can be easily recycled again, which reduces their environmental footprint, thereby supporting their growth in the North American market during the forecast period.

- The International Paper Company, a US-based pulp and paper company, reported the shipments of corrugated packaging in the United States to be growing in line with the increasing growth of shipments of packing products in the country, showing the future growth potential of the segment in the market studied.

- Additionally, with their sturdy construction, versatility, and safe properties, corrugated boxes and cartons have secured their place as a preferred choice in food packaging. They protect and preserve the food products inside and ensure their safe transportation to consumers. Coupled with their sustainable nature, corrugated boxes are a proper win-win solution, benefiting the food industry and supporting the segment's growth in the market studied.

Quick-service Restaurants Hold the Highest Market Share

- The use of sustainable foodservice packaging in QSRs has become crucial. More people are turning to fast food as a supper option because they have less time to prepare meals at home. Foodservice businesses may package meals safely and affordably using sustainable packaging styles, giving clients a quick and easy way to transport meals.

- Most of the foodservice items used in QSRs are either made of plastic, such as expanded polystyrene (EPS), polyethylene terephthalate (PET), polypropylene (PP), and polylactic acid, or paper, including paper, paperboard, and molded pulp. QSRs deliver high-quality food and beverages more quickly than traditional restaurants or cafes. To achieve fair distribution and a high level of consistency in offering these services, several QSRs have implemented dispensers that supply a controlled volume, supporting market growth.

- Some QSRs combine restaurant conveniences with the freedom for customers to express their uniqueness through self-service elements through controlled-volume dispensers, which can help QSRs deliver exceptional customer service, reduce product waste, and save money. The demand for packaging solutions for these small-volume sachets or packets across QSRs in the region is expected to create a growth opportunity for the market over the forecast period.

- Fast food and QSR chains based in the United States are expanding their portfolios in Canada to address the increasing demand for packaged foods, which would support market growth. For instance, in June 2024, the US fast-food chain Shake Shack, known for its burgers and fries, opened its first Canadian location in Toronto, which would fuel the demand for packaging solutions in the foodservice industry during the forecast period.

- Additionally, in August 2023, Inmobi, a contextual mobile advertising company, reported that people were ordering pizza and burgers as the most preferred fast food items in the United States. Such factors could create demand for the foodservice packaging market in the country and support the regional market's growth during the forecast period.

North America Foodservice Packaging Industry Overview

The North American foodservice packaging market will be highly fragmented over the forecast period, with the presence of many players, such as Inline Plastics, Berry Global Inc., Novolex Holdings LLC, Genpak LLC, and Huhtamaki America Inc. There will be increasing competition among local vendors in the region. Owing to the wide range of foodservice packaging suppliers, buyers can choose from multiple vendors.

- May 2024 - Foodservice manufacturing company Genpak invested USD 22.8 million in renovating its Montgomery, Alabama, plant. The upgrades allowed the facility to double its local workforce and included safety enhancements and upgrades focused on better efficiency for the manufacturer's food packaging solutions for clients ranging from convenience stores to restaurants.

- April 2024 - Novolex Holdings LLC, a North American company, announced a strategic investment in Rhode Island-based reusable systems and container brand OZZI. As a part of this investment, Eco-Products, a Novolex business unit and leader in circular solutions for the foodservice industry, will help accelerate OZZI's growth. The OZZI family of products and solutions includes O2GO containers, cups, and cutlery for foodservice packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Convenience Food Remains High in the United States

- 4.2.2 Increasing Emphasis on Sustainability is Causing Vendors to Focus on Recycled Plastic

- 4.3 Market Challenges

- 4.3.1 Increasing Governmental Regulations on Packaging Due to Environmental Pressure and Uncertainty in Polymer Prices

- 4.4 Market Opportunities

- 4.5 Industry Ecosystem Analysis - Material Suppliers, Convertors, Distributors, End-use Organizations, Customers, and Recycling

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET SEGMENTATION

- 5.1 By Packaging Format

- 5.1.1 Corrugated Boxes and Cartons

- 5.1.2 Plastic Bottles

- 5.1.3 Trays, Plates, Food Containers, and Bowls

- 5.1.4 Cups and Lids

- 5.1.5 Clamshells

- 5.1.6 Other Packaging Formats (Cutlery, Stirrers/Straws, etc.)

- 5.2 By End User

- 5.2.1 Quick-service Restaurants

- 5.2.2 Full-service Restaurants

- 5.2.3 Coffee and Snack Outlets

- 5.2.4 Retail Establishments

- 5.2.5 Institutions and Hospitality

- 5.2.6 Other End Users

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Pactiv Evergreen Inc.

- 6.1.2 Dart Container Corporation

- 6.1.3 Amhil North America

- 6.1.4 Genpak LLC

- 6.1.5 Huhtamaki America Inc.

- 6.1.6 Berry Global Inc.

- 6.1.7 Inline Plastics

- 6.1.8 Novolex Holdings LLC

- 6.1.9 Sabert Corporation

- 6.1.10 Silgan Plastic Food Container

- 6.1.11 Bennett Plastics Inc.

- 6.1.12 B&R Plastics Inc. (Gilster-Mary Lee Corp.)

- 6.1.13 Graphic Packaging

- 6.1.14 Amcor PLC

- 6.1.15 Sonoco Products Company

7 LIST OF PACKAGING DISTRIBUTORS AND SUPPLIERS IN THE FOODSERVICE PACKAGING INDUSTRY

食品服務包裝市場:按產品類型、包裝材料、製造流程、應用和最終用戶 - 2025-2030 年全球預測

食品服務包裝市場:按產品類型、包裝材料、製造流程、應用和最終用戶 - 2025-2030 年全球預測 可重複使用食品服務包裝的全球市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

可重複使用食品服務包裝的全球市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029) 全球紡織食品服務包裝市場的未來(~2029)2024-2032 年按產品類型(容器、盤子、碗、杯子等)、材料(塑膠、紙和紙板、鋁等)和地區分類的線上食品配送包裝市場報告食品服務包裝 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)

全球紡織食品服務包裝市場的未來(~2029)2024-2032 年按產品類型(容器、盤子、碗、杯子等)、材料(塑膠、紙和紙板、鋁等)和地區分類的線上食品配送包裝市場報告食品服務包裝 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029) 2023 年至 2028 年食品服務包裝市場預測

2023 年至 2028 年食品服務包裝市場預測 美國咖啡店和小吃店用拋棄式包裝和服務用品市場美國紙質食品服務包裝和用品市場

美國咖啡店和小吃店用拋棄式包裝和服務用品市場美國紙質食品服務包裝和用品市場