|

市場調查報告書

商品編碼

1665319

感應馬達市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Induction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

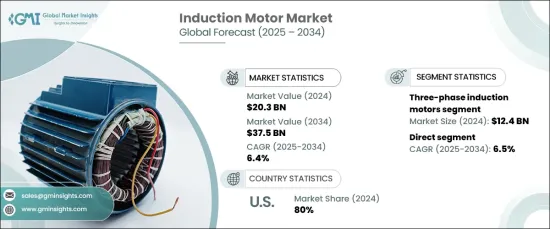

全球感應馬達市場預計在 2024 年達到 203 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.4%。它們對於為製造環境中使用的機械(例如傳送帶、機器人系統和自動化機械)提供精確控制至關重要。

擴大採用工業自動化來提高生產力並降低勞動力成本是市場成長的主要動力。感應馬達廣泛應用於機器人和自動導引車(AGV)等領域,尤其是製造業、物流、倉儲和醫療保健等產業。這些馬達因其提供恆定速度和可靠扭矩的能力而受到高度重視,使其成為需要不間斷運行的高性能應用的理想選擇。此外,人們對能源效率的日益重視導致對節能馬達的需求激增,這支持了永續的工業實踐。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 203億美元 |

| 預測值 | 375億美元 |

| 複合年成長率 | 6.4% |

市場依產品類型分為單相和三相感應馬達。三相部分引領市場,2024 年創造 124 億美元的收入。自動化和快速工業化的不斷推進進一步刺激了製造過程中對這些強勁馬達的需求。

在分銷通路方面,市場分為直接銷售和間接銷售。直銷領域佔據主導地位,到 2024 年將佔據總市場佔有率的 65.8%,預計在預測期內複合年成長率為 6.5%。隨著各行各業對客製化、高效解決方案的需求日益成長,直銷管道因其能夠提供更快、更透明的交易而受到青睞。線上銷售平台的整合進一步提高了客戶參與度,使購買流程更加便利和簡化。

2024 年,美國感應馬達市場佔有 80% 的佔有率,預計 2025 年至 2034 年期間的複合年成長率為 6.4%。汽車、化學加工和食品生產等行業正在整合先進的系統以提高生產力同時降低營運成本。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 提高工業自動化程度

- 對節能解決方案的需求不斷成長

- 電動車(EV)市場的擴張

- 產業陷阱與挑戰

- 節能馬達的初始成本較高

- 維護和營運挑戰

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:感應馬達市場估計與預測:依產品類型,2021-2034 年

- 主要趨勢

- 單相感應電動機

- 分階段

- 電容啟動

- 電容運行

- 蔭蔽柱

- 三相感應電動機

- 鼠籠電動機

- 滑環電機

第 6 章:感應馬達市場估計與預測:按應用,2021-2034 年

- 主要趨勢

- 家用電器

- 商業電器

- 工業應用

第 7 章:感應馬達市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直接的

- 間接

第 8 章:感應馬達市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- ABB

- Allied Motion Technologies

- AMETEK

- Emerson

- Hitachi

- Johnson Electric

- Mitsubishi

- Nidec

- Oriental Motor

- Regal Rexnord

- Rockwell Automation

- Schneider Electric

- Siemens

- Toshiba

- WEG Electric

The Global Induction Motor Market is on track to reach USD 20.3 billion by 2024 and is projected to expand at a CAGR of 6.4% from 2025 to 2034. Renowned for their durability, efficiency, and versatility, induction motors play a crucial role in powering automated production lines. They are integral in providing precise control for machinery used in manufacturing environments, such as conveyors, robotic systems, and automated machinery.

The increasing adoption of industrial automation to enhance productivity and reduce labor costs is a primary driver of market growth. Induction motors are widely utilized in sectors like robotics and automated guided vehicles (AGVs), particularly in industries such as manufacturing, logistics, warehousing, and healthcare. These motors are highly valued for their ability to deliver consistent speed and reliable torque, making them ideal for high-performance applications that require uninterrupted operation. Additionally, the growing emphasis on energy efficiency has led to a surge in demand for energy-saving motors, which supports sustainable industrial practices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.3 Billion |

| Forecast Value | $37.5 Billion |

| CAGR | 6.4% |

The market is divided by product type into single-phase and three-phase induction motors. The three-phase segment leads the market, generating USD 12.4 billion in revenue in 2024. This segment is expected to grow at a CAGR of 6.5% through 2034, driven by its widespread use in industrial applications requiring high efficiency and the ability to handle heavy loads, such as pumps, compressors, and conveyor systems. The increasing shift toward automation and rapid industrialization further fuels the demand for these robust motors in manufacturing processes.

In terms of distribution channels, the market is split between direct and indirect sales. The direct sales segment dominates, accounting for 65.8% of the total market share in 2024, and is expected to experience a CAGR of 6.5% during the forecast period. As industries increasingly demand customized, high-efficiency solutions, the preference for direct sales channels continues to rise, thanks to their ability to provide faster, more transparent transactions. The integration of online sales platforms is further improving customer engagement, making the purchasing process more accessible and streamlined.

The U.S. induction motor market held an 80% share in 2024 and is projected to grow at a CAGR of 6.4% from 2025 to 2034. This growth is fueled by the increasing emphasis on industrial automation, energy efficiency, and modernization within various sectors. Industries such as automotive, chemical processing, and food production are integrating advanced systems to boost productivity while reducing operational costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing industrial automation

- 3.6.1.2 Rising demand for energy-efficient solutions

- 3.6.1.3 Expansion of the electric vehicle (EV) market

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial cost for energy-efficient motors

- 3.6.2.2 Maintenance and operational challenges

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Induction Motor Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Single-phase induction motors

- 5.2.1 Split phase

- 5.2.2 Capacitor-start

- 5.2.3 Capacitor-run

- 5.2.4 Shaded pole

- 5.3 Three-phase induction motors

- 5.3.1 Squirrel cage motors

- 5.3.2 Slip ring motors

Chapter 6 Induction Motor Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Household appliances

- 6.3 Commercial appliances

- 6.4 Industrial applications

Chapter 7 Induction Motor Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Induction Motor Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Allied Motion Technologies

- 9.3 AMETEK

- 9.4 Emerson

- 9.5 Hitachi

- 9.6 Johnson Electric

- 9.7 Mitsubishi

- 9.8 Nidec

- 9.9 Oriental Motor

- 9.10 Regal Rexnord

- 9.11 Rockwell Automation

- 9.12 Schneider Electric

- 9.13 Siemens

- 9.14 Toshiba

- 9.15 WEG Electric

北美低壓感應馬達:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

北美低壓感應馬達:市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 感應馬達市場規模、佔有率、趨勢及預測(按產品類型、最終用途領域及地區分類)2025-2033亞太地區感應電動機:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲感應電動機:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)感應電動機市場:按產品類型、應用分類 - 2025-2030 年全球預測

感應馬達市場規模、佔有率、趨勢及預測(按產品類型、最終用途領域及地區分類)2025-2033亞太地區感應電動機:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)北美感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)感應馬達:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲感應電動機:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)感應電動機市場:按產品類型、應用分類 - 2025-2030 年全球預測 全球感應馬達市場 - 2024 - 2031

全球感應馬達市場 - 2024 - 2031 感應電動機市場 - 2024 年至 2029 年預測

感應電動機市場 - 2024 年至 2029 年預測