|

市場調查報告書

商品編碼

1665271

衛星模擬器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Satellite Simulator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

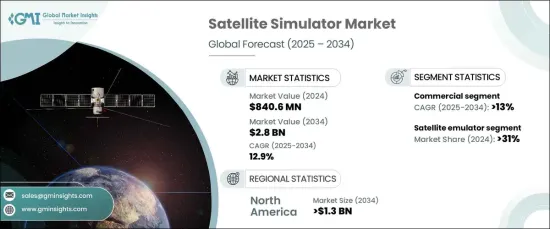

2024 年全球衛星模擬器市場規模達到 8.406 億美元,預計 2025 年至 2034 年期間將以 12.9% 的強勁複合年成長率擴張。衛星模擬器透過提供真實的訓練環境、嚴格的系統測試和全面的驗證,在確保任務準備就緒方面發揮關鍵作用。這些工具不僅可以降低與衛星即時運行相關的成本和風險,還可以提高運作效率和確保通訊網路安全。國防機構始終依賴模擬系統來最佳化設備性能、改善人員培訓並為多樣化的任務場景做好準備。

衛星模擬器市場依類型分為電池模擬器、網路模擬器、雷達模擬器、衛星模擬器、訊號調節系統和太陽能模擬器。其中,衛星模擬器在2024年佔據了31%的市場佔有率,預計在預測期內將大幅成長。現代衛星系統日益複雜,增加了精確模擬的需求。衛星模擬器使組織能夠在衛星發射之前評估性能、驗證系統彈性並改進設計,確保任務成功並減少誤差。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 8.406 億美元 |

| 預測值 | 28億美元 |

| 複合年成長率 | 12.9% |

根據應用,衛星模擬器市場服務於軍事和國防部門以及商業行業。到 2034 年,商業領域預計將以驚人的 13% 的複合年成長率成長,這得益於電信、廣播和全球連接對衛星服務的日益依賴。公司正在大力投資模擬技術,以便在真實條件下嚴格測試衛星通訊鏈路、有效載荷和網路。這些模擬器有助於最大限度地降低操作風險,提高系統性能,並確保無縫驗證過程,支援商業衛星應用中模擬工具的日益普及。

北美衛星模擬器市場規模預計在 2034 年達到 13 億美元,由於太空技術的進步和致力於衛星開發的政府組織的強大影響力,其將繼續保持主導地位。美國國家航空暨太空總署和國防部等機構正在積極投資先進的衛星測試和訓練解決方案,以準確複製太空環境。這種需求在軍事和國防應用中尤其明顯,因為精度和可靠性對於這些應用至關重要。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 大型衛星星座快速發展與部署

- 太空探索和國防投資不斷增加

- 衛星模擬器中人工智慧(AI)和機器學習的融合日益加深

- 基於雲端的衛星模擬器的採用日益廣泛

- 對強化培訓項目的需求不斷成長

- 產業陷阱與挑戰

- 初期投資及維護成本高

- 模擬不同衛星系統的複雜性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 電池模擬器

- 網路模擬器

- 雷達模擬器

- 衛星模擬器

- 訊號調節系統

- 太陽光模擬

第6章:市場估計與預測:依組件,2021-2034 年

- 主要趨勢

- 模擬器內核

- 模擬器

- 太空船模組

- 地面模組

- 環境模組

- 動態模組

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 軍事與國防

- 商業的

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Anritsu

- Atlantic Microwave

- GMV

- Hollis Electronics

- IFEN GmbH

- Indra

- Keysight Technologies

- Kratos

- Mitre

- NGC Aerospace

- Orolia

- Rohde & Schwarz

- Spectratime

- Spirent Communications

- Syntony

- Tampa Microwave

- Terma

- Thales

- VIAVI Solutions

The Global Satellite Simulator Market reached USD 840.6 million in 2024 and is projected to expand at a robust CAGR of 12.9% between 2025 and 2034. The increasing demand for advanced satellite communication systems in military and government sectors is driving the adoption of cutting-edge simulation technologies. Satellite simulators are pivotal in ensuring mission readiness by providing realistic training environments, rigorous system testing, and comprehensive validation. These tools not only reduce costs and mitigate risks associated with live satellite operations but also enhance operational efficiency and secure communication networks. Defense agencies consistently rely on simulation systems to optimize equipment performance, improve personnel training, and prepare for diverse mission scenarios.

The satellite simulator market is categorized by type into battery simulators, network simulators, radar simulators, satellite emulators, signal conditioning systems, and solar simulators. Among these, satellite emulators accounted for 31% of the market share in 2024 and are expected to grow significantly during the forecast period. The increasing complexity of modern satellite systems has amplified the need for precise simulations. Satellite emulators enable organizations to evaluate performance, validate system resilience, and refine designs before satellite launches, ensuring successful missions and reducing the margin for error.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $840.6 Million |

| Forecast Value | $2.8 Billion |

| CAGR | 12.9% |

By application, the satellite simulator market serves the military and defense sectors as well as commercial industries. The commercial segment is projected to grow at an impressive CAGR of 13% through 2034, driven by the growing reliance on satellite services for telecommunications, broadcasting, and global connectivity. Companies are heavily investing in simulation technologies to rigorously test satellite communication links, payloads, and networks under realistic conditions. These simulators help minimize operational risks, improve system performance, and ensure seamless verification processes, supporting the rising adoption of simulation tools in commercial satellite applications.

North America satellite simulator market is poised to reach USD 1.3 billion by 2034, maintaining its dominance due to advancements in space technologies and a strong presence of government organizations dedicated to satellite development. Agencies such as NASA and the Department of Defense are actively investing in advanced satellite testing and training solutions to accurately replicate space environments. This demand is particularly pronounced in military and defense applications, where precision and reliability are mission-critical.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rapid development and deployment of large-scale satellite constellations

- 3.6.1.2 Rising space exploration and defense investments

- 3.6.1.3 Growing integration of Artificial Intelligence (AI) and machine learning in satellite simulators

- 3.6.1.4 Increasing adoption of cloud-based satellite simulators

- 3.6.1.5 Rising demand for enhanced training programs

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment and maintenance costs

- 3.6.2.2 Complexity in simulating diverse satellite systems

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Battery simulator

- 5.3 Network simulator

- 5.4 Radar simulator

- 5.5 Satellite emulator

- 5.6 Signal conditioning systems

- 5.7 Solar simulation

Chapter 6 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Simulator kernel

- 6.3 Emulator

- 6.4 Spacecraft modules

- 6.5 Ground modules

- 6.6 Environment modules

- 6.7 Dynamic modules

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Military & defense

- 7.3 Commercial

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anritsu

- 9.2 Atlantic Microwave

- 9.3 GMV

- 9.4 Hollis Electronics

- 9.5 IFEN GmbH

- 9.6 Indra

- 9.7 Keysight Technologies

- 9.8 Kratos

- 9.9 Mitre

- 9.10 NGC Aerospace

- 9.11 Orolia

- 9.12 Rohde & Schwarz

- 9.13 Spectratime

- 9.14 Spirent Communications

- 9.15 Syntony

- 9.16 Tampa Microwave

- 9.17 Terma

- 9.18 Thales

- 9.19 VIAVI Solutions

2025 年全球航太和國防零件市場報告

2025 年全球航太和國防零件市場報告 航太和國防領域的 5G 市場:按通訊基礎設施、工作頻率、核心網路技術和最終應用分類 - 2025-2030 年全球預測

航太和國防領域的 5G 市場:按通訊基礎設施、工作頻率、核心網路技術和最終應用分類 - 2025-2030 年全球預測 全球防禦複合材料市場(2024-2034)

全球防禦複合材料市場(2024-2034) 航空航天:訂閱競爭和市場情報

航空航天:訂閱競爭和市場情報 Market Forecast:年度訂閱服務

Market Forecast:年度訂閱服務